Drilling into Capital Limited

Could an upcoming results statement finally lead to a re-rating?

Summary

Capital Limited (CAPD.L), formerly Capital Drilling, is forecast by broker Tamesis Partners to grow underlying earnings per share at over 50% compound over the next two years.

Our analysis of publicly announced contract wins combined with the industry-wide outlook statements back up these forecasts as reasonable.

Despite this exceptional growth rate, the company trades on a single-digit forward P/E ratio. Although the company operates in a cyclical industry, an increasing number of long-term contracts give greater forward earnings visibility.

Persistent share sales into the market from a former director over the last few years and more recently an overhang from one or more funds leaves the company 'bewilderingly undervalued' according to Tamesis. An assessment we largely agree with.

The 2020 full-year results and 2021 outlook scheduled for Thursday (18 March 2021) could provide the trigger for the valuation to re-rate.

Sources of Alpha

Our first Small Caps Life write-up ended having to be re-written the day before publishing as the company themselves issued an unscheduled trading statement which removed quite a bit of our informational advantage!

So, for this second article, we've decided to focus on something where the likely news cycle is known. In its Q4 trading statement, Capital said:

2021 guidance is to be announced on 18 March 2021, alongside the Group's full year results and together with any dividend declarations.

The 2020 results are unlikely to contain surprises since the company provides quarterly operational updates, and the business model is relatively simple: the company provides drilling rigs to the mining industry and associated mining services. The Q4 trading statement had Full Year revenue of USD135m, bang in the middle of the guidance range. So, what is our edge? Simply that the current valuation anomaly appears to be so great that it must correct, one way or another.

Sources of investment alpha are usually categorised as:

Informational: knowing something other market participants don't;

Analytical: having a better model than other investors; or

Behavioural: acting more rationally than other investors.

So, it seems our advantage with finnCap was actually an analytical one since most of the information about its trading was available from a source that UK investors use every day: the Regulatory News Service. Despite this, it seems the majority of market participants hadn't done the analysis we had and that led to an opportunity to generate alpha.

For Capital, we believe our primary source of alpha is not informational or analytical but behavioural. Good forecasts are publicly available through broker research, but the company's improving outlook over the last six months or so has not been reflected in the market price. The investment opportunity lies with this gap closing, so in this case, it is patience that may generate alpha.

Let's start by looking at that broker coverage.

Broker Coverage

Capital has three brokers notes written about the company. Those by Berenberg and Peel Hunt are not available to mere mortals such as us. However, Tamesis Partners' note is available to all sufficiently experienced investors.

The last note, written on 14 January 2021 with the share price at 62p per share, gives the opinion that the shares are 'bewilderingly undervalued'. With the price still just above 60p to buy on most days, this is a sentiment we agree with.

Tamesis has increased its EBITDA estimates for 2021 by over 25% since August 2020, as the outlook for mining services has improved significantly. Yet over this period, the share price has dropped by almost 20%. With further growth forecast into 2022, the shares currently trade at 2.6x 2021 and 1.9x 2022 EBITDA Tamesis’s estimates. Although this is a capital intensive industry, the company generated an 18% ROCE in 2019 indicating that capital investments generate an acceptable return.

The market may have ascribed such a low forward valuation multiple to the company because most investors don't believe the forecasts. Alternatively, it may be that the location of the company's assets in a variety of African countries also makes most investors uneasy. However, this is hardly a market where most investors are focusing on the risks of equity investments. At the moment, many stock moves are driven by momentum not fundamentals.

Although we are not going to engage in a rant on current market conditions, Cliff Asness recently did a study looking at the power that knowing future earnings would do for investor returns. This study contained explicit cheating: it didn't use forecasted earnings but looked at what would happen if you knew the actual future earnings a reporting period ahead. Of course, over the long term, knowing future earnings generated exceptional investment results. However, there were two years where knowing future earnings led to very poor returns: 1999 and 2020. In those years, it appears that something other than earnings performance drove returns. Make of that what you will.

