Small Caps Live Weekly Summary

CARD GDWN HAT SDG SDI SMRT ZOO ZTF

Straight in with the results commentary this week:

Card Factory (CARD.L) - Trading Statement

The positive start to the financial period, highlighted at the preliminary results, has continued. Trading in the first six months was materially ahead of the Board's expectations.

No broker coverage for private investors, so we have to guess what this means until the consensus progressively filters through to us. Stockopedia shows EPS moving from 11.4p to 12.4p, but it is not clear if all broker updates have been reflected here.

At year-end, the company had £67m of debt plus £105m of lease liabilities (£5m more than their assessed value). Payables are far higher than receivables, which is a great place to be until it isn't.

The revised facilities comprised term loans of £30 million, CLBILS of £20 million and an RCF of £100 million. The CLBILS are subject to an amortising repayment profile with final maturity in September 2023. The Term Loans are set in two tranches, both with an amortising repayment profile. Tranche 'A' has a final maturity in January 2024, and Tranche 'B' is coterminous with the RCF in September 2025.

Total borrowings were £67m at year-end, and assuming two term loan tranches of £15m each, facilities would be £115m at January 2024. That could be tight if suppliers get cold feet on those £85m of trade and other payables.

As such, although EPS includes debt interest, the company clearly does not justify being on as high a P/E as one without this debt and poor current ratio.

With four brokers but none that we can access, the company doesn't appear to want the likes of us as shareholders. And it is not so special or cheap to go against that. But nor does it look expensive, even in today's market. If things continue to go well and they spend a couple of years repaying debt, then there would be scope to significantly increase the dividend payments, which would make it look considerably more attractive.

One plus may be that competitor Clinton’s is closing a number of stores. As we’ve seen with DX & Tuffnells, the failure of a large competitor can drive strong near-term returns that aren’t priced in.

However, it seems strange that Clinton's is largely failing, but Card Factory is beating expectations. We have yet to come across someone who’s said "well I'm a Card Factory man through and through. I wouldn't be seen dead in a Clinton's Cards". The difference may well be Card Factory’s largely in-house manufacturing which we don't think Clinton’s have. So Card Factory have been able to take cost out of their products, whereas Clintons are stuck with what other suppliers will make. Taking cost out of a product is often only a short-term gain, though. Particularly when the products are already low-end.

Goodwin (GDWN.L) - Preliminary Results

The management here were clearly very savvy to have fixed their debt at such low levels for so long, but it seems correct to exclude these gains from trading profits. As such, 10% underlying profits growth and a 7% increase in dividends are roughly in line with inflation over the period. Management’s preferred metric of PAT+DA is only up 3.9%, so behind inflation:

This is also below recent trends. Revenue is up around 30% though, so the big question is if this negative operational gearing is temporary due to inflation or permanent due to mix.

Underlying EPS without the swap effect is around 190p. Making the shares currently trading on a 25x multiple. This seems completely incongruous with a company struggling to grow in line with inflation in the recent past.

Several board contributors point to a number of initiatives that should see growth accelerate from here. However, when the current multiple is already pricing in something like 25% CAGR EPS growth over the next five years, then investors need to be expecting 30-40% CAGR EPS growth over the next five years to generate acceptable returns for holding this illiquid small cap. It may well happen, but we prefer to hold something where no growth is priced in, but there is a chance of a surprise to the upside rather than something priced for high growth and hoping for exceptional growth. Particularly when recent growth has been lacklustre at best.

H&T (HAT.L) - Interim Results

Strong results here for a cheaply-rated stock:

· Profit before tax increased by 31% to £8.8m (H1'2022: £6.7m), as continued momentum in our core pawnbroking business provides a robust revenue and profit foundation for the remainder of the financial year.

· The pledge book grew 14% to £114.6m (December 2022: £100.7m; June 2022: £85.1m) with demand for pledge lending remaining at record levels. Gross lending grew 22% to £128m (H1'2022: £105m).

· Retail sales increased 11% to £23.0m (H1'2022: £20.8m)

On top of which, they say:

We expect a lower level of cost inflation in the second half of the year which, alongside the growing revenue momentum of the business, puts us on track to deliver record profits in 2023.

However, their broker Shore cut their EPS forecast by 7% to 53.7p (adjusted). After making 16.3p in H1, it needs a very good H2 (or a lot of adjusting!) to make 53.7p for the full year.

Cashflow and profitability are also adversely affected by loan book growth which will not please shareholders, but help the scale economics of individual stores. There seems to be plenty of scope for further growth without significant capex - working capital outflow, yes, but that is reversible.

