It has been a busy time following our last long-form stock write up on Capital Ltd (CAPD.L). We looked at the company’s results last week. Then on Monday, Mark joined the panel at the Mello Monday investor event to present some of our research.

Both Mark and Leo joined the Capital investormeetcompany presentation on Thursday. Then today the company have published a white paper on West African gold exploration. Plenty of weekend reading/viewing there!

Right, on to this week’s discussions. A reminder that to see the full debate you will need to be a ‘member’ of the server. This is free and easy to access, so if you don’t already have it then here is an invite. Links will usually go to the browser version. So if you are a member with the app installed putting the company ticker into the search bar to find the section may be the easiest option for you.

Large Caps Live Monday 22nd March

On this week’s Large Caps Live, Wayne took an eclectic look at

Building suppliers such as Kingfisher, Ferguson and Travis Perkins and Howdens

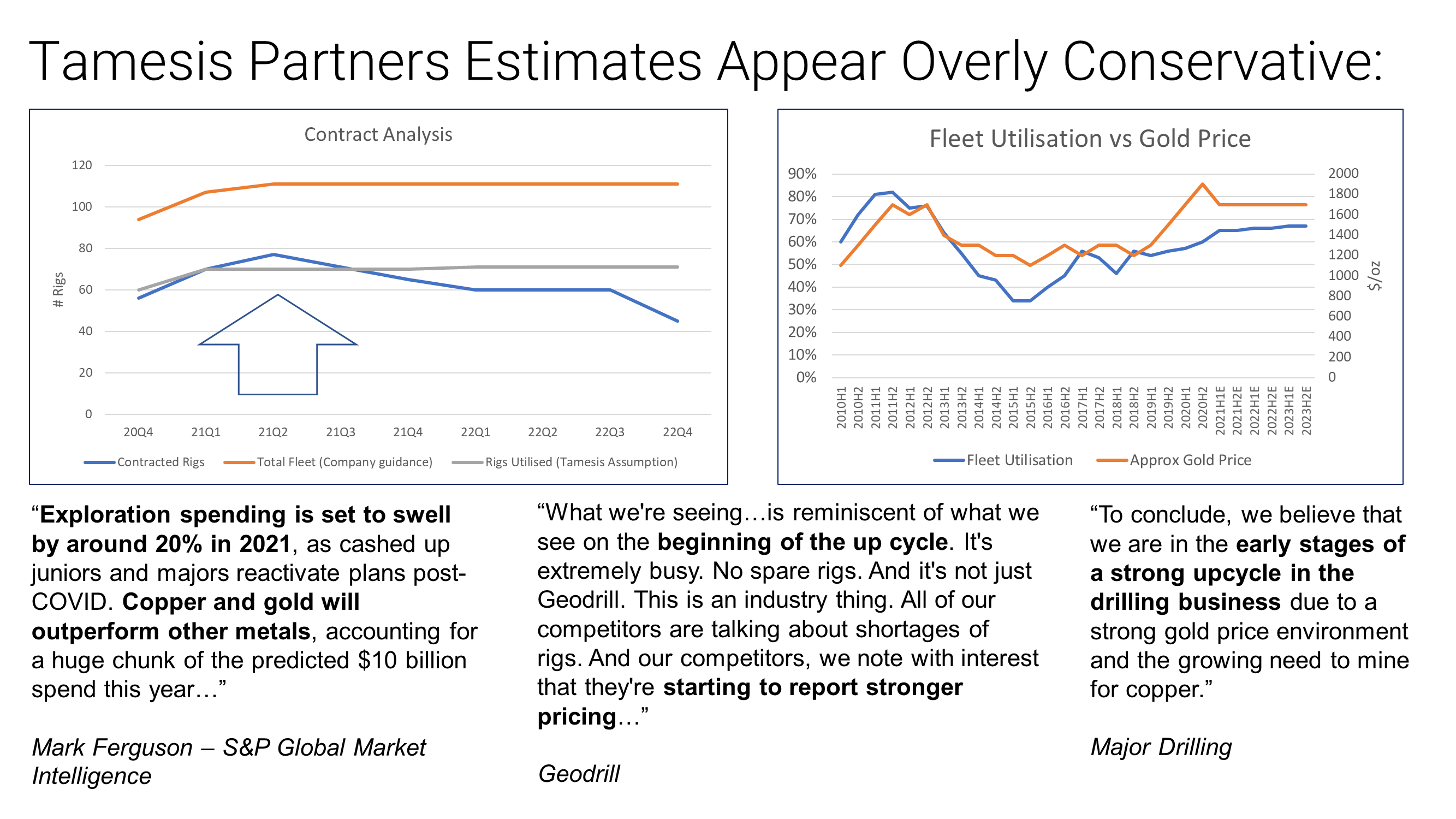

Although not really a small cap, we think this is worth following as a pure-play gold producer and since it is Capital Ltd’s biggest customer.

