In many ways, it was a quiet week for news. However, we still managed to keep ourselves entertained. On Monday night, Mark hosted an Investment Mistakes panel at the Mello Monday online investor event, and Leo joined as a panellist along with well-known Twitterati Reb & James. Do check it out if you haven’t yet caught the session.

A reminder that to see the full LCL & scl sessions you will need to be a ‘member’ of the discord server. This is free and easy to access, so if you don’t already have it then here is an invite. Links will usually go to the browser version. So if you are a member with the app installed putting the company ticker into the search bar to find the section may be the easiest option for you.

Large Caps Live Monday 12th April

On LCL, Wayne admitted to turning increasingly bearish on the US, despite indices hitting all-time highs:

1. There is a hell of a lot of liquidity

2. But it is not clear what the unemployment situation is

3. The 'balance' sheet of the average consumer is probably both directly and indirectly dependent on property prices - but they are not 'revalued' every minute of every day .

4. That a lot of cash may be due to furlough, govt handouts and remortgaging but not actually a sign of wealth

This is market breadth:

1. We have had massive flows into the markets as there is not a lot else for a lot of people to do either with their time or their money

2. As we open up - both the UK and the US - that changes

3. The rest of the world will gradually open up over TIME - ie not everyone will open up at the same time

4. That latter point is crucial - as I think some inflation expectations are anchored on massive synchronised global demand

5. The middle classes have - interestingly shrunk in a number of countries during Covid (ie some people due to job loss or financial issues are no longer classified as middle class)

6. Over the next 12 months the remaining owners of productive capacity or retailers (eg hairdressers, retailers etc) will invest in their business with their surplus cash

7. There will be a burst of rent collections

8. And some defaults/evictions and people's mobility will increase

9. But short term market pricing depends on FLOWS - and all the above moves flows AWAY from the market into the real economy.

We started looking at this niche supplier of flavourings.

“Highlights

Strong performance across all categories with revenue expected to grow by 14% to approximately £60.8m (H1 2020: £53.6m).

Growth particularly strong in tea, health & wellness and fruit & vegetables categories meeting growing global consumer demand for healthier living.

Gross margin improvements reflect the growth of the above categories and the transition into more sophisticated, solution-driven products in citrus.

New, state-of-the-art, UK headquarters opening April 2021 with colleagues beginning to transition on a phased basis, which, along with the recently expanded US facility, ensures the Group is well-positioned for future growth.

Trading in line with the Board's revised expectations as announced in January 2021.”

At the end of the day, this is an in line statement, for a company that is on a forward P/E of 44 that in the past has struggled to grow its topline and has generated barely acceptable ROCE. There is a strong argument that they will be doing better than their historical performance going forward and this trading statement we see some signs of that, but it is hard to argue that a forward P/E of 44 doesn't already price this level of growth, and then some. In the current market, people forget what levels of growth it requires to justify these sort of ratings.

Interestingly, paid-for research from broker Edison says:

We value Treatt using a DCF model, which indicates a fair value of 870p.

A lot has been written about Revolution Bars Group over the years. Despite numerous challenges, not least the closure of all of their sites due to COVID-19 restrictions, they have retained an almost fanatical following in some quarters. So what more can we add to the narrative? Perhaps nothing. But as an investor, it is the figures that talk loudest. And for these, I turn to the balance sheet of this week’s interim results.

A current ratio of just 0.5 at 26th December 2020 suggests some distress. Although they have already operated with negative working capital, a further 4 months of site closures will not have improved this. With lease liabilities exceeding lease assets by c.£36m, despite a CVA and other rent negotiations, this gives negative equity.

Net debt is given as £21m, but since then has increased to £30.8m:

“Additionally, in April 2021, NatWest approved a further £3.5 million CLBILS taking committed total facilities to £40.3 million as at the date of these interim financial statements. As such, as at the date of these interim financial statements the Group's net bank debt was approximately £30.8 million, and therefore the Group has available liquidity of £9.5 million.”

Using CLBILS loans, a CVA & equity raise has kept them going, but debt is likely to peak around £40m. Combined with the low current ratio, unless they raise a lot more equity from the market soon, this is not an investment IMO. And I can't believe that the lenders & landlords are taking this much risk without a plan to push for a further recapitalisation at the right time.