They look to cheap on a P/E basis despite profit being adversely affected at times of growth by the accounting treatment of early redemption impairments. Net tangible assets look little changed since year-end, giving the beginnings of valuation support at 1.3 P/TBV and may be understated on the basis of rapid liquidation of inventories. This has never been expensive on a P/E-basis, though, with investors perhaps tending to treat it like a bank and use P/B as their preferred metric. In reality, this is a bit of a hybrid business, although pawnbroker still makes up a much bigger proportion of Gross Profit (59%) compared to Ramsdens (20%).

If the demand for pawnbroking services were to turn down, then free cash would start to be released very quickly. Likewise, they could generate cash quickly if they somehow overstretched themselves. The modest cut in near-term broker forecasts seemed to hit the share price initially. But the subsequent recovery is quite bullish from what was a weak chart.

Sanderson Design (SDG.L) - Half-Year Trading Update

This is a nice detailed update giving a good insight into how the business is developing. The upshot is:

the Board's expectations for the Group's full year profits remain unchanged.

They have been saved by the US and strong licensing performance. Manufacturing is looking pretty weak:

Volumes here must be down 30% or so once you include price impacts. Although they say this was against strong comparators due to post-COVID restocking.

We are tending to avoid most companies that have exposure to UK housing or consumers, given the very weak trading outlook for these sectors following recent interest rate rises. This remains an exception, though. The strength of the IP licensing and lowly rating continue to stand out in the sector.

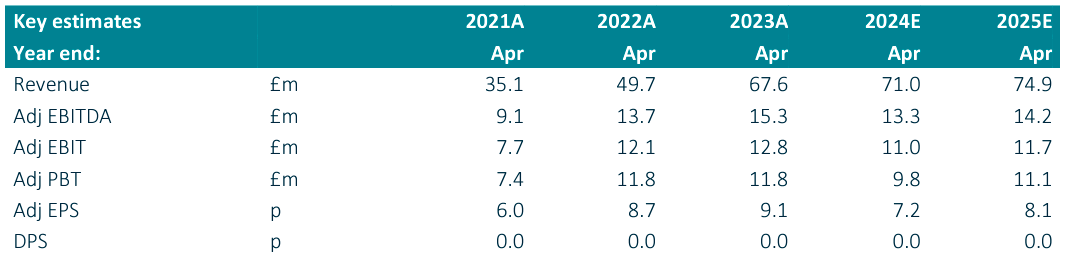

SDI (SDI.L) - Final Results

· Revenue increased by 36.0% to £67.6m (FY22: £49.7m)

· Adjusted operating profit* increased by 5.8% to £12.8m (FY22: £12.1m)

· Reported operating profit reduced to £6.8m (FY22: £10.2m) due to a non-cash £3.5m impairment charge against Monmouth/Uniform

· Adjusted profit before tax* of £11.8m (FY22: £11.8m)

· Reported profit before tax decreased to £5.8m (FY22: £9.9m)

· Adjusted diluted EPS* increased by 3.6% to 9.02p (FY22: 8.71p)

· Diluted EPS of 3.72p (FY22: 7.23p)

The revenue growth here is impressive, although it is not organic. However, 9.02p EPS here looks like a small miss on consensus. It is probably right to exclude the write-offs at Monmouth/Uniform from the adjusted figures. However, this shows that this is a company that is struggling to generate growth and decent returns apart from via acquiring other businesses.

2023 was still an exceptional year for optics performance, and brokers have been guided that this won't continue. So 7.5p EPS is forecast for next year by paid broker Progressive. House broker finnCap are more pessimistic with 7.2p for this year:

Although they are willing to put their finger in the air and come up with 8.2p for 2025.

Presumably, these don't include acquisitions which may increase EPS above this level. However, with just £9m of headroom on their facility, these can't move the dial in the way they used to. There is also still the outstanding question of acquisition multiples expanding. Management explains this as having to buy freehold property with the latest acquisitions and the multiples being similar if you adjust this out. However, they fail to adjust back in the rent they are saving. We are not sure if they don’t understand this concept or are choosing to gloss over it. In addition, the latest acquisitions, such as Monmouth and Safelab, appear to be lower-margin, more commoditised businesses.

