Small Caps Live Weekly Summary

Inflation Stagflation DRV NCYT RBG TGP VNET

This has been a difficult week for investors with the spectre of high inflation (see WayneJ’s thoughts on inflation below) and rising interest rates causing large falls on the indices. It is not clear to us that this is totally rational - it certainly seems like some of the low-interest-rates = high-growth-stock-valuation narrative was simply a post-hoc justification of another speculative tech bubble which is now bursting. Neither is it obvious that, in a period where inflation is running much higher than interest rates, you should prefer owning cash to the real assets that many equities represent. In light of this, then all equities selling off together with cryptocurrencies & loss-making tech isn’t wholly logical. Inflation increases the uncertainty of outcomes though and equity markets don’t like uncertainty. There is a market saying that:

In a crisis, the only thing that goes up is the correlation.

Knowing this doesn’t make investing in the current markets any easier but perhaps provides perspective for those with a long-term investment horizon.

Large Caps Live

So let’s start with inflation....

Obviously, there was a surprising print on inflation at the end of last week. But I must admit that I am surprised that people are surprised.

Now I would like to start at an odd starting point - economic models and boxes. Most economic models in essence treat a country like a closed box - so fiscal and monetary policy offset each other. And the supply / demand curve sets prices. What we are seeing now is something 'outside the box' ie an external supply shock - ie Russian invasion of Ukraine impacting oil and grains. Add onto that the supply shock of lockdowns in China impacting goods and supply chains over the last 2 years.

From Investopedia:

The U.S. CPI basket includes a 33.3% weighting for shelter costs derived mostly from rents and owners' equivalent.

So what I have been thinking is that shelter costs are pro-cyclical ie when central banks face low inflation they cut rates and when they face high inflation they raise rates - but does that also then move shelter costs in the same direction?

There was incidentally also discussion on CPI vs the PCE deflator - in the US apparently, the CPI uses out-of-pocket healthcare costs whilst the PCE uses Medicare and Medicaid costs - so they end up with different inflation for healthcare.

So the key point for me is how does shelter costs interact with interest rates - landlords rarely 'cut' the value of the property in their portfolio when the market moves - rather they increase the rent to match their interest rate - so surely as interest rates rise the cost of shelter might actually go up (until house prices fall massively). Shelter costs are definitely lower - but house prices are higher - and the difference is explained by interest rates - and that is my argument - that shelter costs move in the same direction as inflation but perhaps on steroids - due to interest rates moving in that direction).

Next point on inflation - DESPITE or IN SPITE of Chinese lockdowns the imports into the US have been going up:

So I am thinking that over the next few months we will get imported goods DEFLATION. I think I may have mentioned a week or two back that B&Q already seem to be discounting garden furniture 25% and that seems to me to suggest that they are having excess inventory.

Next point - I think that we are going to have an increase in wages - I was shocked earlier this year (may have been last) that council bin men were demanding 10%+ somewhere in the UK. I think we will have circa 5% across the board as the new 'normal' - and maybe 7 - 10% wage rises. But I think that this will work throughout the system over the next 12 - 18 months.

Using a US chart again I think the real problem in many ways is this chart:

It could take quite large wage rises to encourage labour force participation again.

Before we discuss the result of the above I would like to add a couple of other points:

(1) Inflation is the year-over-year change - this means that the headline number might move down from 8.6% to 4.5% say but that still means prices are going up - and the movements are independent of central bankers.

(2) In the UK we have an economy that is (a) perhaps closer than it was 5 - 10 years ago (Brexit - loss of FoM) and (b) susceptible to currency movements (c) has a debt issue (coming to that in a sec)

So it is worth remembering that the year before the Scottish and the EU referendum we had GBP:USD of $1.72. As I write it is $1.22. So someone whose assets are in sterling is now 29% poorer in USD terms. I don't want to go into the argument about the right currency to measure stuff in etc or purchasing power etc BUT remember that the rest of the world has already decided that - most serious funds / investors measure their assets in USD. The UK in the 1970s - 1980s used to be highlight sensitive to IMPORTED inflation on goods and commodities (eg petrol / oil etc). And that is before we get to trade barriers etc