So, back to Capital - we think it isn't going up simply because it isn't going up. Part of this has been due to some persistent sellers. One of Capital’s founders, Craig Burton, has been reducing his stake for a couple of years.

In previous periods, he had engaged Tamesis & Peel Hunt to place the shares in blocks. However, over the last year, he appears to have consistently dripped shares into the market. He went below the 3% notifiable threshold on 18 September 2020. Given the recent volumes, we expect he is no longer a holder.

Sustainable Capital declared that they had reduced from 5.63% to a 2.11% holding on 11 February 2021. The presumption here is that they will continue to sell down to zero.

Why these holders didn't sell as a block trade, no one knows. There was significant demand for the stock at 58p in a recent placing, so much so that the placing was increased in size, and even then, there was a significant scale-back of allocations.

It is also possible that some holders bid for stock in the placing with the intention of 'flipping' the stock into the market. However, Capital is not the most liquid of stocks, so this wouldn't have been my first choice to play this game. Whatever the cause of these overhangs, they have enabled current investors to buy stock in the market close to the 58p level that institutions & high net-worth individuals could buy in the highly oversubscribed placing. The price has risen slightly this week to above 60p, which may indicate that the seller has cleared, although there have been quite a few false dawns on this one.

We'll look in detail at what investors are getting for this price, but first, let's give a brief overview of the business.

Drilling Services

Until recently, the bulk of Capital's revenue came from providing drilling rigs and crews, mainly to the gold mining industry in Africa. After listing in 2010, Capital Drilling as it was then, invested into growing its fleet of rigs:

As you can see, this worked well until 2013 when demand for rigs fell away, leading to much lower fleet utilisation, primarily due to the fall in the gold price:

Although this led to losses at the EBIT level, the company was able to remain EBITDA positive over this period:

By focussing on longer-term contracts, the company maintained the operational performance of the business. They were able to retain a high average monthly revenue per operating rig even as the number of rigs they were able to deploy dropped:

Note that the company has also been able to increase its gross margin on the drilling part of the business in the last few years. While not at software company levels, this shows that the company has a competitive advantage of some kind. They often don't price themselves as the cheapest option but sell on reliability, quality, and consistency of service.

This meant that the company was able to cut capex below depreciation to generate free cash flow even during the difficult times:

They recently changed the useful life of some assets, extending the time over which rigs are depreciated and increasing earnings. However, due to solid maintenance & rebuild schedules, they were still using some assets that had been fully depreciated, so this seems a reasonable change.

They started 2012 with significant debt, so this drop in EBIT must have created quite an alarming time for the management. However, this disciplined capital allocation allowed them to reduce their debt in this period from over £20m to a net cash position in 2015.

They even managed to start paying a dividend in 2014 even though their fleet utilisation remained weak. By 2019 the gold price strength encouraged them to increase capex again to expand their business. They did this without raising equity until last year's transformative mining services contract, which we will cover in the next section.

The fleet size increased in 2019 through new rigs being bought to service long-term contracts. Utilisation has been growing recently, mainly through the redeployment of more rigs into the fast-growing West African region.

Mining Services

In 2015 the company began to diversify into mine services, initially providing laboratory work assaying the drilling samples. This has expanded nicely, with contracts we know about with Allied Gold, Barrick, Endeavour, Kinross, Newmont and a few others. However, this is still a relatively small part of the overall business.

The company had ambitions to expand its services further. In October 2019 were awarded their first full mining services contract for Allied Gold's Bonikro mine in Côte d'Ivoire, providing the load and haul for the mine, in addition to drilling, maintenance and lab services. Although load and haul contracts tend to be lower margin than drilling, the longer-term nature of these deals means that the revenue is much more stable and less prone to the big swings in utilisation that come with running a fleet of drilling rigs.

