Here’s a selection of what we looked at this week:

Carclo (CAR.L) - Trading Statement and Delay to Audited Results

This is never a good sign, especially for a company as wobbly as Carclo:

Forvis Mazars LLP, the Group's current auditor, has informed the Audit Committee that it requires additional time to complete its audit procedures for the year ended 31 March 2025.

But they are quite insistent it is not their fault:

The Group is disappointed with this situation and is working with Forvis Mazars to ensure that the audit is completed as soon as possible. To date, Carclo has not been informed of any significant audit issues affecting the Group's consolidated financial statements.

We’ve often thought that AIM companies are better regulated than those on the main market due to the presence of a NOMAD with a reputation on the line supposedly checking everything, but the main exception is the requirement to produce audited results within 4 months of the year-end. For some reason, Carclo is main market listed and so:

Carclo expects that its shares will be temporarily suspended from listing and trading from 1 August 2025 until the audit is completed and the 2025 annual report and accounts are published.

In order to reassure investors, they then repeat the last trading update, which was issued a month after the year end on 30th April. The lack of any more timely trading information suggests that the accounting isn't entirely straightforward.

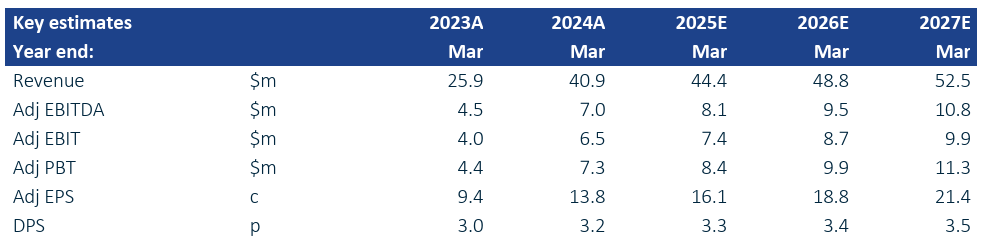

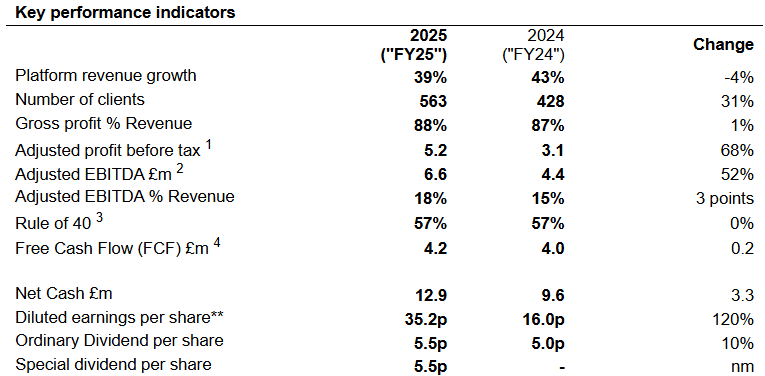

Celebrus (CLBS.L) - Final Results

The numbers here were largely known after a trading update:

Total Revenue of $38.7 million (FY24: $40.9 million), with Software Revenue (excluding third-party hardware) of $30.3 million (FY24: $27.7 million), an increase of 9.4%.

· Gross profit margin of 61.9% (FY24: 52.9%) due to a lower proportion of lower margin third party hardware revenue. Software revenue gross margin of 75.0% (FY24: 72.8%).

· Adjusted profit before tax** of $8.7 million (FY24: $7.6 million), and statutory profit before tax of $7.3 million (FY24: $7.0 million)

· Adjusted diluted EPS of 18.24 cents (FY24: 13.39 cents) and diluted basic EPS of 15.78 cents (FY24: 12.27 cents)

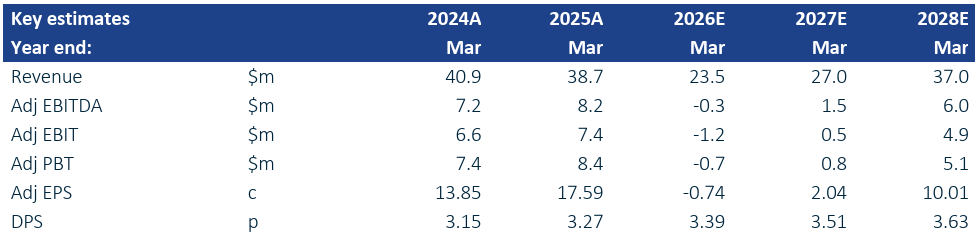

However, they also changed revenue recognition and are now only booking the margin on third-party hardware, not the sales and costs. Therefore, brokers have removed forecasts for FY26 and beyond.