Leo commented on this worrying statement from last week:

“In the full year trading update announced on 29 January 2021, Novacyt explained it was in active discussions with the DHSC regarding an extension of the supply contract. Unfortunately, an extension has not been agreed, although the Company supplied PROmate™ in Q1 2021 in accordance with DHSC demand. Regrettably, the parties are now in dispute regarding the contract, which may have a material impact on Q4 2020 revenues. However, the Company has taken legal advice and believes it has strong grounds to assert its contractual rights.”

We have already reported here that this contract was in trouble and unlikely to be extended. Near-patient PCR testing just never got off the ground and has been made obsolete by centralised testing finally getting their act together and lateral flow testing proving more reliable than originally feared. Also, lateral flow testing is much better at discriminating between potentially infectious cases and those where the person has just been exposed than PCR testing as practiced in the UK.

But there's a big difference between contracts not being extended and being in dispute. Especially when approximately 50% of Q1 revenue was driven by sales to the DHSC.So what is going on here?One possibility is that Novacyt have screwed up.Another is that the DHSC have screwed up and are blaming Novacyt to save face.Whatever the truth, this is not a good look for other potential clients.

What I suspect has mainly happened here is that the balance of power has changed - in March - June last year the government was desperate for PCR consumables and most suppliers were short.Now there is plenty of supply and a company with 50% of its revenues coming from a single source is in danger of getting bullied.

So, clearly bad news, but what is Novacyt now worth?In the FY 2020 (to Dec 31st) trading statement, they said they had cash of £91m.The conversion from revenue to cash was about 1/3rd.So perhaps now they have £115m cash.That puts some floor under the share price, with a current market cap of £310m.

If they fall to £250m market cap then I will certainly be doing some more detailed modelling.The trouble is of course that the past is very little guide to the future here.

Mark took a look at another well-followed micro-cap following its trading update:

Given the level of closures then it is not surprising that store sales are down 82%. However, they seem to be in completely the wrong segment with their online sales almost halving despite online going great guns everywhere else.And the company was struggling even before being covided, with 2020 revenues down on 2019. The market is clearly pricing this as a recovery stock with the share price up 50% in 2021 despite these results.

One of the most compelling arguments for buying Quiz in the past was that you were getting it at a significant discount to cash and inventory. However, that argument appears to have gone out of the window:

“Despite this drop in revenues in the year, reflecting tight cost control, the Group has retained a net cash balance of £1.5 million at 31 March 2021 (comprising a cash balance of £4.2 million offset by a £2.7 million drawdown of available bank facilities).”

This is down from £5.5m at the half-year.

With Debenhams gone then web sales & concessions will face a headwind into 2022, although the company say that these had already declined that they are unlikely to be material.Like so many other stocks, the market appears to be pricing in a recovery and then some. The share price today is not far off where it was in 2019, and the EV is above that level. I think the company will do well for a couple of months post-lockdown, but it is hard to argue the long-term outlook for them is better than it was a few years back, which is what the market is pricing now.

Annual Reports

Finally, Leo followed up with some details gleaned from the Annual Reports of Mpac and Cenkos. Do check them out on the scl server if you have a particular interest in these companies.

Leo cycled back to take a look at results that were released earlier in the week from this supplier of high-end carbon fibre brake discs:

Last year I wrote up Surface Transforms for another publication. As usual, I didn't have much of a view on the company before I started writing, but by the time I'd finished my major issue was that they were a serial disappointer, as demonstrated by this graph:

But it was certainly a good story and long-suffering investors dreams came true in September with this contract award.

“The lifetime revenue on this specific vehicle model contract, commencing in the summer of 2021, is estimated to be approximately £27.5m.”

Broker forecasts from FY 22 jumped from revenues of £5.8m (and surely due to be lower based on past performance) to £12.5m, with EPS up from zero to 1.7p. As it turns out the September announcement would have been a great time to buy. Even if you didn't get the right price on the day, further contracts were won and the share price has done well over the months since.

So, on to this week’s announcement:

“Revenues stable at £1,952k (Year to 31 December 2019*: £1,938k) (7 months to 31 December 2019: £1,451k).”

Doesn't sound very special.

“Gross margin increased to 67.1% (Year to 31 December 2019*: 59.5%) (7 months to 31 December 2019: 59.6%).”

Much more important. Adds evidence they are not a cheaper / inferior alternative to competitor Brembo.