Mark thought that this looks reasonable value at the current price:

The outlook for 2021 is given as:

“• 2021 gold production of 400,000 to 430,000 oz, at cash costs of US$800-900/oz produced and AISC of US$1,150- 1,250/oz sold

• The Board reiterates its intention to recommend a minimum 2021 dividend of US$105 million (interim and final).”

With spot gold around $1730/oz this generates a range of $332-400m for 2021 EBITDA and $192-249m PBT.

Market cap is around $1.7b, with net cash of $310m, making the forward EV/EBITDA somewhere between 3.5-4.5x.

Reasonable value then, and with a yield of over 6%, there is potential value here.

The market may be concerned with the reduction in reserves in the accompanying reserve statement. However, having listened to the results call, Mark was reasonably sanguine about this:

On the management call, they spoke about this and a lot appears due to pit design. A new CEO has been in place for around a year and he has focused much more on cash generation. They re-iterate this in the reserves statement:

“Centamin is employing a consistent approach to the estimation of Mineral Reserves using economic cut off grades in both the open pit and underground. The mining operations are focused on the generation of cashflow rather than headline ounce production for the balance of the operating life. This approach is further considered against maintaining the life of the asset given the potential for further discovery in the concession (some of which is described below) and regionally.”

It seems to access the additional ozs for production in 2023+ they would have had to start waste stripping now and they were not willing to put the capex in when they have other potential prospects.

Leo was unconvinced by the outlook for this pawnbroker that has diversified into selling jewellery and unsecured lending.

In common with Centamin, a strong gold price is good for them as people cash in unwanted jewellery.

Clearly lockdowns are bad for them, but strangely H2 is was worse. Here's the H1s:

So it is unclear to me why H1 when they were closed half of the time they did worse than in H2 when it was only November and just before Christmas…So for me, this was a mildly disappointing H2.

This also suggests that H1 will be relatively weak with profits building later in the year….But the dividend increase sends a strong message about the medium term.

Likewise, Leo was less than impressed with the potential oulook for Personal Group:

“Group revenue resilient at £71.5m (2019: £70.9m) despite the COVID-19 impact, owing to a high level of recurring revenue and diverse income streams.”

This was as I expected, no immediate impact. But here's the killer:

“Introduced new sales channels of virtual visits and telesales in the core insurance business to mitigate inability to perform face to face visits on client premises due to COVID-19, but new annualised insurance premium still impacted at £2.4m (2019: £9.0m)”

Prorataed for the period before the first March 2020 lockdown you'd expect around £1.8m of sales. So this implies they only made £0.6m in over 9 months for the rest of the year. This is despite "new sales channels". This is far far worse than I had modelled and bodes exceptionally badly for 2021.

On the positive side:

“Our policyholders have demonstrated their belief in the value of our products, with retention rates increasing to reach over 80% year-on-year retention. We are proud to have kept our promises through the pandemic, paid out claims promptly and in full, as well as developing an immediate response to assisting financially vulnerable customers. Our genuine desire to protect our policyholders remains an important part of why they choose to stay with us.”

But my suspicion is retention rates will normalise before sales do!

The SaaS business did appear to be a bright spot, but when I did the sums the incremental margin was virtually zero.

Finally, we noted that house broker, Cenkos, put out a ‘Hold’ note, which is never a sign of confidence! Speaking of which…

However, these underperformed my expectations. My first bugbear is that you have to go to the Annual Report to actually get the info you need to make an informed investment decision. At least this was issued on the website at the same time:

Here we get to see the split between different revenue streams. H2 corp finance revenue was up from £9m in H1 to £13m. This was slightly less than I expected from the strength of their transactions.Market making exceeded my expectations generating £3m revenue in H2.

However, the real problem is that staff costs went up from £7.4m in H to £15.2m in H2.So you have around £7m incremental revenue in H2 but almost £8m incremental staff costs.

Leo noted:

The standout figure initially appeared to be the cash, up from £18.3m to £32.7m... But a lot of the cash was due to increase payables of £10m. Again to see what these are you need to go to the annual report, and it turns out a lot of them are performance-related pay owed to staff.

With Mark concluding:

Well, round hill music & US solar fund are due to raise more money at some point so these may save their 21H1 - without these 21H1 is maybe looking more like 20H1 than 20H2 on the revenue side.Of course, none of this revenue growth matters if all of it and more ends up going to the staff rather than shareholders.