Here’s this week’s outlook:

The new financial year has started with a strong pipeline, new customer wins boosting ARR to almost $20.0m and a good proportion of revenue already committed to the current financial year.

So, we were expecting EPS to grow, making this look good value, we just didn’t know by how much. Instead, the effect is an absolutely huge profit warning compared to the previous forecasts, which were withdrawn. Indeed, they are forecast to be loss-making this year!

This is Cavendish prior to the accounting change:

Updated this week:

Reading between the lines, the accounting change implies that the figures attributed to the hardware sales look like they generated around $8m EBITDA, with software losing a couple of $m, even at the EBITDA level, which, of course, is not a good measure for a software business.

We’re not totally convinced that this is a strategy change they have pursued willingly. Why would you give up a highly profitable hardware reselling part of the business to focus on a loss-making software business alone? It may be that this is driven by the move to cloud hosting, meaning that customers just don't want the hardware side anymore. And it has revealed how unprofitable the software side has been and will be.

Partly this is accounting treatment due to the change to booking revenue as subscription rather than licenses, and they are forecasting modest free cash flow, but all of this is working capital, ie being paid up front. According to Cavendish’s forecasts, all of the FCF in 2026 is from upfront payments, and 87% of the FCF in 2027 is from being paid upfront. FCF ex-w/c in 2028 is forecast to be just $3.9m, if you believe the forecasts 3 years out for a company where forecasts are regularly slashed. They may be changing their billing structure, but it is not reducing their reliance on upfront fees being paid in order to generate cash, which was exactly the thing SaaS billing was meant to make less variable.

The narrative is one of temporary misses while they transition their business model, which is exactly what they started saying over 5 years ago. Sooner or later, we have to conclude that this is simply a poor business. Is a decade of underperformance long enough to come to this conclusion?

With the outlook here less Celebrus (Esperanto for being celebrated) and more Cerberus (the dogs of hell), we were expecting the share price to plummet. Yet investors seemed keen to bid the shares up on the news. How bad did they expect them to be for these forecasts to beat their expectations - permanently loss-making, not just near-term loss-making? Either that or the investors simply didn’t read the brokers’ notes.

James Cropper (CRPR.L) - Trading and Paper & Packaging Customer Update

This is a confusing one, sounds like paper & packaging was trading ahead of expectations, but these expectations were for losses anyway:

…provisional results for the first quarter of the current year to 28 March 2026 ("FY26") show this Business Unit trading ahead of both the same period in the previous year and of the Board's expectations. This first quarter performance has been driven by business with other customers and efficiency savings pursuant to the revised operating approach. The Board's expectations for the Paper & Packaging business in FY26 remain for it to report a significant improvement in Adjusted EBITDA against FY25, and the achievement of run-rate Adjusted EBITDA breakeven in the final quarter.

They’ve now lost a major customer, which wasn’t expected, although that customer had been placing reduced orders. They still expect this division to reach break-even at the end of the year, but only at the adjusted EBITDA level. I.e. BS level. However, Advanced Materials is doing ok.

It seems a coincidence that a major customer left just as they were implementing a revised strategy that would reduce losses. Speculating wildly, we wonder if the new strategy is to raise prices to cover their costs, but one customer has found a lower-cost supplier. In this case, we would be worried that other customers will also leave, and a large part of the business will be confirmed as fundamentally unviable.

Forecasts remain suspended, and their broker seems less "Shore" than ever about how and when profitability might recover:

we still believe that our investment case of growing revenues and/or improving margins will lead to a substantial increase in Cropper’s PBT in due course.

However, there is a possible SOTP valuation in excess of the current £20m market cap:

Advanced materials say £70m (£7.7m historical adjusted operating profit, revenue slightly ahead of last year, high margins, exposure to some growth areas, then 9x Op Profit seems reasonable)

Paper and packaging £0m,

-£13m debt

-£17m pension deficit

This gives £40m But if we add in the cost to actually offload the pension to someone else, a discount for the risk of the high debt, the current cash burn from Paper, the difficulty of making disposals with a pension problem, and a discount for the family controlled stock market listing with £600k of central costs then maybe £20m is about right.

Given their track record of poor capital allocation, and Mark Cropper still being the chair (with frequent CEO changes), we are not comfortable with SOTP here. It would be hard to sell to the family on offloading a now worthless, 1889-founded family paper business for nothing, even if that was the best thing to do.