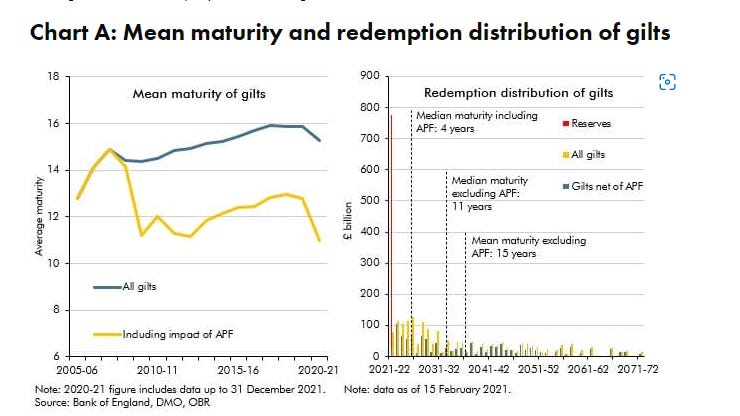

Now the next point I want to make is one that shocked me - and I need to confirm it. But the maturity of the UK govt debt has shortened considerably. Have a look at the following chart:

The FT says:

Because the UK has almost £500bn of government debt linked to inflation rates, the debt servicing cost is forecast to rise from £53.5bn in 2021-22 to £83bn in 2022-23.

So what we have is:

(1) reduced workforce participation - both at the elderly end and at the junior end - ie kids feel that they need to do an MSc or PhD to get attractive jobs.

(2) goods that will be overstocked this year

(3) interest rates going up - leading over the next few months - into mortgage rises - and remember that we have had a virtual freezing last week on RMBS (will come to that in a minute) - but anyway a lot of people have mortgages with only a period of fixed before it moves to variable - so let’s assume people have 1 - 2 years left at fixed rates on average - it means that over time we have a further jump in actual shelter costs

(4) fuel - which frankly it doesn't matter if oil is $85 or $90 or $110 - it is expensive for a lot of people. And natural gas even more so. Clearly leads to issues this winter unless the winter is mild

(5) And the risk of food riots in parts of the world during the autumn.

(6) In the UK we have the issue of imported inflation with a weak currency - and in fact that becomes a self-fulfilling vicious spiral.

(7) And the service cost of govt debt squeezing its ability to pay nurses etc. Part of what I want to get across is that it is not just debt as a % of GDP that matters but also the maturity of the debt and the sensitivity to inflation of the debt - and the UK seems to have a decent whack of inflation-linked debt.

And may I just discuss another obscure area that I think will have a massive impact in the UK related to housing?

Basel 3 and ECL. See this. Under Basel 3 a bank has to classify loans into different categories. If you fail to pay a payment when it is due then the bank has to start provisioning for 12 months or more of losses ie the ECLs up front. ie the bank has to provision UPFRONT in a regulated and managed way for loans which have not gone into full default but are just late paying. It is a bit more complicated than just the ECL, but the point is that I suspect that Basel 3 ECL rules will make bank earnings more volatile and as a result, they will raise rates or lend less and so house prices will lose their support over the next 18 - 24 months Then add to that that due to constraints on govt budgets I think that taxes will rise to pay for education, military and health. I suspect the UK will start looking at wealth taxes.

So above we have discussed the reasons why inflation will go up. The question is what the offsets will be? (1) supply chain sorting itself out (2) a more conciliatory nature towards Europe (perhaps under a new government) (3) end of the Ukraine war which probably means that Putin is no longer leader.

So putting all the above together I can't see why we will not have stagflation ie high inflation and low growth. Now I do not know the exact definition of stagflation but I would suggest that a useful working definition is when inflation is higher than growth. So I expect inflation over the next year to be volatile but the average will be over 5% - and a round of wage increases to follow leading to further inflation. And in parallel, we will have poor growth so stagflation.

Small Caps

Leo wrote up the company Mpac on his blog here, which is well worth a read.