Despite these niggles, it is generally a well-run company which is shareholder friendly. Mark has owned it in the past and will probably own it again in the future if the price is right. So what is the right price? We think an argument can be made for the fair value being around 12x forward earnings consensus at the moment, assuming they can maintain longer-term growth rates via acquisition without massively diluting holders. This comes to around 88p. This is still significantly below where the shares currently trade, and a savvy buyer will be looking at a further discount to fair value. It shows that it can take a long time before a widely-loved stock comes back down to fair value after everyone gets excited about it.

SmartSpace (SMRT.L) - Trading Update

Cash balance at the period end of £2.2m (30 April 2023: £1.25m) with no debt

So £0.1-£0.2m burnt after considering receipts from A+K sale. Perhaps less after costs, and less still going forward given the lack of mortgage payments. Of the sale, they say:

The net disposal proceeds of approximately £1.1m will be used for working capital purposes and to invest in growth of the business where opportunities arise.

So they aren't going to splurge it right away on increased marketing. Yet we suspect marketing costs will increase somewhat going forward, and this might be the last period where it has been significantly constrained. Under these circumstances, this looks like a good performance:

Annual recurring revenue ("ARR") up 21% year-on-year to £5.8m* (31 July 2022: £5.0m or £4.8m on constant currency basis

But actually, this is behind the trend in the graphs we have posted in the past. The culprit appears to be ARPU:

Monthly average revenue per user ("ARPU") increased by 9% year on year to £94* (31 July 2022: £90 or £86 on constant currency basis)

This is (and to date, has been) an APRU story, just as dotdigital was: Selling ever more features to a relatively gently growing user base. In stark contrast, 9% growth is behind the RPI figure, where many UK contracts will be pegged.

Part of the problem will be the one-off price increases in the previous period, as previously announced, although we would expect some of those to still benefit them in H1. But there does seem to be strong momentum on new customers:

There was a strong return in sales momentum in SwipedOn during May, June and July. With digital marketing now back inhouse, there has been an increase in both the quality and volume of leads. New customer wins have been achieved on a lower Customer Acquisition Cost ("CAC") than previously, further improving our LTV:CAC ratio.

As a result, growth in customer numbers over the last six months has been the highest recorded in the last two years, adding 637 new customers in the period. Of these, 128 were signed in July, 103 in June, and 125 in May.

If the customers acquiesce to Microsoft-style forced bunding, then some better ARPU news is on the horizon:

A new pricing model, bundling addon's with main product lines, was implemented towards the end of the period and is expected to raise new customer ARPU in second half of the year.

Space Connect remains small.

The Board continues to see good opportunity for growth over the coming months from both new customers and expansion within SmartSpace's customer base, in particular with the release of Spaces and traction in new markets. As a result, the Board expects, on a constant currency basis, full year results to be in line with market expectations.

Overall we think they are indicating a reliance on faster growth in H2 to meet expectations. Broker Canaccord seem a bit confused:

At constant FX, SmartSpace expects FY24E will be in line with market expectations.

But FX hasn't been constant, it has provided a headwind in H1! So are they saying they are assuming constant FX from here? They highlight a recent transaction in the sector:

In July, FM:Systems was bought by Johnson Controls for US$455m, which is notable for being the first major consolidation within the workspace management software sector by a trade buyer.

Their valuation continues to be based on innumerate ARR acquisition multiples that have only ever applied in bubble markets:

we think a premium is warranted given recent sector M&A (typically at >7x ARR) with few strategic assets left in play. Maintain BUY and 125p TP.

Forecasts show minimal to no cash-burn, giving them time to grow. No profits or positive cash flow are expected until at least FY 1/2025. Despite the forecasts for level cash, no doubt the company will be exploring whether that recent higher LTV:CAC scales and whether it is worth pushing a little harder for growth.

And in a hard-to-value company, board shareholdings are important. And until this week, none of the directors held shares. They appear to have waited until they had re-based all their options until they started buying. Almost nothing screams failure more than re-based share options. However, perhaps the failure is finally over, and the outlook is brighter from now on.

Zoo Digital (ZOO.L) - Final Results

The results to 31st March 2023 here are pretty good:

Revenue grew by 28% to $90.3 million (FY22: $70.4 million).

Adjusted EBITDA* grew to $15.5 million (FY22 restated: $7.1 million).

EBITDA* margin increased to 17.1% (FY22 restated: 10.0%).

Operating profit has quadrupled to $8.1 million (FY22 restated: $1.9 million).

Reported profit before tax of $7.9 million (FY22 loss restated: $0.2 million).

However, the company have already warned that 2024 are going to be much worse.