“Trading since the announcement of our FY20 results on 16 February 2021 has remained strong, with all areas of the business performing well.”

They also confirm that they expect profitable trading in 2021:

“We are focused on sustaining this positive momentum across the business and remain confident of returning to profitability this year.”

So unlike CNKS don’t seem to be paying all extra revenue out as staff bonuses! News of potential IPOs is good too since these are typically larger, higher-margin capital raises:

“Our deal pipeline remains strong, including a number of IPOs which we plan to bring to market over the coming months.”

Although this remains subscale at the moment in my opinion, if it can trade profitably then I don’t see why this should continue to trade at a big discount to net tangible assets. Particularly since they are mainly cash.

Mark took a look at this Heavy Mineral Sands miner, having joined their analysts call in the morning.

This is the sort of capital markets cycle play I like, generally. Today they shared a further strong market outlook:

However, I am not rushing to buy at the current levels. If we get big price increases in HMS pricing Kenmare will look good value. However, my more conservative DCF assuming HMS rising in line with inflation doesn’t show much upside.

I get a £4.54 per share NPV12 valuation vs a share price of just over £4. The c.11% upside isn’t enough to tempt me. Mainly because a similar calculation on competitor Base Resources (BSE.L) yields more than double their current market cap.

Leo took a sceptical look at this company’s results, following its large rise off March 2020 lows, at least partly driven by the news that the main ingredient in mouthwashes kills COVID-19 virus.

Of course, it should be no surprise that mouthwashes would kill viruses, since they are designed to kill bacteria and lipid-enveloped viruses are prone to the same kind of attack. You'd expect the alcohol alone to have some effect, but there they highlight CPC.

So do VLG have some kind of patent on CPC, or special manufacturing know-how?No, it is a standard ingredient of many mouthwashes.

And is french kissing a major covid disease transmission vector? Well I'm not aware of any scientific research on the matter, but I'd say no, the evidence is that the primary transmission is airbourne, with secondary directly via hands.

Looking at the house broker forecasts:

So they've got a headline PE of 12.9x, which sounds cheap. But...it is cash adjusted! EPS of 4p on a share price of 85p is clearly a PE of over 20.If you want to cash adjust then EV/EVITDA is the traditional place to look, and that doesn't look amazing.

So the PE of 12.9x relies on either a) them returning the cash they have just raised or b) doing an acquisition at their 12.9x PE equivalent or less.

Concluding:

So my summary would be - yes, Venture Life have executed well, but they have also created a problem for themselves with that cash. Plus they got overhyped and seem to be on a downtrend.

Mark noted that not only had current trading been affected by the lack of footfall, but that:

“The continued closure of venues led to the Group having to credit and refund a significant amount of revenue that had already been recognised in previous years…”

The outcome is that they are changing their revenue recognition policy in promotional segment to match retail. This obviously has an effect on results. I assume they will then restate prior years but this appears to have had a positive impact on 2020 results.

Without this change the loss would be £3.1m. Making £1.5m loss for H2.In light of this, the debt looks a little precarious:

“As at 31 December 2020, the Group had cash of £0.8 million with £1.8 million of drawn bank facilities and undrawn bank facilities of £0.5 million. Since the year end, and as previously reported 29 January 2021, Group borrowings were refinanced and an additional £0.5 million of bank facilities agreed.”

They also had about £1.3m negative working capital at the HY. In light of this, cash & headroom on facilities of £1.8m look light and it is hard to ascribe any value to the equity. And at £1.8m market cap this is a gambling chip not an investment.

“Revenue for the year ended 31 March 2021 has continued its strong recovery, after the first quarter was significantly impacted by the first lockdown. Full year revenues are expected to be broadly similar to the revenue figure reported for the year ended 31 March 2020. Gross margins have also continued to show improvement and are expected to be ahead of the figures reported in H1. The Company's balance sheet remains strong.”

Last year they did £247m revenue, so I take that to mean around £245m for FY 2021. That means in H2 they did £148m vs £107m in H1. Traditionally they have had no H1/H2 weighting, although H2 of 2020 did have a slight covid effect. H2 2020 was £121m revenue and might have been £125m without covid, so it looks like some significant catch-up revenue here.

So, not much to say about James Latham, except this is an excellent example of a well-run family company and a caveat that you should not expect the current run-rate to continue.For me it remains too expensive, but if I were looking for an invest-and-forget IHT exempt company it would be high up on my list.

Leo pondered how this bounce back in the building trade had not trickled down to FireAngel.

This is their second CLBILS loan. I never understood how they got the first one because these are IIRC supposed to be for companies that would be viable "were it not for coronavirus". Whereas FireAngel has been dependent on "shareholder support" for several years now.