Driver Group (DRV.L) - Interim Results

Underlying PBT come in smack bang in the middle of the £300-500k previously guided. However, this excluded a rather sizable Share-Based Payments charge. The SBP charge is a bit of an accounting gimmick though and many companies make a cogent argument that you should be looking at the company on a fully diluted basis rather than what goes through the income statement from SBPs. In this case, share options represents about 5% dilution:

The weaker performance is due to the previously discussed issues with APAC and the Middle East:

These should be the low point of performance though as they say:

The Board's operational review of performance in the Middle East and APAC, undertaken with independent external support, identified significant realisable cost savings and opportunities for better utilisation and, as I have indicated, we have taken early steps to take advantage of these performance gains.

On the outlook they say:

Driver Group's business in Europe and the Americas continues to trade very profitably with lower cost bases, offsetting losses in the Middle East and APAC. We expect to see a greater share of EuAm profits drop through to the bottom line.

The addition of the word "very" bodes well, although this isn't a business that has great forward visibility:

Due to the nature of our business, we only have short term visibility in terms of forecasting. However, the Group has a strong pipeline of convertible opportunities in Europe and the Americas, with the Madrid office working closely with our colleagues in New York to strengthen our competitive positioning and new business leads from the fast-growing Latin American market. Similarly, the Group has a growing pipeline of opportunities arising in Africa.

The drop in cash is perhaps a little worrying, however we already know this was due to receivables build in the ME:

The Group's net cash** balance at 31 March 2022 was £3.7m (2021: £7.2m) a decrease largely attributable to the delays in the timing of customer receipts. Post-period end, an agreement with a counterparty in the Middle East saw the Company's net cash balance increase to in excess of £5.0m. This comfortably exceeds the Group's near-term operational requirements.

The outlook confidence is backed up by a maintained dividend:

The final dividend announced at the time of the results for the year to 30 September 2021 (0.75p per share) in January was paid in April 2022. Reflecting our confidence in the medium-term prospects for the Group and with the strong balance sheet position the Board recommends the payment of an interim dividend of 0.75p per share for 2022 (2021: 0.75p per share).

Plus we also get news today of a buyback:

…it intends to conduct on-market purchases under a share buyback programme to repurchase £0.5 million of the Company's ordinary shares

£0.5m isn't exactly a large amount, but perhaps reflects the relatively tight shareholder base and illiquidity:

The maximum amount (excluding expenses) of share value that can be traded in one week is £125,000.

On the ED results pesentation they indicated that they would be willing to extend the buyback if required, presumably if the share price fails to respond positively.

The always bombastic, Equity Development call this an "Inflexion Point" although they haven’t re-introduced forecasts.Which annoyingly makes it hard to judge valuation here.

The current 1.05 TBV looks good value, particularly since, following the ME deal, the company have indicated that receivables are more likely to be written back than written down in the future.

Mark doesn’t see why they can't grow Europe & Americas and get APAC & ME to break even in a relatively short period of time. Indeed the breakeven of APAC & ME in the near term was confirmed by management on the results presentation. It seems the loss in revenue in ME will not be pro-rata with the headcount reductions so utilisation should go up here. Overall, this would potentially be 5p EPS for FY23 and a very low rating once you cash-adjust it. Hence Mark is now more positive about Driver than he has been for a while (although from a very low base!). We can see why the market will want to see it to believe it in the short term, however.

Novacyt (NCYT.L) - DHSC dispute update

Here's the news:

On 15 June 2022, the Company filed a defence of the claim received on 25 April 2022 and a counterclaim of £81.5m against the DHSC. The value of the counterclaim is broadly in line with the amounts previously announced by the Company in its full year 2020 results, plus related interest.

But they can say nothing more. Yet:

The information contained within this Announcement is deemed by the Company to constitute inside information as stipulated under Article 7...

Leo looked at this earlier this week and he calculated £110m of the DHSC claim is unprovisioned, which is enough to zero the tangible assets and probably destroy the company, whereas if they are successful in their full counterclaim then it would be very difficult for shareholders not to see some kind of return.