Current trading has been impacted by several major streaming companies carrying out strategic reviews to refocus on profitability and the first simultaneous strike of US writers and actors in 60 years. This has created short-term market disruption and temporarily lower volumes of localisation and media services work.

The Board has been taking steps to adjust the cost base to reduce the impact of the temporary industry slow-down on ZOO's business while there remains uncertainty around the timing of the resumption of former levels of production and orders. The Group remains financially strong with net cash at 30 June 2023 of $23 million.

It sounds like things are getting worse, not better. And there is enough negative newsflow to justify another downgrade here, but it looks like their toes are joining their crossed fingers for an H2 recovery:

However, despite this short-term industry-wide uncertainly, ZOO expects to be in an even stronger position with several customers following a rationalisation of their supplier bases and to take further share of the media localisation market once former order levels resume. At this stage, it is reasonable to expect this will be in H2 of our financial year.

Progressive are forecasting a very rapid recovery in 2025. In their latest piece they say:

We also maintain FY25 estimates, with revenue at $115m and adjusted EBITDA at $19m.

They forget to mention this is a small cut in EBITDA, and the $19m is a rounded figure. Plus, they’ve cut their 2025 EPS from 12.7c to 11.5c. Still, this is a P/E of less than 7 if it is realistic. The cuts don’t help build confidence in this, though.

We suspect this is one of the better turnaround opportunities out there. Although with the risk of a further big sell-off before it arrives. However, they should have enough cash to see them through a period of weak trading. Of course, at this point, shareholders will be hoping they don’t use it for any acquisitions. There is no visible progress on the announced Japanese acquisition. Are they trying to renegotiate the price in light of a marked deterioration in their markets? A collapse of the deal would potentially be positive for current shareholders, with cash raised at 160p versus the current share price of 60p.

The real risk is that streaming companies decide they don’t want to spend hundreds of $m creating series that don’t generate any incremental revenue. Perhaps this is the new normal?

Zotefoams (ZTF. L) - Interim Results

Revenue appears to be slightly ahead of inflation:

Group revenue of £64.6m, 9% higher year-on-year (HY 2022: £59.0m)

However, higher gross margins translate into much improved profitability:

Profit before tax (PBT) increased 30% to £7.4m (HY 2022: £5.7m)

The outlook is cautious, though:

The short-term outlook for the remainder of the year is somewhat tempered by market expectations of squeezed consumer spending and industrial deflation, resulting in inventory reductions in some of our markets. Other markets, such as aviation, are not expected to be impacted by this trend, with underlying structural growth drivers remaining robust. We expect energy and polymer input costs to be more beneficial while the US dollar, at a current rate of around $1.28, will provide a headwind to profitability for the remainder of the year, after benefitting operating profit by £1.1m in H1 2022 despite being partially hedged.

We're all familiar with companies reporting a weak H1 and an H2 weighting that never materialises, but here they seem to be hoping a strong H1 will carry them through:

We remain confident that the Company can deliver a full year performance in line with market expectations, underpinned by a strong first half performance.

In cases like this, we are never surprised if a downgrade has been sneaked in by their broker. However, their broker is holding steady. But the market is unimpressed.

Mark has always been unimpressed by this company. A decade of returns on capital below their cost of capital means that much shareholder value has been destroyed here by the company’s attempt to grow the business. Yet the 20x P/E rating inexplicably remains up there with the best of companies. The bull case here is that a capital-intensive legacy business is giving way to better, more innovative divisions. These results do little to back this story up, though:

It is the low-return legacy business that is the one driving the increase in profitability this year. Despite the repeated trumpeting, MuCell revenue has collapsed, and operating losses ballooned this half-year.

That’s it for this week. Have a great weekend!

I'm a Card Factory man through and through, you wouldn't find me, dead or alive, in a Clinton card shop.

I'd say owning your own card making factory isn't a one off to strip out costs, it's long term margin enhancement, with flexibility to make what you want when you want, to make a new card (I think they CARD have cited a few examples of doing this), and if it works make more fast. Think of CARD as the fast fashion of cards. Or from a price perspecitive the Aldi of cards. If they do gain from Clinton's losing, (and I'm not sure what the overlap is, or whether there is any receivership acquisition opportunity), then so be it, but it's another nail in the high street and for that all survivors must beware, Card Factory included.

I appreciate your insights on debt thank you, and the poor stakeholder engagement is a warning. The bottom line though is that if I must buy a card I want to pay as little as possible. I was so proud of the value of the Card Factory card I bought for my business partners 50th birthday I left the price sticker on so he could appreciate it too. [I hold]