Small Caps Live Weekly Summary

Mello London MADE VTU HTG ALU HSP NWT BSE

A surprisingly quiet week on SCL, with no Large Caps Live and many of the companies we follow simply reporting in-line statements.

The good news is that we have a Mello discount code to share with you. Use SCL50 to get 50% off tickets to this great event.

The company lineup is looking increasingly interesting, with companies such as Billington, Belvoir, SDI, Time Finance, Thruvision and Van Elle being ones we’ve covered on SCL in the past. There should be more announced soon, as well.

Lots of interesting speakers, too, including Mark. We will all be there, either in the presentations, talking to management or in the bar. Come and say hi if you spot us.

Small Caps

Made.com (MADE.L) - Strategic Update & End of FSP

The Board invited a select number of parties to work towards firm offers by the end of October. Following further discussion, those parties have all now confirmed to the Company that they are unable to meet the necessary timetable. As a result, those discussions have been terminated and the Company is no longer in receipt of funding proposals or possible offers for the issued and to be issued share capital of the Company.

So nobody wants it, or at least not on the timetable that the company need them to be to shore up the finances. There is a high chance that any interested parties will be able to make an offer to administrators rather than the company itself.

In such a situation, the company clearly can’t keep taking customer orders which is why the website says:

Not taking customers’ money when there's a high chance they won't be able to deliver the orders is an "improvement" of sorts!

However, we note the change in the language:

25th: "the Board will take the appropriate steps to preserve value for creditors."

26th: "The board of MADE will continue to look to preserve value for its creditors and shareholders."

27th: "The Board of MADE will continue to look to preserve value for its creditors and shareholders."

So shareholders are back in the picture. In the last announcement, they make it clear that the strategic review is ongoing. Bear in mind much of the board is relatively new and so they may feel less obliged to support the now-closed operating business. They may have closed the operating business to retain cash at the holding company level that may be available to return.

Still, we don't see any discount to likely free cash at the current share price of 0.74p. And there is a risk that if they make shareholder returns but don’t deliver customer orders, they make their brand equity worthless. Irate customers are unlikely to see the distinction between the holding company and the operating subsidiary.

Vertu (VTU.L) - CEO Interview

Robert Forrester makes a strange comment in this interview

...we're making decisions, we need to know where interest rates are going to go, we're in, you know, we're in the market for potentially looking at swaps and things like that...

Why would a company with masses of net cash be looking at taking out (more) interest-rate swaps? It seems more evidence that a major acquisition may be underway. Of course, we have previously reported that the buyback being announced but not executed looks like something is in the works.

Scale is their number one strategic priority, and in the last set of results, they said:

The Group's balance sheet strength is underpinned by a significant freehold and long leasehold property portfolio with a net book value of £243.8m and a net cash position at the end of the Period of £17.8m. There is significant opportunity to leverage the strong balance sheet to provide firepower for acquisitive growth.

Any debt-funded acquisition is likely to be highly earnings accretive, even at the current higher long-term interest rates. However, any acquisition has to stack up against the alternative use for the cash. They are on a forward P/E of 5 and a big discount to TBV, so if they secured say £50m of debt against their freehold property and bought back a third of their shares in the market, this would also be highly accretive to EPS.

Hunting (HTG.L) - Q3 2022 Trading Update

Hunting saw strong trading:

Trading in Q3 2022 has been strong as momentum within the global oil and gas industry continues to accelerate. Group EBITDA in the quarter was ahead of Q2 2022, with a year-to-date EBITDA of c.$36 million being recorded, with all operating segments and product lines seeing improved performance as clients commit to new projects.

And, perhaps more importantly, all regions are contributing:

Hunting Titan continues to see strong sales in its core market of North America, along with increased international market opportunities, particularly in South America…

Within the North America segment, sales momentum within the Premium Connections and Accessories Manufacturing businesses saw strong increases as clients continue domestic and international project development…

The EMEA operating segment continues to see improving results, supported by the Tubacex contract for Brazil, which is being completed in the Group's Netherlands and Aberdeen facilities. The segment's Norway and Saudi Arabia businesses reported sales improvement throughout the quarter as international activity levels return to growth…

The Asia Pacific operating segment saw an improvement in sales during Q3 2022 after a challenging H1 2022. The segment begun work on the CNOOC contract that was awarded in August, which will contribute to sales and profitability in 2023…

However, it looks like Q3 EBITDA was a miss versus the August Arden note, coming in at c.$15.4m vs $16.7m estimated. However, they say:

In summary, the Board remains comfortable with current market expectations as sales momentum and profitability continue to increase, with the outlook for 2023 remaining particularly positive.