In reality Leo thinks perceptions and politics are all that matter. Given the other behaviour at the DHSC, perhaps the issue is they bought something they didn't need and got out the lawyers to avoid taking the blame. So what next? Leo thinks the overriding consideration will be to avoid a court case that the press might pick up on resulting in the incompetents responsible losing their job.

So he thinks the DHSC will settle their claim out of court provided Novacyt settle theirs. Probably Novacyt will just keep the payments have already received, but get no more. However DHSC have effectively destroyed other diagnostics companies for no obvious reason other than not making the requisite political donation.

If it settles as above, then Novacyt looks superficially cheap, but they seem to be firmly down the path of spending their cash on research rather than ever returning it to shareholders. And Leo thinks a settlement with DHSC would include a clause preventing dividend payments in the near term that would "look bad".

However the most likely outcome is a drift in Novacyt's share price as they spend money on lawyers fees followed by a bounce when settlement is announced (which could be anything from 1 month to 5 years time), followed by further drifting. They remain on Leo’s watchlist as the share price is highly dependent on sentiment.

Revolution Bars (RBG.L) - Trading Update

Following positive trading over the Jubilee Bank Holiday, the Board is confident of delivering adjusted EBITDA after rental charges (on an IAS 17 basis) slightly ahead of the top end of market expectations, which currently stands at £10.0 million.

Adjusted EBITDA on a IAS17 basis was £7.6m in H1. So they are forecasting just over £2.4m for H2. Depreciation & Finance costs were £3.8m in H1 so they will be loss-making in H2, although this is clearly a seasonal business.

They are starting a program of refurbishments & expanding by a further 6 bars in 2023. What we really need to know is how many rent-free or reduced rents they got in the current period too, since this could flatter profits. They had £4.2m net cash but also £1.1m of short term provisions.

Their debt is all CBILS:

As at the date of the consolidated financial position, the Group had an undrawn revolving credit facility (the " Facility " ) of £17.3 million expiring in June 2023, and £15.3 million remaining of Coronavirus Large Business Interruption Loan Scheme ( " CLBILS " ) loans. The CLBILS is a three-year amortising loan which expires in July 2023 and May 2024.

Which will require refinancing if they continue with their expansion plans and the debt expiry dates look quite close. Being CLBILS also acts as a blocker to any dividends.

We are still not convinced this is good value at the current price given the inflationary headwinds they face.

Tekmar (TGP.L) - Interim Results & Formal Sales Process

We’ve followed this company for a while. The initial attraction of analysing the business was a high market share in a market predicted to grow 15% CAGR out to 2030. However, the company seemed to consistently grab defeat from the jaws of victory and we identified a number of red flags: a founder CEO leaving, the CFO leaving, Downing Strategic taking a toehold position and then backing away quickly, but primarily the big concern we had was that the contract assets, that represent unbilled work, soared even as revenue declined.

We were right to be wary as the company increasing relied on CBILS loans to operate, and we predicted a fundraise which they eventually did at 45p. It seems they didn’t raise enough money, since they now say:

Whilst we are making satisfactory progress in delivering on our strategic plans, our planned timeframes to establish the improved financial performance for the business we are targeting are being hampered by the prevailing industry conditions, which remain challenging.

Which seems strange since it is difficult to imagine a backdrop more positive for them! The wind industry is in such good shape the UK government have threatened a windfall tax.

The result is that they have started a formal sales process. The problem is that they are doing so from a position of weakness not strength, as this week’s results confirm:

Revenue of £13.0m (6M to 31 March 2021: £13.9m) and Adjusted EBITDA loss of £1.8m (6M to 31 March 2021: loss of £1.1m), is in-line with management expectations for the period

The trouble is that management expectations for H1 are almost never disclosed by any company, and for all we know those management expectations were set yesterday. What we do know is that 2x13 = 26 which is quite a bit less than forecasts of £44.2m revenue for the full year.