The Bonikro contract was announced as worth $25-30m per year in revenue. So far, a delay in setting a long-term mine plan has meant that this appears to not yet be running at full capacity. By backing out the drilling revenue, we calculate that the company is likely to have done about $18m in total mining services revenue for FY20, of which over $10m was in H2. When the final mine plan is agreed upon, we expect this to perform in line with the initial contract announcement.

Since that initial contract, the company indicated it was bidding for further large mining services contracts. In November 2020, the company announced a deal that was described as transformative:

"Collectively, the Sukari Contract and the Amended Sukari Drilling Contract are expected to deliver incremental revenues of US$235 - 260 million (vs 2020 revenue guidance of US$130 - 140 million) based on Sukari's mine plan at the point of tender submission."

It seems that Centamin got themselves in a bit of a bind with their mine plan and needed excess mine waste stripping to keep their production on target.

"Centamin announces it has taken the proactive measure to partially integrate contract-mining into the open pit medium term mine plan at Sukari. This cost-effective and time efficient solution enables the company to accelerate the increased waste stripping programme and improve overall operational flexibility in the open pit."

As part of the deal, Capital gets to increase their mining fleet by nine blast hole rigs on a long-term contract through to the end of 2024. So about $75m of the incremental revenues are rig revenues on likely 40% gross margins.

Centamin required Capital to raise at least $20m of equity to fund the project's capex. Capital initially aimed to raise $30m. We expect their experience with entering the cycle downturn with significant debt in 2013 is one the company does not wish to repeat. Hence they wanted to fund most of the capex on the Centamin contract via equity and internal cashflows.

In the end, the placing was expanded to $40m due to institutional demand. The extra Capital allows them to bid for further contracts, which may require initial capex. Although the discount for the placing was low, the dilution was severe at c.40%, and the price achieved was not helped by the persistent sales of Mr Burton, which prevented the share price from rising along with the advancing company prospects at the end of the year. Without a retail component to the placing, shareholders may well feel a bit miffed at the level of dilution. However, due to Sustainable Capital's sales and maybe others, shareholders of any size will have been able to maintain their percentage holding by buying in the market at or close to the price of the placing.

Industry outlook

In an interview on 17 July 2020 Capital's Executive Chairman, Jamie Boyton, said:

You feel an absolute wall of demand coming through. So, I think we are going to have a very strong Q4 and a very strong 2021 with this gold price environment.

When an ordinarily conservative management team speak like this, it certainly makes you stand up and take notice. At the time, the gold price was around $1800/oz, and although the price has slipped recently to just over $1700/oz, this is still highly supportive of further exploration.

We think Mr Boyton may have been suffering from a bit of the planning fallacy here. Most of us are too optimistic when projects may start or complete. Rig utilisation for 20Q4 came in at 59%, which meant that an average of 56 rigs out of a fleet of 95 were operational during this period, while an average of 60 rigs were operational in 20Q3.

However, we have tracked additional known contract wins, or drilling starts through the company RNS's, tweets and customer announcements. These show a sharp increase in rigs being deployed in 21Q1 and we expect the quarter to end with around 68 rigs operational, up from 56 in 20Q4. This level is likely to be maintained throughout 2021. We believe that the current market backdrop means that the company is highly likely to win additional contracts in the coming months. We also expect a significant number of longer-term contracts to be extended when they end in 2022.

Both industry analysts and competitors back up this market view:

Exploration spending is set to swell by around 20% in 2021, as cashed up juniors and majors reactivate plans post-COVID.

Copper and gold will outperform other metals, accounting for a huge chunk of the predicted $10 billion spend this year, but exploration will be more "broad based" than S&P anticipated six months ago when gold was the only bull in the metals market.

Mark Ferguson, head of mining studies at S&P Global Market Intelligence, quoted in Mining Journal 9 March 2021

As we enter 2021, utilisation has increased, I'm pleased to tell you it. It is getting to a stage where we're part of almost totally maxed out. We're actually -- we're buying rigs, okay? We're back in the market.