So they expect to hit guidance of $54m EBITDA, meaning $18m for Q4 and positive momentum into 2023. This positivity is supported by an order book that has increased by $38m since the end of August.

Net cash decreases as they invest in working capital to support renewed growth. However, their finances remain strong, and the company still trades at a significant discount to Tangible Book Value. This reflects the market’s assumptions that these assets will never become productive again. If the strong momentum continues into 2023 and beyond, this view may well rapidly change.

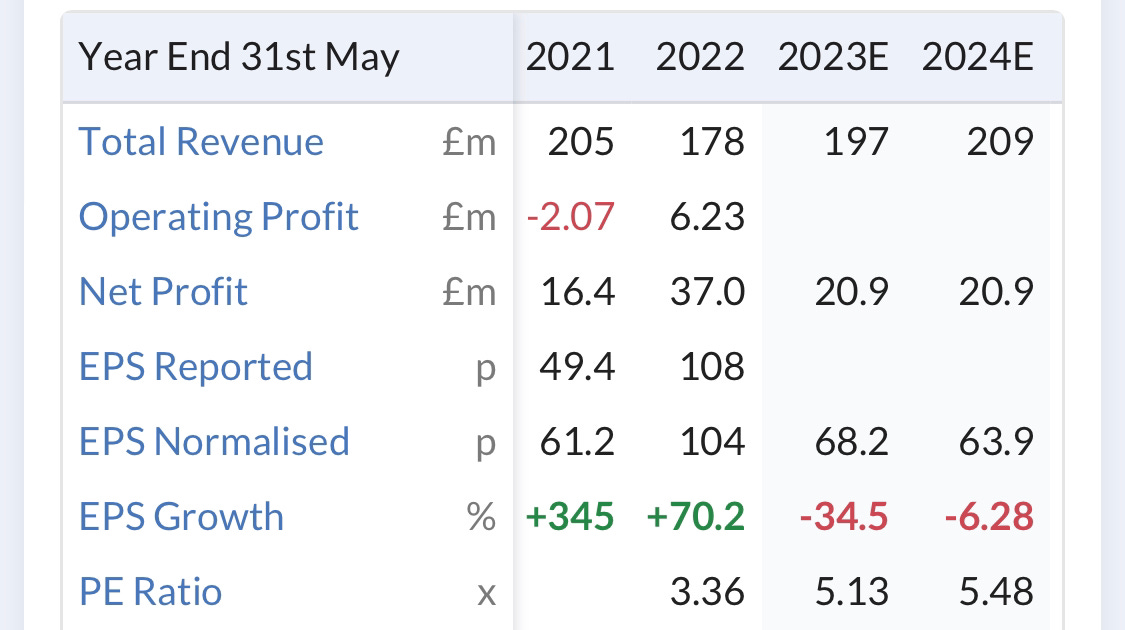

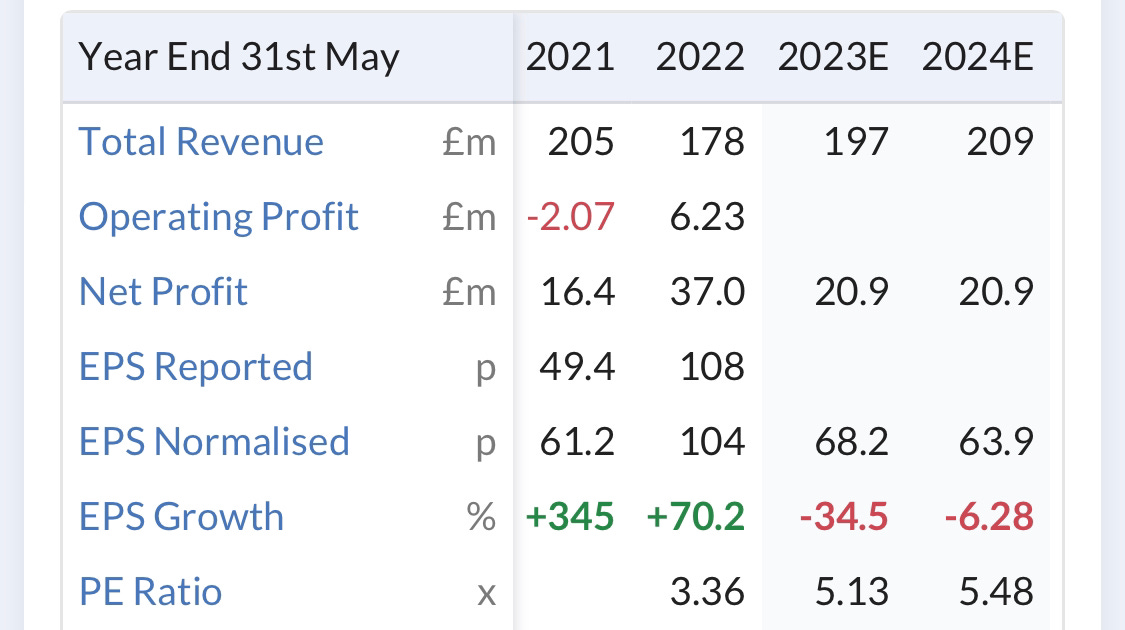

Alumasc (ALU.L) - AGM Statement

They start with a bit that isn’t really a trading update since we already have FY results!

The Group is pleased to report that following the strong performance in the year ended 30 June 2022, and the disposal of Levolux on 26 August 2022

FY22 was a year where they managed to hit expectations by selling Levolux for £1 and hence moving their losses to discontinued operations! However, they do go on to say:

…trading in our continuing operations over the first quarter of the current financial year has remained robust. Both volumes and margins in our continuing operations have been strong, and ahead of the corresponding prior year period.

Which is presumably why the market has responded well to this statement. If 2023 does end up ahead of last year, this is looking very cheap (although we are not sure we should trust these adjusted figures from Thompson-Reuters here):

There is still debt and a pension deficit, however, and surely they can’t buck the massive housing recession that is being priced into their customers’, the house builders’, share prices.

And they don’t say anything about actual trading figures or their alignment with market expectations. Surely they must know this, so why obscure it? Instead, we get a statement full of vague hand-waving from the management, such as:

"We have three strong divisions with excellent teams aiming to deliver ambitious growth in their markets, all of whom have well-defined strategies for delivering their goals. The Board is focused on supporting these divisions to purse their ambitions."

Perhaps revealing that management are as clueless as the rest of us on how 2023 will turn out for the company.