The Group extended its £3.0m CBILs facility to October 2022 and extended and increased its trade loan facility to £4.0 million, which is available at least to November 2022

Is all the debt financing expiring in 4-5 months supposed to be good news?

Cash on the balance sheet of £10.3m at the period-end is overstated by £5.2m due to a customer overpayment, which has now been repaid.

That's a big overpayment. Are they now being supported by their customers?

At the period end, the Group had received a milestone overpayment from one of its customers of £5.2m

So sounds like they were paid for a milestone that hadn't been reached?

We continue to see 2022 and 2023 as transition years for Tekmar

Leo would say a metamorphosis has been going on for several years now. And the result both as ugly and doomed as the one in Kafka's book.

What about those red flags on the balance sheet?

Overdue receivables have blown out. Surely there is at least one significant contract dispute here? But the liabilities side doesn't seem to include any provisions.

On the other hand contract assets look in far better shape than in the past. However, Leo suspects most of that £5m overpayment will go back into contract assets. So they could end up worse than 6m earlier.

Even in terms of claimed profitability (including profit from work that they may never be paid for), the situation seems to have deteriorated significantly. Leo no longer sees any value from future cashflows at the consolidated group level. It may be that there are limited company subsidiaries that are profitable. If the others do not have parent company guarantees then perhaps they could be jettisoned? But we think the baseline valuation should be realisable assets.

Leo would take a big write down of receivables here, which effectively would leave realisable assets of zero and only leave option value.

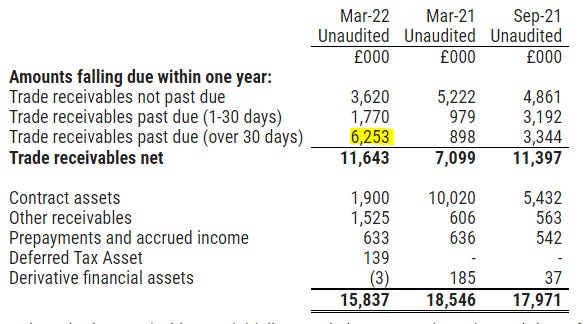

Mark would be more genourous. The NCAV of the business comes out at £14.4m as of 31st March. However, the trade receivables 30 days+ past due have absolutely soared and now stand at £6.3m. Although the company don't think there is a problem, they have failed to see problems with their business over the last few years as it has gone wrong. So, given the size of the increase, there has to be a material risk that these will not be paid and are under some kind of dispute. Also, there are £1.9m of contract assets and these represent unbilled revenue. Again, given the history, there must be a material risk to these being paid.

Taking these off we are left with £6.2m of NCAV. Being conservative, ongoing losses will eat away another £1m or so and a NCAV of more like £5m. Prior to this week’s announcement the company had a market cap of c.£27m and at the end of the week this sits at just £6.6m. Despite these precipitous falls there is still some way to go down before this will to start to be worth considering as a NCAV play (and maybe never if you take Leo’s view on this!)

In terms of buyers, anyone buying will want to be sure that the warranty issues with Orsted are ring-fenced. I suspect part of the reason Orsted have not gone after Tekmar for refit costs is that even the legal case costs alone would probably bankrupt them and a bankrupt supplier doesn't gain them anything. This restriction may not apply to a better-financed purchaser, however.

One possible option would be to put the "bad" business into admin and sell off the Pipeshield & Consultancy parts. It is possible these could be worth the current price alone but you'd have to be sure there are no parent guarantees and any issues die with the bad business. All seems a bit risky when there is no guarantee you'd actually make money vs the current market valuation. So again you'd want a much bigger margin of safety than currently on offer.

Vianet (VNET.L) - Final Results

Like a lot of companies post-covid, now is the time to worry about cash:

At the year-end, net borrowings were £3.00m (2021: £2.66m) and the Company had a gross cash balance of £1.58m (FY2021: £1.89m).

Which is made up of CBILS financing:

A £3.5m Coronavirus Business Interruption Loan ("CBIL") was taken on 26 May 2020 to provide a buffer against a prolonged recovery period and facilitate investment in our commercial sales team and technology roadmap. We ended the year with net borrowings of £3.00m (FY2021: £2.66m, FY2020: £0.95m) and a gross cash balance of £1.58m (FY2021: £1.89m, FY2020: £1.73m).