Enereaqua Technologies (ETP.L) - Subsidiary Administration & Suspension

Several SCl contributors have been sceptical about the real value-add of the flow regulator technology the company has, believing it to mainly be a contractor business in a highly challenged sector. Like all contractors, they appear to have only been one undperforming contract away from serious trouble. This week, we find out which contract it was here:

The Company has today been notified of a material adverse adjudication award against its operating subsidiary Cenergist Limited ("Cenergist") in the sum of approximately £1.2m including costs relating to a contractual dispute. The adjudication award requires payment within five days and although the Company believes there are grounds for a counterclaim. This cannot currently be pursued due to the cash constraints of the Group.

Leading to:

Due to the ongoing financial uncertainty regarding the Group, its limited working capital and the circumstances noted above, the Company has requested that its shares are suspended from trading on AIM with immediate effect.

We suspect things are rather more certain than they try to make out, and the suspension may prove less temporary than they claim!

Hunting (HTG.L) - H1 2025 Trading Update

All sounds pretty positive here, with EBITDA up 16%:

· Good year-on-year growth in EBITDA to c.$68-$70 million in H1 2025, up c.16% from H1 2024, led by a robust contribution from the OCTG product group.

· EBITDA margin of c.13% generated in the period.

· Total cash and bank / (borrowings) of c.$79 million as at 30 June 2025, with significant additional liquidity available via the Group's credit facilities to fund growth.

· Period-end sales order book of c.$450 million, ahead of Q1 2025 position of $439 million, with a tender pipeline of c.$1.1 billion.

We get FY guidance:

2025 full year EBITDA guidance of c.$135-$145 million retained. Targeted year-end total cash and bank / (borrowings) position of c.$65-$75 million.

However, a quick look at recent RNSs doesn’t reveal where they guided this in the past. Doing the maths, this gives a similar H2 result to H1, giving 11% EBITDA growth for the year versus 16% in H1. This should also be helped by acquisitions, so it is a little underwhelming.

However, this is anything but:

· Targeted annual dividend increase raised from 10% to 13%.

· Share Buyback programme of up to $40 million scheduled to commence following publication of the 2025 half year results, with the intention to complete over next 12 months.

That’s a significant buyback, about 6% of the share count and in excess of what many were expecting. The dividend increase also signals a shift towards greater shareholder returns, but given that they are likely to still be buying back shares below TBV, we would have preferred that cash was also allocated to buybacks. Given that they had previously announced a change to capital allocation, it seemed pretty obvious that a buyback was on the way, so the strength of the share price response is a little surprising. It shows that individual investors can still have an advantage in the mid-cap space, as many smaller institutions rely on brokers’ notes for their view, which are often slow to be updated for “known unknowns.”

Macfarlane (MACF.L) - Trading Update

Bad news here:

In a year of challenge and economic uncertainty, we currently expect full year 2025 Adjusted Operating Profit1 to be approximately 10% below 2024.

Previous forecasts were for a recovery in profitability. Shore do the hard work for us:

Our revenue line for FY25F reduces by £3m to £307m, EBIT by £4.7m to £24.7 (-16%), with adj. PBT at £21.1m (-18%) and adj. EPS at 9.8p (-19%). We also cautiously reduce our expectations for FY26F, revenues falling by just £1m to £320m, with EBIT reducing by £4.7m to £25.9m (-15%), with adj. PBT at £22.4m (-15%) and adj. EPS at 10.4p (-15%). The balance sheet remains robust with net debt well within facilities.

19% out of FY25 EPS and 15% out of FY26 are the key figures, which makes the 15% or so drop in share price look reasonable. However, with little medium-term growth forecast, we have to question whether a further rating fall is now warranted. Shore also estimates net debt at the end of 2025 going up from a £16m previous forecast to £22.8m, which may put a dampener on acquisitions, which historically have been their major growth lever.

If we were being optimistic, we’d note that there wasn’t much change to revenue forecasts for this year or next. Meaning that if they can pass on costs over time they would see better margins agian. The big unkown is if the costs are admin-related (NI, Minimum wage) or product-related (where flat revenue and higher costs for a distributor means a volume drop). We’ll probably need to wait for results to get to the bottom of that.

Plexus (POS.L) - Board Changes

Plexus Holdings PLC, the AIM quoted wellhead services business, is pleased to announce that Dr Stuart Paton has been appointed as a Non-Executive Director of the Company with immediate effect.

Dr Paton brings over 30 years of experience in the energy industry, having held a range of senior positions, including Chief Executive Officer of Dana Petroleum plc and Chair and Non-Executive Director of Getech Group plc.