…What we're seeing, if I may summarise, I would say, is reminiscent of what we see on the beginning of the up cycle. It's extremely busy. No spare rigs. And it's not just Geodrill. This is an industry thing. All of our competitors are talking about shortages of rigs. And our competitors, we note with interest that they're starting to report stronger pricing, and I would concur with those comments, we're starting to see the same thing. And it's a natural function of a rising market, rising cost. It's all looking very good.

Geodrill Conference Call 8 March 2021

Many of our senior gold and copper customers have identified exploration and reserve replacement as an important part of their future plans. And so, we are naturally optimistic given the commodity price environment. Additionally, junior mining companies continue to raise Capital and are getting ready to deploy the capital raise recently on exploration projects. This pickup in financing activity is indicative of the changing sentiment in the capital markets. For a number of years, the mining industry has seen under investment and will need steady exploration activity and, of course, associated specialised drilling services to replenish reserves for years to come. To conclude, we believe that we are in the early stages of a strong upcycle in the drilling business due to a strong gold price environment and the growing need to mine for copper.

Major Drilling Conference Call - 5 March 2021

Testing the Tamesis Assumptions

In order to understand how realistic the Tamesis assumptions around rig utilisation for 2021 and 2022 are, we analysed the number of additional rigs that we know have started drilling in 21Q1. We get this information from contract announcements made by Capital, announcements of drilling campaigns by customers, and tweets made by Capital announcing the commencement of drilling.

By making some assumptions about how fast additional rigs can be deployed at Sukari plus how long the average exploration drilling lasts, we expect around 68 rigs to be in operation at the end of Q1 and this level to be maintained into Q2. Without additional rig contracts, this would begin to tail off. However, in the current environment, we expect that further exploration contract wins will be made and mine site contracts extended. Tamesis estimates around 70 rigs on average operational in 2021.

Looking further forward into 2022 and beyond, we note that a number of client exploration drilling campaigns have shown significant mineralisation and we expect at least some of these to enter delineation and production phases. We believe that Capital would be strong contenders to win these given their history of supporting these clients both as drilling contractors, and in some cases, significant providers of equity capital (see next section).

Tamesis assumes an average monthly revenue per operating rig to be around $175k going forward, compared to $171k for 2020. We consider this value to be conservative given the tightness that competitors report in the rig market. In addition, contracts tend to increase as they mature. Longer-term contracts require less rig mobilisation so the operating time increases, and sometimes single-shift operation can be extended to double-shift on production contracts. ARPOR has often approached $200k per month in the past and we don’t see why that isn’t possible as more contracts mature.

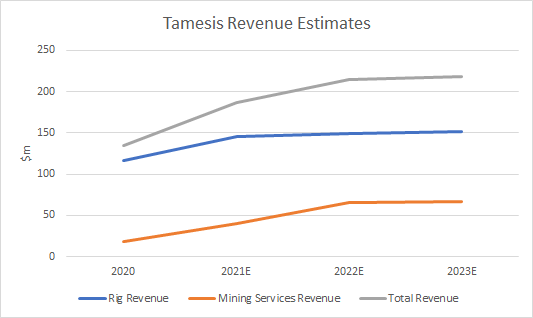

On the mining services side, this is what Tamesis is forecasting:

We can calculate from the Capital Q4 trading statement that they booked about $18m of mining services revenue in 2010. Tamesis are therefore forecasting an additional $21m of mining services revenue for 2021 and around an additional $48m for 2022 and 2023.

Centamin is forecasting slightly lower waste stripping in 2024 so we would extrapolate $36m for this year. This comes to $153m. Adding in the $75m additional rig revenue from Sukari gives $228m of total contract revenue. This is lower than the range of $235-260m given in the contract announcement. Therefore, we conclude that Tamesis is being conservative with their estimates here, particularly since this appears to exclude any improvement in the mine plan in Bonikro or additional contract wins for the mining services part of the business.

In summary, we don’t see any reason to assume that the Tamesis assumptions are in any way optimistic on the revenue side.