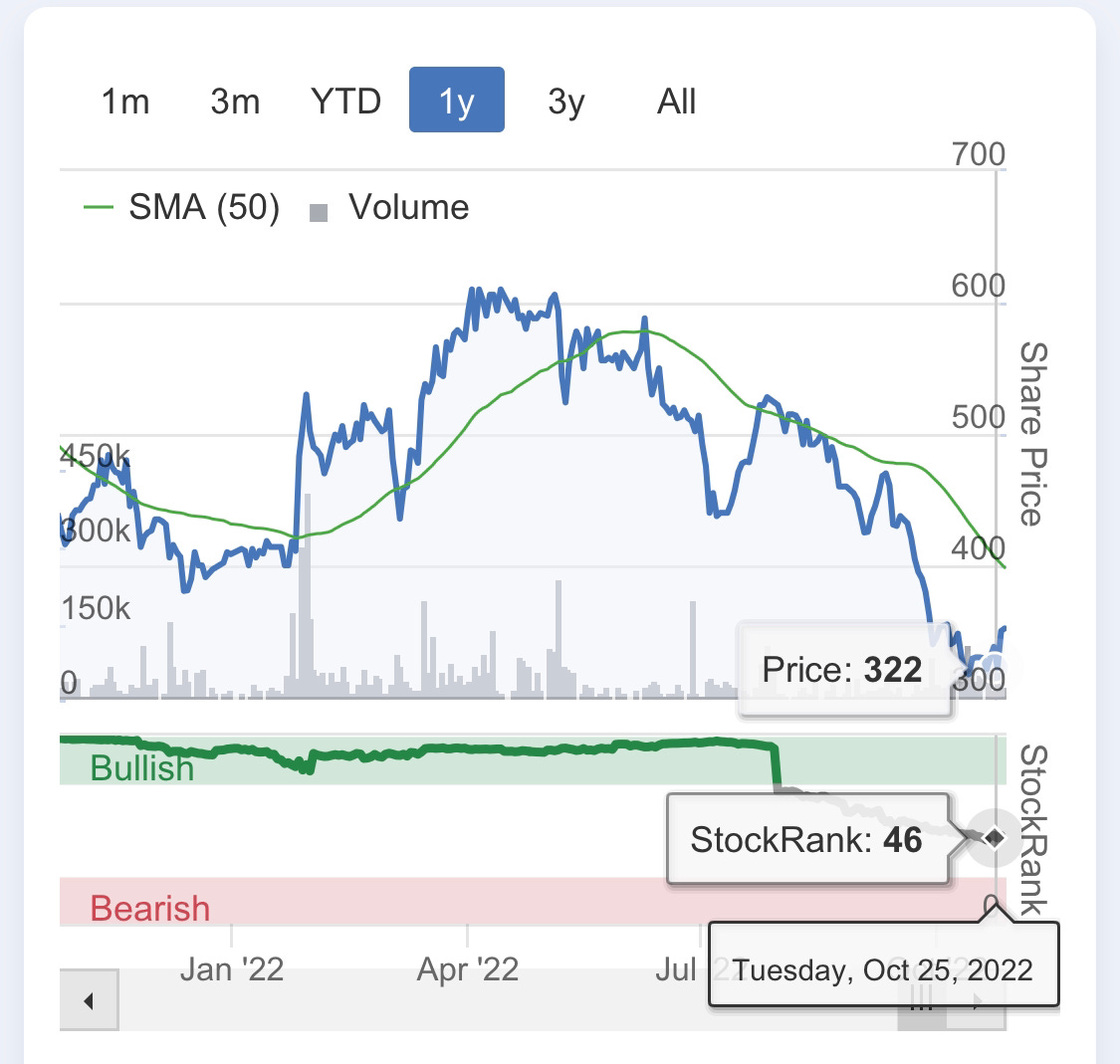

Hargreaves Services - AGM Statement

In-line from Hargreaves:

I am pleased to confirm that all three business sectors, Services, Hargreaves Land and HRMS, are trading in line with the Board's expectations.

Services, Land Sales & their German JV, which makes coking coal and recycles steel, amongst other things, are all trading well. This is surprising on some levels, given the turbulence in their end markets. They do say, however:

The first four months of the financial year has seen a strong trading performance within our German Joint Venture, HRMS. Uncertainty within German industrial markets and short visibility on trading means that it remains unclear how long current conditions will persist.

This is probably why the share price didn’t react to the statement at first. The price has been very weak lately in anticipation of this coming trading weakness:

It looks cheap, however, with £19m cash & no non-lease debt:

And the share price eventually reacted to this inline statement and ended up 13% on the day. However, the German JV is a bit of a black box and is responsible for the bulk of the profit of the last few years. And the property exposure is likely to provide weakness going forward. This doesn’t seem like the time to be chasing the share price.

Newmark Security PLC - Trading Update

This company presented at Mello prior to Covid, where the story was one of a shift from hardware to software sales. There has been little sign of this having any positive impact on their earnings over the last few years, though:

They’ve still not managed to produce any results for the 30th April year-end, but they have released a trading statement. Tl;dr - last year terrible, this year not terrible:

Post period end, the Group returned to profitability and positive operating cashflows during the first five months of FY 2023, whilst also continuing to grow revenues.

The share price reacted strongly to this statement, but this is so illiquid it’s really just a few buys and can quickly reverse.