At this point, we will simply post a timeline we pieced together from RNSs and Companies House:

27 April 2011: Getech Chairman, Dr Stuart Paton, is awarded 900k share options that expire on 27 April 2021 at 17.5p.

9 June 2020: H2 Green Ltd is incorporated with 1p of share capital.

20 November 2020: Dr Stuart Paton is appointed as a director of H2 Green Ltd. The GTC share price is 11.25p. At this point, options exercisable at 17p have negligible value.

26 January 2021: Getech’s exclusive strategic partnership with H2 Green is announced. The GTC share price rises 85% to 25.2p.

28 January 2021: Getech announces that, after a handover period, Dr Stuart Paton will leave the Getech Board. The GTC share price is 33p, making Dr Paton’s options worth around £140k on this date.

Today, the Getech share price is 2p per share (although this is probably a significant undervaluation compared to the value of the Globe database and contracts that Getech have). So perhaps Plexus can look forward to some exciting strategic opportunities in about a decade’s time, followed by a (further) collapse of the share price.

Shearwater (SWG.L) - FY25 Trading Update

Slightly ahead here, and positive outlook:

The need for the Group's services continues to grow as organisations seek to navigate an increasingly complex cyber threat environment, with the costs of failure well-publicised over recent months. The improved outlook and growing pipeline of opportunities provides confidence in the ongoing delivery of growth in both revenue and EBITDA in FY26.

This ends up much more than slightly ahead at the EPS level, as it goes through the broker’s model: +62%

However, this is largely valued on 2026 estimates, and these are unchanged. The shares understandably jumped on this news, making this exactly the type of stock that Ed's research on Stockopedia suggests we should be buying on a beat. His three simple rules are:

Trading ahead, preferably materially.

Share price jumps more than 10% on the day.

Stock Rank above 75 (provides a basic quality check).

The theory is that shareholders are too quick to take profits on a large one-day jump. After all, momentum over short periods of time tends to see a reversal (presumably the stocks that have short-term rises on no news, or because they release news that doesn’t upgrade expectations, see those rises fade). However, the strength of the share price reaction suggests genuine surprise amongst investors and indicates a stock where the rise tends to keep going over the next six months or so (on average). It's a fascinating piece of research and one that holders of companies that see big one-day rises, such as Shearwater, should probably read.

System1 (SYS1.L) - Final Results & 26Q1 Trading Update

Here are the KPIs for the year:

FY25 EPS at 35p beats Mark’s estimate of 30p and is a whopping 28% above the consensus in Stockopedia of 27.4p. However, Q1 26 looks a bit crap (technical term) in comparison:

To be fiar, they are in line with Mark’s expectations, at least after he’d updated them for the weak Q4. Although he had a higher data revenue mix, the margins are probably below his expectations.

The outlook is very important, given this Q1 weakness:

Outlook for FY 26

Based on strength in our US and UK businesses together with a slower recovery in Europe the Board expects the following for FY 26

- Overall revenue to grow at approximately 15% year on year

- H2 revenue expected to be seasonally stronger than H1, in line with historic trends

- Profits expected to be in line with Board expectations based on prudent cost controls and continued investments as previously noted in US growth, innovation and go to market

If they can generate revenue of +15%, they should be on to beat the 33.6p previous consensus. Although optically, if they have slightly declining EPS forecasts, this isn't a great look for a "growth" company. The share price drop on the day suggests that the market doesn't believe that +15% figure, or that the returns on them increasing costs faster than revenue as they invest in a new(ish) product, Innovation, will not be as good as they expect.

Trifast (TRI.L) - Final Results

We like the turnaround story here, but not the US exposure. This is the key line for what their aims are:

Significant growth in Underlying EBIT to £15.6m (CER) (FY24: £11.9m), with EBIT margin increasing to 6.8% (CER) (FY24: 5.1%), demonstrating successful execution of our strategic initiatives and supporting our confidence in the Group's ability to achieve > 10% EBIT margin in the medium term

If we assume constant revenue, then they have an aspiration to reach £23-24m EBIT. However, there is still a long way to go as the short term isn't so good:

Trading headwinds have persisted into Q1 FY26, driven by macroeconomic pressures, softness in the automotive sector, US tariffs on steel and aluminium, and USD weakness. However, our geographic diversification, global manufacturing footprint, and close customer partnerships provide resilience. We enter FY26 with positive momentum, strengthened by our transformation progress, and remain confident in achieving our medium-term EBIT margin target of >10%, while continuing to explore targeted investments and bolt-on acquisitions to support future growth.

As well as recovering margins, they have acquisition aims:

We continue to actively look at investments, such as bolt-on acquisitions in target end markets and regions to drive the EBIT growth.

