Small Caps Live Weekly Summary

G4M ANX LOOK D4T4 NTBR SDY

A short trading week this week, so the summary email arrives a day earlier. Happy Easter!

Those who are missing the markets should be able to catch the latest Value Trapped podcast episode, with Mark and his friend Bruce Packard that will hit the airwaves later today.

Here is the first episode for those who missed it:

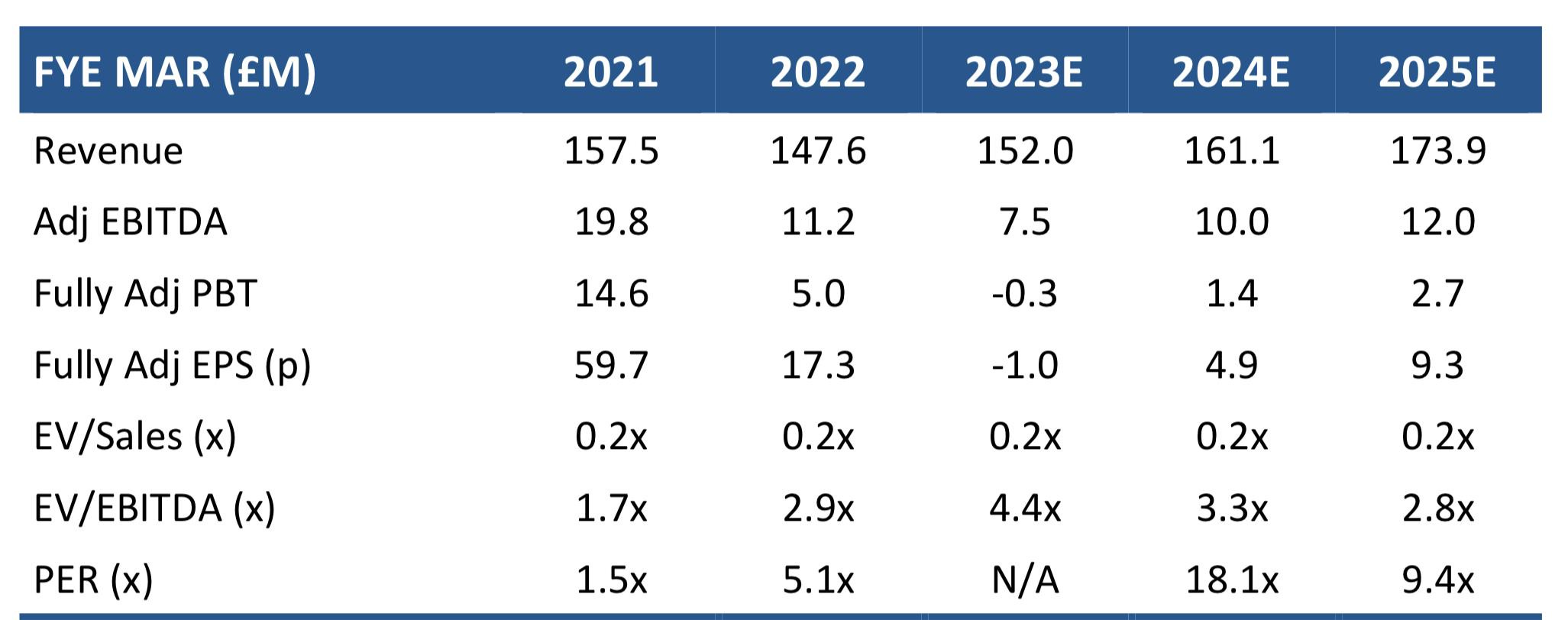

Gear4Music (G4M.L) - Year-End Trading Update

It’s a profits warning from this musical equipment retailer. In January, they said:

FY23 EBITDA and net debt reduction in-line with consensus market expectations

And:

Gear4music believes that current consensus market expectations for the year ending 31 March 2023 are revenue of £155.1 million, EBITDA of £8.9 million, profit before tax of £1.0 million, and pre-IFRS16 net debt of £17.5 million.

Now they say

EBITDA now expected to be in the range of £7.3m - £7.7m

This is due to a small miss on revenue (£152.0m versus £155.1m), but it’s the poor gross margins (25.7% vs 27.8% prior year) that do the damage to give the 16% EBITDA miss overall. The blame is put on recent weak trading:

FY23 revenues and profits impacted by weaker consumer demand during February and March.

But it seems strange to us that sales in one of their weakest quarters could have such an impact. Perhaps they also missed the levels of post-Christmas returns to expect in the January statement? Shareholders who took January's trading update at face value have a right to be quite angry here. It is difficult to see how February / March trading could have deteriorated so much as to throw them into a loss.

The cash/debt situation is better, though:

Net debt of £14.5m at 31 March 2023, reduced from £24.2m at 31 March 2022

In January, Progressive were guided to £17.9m net debt and have £24.2m for the year before, so it is on the same basis as today's update. So this is a material cash beat. However, we don’t know where it came from without seeing the balance sheet. Inventories would be good, payables/receivables less so. Average net debt is more important than a point in time, too.