“Net research costs of £2,468k (Year to 31 December 2019: £2,437k) (7 months to 31 December 2019 £1,502k) after capitalising £141k (Year/7 months to December 2019: Nil) of gross expenditure. Research costs partially offset by an accrued R&D tax credit of £600k (Year to 31 December 2019*: £1,131k** reflecting 19 months tax credit in FY19)”

For me, R&D tax credits are a red flag second only to companies being run by academics. Still, this is a substantial amount of money and hopefully, the work bidding for it and the conditions didn't distract them too much.

What I think is telling however is the broker forecasts. But look at the FY 2021 trend:

In conclusion: I should have continued watching this and bought on the September announcement at a reasonable price. Yes it is overvalued, but so are a lot of things.The next milestone will be this “profitable and generating cash from operations on a monthly basis in the second half of 2021”.Unfortunately that might prove a trigger for the market to value on a P/E basis...

We looked at the Q1 results from this company that was the subject of our last Small Caps Life long-form write up.

Leo pointed out that this was a small miss compared to Tamesis Q1 forecasts:

He didn’t think this was important though:

The fact the share price was so low and that it went up on the update demonstrates that many didn't believe the forecasts anyway. My view here is that fleet utilisation is the most important thing in the short term. We won't know for certain for years what return they will get from new rigs and new bulldozers, but increased utilisation of existing rigs is money in shareholders pockets.

Mark then went into some of the details;

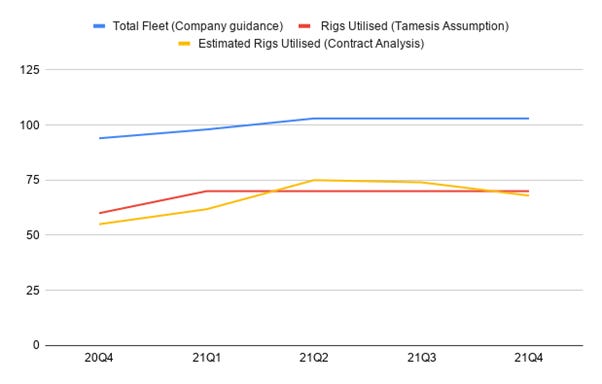

Average utilised rigs was slightly behind the graph I had produced from known contracts:

However, what I was predicting was rigs in use at the end of the quarter which is obviously not what they report & book revenue on. Given the rapid increase in rig numbers then I’ve adapted this to be more granular when contracts are starting. (The effect is to shift the demand out into the future.):

The fleet hasn’t grown as fast as I or Tamesis had expected either, and I think this is just the time taken to deploy new rigs into the Sukari & Geita mines. The good news is that these will be fully utilised as soon as they are commissioned.

As Leo said it was particularly pleasing to see the ARPOR (average revenue per operating rig) rising. Especially since some recent contract wins are underground rigs which command lower ARPOR (but higher margins so are roughly equal in profitability.)The company ARPOR is one area that my understanding has developed much more over time. You would think that this was simply supply & demand related pricing. However, the negotiated price is only a small part of what impacts ARPOR.They talk of contracts 'maturing' to generate higher ARPOR - crews get used to the type of material they are drilling through, ground conditions etc. and become more efficient over time, which drives the higher ARPOR. I think for a lot of contracts they are getting paid on metres drilled and samples collected, not simply a daily rate.Moves from single to double-shift operations has probably the biggest positive impact since they are getting double the output from the same rig.

Despite not quite hitting Tamesis Q1 revenue estimate, running the numbers from known contract starts, I think you'd have to make some fairly pessimistic assumptions to see anything other than the top end of the range of revenue for 2021.I get a forecast of $194m revenue for FY21 based on the number of rigs currently contracted.Plus the same mining services revenue as Q1 plus some growth in MSLABS.So this assumes no more contract wins, no further increase & no increase in revenue booked from Sukari in 2021.

Given the ability for everything in this region to take a bit longer than you think, I don't think they will update guidance until we are further into the year and all the new contracts are performing to plan.Tamesis, however, are currently forecasting the bottom of the guidance range for revenue, so if/when the guidance upgrade comes from the company it is likely that Tamesis will have to make significant upside revisions.

I think the ARPOR is the one to watch. Tamesis have 175k x 70 rigs = $147m + $39.7m mining services. By my calcs the 70 rigs average is slightly light but if the ARPOR can grow further this will be where the real beat will happen.

It was a quiet end to the week news-wise so we called it there. Have a great weekend everyone!