Similarly, rebuilding of working capital is a common theme:

Net cash generation pre-working capital movements was an inflow of £2.74m (2021: £0.34m outflow, 2020: £3.72m inflow), impacted by the strong recovery in results.

but:

Working capital was closely managed, noting the impact of semi-conductor supply and stock premium costs together with inflationary pressures, which delivered a contained and managed working capital generation outflow of £0.34m (2021: £1.39m inflow, 2020: £0.49m inflow) and has meant that after working capital movements there was an operational cash generation of £2.40m (2021: £1.05m, 2020: £4.22m) which is c. 57% of pre-pandemic levels.

So working capital outflow was not as large as it will be for many other recovering companies. It is "investment" that has done the damage:

The cash generated was principally used to service varied terms for our customers particularly in Smart Zones and the tail end emergence from C19, full year investment in our sales capability in Smart Machines and continued investment in R&D and servicing of borrowings. This resulted in an overall cash outflow of £1.63m (2021: £1.51m inflow, 2020: £0.42m outflow noting 2021 benefitted from a £3.5m CBIL).

So what about the cash outlook:

With the cash and facilities we have and the expected business plans we have developed over three indicative years, we believe we have solid cash runway forecasts well into 2023

Oh dear, so potentially less than a year's cash left. No updated cash level is given, suggesting a significant outflow since 31st March.

We can't understate the importance of looking at full annual reports, not just the summary results RNS. First stop should be going concern for a company like this - page 14:

The Directors, after having made appropriate enquiries, including (but not limited to) a review of the Group’s budget for 2022/2023, and cash generating capacity at least 12 months from the date of signing (underpinned by long term contracts in place and historical results), renewal of bank facilities and support which was renewed to 31 May 2023 with a bank support note stating there was no reason why facilities would not be renewed beyond this date, have a reasonable expectation that the Group has adequate resources to continue in operational existence for the foreseeable future. For this reason, they continue to adopt the going concern basis in preparing the financial statements.

So that's clean. But:

The Group’s trading and cash flow forecasts have been prepared on the basis of assumptions based on more normalised trading post COVID19, underpinned by historical performance noted above.

So flagging an issue if restrictions in pubs or offices where many vending machines are located. Next stop is the auditor's report, page 29. The going concern audit is also clean:

Based on the work we have performed, we have not identified any material uncertainties relating to events or conditions that, individually or collectively, may cast significant doubt on the Group and the Parent Company’s ability to continue as a going concern for a period of at least twelve months from when the financial statements are authorised for issue.

They also (correctly, in Leo’s view) identified valuation of acquired intangibles and capitalisation policies as key audit concerns and these are clean. Here's the key thing to look out for:

If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact.

We have nothing to report in this regard.

Nonetheless, things still look tight to Leo. They report £1.0m of (presumably CBILS) to be repaid in the current year versus my earlier projection of £1.1m. That would leave them with cash of £0.6m, plus an undrawn overdraft facility of £0.2m.

So while things are better than Leo projected (he thinks by £0.3m), regardless what the auditors think, he sees a material uncertainty over going concern. If that wanted to reassure shareholders they would have given current cash / debt figure.

Cenkos now have some 2023 (and 2024) forecasts. These show 3.8p EPS for 2023, this is close to Leo’s model at 4.0p. But the departure is that they are predicting 8.8p for 2024 on annualisation of the recovery, whereas he sees ongoing weakness Smart Zones acting as an ongoing drag.

The trouble is that, as can be see today, conversion from operational cash flow to change in cash is very poor due to high "investment" levels. So, if they make it through the year then things might be looking much better this time in 2023. Leo continues to predict a fundraise however. And it's not exactly cheap at the moment for a company with long standing management who have generated a total shareholder return of less than 1% per year over 15 years.

That’s it for this week, hope everyone is enjoying the sunshine if not the markets!