This week we published our second long-form write-up of a stock. We picked Capital Limited (CAPD.L) since it ticked our boxes of looking undervalued and with news due in the form of results. Read our original write up here and our thoughts on the results below.

A reminder that to see the full debate you will need to be a ‘member’ of the server. This is free and easy to access, so if you don’t already have it then here is an invite. Links will usually go to the browser version. So if you are a member with the app installed putting the company ticker into the search bar to find the section may be the easiest option for you.

Large Caps Live Monday 15th March

This week Wayne took a look at some of the impacts of the vaccine programs around the world. And in particular what it means for cruise companies, such as Carnival (CCL.L).

Historically this company had an ROE of 11-13% so with base rates low I would imagine that people would have used a circa 8% cost of equity so this business probably traded circa 1.5x book value. Currently, it is at 1.25x….

Generally I dislike cruise liners as they are capital intensive, cyclical and the promise of massive Chinese demand was met by Chinese specific ships (Chinese owned / Chinese designs etc). So my entire idea here is really that as the elderly population ie over 50s get vaccinated they go crusing…

So I feel it is not the purest idea and I feel it is a trade but my thoughts are that desperation for revenue and tourists will lead to countries pending over backwards. Admittedly the balance sheets of the cruise companies are not great either - so they need cashflow.

This is definitely a DO YOUR OWN RESEARCH kind of idea. As I said I have no position in it - but am thinking about it but could easily change my mind.

He also took a look at Rolls Royce (RR.L), summarising:

1. Warren East is frank, open and honest

2. He was brought in to fix this business in 2015.

3. I think that the fact that 5 years later he is still fixing it says a lot about how fundamentally bad some of the stuff in the business was

4. On the chart you can see the issues in 2015 - 2016.

5. I have clearly missed the absolute bottom in 2020.

6. But we now have greater visibility

7. And I also think that from mid to late this decade we will have an upgrade cycle for low carbon aero-engines

8. There are two big contracts that could be won or lost this year - for B52 and VTOL - my suspicion is that a US supplier will be preferred but we shall see.

9. The other big issue is that there is customer consolidation. GE is selling its leasing arm to Aercap.

So I think again that Rolls Royce is a trading stock with a chance of breakout if the airline industry starts flying faster.

“• Full year net booking volumes declined by 79% (2019: -6%).

• Net revenue of €15.4m, a decline of 81% compared to 2019 (2019: €80.7m).”

However, the company remains long-term positive:

“We remain convinced that when travel restrictions are lifted, we will be well positioned to benefit from the recovery in demand, driven by our improved platform and loyal customer base.”

I think there are reasons why this optimism may be misplaced:

Although the UK & US appears to be on a strong path to re-opening, this doesn’t mean that the rest of the world will be as lucky.

Which means that those travelling abroad, particularly more exotic areas, will need to quarantine for quite some time.

It is already quite a niche business competing with the likes of booking.com & expedia.

So I think there are some structural reasons why this will bounce back more slowly than travel in general.

The future cash outflows show little sign of abating in the short-medium term:

I think it is unlikely that we will see significant bounce back in 2021 given the nature of the business so we should expect a further €17m of operating cash outflow, €4.4m of cancellation refunds, €4.1m of Irish Revenue tax owed & €1.3m of deferred consideration due in July. Less €5m - €3.4m = €1.6m that we are assuming has already been paid out in the first two months.

This comes to a total of €25.2m of cash outflow for 2021 and a cash balance of €15.6m. Looks like the company survives but net debt will be around €14m and you can see why they needed the €30m loan and were willing to pay the equivalent of around 12% interest to get it.They don't have much spare capacity if any severe disruption lasts into 2022 though making it quite risky. Market cap at 92p is currently around €128m so EV will be €142m.

Concluding:

The chance of this being a zero in the short term has declined with the loan issuance but the risk-reward here looks far from favourable at the current price even assuming a bounce back in travel spending.

Leo questioned their definition of recurring revenues

Given the poor outlook in the sector I'm surprised to see:

“Annual Recurring Revenue ("ARR") committed at the period end increased 13.4% to £47.5m (2019: £41.9m constant currency), providing a strong basis for future growth”

Well, it may be the definition of "recurring".

“o Group revenue of £73.0m (2019: £77.6m constant currency), reflecting impact of Covid-19 on Education Services segment

o Core Student Information Systems revenue £56.9m (2019: £58.0m constant currency)

o Education Services £16.1m (2019: £19.6m constant currency)”

Mark like the cashflow characteristics of this sofa retailer.

This has been a cash-machine over the last few years.

“Strong balance sheet with cash of £91.8m at 23 January 2021 (2020: £61.5m)”

This compares favourably with a market cap of £92m. We have to be careful with just looking at just the cash figure as they run a negative working capital model. I have calculated what I consider to be "shareholders' cash": Cash minus the negative working capital and things like provisions.

Even if H2 generates no FCF, then the figures look like this i.e. I have not annualised the H1. (EV = market cap - shareholders cash)

H2 performance is highly uncertain given the lockdowns but there does seem to be significant pent-up demand for their re-opening which should give H2 a much-needed boost. Given the cash on the balance sheet, this looks cheap on almost any metric you could choose.