With a 16% miss on EBITDA at the midpoint of the range, we have to expect them to be loss-making for the FY if that £1.4m reduction drops through to the bottom line. The tax charge is likely to be less, however, so they may scrape break even on an adjusted basis if they can deliver toward the top of the range. Progressive assume middle of the range and a loss-making year:

This brings us to the biggest problem. The 2024 EPS consensus on Stockopedia was 11.2p, so 4.9p looks like quite some drop. Even out to 2025, the forecast has halved, 9.3p versus 18.4p. So this looks pretty serious.

In light of this, the shares opening just 12% down looked light. That they rallied to 6% down at one point seemed bonkers. Nimble shareholders had a lucky escape here and were able to exit at a price not far below the level the shares traded at before this disastrous update.

There is some tangible asset backing with them trading around tangible book value. The big question is how much of a discount to demand, given that the assets are not particularly productive at the moment, nor are they forecast to be in the near term. FY24 estimates put this on a debt-adjusted P/E of 30. This drops to 17 if they hit FY25 estimates. So not particularly cheap, even if investors believe the brokers on this one.

Shareholders have the right to question strategy here. They potentially have too much stock tied up in large, slow-moving pieces of kit in order to be the best on delivery time, and overall this has made their assets unproductive as a whole. Unfortunately, it is a particularly competitive market, and so they have to distinguish themselves from the crowd, and they choose to do this on availability/delivery rather than price. The best news for shareholders would be if the likes of GAK and PMT eased off on chasing prices.

Nor does this sound like the idea to turn them around:

Second-hand trade-in system launched in March 2023 with promising initial results

Some competitors have a big pre-owned section. Although they say:

Our proprietary second-hand trade-in system simplifies the process for consumers of selling their equipment, providing instant trade-in prices across thousands of products*.

As Music Magpie shows, pre-owned is a hard business to make consistent returns in, even if you are the market leader for your category.

Anexo (ANX.L) - Pre-Close Trading Update & Mercedes Class Action

Revenue is expected to be between £135.0 million and 137.0 million.

Profit before tax for the Group is expected to be between £24.0 and £26.0 million, at the upper end of this range broadly in line with market expectations.

They've cleverly managed to get in two degrees of separation from actually being in line with expectations without explicitly admitting to a miss. The last broker note from WH Ireland in September forecasted a PBT of £26.6m. At the middle of their new range, that's a miss of 6%.

That they still don't know their revenue or profits from over three months ago should act as a red flag to those new to the company. Although, for anyone who has looked at their balance sheet, it is simply one to add to the many existing red flags.

Lookers (LOOK.L) - Full Year Results

Revenue of £4.3bn is a small revenue miss versus Stockopedia's consensus of £4.4bn, which includes a post-period-end forecast of £4.6bn from Zeus, who seem to take a more independent view. Their preferred measure of underlying profit before tax of £82.7m compares to January guidance of "greater than £80m".

Excellent start to Q1 with underlying profit before tax ahead of 2022 driven by used vehicle and aftersales revenue growth, stable margins and ongoing working capital and cost disciplines.

On the one hand, this means Q1 must be the second-best ever and way more than the average Q1. On the other, Q1 is the quietest time of year, and so has limited impact on the final result. But what surprises us is that they are not more heavily leaning on new car deliveries. They give exact figures for the year-end order bank:

retail (17,321) and fleet (23,393)

And then say the Q1 end is slightly up:

Continued robust order bank with c.18k new retail units and c.24k fleet units as at end of Q1.

Also, on cash - year end:

Robust balance sheet with net cash of £66.5m

Q1 increases this further:

Continued cash generation with net cash* at 31 March 2023 of c. £93m.

So an exceptionally strong Q1 with more to come from new car deliveries. So it is hardly surprising:

The Board's expectations for underlying PBT for the year ended 31 December 2023 are now ahead of its previous expectations.

Zeus have now published the upgrade, but remember, this isn't quite as directly from the horse’s mouth as with house brokers:

On the back of the strong outlook statement, we are raising our FY23 PBT forecast by 23.1% which equates to a 22.3% EPS upgrade. For FY24 we upgrade by 19.8% and 19.1% respectively. We introduce our FY25 forecasts for the first time, which assumes modest growth on FY24.

Compared to Stockopedia consensus, Zeus' EPS forecasts are up 16%. On valuation:

Based on latest Zeus forecasts, Lookers trades on a FY23 P/E of only 6.1x, and EV/EBITDA of 3.5x, with a 4.7% FY23 yield based on 3.5x earnings cover. At 31 December 2022, the Group held property and cash equivalents of 122p per share, 43% above last night’s closing share price, highlighting the Group’s significant asset backing.

However:

The Lookers Pension Plan received deficit contributions of £12.9m in 2022, plus expenses and PPF Levy of £1.3m. The deficit contributions are subject to increases linked to CPI, which will result in a £13.6m contribution in 2023 (plus expenses and PPF levy). Further, the Group pays additional contributions of 10p for every £1 of returns to shareholders (ordinary dividends and share buyback) in excess of £5.0m. This will result in an additional payment being made in May 2023 relating to 2022 financial year.

