Small Caps Live Weekly Summary

ANP CML MRK OMG REC

Here’s a selection of what we looked at this week.

(Remember this is a summary of many opinions, and isn’t the view of any one commentator; check out the actual discussion on Discord if you want the nuance of the different opinions.) To avoid spam, the only way for new members to join the Discord server is via the Small Caps Live website. This will be instead of direct invites via Discord. All genuine investors are still very welcome to join in the discussions.

Anpario (ANP.L) - AGM Statement

The good news is that growth continues:

The Group has made a good start to the year with revenue and profit performance ahead of prior year and in line with full year analyst consensus expectations1, despite well-reported geopolitical and related economic conditions.

We are always a little sceptical when the headline is revenue/profit ahead of the prior year, especially for a company that has often been priced to be trading ahead of consensus. And given recent performance here, there is always the concern that the market now expects that expectations will always be beaten, despite this being a relatively small company buffeted by volatile international markets.

However, it would be unusual for Anpario to upgrade at this point, exactly because of the nature of their markets and their conservatism. Surely they would be doing better if they had not had transport and organic acid headwinds, and those are now set to unwind.

Hence, EPS forecasts could well be beaten what with the buyback and strong H2 margin outlook.

Cash has been deployed well in the past and should be considered in the valuation model, but it is not as cheap as it once was, and 12x earnings doesn’t seem wildly the wrong price for a microcap such as this unless growth accelerates above forecasts. However, there are a plethora of business development initiatives that collectively should allow decent growth over the next few years. Let’s hope they come off.

CML Microsystems (CML.L) - Full year results

You always know where it is going when the highlights don’t contain any profit measures:

· Revenue of £20.45m (FY25: £22.90m), with a significant improvement in trading performance during the second half.

· Gross profit of £12.89m (FY25: £15.89m) equating to a gross margin of 63% (FY25: 69%), reflecting a higher contribution of NRE income in revenue mix.

· Cash balances at period end increased to £12.80m (31 March 2025: £9.92m).

After scrolling for what felt like about 20 minutes, we finally got there:

The reduction in product revenues year over year is the overriding factor in the Group delivering a loss from operations, excluding exceptional items, of £1.93m against an FY25 profit of £0.53m, again excluding exceptional items.

The increase in cash is due to selling off surplus property.

However, if a company seems completely disinterested in reporting an operating profit, perhaps that’s a sign that investors shouldn’t be interested in investing in it.

Mark’s Electrical (MRK.L) - FY 26 Results

If you think FY26 looked bad:

Adjusted EBITDA(1) of £2.5m (FY25: £4.2m) as previously guided. A much improved performance in the second half of the year with a good “peak” period outturn and decisive actions taken, delivering improved operational efficiencies and fixed costs savings.

· Diluted adjusted EPS of 0.67p(2) (FY25: 1.54p), statutory loss per share of 0.40p (FY25 loss per share: 1.38p).

· No final dividend is proposed as we prioritise delivering trading profit recovery in the year ahead.

· Robust balance sheet, with Group net cash of £4.4m (2025: £8.8m).

Things are about to get a lot worse:

Whilst we continue to target profitable growth, with the benefits of our rigorous focus in FY26 on efficiencies and operational cost controls expected to benefit the Group’s FY27 adjusted EBITDA performance, we are taking a more cautious outlook for the year ahead on sales growth and gross margin.

As we’ve probably discussed before, Marks’ real advantage was getting full vans of higher value kit, so the revenue per van was higher and the distribution cost margin lower. National distribution helped with this. However, they ran out of growth as customers traded down so went downmarket to keep volume and lost their advantage.

Maybe AO also cottoned on to the high-value van idea, but the reality was they were between a rock and a hard place: lose volume, and the distribution advantage weakens; go downmarket, and the distribution advantage weakens. Perhaps that advantage returns in better market conditions, but that’s not a bet any of us are willing to take, especially at the current price.

The current price has been held up by Frasers buying stock. However, a recent fridge-buying experience by an SCLer at Marks revealed what Frasers are interested in, as their credit offering was plastered across every page of the website. Providing credit for one £500 appliance is much less work than providing credit for 500 big mugs, or 50 golf umbrellas!

Even if they improved to best-in-class margins, say 4%, that’s £4m PBT, £3m PAT, then a P/E of 8m gets us to £24m, so about half the market cap.

Lower population coverage than AO is a potential problem because it means marketing doesn’t scale as well, especially regional advertising at the limits of their range. But the real marketing scale issue is the lack of market share within their area versus AO, and they have spent the last 3 years proving they can’t increase that without hitting margins. What they have left is customer loyalty, but anecdotally, according to Trustpilot, and according to the CMA they are blowing that.

The bull case is that AO loses focus on MDA delivery in its hunt for mobile and other revenue streams, plus perhaps stronger economic conditions. The bear case is that Currys start competing on service.