Mark started off by looking at this online mattress supplier. On the surface, things may look good for them with Revenue, Gross Profit and Net Cash all rising year on year, although in a market where online retailers are clearly thriving.

The outlook didn’t seem to bad either:

“Revenues in the first two months of the year increased 16%, representing an acceleration from the last quarter of 2020, where growth was held back by some supply constraints.”

However, diving into the details things are less rosy:

They have gone from a roughly balanced working capital profile, with inventories and receivables matching payables, to £1.5m of negative working capital. I suspect this is unsustainable.

They also have around £1m of current provisions. From these combined, I expect at least a couple of £m cash outflow in 2021.

Large share-based payment charges, combined with capitalised intangibles exceeding amortisation by some margin, mean that the real economic value delivered to shareholders may actually be worse than the £2m loss.

And I think the key point is that it is not clear whether trading is actually cash flow positive in 2021 either. 16% increase = £4m incremental revenue = £1.7m addition profit after distribution costs (based on the 43% margin in 2020). This is not enough to make the company profitable, even if you assume that it hasn’t been necessary to increase marketing spend to get there.

Leo pointed out that they seem to be presenting results in an overly optimistic way and using basis points where percentages would be normal.

Mark concluded that:

This has the slight whiff of a company still struggling and trying to put a brave face on it. I think they are a pretty good product, e.g. they come top in this recent review. Just that the investment case is a lot less clear-cut than a superficial reading of the narrative would lead you to believe.

The results call at 9am felt a little rushed since the company had technical issues getting the results into the RNS system which left only 19 minutes to digest them before the call. Therefore it is good news that the company are presenting on the investormeetcompany platform on 25th March.

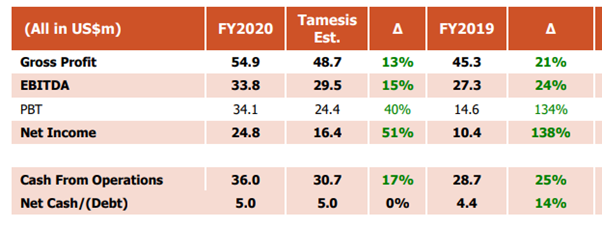

Revenue was in-line, as we knew it would be from the recent trading statement, so Mark started with the following table from the Tamesis Partners note showing that these beat their profit expectations:

This is all about 2021 though and here these results and the call backed up our previous bullish stance:

There are multiple signs from the results that Tamesis 2021 forecast may be conservative. We have some new contract announcements and some indication that ARPOR is going to go up with the cycle and higher margins.

Tamesis retain their 127p Price Target but this could be reviewed if (when?) the results reflect this strong trading outlook.

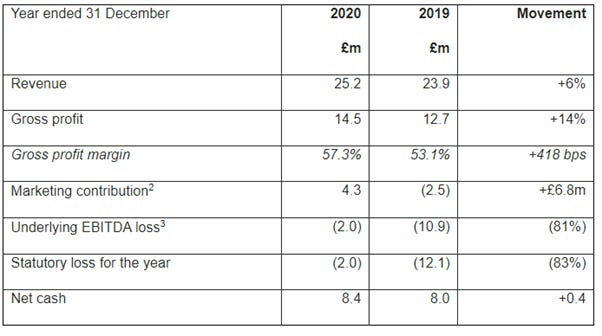

Again, I'm really surprised that H2 is down YoY. Given the poor H1 and strong homeware spending elsewhere, I would actually have expected catch-up revenue in H2. But, of course, they mostly sell tableware that you need when you have guests around, not when you're stuck inside watching TV.

But here's the main problem I have with these results:

Note that there is absolutely no attempt to split costs between costs of sales and admin costs! And in the preliminary results there is no breakdown of these costs.

Regarding the brands, there is a particular problem of H2 weighting in North America which reduces visibility. The UK is much better in this regard. My issue here is that we have little idea whether the downturn will reverse when lockdowns end, whether restructuring will lead to cost savings or whether margins will continue their recent falls.

I do feel there is scope to monitor the strengths of the brands on ebay etc. and this is something I'm going to look into further.

Mark felt that this is now fully valued, at best, with the market pricing in a full recovery in 2021. Concluding:

The margin of safety on this one looks non-existent to me at the current price.

Finally for this week, Leo was sceptical about this announcement from HeiQ:

I think it pays to read this kind of announcement fairly carefully and cynically. So there are two parts to this: a licence and a supply of chemicals. The exclusivity is presumably related to particular application areas.

“exclusive worldwide rights to apply HeiQ Viroblock to coatings for printing processes such as commercial print, food, beverage and pharma packaging.”

That sounds like quite a wide area of application and means that they presumably can't licence to competitors in this area.

“The two companies have signed a five year contract (US$8m in the first two years, at which point the contract is subject to renewal) which is expected to deliver US$30m of royalty revenue to the Company ("the Minimum Exclusive Requirement")”

So I read that as "not a 5 year contract". Looks like a 2 year contract to me? And will only be renewed if they take at least $8m in the first two years. It isn't clear whether they have to take $8m though.2

And also the contract hasn't exactly been signed: The two companies are currently completing the product development, due to be finalized at the latest by 1st August 2021, following which the exclusivity period begins.

So I think shareholders will need to monitor the progress of this one carefully rather than counting the $30m as being in the bag.