Investors / potential investors will need to do the sums and make appropriate adjustments and judgements. One judgement is how much longer payments need to continue.

At 31 December 2022, the aggregate IAS19 pension deficit is £23.5m (2021: £43.2m). The year-on-year decrease arises due to the continued deficit contributions made by the Group and significantly increased discount rate assumptions, which have been driven by increased corporate bond yields. The increase in discount rates has not been offset by increases in inflation, rather the inflation assumption has decreased year on year.

It is common to omit the H1 figures in this kind of update. With Mpac, this appeared to have been done in an attempt to underplay the massive losses they'd incurred in H2 with leveraged equity speculation through LDIs. Not so here. From the interims:

At 30 June 2022, the IAS 19 pension valuation showed a total deficit of £24.3m

And today, they comment:

The extreme volatility in the long-dated gilt markets following the Government's "mini-budget" in September 2022 resulted in some pension schemes suffering liquidity shortfalls; however, neither of the Lookers defined benefit pension schemes was materially affected, as a reasonable collateral buffer had been maintained.

In contrast, we continue to have serious concerns over the Vertu scheme, given the comments made by the CFO and previous pension fund trustee, demonstrating what appeared to be a lack of understanding of the situation and where responsibility for it lay.

D4T4 Solutions (D4T4.L) - Trading Update

The shares opened down around 20% on this profits warning:

Due to the delays in signing of a project with an existing banking customer which included a high proportion of low margin hardware, and a Celebrus multi-year contract with a new customer, results1 are expected to be lower than management expectations, with full year revenues in the region of approximately £21.5 million (FY22: £24.5 million) and adjusted profit before tax2 of approximately £3.5 million (FY22: profit £3.3 million).

This seems a little harsh if this really is just delayed contract signing. A slight concern is that FY 2024 forecasts have not been raised to reflect the delayed orders. finnCap say:

It is early in the year and the delayed hardware deal might have a knock-on impact on further project and hardware delivery schedules with that customer

However, they do expect a better H1 balance giving better visibility. This company has always been very highly rated for a company whose historical earnings look like this:

This won’t look too bad if they hit FY24 EPS forecasts of 11.0p, which would put them on a P/E of 17. They always generate reasonable cash because they get paid upfront for their software/services, cash is ahead, and this company has always been keen to support its own share price with buybacks. Investors will need to make their own minds up if this is positive or negative.

Northern Bear (NTBR.L) - Strategy, Dividends, and Trading Update

After a review of strategy and dividend policy, the Board is pleased to report that the Group will pursue a dividend growth strategy supported by the organic progress of the Group's businesses and, to the extent accretive, bolt-on acquisitions.

Given the amount of time they have had to consider their strategy, this isn’t exactly ground-breaking. However, they start off by paying a 4p ordinary and a 1p special dividend. Which is a decent yield on the share price earlier in the week. The dividend announcement has had the effect they wanted, though, with the share price up 25%. I never quite get investors who buy shares that have gone up 25% in order to receive a 10% dividend!

Looking at their cash generation history, you would question their dividend growth aspiration. In three of the last seven years, they either had zero or negative free cash flow. So they are going to have to manage operations very differently in future. Nor does their current ratio make their balance sheet look robust and suggest they can pay dividends out of past profits. So paying out a large dividend in a good year in a cyclical business is more likely to disappoint shareholders in the future than delight them. Part of the rise may well be because it appears there may be a change of position towards shareholders rather than the dividend itself.

As for trading:

Based on management information for the eleven months to February 2023, the Group has traded ahead of the prior year's results except for a provision at our Northern Bear Building Services Limited subsidiary, anticipated to be in the range of £500-£750k, to account for certain unprofitable contracts. The Board expects that operating profit for FY23, stated before amortisation, one-off costs, and other adjustments…

This doesn’t read too badly. Although, a contract building group excluding unprofitable contracts seems a big credibility stretch. I’m sure we all had great investment results last year if we ignore unprofitable investments!

Speedy Hire (SDY.L) - Year-End Trading Update

An in-line update for FY23 just ended. Revenue growth here looks good, given the economic backdrop:

The Group performed well during the year, with revenue2 up c.14% over FY2022. Revenue growth was underpinned by rate increases to counter inflationary cost pressures alongside a strong performance from the Services business.

However, the market didn’t like this:

Against the backdrop of the continuing challenging trading environment, the Group has experienced some softening of demand in recent weeks,

And they are expecting us to ignore some large exceptional costs:

Group initiatives, including an ongoing operational review and a management restructuring, will improve the efficiency of our operations and are progressing well. The cost of these items in FY2023, including the depot consolidations already announced, will all be accounted for as exceptional items, and is expected to be c.£6.6m and will deliver associated benefits in the region of £5m per annum.

They are still expecting growth in FY24, however, saying:

The combination of these actions and contract momentum means we enter FY2024 with confidence.

Adding in the cost savings could deliver a strong year if they can generate even modest revenue growth.

They still have no idea yet why half their non-itemised kit went missing, but at least no more disappeared in March. Not exactly surprising that things stop going missing when you start counting them.

That’s it for this week. Happy Easter!