Gross margins become increasingly hard to estimate as mining services revenue becomes an increasing proportion of revenue. We expect mining services revenue to be lower than drilling services, and in some cases, the industry can expect as low as 20% gross margins. If we assume the drilling part of the business retains its 40% gross margin, then Tamesis is estimating a gross margin between 25-30% for mining services. This seems reasonable given that we know from the Centamin capital markets presentation on 2 December 2020 that Capital were not the cheapest bidders but was chosen primarily on reliability and willingness to engage and train a local workforce.

The Equity Portfolio

Even after recent falls, the current price of gold has been highly supportive of equity capital raises in the gold mining sector. Companies have been able to raise equity finance at-will for increased production or exploration projects.

However, in 2018-19 the story was different. For many years, gold prices had remained low, which had starved gold miners of exploration capital, even for some of the most promising prospects. Since 2012, global gold reserves have reduced by about 30%, leaving miners in dire need to replace reserves to maintain production.

Capital faced challenges of their own in the last mining cycle but had built up significant cash balances by this time. This enabled them to use their balance sheet to win drill-for-equity contracts. They identified companies with promising prospects and were willing to provide drilling services in return for equity stakes in these listed or unlisted companies.

In 2020, the growth in the value of these stakes meant that the company started to report them separately. The company doesn't reveal what these holdings are. Still, we know from public filings they include Predictive Discovery, Cora Gold, Golden Rim Resources, Arrow Minerals, Firefinch, Tanga Resources, Awale Resources, Desert Gold and Marvel. Based on current market prices and including the $11.3m last valuation of the unlisted securities, these are currently worth over $26m or around 17% of the current market cap.

With the equity markets now highly favourable towards gold mining equities, there is little scope for new drill-for-equity deals, but this strategy has proven itself both in absolute returns and as a business development strategy. Capital continues to win business from this and has active drilling campaigns with at least 7 of the 9 listed companies we know they own equity stakes in.

Competitor Comparison

While comparative analyses have to be treated carefully, both the Tamesis note and the company in their presentations highlight the mismatch between the EV/EBITDA rating of Capital versus drilling and mining services peers.

(Source: Capital Presentation – December 2020)

These show that, on an EV/EBITDA basis, Capital is trading at around half the rating of the average competitor. This is despite Capital having a younger rig & mining fleet than the majority of those. Since the Capital last conducted its analysis in December 2020, the average drilling services competitor has gained 11%, whereas the Capital share price is at the same level, making this difference even starker.

Risks

Every equity investment has risks. However, Capital operates in some of the riskiest countries on earth. This is mitigated though through the extensive use of experienced local employees and diversification across multiple countries. One of the good things about rigs is that they are mobile. This helps to shift resources to where demand is and means that the company is less exposed to adverse events than a mine fixed in one location.

The mining industry can be one of the most cyclical around. Although we are currently in a strong uptrend, this will not last forever. The company has been targeting much longer contracts though and this will reduce their exposure to the short-term mining cycle.

With the latest mining services contract, Capital has 35% of their rigs and more than half their mining services revenue coming from the Sukari mine owned by Centamin. While Centamin is a profitable cash-rich listed company that has operated in Egypt for over a decade, this is still a significant customer concentration.

Conclusion

All the signs from Capital, competitors, industry analysts and our own independent work point in one direction: that there will be increasing demand for drilling and mining services in Africa over the next couple of years and that companies with the experience to deliver into these difficult markets will prosper. Capital has both the assets and expertise to support that demand. Despite this, the company trades at a discount to both the market and listed peers.

The recent share price has been weaker than competitors despite increasing rig utilisation and, in most cases, a newer mining and rig fleet. The results due to be released on 18 March 2021 will not stand out as exceptional on their own. However, they will contain the company’s 2021 market guidance, which may lead to the market re-examining this enterprise's potential. If not, and the company delivers anything close to Tamesis forecast of 50% compound growth in EPS over the next two years, it would seem that a material re-rating must occur sooner or later.