“The timing of securing the New Loan has impacted completion of the audit of the Company's results for the year ended 31 December 2020 (the "Year")…”

Surely they can do the financial results ahead of the loan being approved!?! Clearly there will be a going concern issue before the loan is signed off, but they are no stranger to near-misses here.And why did the new loan take so long?I suspect because the bank weren't clear that they met the requirements I gave above.

And also, why when every other building-supplies related company have recovered are they still doing so badly?

John Conoley, Executive Chairman of FireAngel, commented: "Whilst this process of stabilising the nature of Government support has taken longer than anticipated, the supportive stance of our bank over recent months has enabled the Group's return to growth in 4Q 2020, which has continued in 1Q 2021. Whilst our Scottish and EU markets are still subject to various restrictions, conditions are improving across all our markets, and this CBILS support underpins our ability to respond.”

Mark thought these results were ok, but might be a bit weaker than some may have hoped for:

H2 is perhaps a little underwhelming here, with GM down from H1 and PBT of £0.7m for H2 vs £1.1m for H1.

This is a family-owned business and the dividend is very important to the family so this has been maintained at a high level.Despite this, a more dynamic management team in the last few years is trying to grow the company, most recently with an acquisition:

“On 10 February 2021, we completed the acquisition of Schela Plast, a specialist in the design and manufacture of blow moulded containers, based in Denmark.”

They paid £7.7m and funded this with new £12m bank facilities.

Perhaps a little risky for a £23m market cap company.EBITDA was c.£5m so perhaps not a crazy debt to EBITDA multiple, but they had problems following their last acquisition so this adds risk.£35m EV leaves 7x EV/EBITDA so probably fairly priced unless they can generate significant organic growth.

One of the bull points has been property assets on the balance sheet and they have made some progress here. However, there have been here multiple times before over the years though. Lack of planning permission has held this back.Particularly the need to maintain the listed building that is the old factory and other features - making the land expensive to develop. Maybe they will get it over the line this time but I'm not holding my breath.

Mark didn’t think these results changed the investment case one way or another, concluding:

A strong strategy under the new CEO and some very prestigious client wins, helped by Accenture pulling out of some of the market, means that you are getting a lot of company for the current £25m market cap.

How soon this strategy ends up reflected in the bottom line remains to be seen. However, I still think this could be a major turnaround story given the strength of the products & client list. These results don't really change my mind on this nor do they significantly strengthen the case.

Although no longer a small cap, this is a company where brokers seem to be consistently behind the curve, hence we still track it.

Both Leo and Mark thought this trading statement held some hidden gems:

“As a result of the strong performance, net operating income for the financial year ended 31 March 2021 ("FY 2021") is expected to be slightly ahead of the upper end of the current range of consensus of £399.61 million, which, combined with continued cost control, is expected to provide positive operating leverage.”

After Cenkos the other day, it is good to hear about cost control. Clearly they are also ahead of EPS forecasts. But they have been looking cheap on FY 2021 forecasts for quite a while now. The issue has been how sustainable the performance might be. They've come away from the lows below 80p in 2019:

Yesterday they said:

“We continue to see ongoing high monthly active client numbers, which for the full year will be over 75,000. Client acquisition levels have remained high during the period driven by increased marketing expenditure. As previously stated, the quality of this year's new cohort of clients remains encouraging as the clients continue to show similarly high value and longevity qualities to prior cohorts.

This builds the Board's confidence that this new cohort of clients will contribute meaningful revenue streams for the Group into the next financial year and beyond, raising the Board's expectations for FY 2022 to deliver net operating income in excess of £330m.”

When I stuck this into my model I my EPS forecast went from around 25p to 40p for FY 2022 due to operational gearing, even taking into account higher variable compensation.I was sceptical about them providing guidance so far ahead, but...

Noting the 75k client numbers and assuming this stays constant in FY22 then this means they are forecasting c£4k revenue per active client (assuming 85% retention). This is back at 20H1 levels. (That's the 6m to 30th September 2019).

In comparison 21H1 was £3.4k for the half-year and, based on my estimates, 21H is c£3k for the half-year. Now there will be some client attrition - maybe some joined when IG threw some customers under the bus - but with 21H1 client number at 59k this has room for some attrition.It is possible £330m is conservative.

OK, so I see two scenarios:

1) FY 2022 fully normalises. They get EPS of 40-45p as Mark and I predict. From there they will grow EPS at maybe 10-15% a year.That's surely worth a PE around 15 for a midcap => valuation of 600p+

2) FY 2022 still has some covid effect. They get EPS of 60p. Even with doubts about sustainability into FY 2023, a PE of at least 10 is still justified => valuation of 600p+

This compares favourably to the current share price even after recent rises.