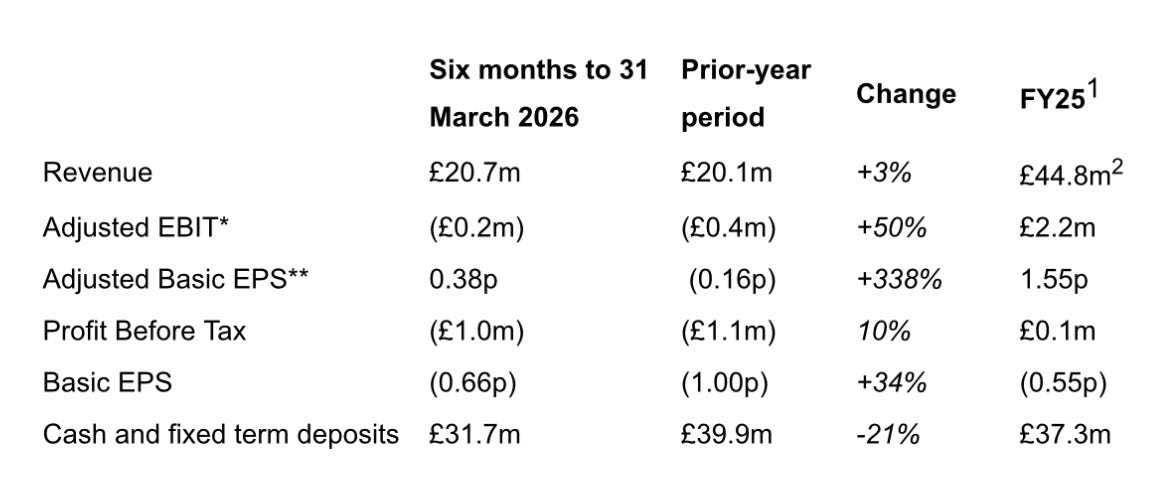

Oxford Metrics (OMG.L) - Interim Results

It is very Oxford Metrics to describe a £1m loss versus a £1.1m loss last year as a 10% rise!

Motion capture is growing again with a good Gross Margin. However, the unmentioned corollary is that smart manufacturing must be declining, making the previous rapid growth there look like an anomaly.

It’s great to say this is the strategy:

Doubling Group revenue through a mix of organic and inorganic activities

· Increasing recurring and repeatable revenue to c.25% of Group revenue

· Increasing Adjusted EBIT* margin to mid-teens

But there’s not much evidence of any progress. Their “medium-term ambitions” sound a lot like Bernard from Creighton’s “aspirations”, which turned out to be total bollocks in the end.

The only part of the strategy we truly believe is the well-flagged dividend cut:

The Group is rebalancing its approach to capital allocation, prioritising investment in strategic growth opportunities while maintaining balance sheet strength and flexibility for selective bolt-on and opportunistic M&A, with dividends paid as a percentage of free cash flow and selective share buybacks where appropriate.

Current management started with £70m in the bank and a business making £6m operating profit a year. The market cap is now £52m and half the cash is gone. Hands up who wants them to spend the rest? Anyone? Anyone….?

When the broker’s note from Progressive arrived, it looks a lot like they had just issued a closet profits warning via the broker:

So why did the outlook in the results not give any indication that full-year trading was below expectations?

The first six months of FY26 showed further progress for Oxford Metrics, with revenue growth, improved Adjusted EBIT and continued strategic progress across the Group.

The motion capture part of the business is a good niche with 60%+ gross margins. It just looks increasingly like it will never grow and faces an increasing competitive threat at the lower end via AI. There are few companies where £54m of revenue and £3.6m of EBIT are available for a £15m EV. However, the management repeatedly makes this look uninvestable through their statements and actions.

Record (REC.L) - Annual Financial Report

We are not entirely sure how an asset management business can turn +14% AUM and lower costs into an EPS miss and an unexpected dividend cut!

· AUM up 14% to $114.6 billion (FY25: $100.9 billion) with strong inflows from new business wins, and favourable foreign exchange and market movements

· Total revenue down 4% to £40.1 million (FY25: £41.6 million) due to mandate re-compositions and lower performance fees

· Operating costs down 2% to £30.4 million (FY25: £30.8 million) whilst still investing selectively in key areas that support strategic objectives

· Profit after tax down 23% to £7.0 million (FY25: £9.1 million) reflecting tax rate normalising following prior year deferred tax credits

· Basic EPS down 22% to 3.92 pence (FY25: 5.03 pence), broadly in line with expectations

· Final ordinary dividend of 1.45 pence per share (FY25: 2.50 pence) brings full year ordinary dividend to 3.60 pence (FY25: 4.65 pence), reflecting a dividend payout ratio maintained at 92%

Presumably this is the mix, as passive hedging is where the growth is and is much lower margin:

Part of the issue appears to be a major change in the tax rate, but we don’t remember them highlighting in the past that they were benefiting from tax credits that were about to run out. The risk here is that it is a value trap as revenue gradually declines, margins get compressed, and forecasts keep coming down. We are not entirely sure why institutions choose them to manage an absolute return currency product . Surely there are other larger outfits with better track records?

Still, there are a few asset managers growing AUM at the moment, even if they are suffering from the trend towards passive and facing the associated fee pressure. It would only take another 20% or so share price fall from here to see this back on a 10% dividend yield, and at those sorts of levels, it may be worth owning for the yield alone.

That’s it for this week. Have a great weekend!