Accordingly, it is especially worth looking at their finances and goodwill amortisation. Looking at adjustments in general:

As we've seen at Mpac recently, it is only conservative to amortise acquired intangibles, at least in the early years, and if you are a serial acquirer, otherwise the financial incentive is to keep buying cheap companies that are entering decline. High restructuring costs can also flow from continued acquisitions, but in this case, clearly, there was some exceptional one-off (or at least, only ever 10 years) restructuring driving the turnaround. In this industry, we think there should be some ongoing expectation of receivables impairment. The payment fraud thing appears to be the maximum liability. Accordingly, we estimate recurring exceptionals to be around £3.5m.

On finances:

Net interest costs decreased to £4.5m (FY24: £5.4m), primarily due to a declining interest rate environment. Interest is incurred at an aggregate rate based on EURIBOR, SONIA or SOFR, plus a margin ranging from 2.10% to 3.60%, depending on the Group's leverage.

Commitment fees, amortisation of arrangement and extension fees increased to £1.2m (FY24: £0.8m), reflecting the impact of covenant amendment fees paid in FY25 and the full-year amortisation effect in FY25.

In addition, IFRS 16 lease-related interest contributed £1.0m (FY24: £0.8m) to total net financing costs.

Our average borrowings (excluding IFRS 16 and arrangement fees) in the year were £42.7m (FY24: £58.6m).

It is now just under 2x EBITDA. So it looks like they currently have no scope for material acquisitions, but they may do in a year’s time. There is a risk that they'll do one anyway, either diluting shareholders or blowing themselves up.

Anyway, based on their aspirations. £23m EBIT less £4.5m interest less £3.5m recurring exceptionals, taxed at 25% £11.25m, spread over 136m shares = 8.3p EPS. Given the industry and the debt, we wouldn't assign a high PE, but a valuation of 90p ought to be achievable. Taking Zeus as an example, their FY28 EBIT forecast is indeed £22.5m, although this is achieved on slightly sub-10% margins, as higher revenue is offsetting some of the work. They achieve an adjusted EPS of 10.8p with debt repaid, which looks significantly cheaper, and with the March year-end, isn't quite as far away as it appears.

Although higher margins meant profits were slightly ahead of Zeus' forecasts, revenue was still behind, and they think that's what should be extrapolated to FY3/2026:

we reduce our FY26 revenue forecast by 11% to £214.0m, which flows through to an 11% drop in adj. EBIT to £15.8m

Harwood have been lamenting that the share price has gone nowhere in over two years despite all the progress on transformation. We would say that (at least with the benefit of hindsight) it was overpriced before and only now is even approaching some kind of value.

With their IMC presentation, the questions that weren’t answered were as indicative as the ones they did answer. For example, when asked about the impact of the short-term issues on UK EBIT margins, they provided detailed explanations for the weakness but failed to provide a specific figure. This suggests that the issues are more structural and related to UK automotive exposure rather than one-off in nature. They skipped a delicately worded question on why they used the brokers to reveal the numbers of their profit warning rather than being up front with investors. However, seemed happy to answer a question as to whether the CFO wanted to buy shares! However, with the share price rising despite a multi-year profit warning, it seems a successful presentation overall!

That’s it for this week. Have a great weekend!

Absolutely love the demolition job on the Getech/H2 Green connection.

I will be deploying my bargepole on the basis that the appointment seems to add to unknown risk rather subtract it.

Some and some. like your review of HTG. Not so sure of the rather dismissive flippant remarks about Plexus nor what the relevance is of highlighting the newly appointed non exec Dr Paton’s role with Getech and choosing to ignore his senior role as CEO with Dana Petroleum. Whilst I admit that they have not been great at communicating with the market there have been a number of extenuating circumstances. Aside from the devastating impact of the collapse of the oil market which they only just survived, there is new leadership. The directors bought most of the shares about £2 million of the £3 million placing earlier this year. They have remodelled their well head cap technology equipment and now have eight new ones on order to satisfy demand now gas escape emission laws have been tightened. Allegedly they saved an oil company 100 million dollars with the rental of their equipment. There was an NDA for some reason about this due to expire this September, not that it matters that much. The financial history of this company is not flattering, but nowhere more than the energy sector can fortunes change very dramatically. It might take another year but certainly things are going to happen for POS. HTG are one of many crying out for the UK idiot government to change North Sea energy policy. This would also be beneficial. That might easily take ten years and a new government. I think my main concern is that like many innovative UK listed companies it will get bought out well short of potential.