The Group secured a $2 million US invoice discounting facility in February 2022 to provide additional working capital headroom and successfully managed supply chain challenges by building inventory to satisfy ongoing customer demand and stay ahead of the competition.

The Group had £0.2m of cash and cash equivalents at 30 April 2022.

Hmmm, note they don’t say net cash! So they ran this pretty close, and we expect the going concern statement in the FY22 results to reflect this when we finally see it. They do appear to have lived to fight another day, however.

Base Resources (BSE.L) - Q1 Activities Report

The first quarter of FY23 has started well, with the Ilmenite production rate slightly up on FY22:

This run rate should see production at the upper end of guidance if maintained throughout the year. Sales were lower due to the timing of shipments. However, the price received is very strong:

Some weakness in pricing is expected going forward due to global economic conditions, offset by global supply constraints.

It is relatively easy to estimate free cash flow from these figures, which comes out to be about $20m after central costs and a relatively large $9.2m capex for the quarter. Cash increased by $18m to $73.1, and they also paid a $27.3m dividend in the quarter. This suggests that they will have reduced their receivables balance by around $20m to achieve this.

Going forward, if they hit the upper end of production guidance, shipments catch up with production, and pricing doesn’t come off too much, then they should do another $120m FCF before the end of the year. This means their cash balance should largely cover their approximately $190m market cap.

The bad news is that progress remains slow in extending the mine life in Kenya, plus their Toliara project in Madagascar remains becalmed by fiscal term negotiations, as it has been for the last few years. While they claim positive progress in the quarter, there appears to be little tangible news on this front.

The market appears to be increasing pricing the slow progress here rather than the prodigious cash flows from the current Kenyan operation.

That’s it for this week. Enjoy the unseasonally warm weekend.