Small Caps Live Weekly Summary

RR. SCE JOUL BOO CINE HUM HTG

Large Caps Live was back this week with WayneJ taking a look at Rolls Royce. Mark presented at the Mello Christmas Special this week talking about how to account for pension fund deficits in company valuations. Do check it out if you haven’t already.

Large Caps Live Monday 13th December

Rolls Royce (RR.L) - Trading Statement

First up a request that we look at Rolls Royce. Here are the basics:

Market Cap £10.28BN

EV: £15.29bn

Revenue £11.16bn

Operating margin -2.66%

ROCE -1.68%

My view approaching this stock is that it has been hit by a number of issues:

Potentially dodging accounting where the company was booking service contracts as profit ahead of cashflows.

The engineering giant will pay £671m to settle corruption cases spanning nearly 25 years after court approval.

Covid 19 hitting aircraft movements

The need to sell businesses to rebuild the balance sheet

Emergency fundraise – probably too little too late meaning that it is disposing of businesses it should have kept (ITP Aero)

Underinvestment?

Sold off single-aisle engine JV to P&W

A new chairwoman – Anita Frew – who some have said has no known background in STEM

Industry going through an evolution to low carbon fuels.

Pension deficits

Onto the trading statement from 9 Dec 2021:

The key point is that there are cash disposals bringing in £2bn over this year / into fiscal 2022 (as some of the transactions are still in progress). But actually, this reinforces my point that the company delayed its fundraising and did not raise enough. Secondly, this discusses the cost-saving programme (restructuring) delivering savings of more than £1bn in 2021.

One of the major issues I needed to get my head around was engine concessions. I find this weird.

Essentially if the cost of an engine is $X, then RR will sell the engine to an OE (eg Airbus / Boeing) for $X. Then, when the plane is delivered to an airline, there will be a discount on the plane, some of which relates to the engine. So RR then ends up paying Airbus or Boeing a certain amount – let’s say $Y as a ‘concession’.

As a result, RR makes about $1.3M loss on each engine – which we kind of knew – but I am not sure that I realised that it was done in this way. So part of the better cash flow in 2021 was because fewer planes were delivered so there were fewer concessions to be paid by RR to the OEs. In fact, that was £300M less. My impression however is that the sales to the plane makers of the engines were booked in 2021 – I need to confirm this. But if so there is a deferral gap. i.e. RR recognised the sale of engines in 2021 BUT the losses on those sales ie £300M will be recognised in 2022. However, I am not entirely clear except to know that they are explicit that there is a £300M cash OUTFLOW delayed to 2022 for OE concessions.

In that context, there are a couple of terms we need to learn:

LTSA - Long Term Service Agreement

EFH - engine flying hours

The whole point was that mgmt was trying to provide flying power as a service. That gives us this beauty:

So you can see that revenue for the LTSA is recognised regularly - and it makes the profits look great in the early years. But in year 5 you take a hit on that engine - however, if you have sold other engines which are earlier in their lifecycle then that should cover it up initially.

Also - I think there are issues in that slide that is not dealt with and one that is elsewhere:

Your pricing for $ per EFH is in DOLLARS. I find it almost unbelievable that the company has a $24bn + a $4bn ie a $28Bn hedge book.

You are making an assumption for INFLATION. You do not need much in the way of swings in inflation on $28bn to make your contracts loss-making.

You are making an assumption on how many flying hours so utilisation etc.

So then the obvious question to ask is what is the current fleet:

I think the most important part of that page is that it excludes the temporarily parked planes.

You can see that in the Trent line which fell from 3,992 in 2019 to 2,764 in 2021 H1 - or in large Civil from 5,029 to 3,481.

I also want to highlight another line - the Pearl engine line is aimed at business jets and some single-aisle jets. The reason that this is all-important is that:

Single aisle jets have been the big grower in the aviation market

In the covid recovery, single aisles - which tend to fly on DOMESTIC routes - have recovered faster than wide-body (ie twin aisles) which tend to fly on INTERNATION routes

And incidentally, cargo has picked up even faster:

RPK = revenue passenger kilometer, CTK = capacity tonne kilometer

I am annoyed that I did not back up the truck last year around the time of the fundraise, which with hindsight was a steal. Short term I think it will continue to drift down. However, I think that on a 2 - 5 year view if I was a big UK fund manager I would buy because:

I believe that aviation will recover - and that will drive an increase in RR aviation revenues. I would like to say that they will go up 50 - 100% but frankly, that is guessing and nonsense as I bet no one can really work out what maintenance is deferred - and remember - from the charts above - it is possible that in the year of maintenance RR actually makes losses for an engine.

The sale of ITP Aero and various other bits and bobs means it is hard for a retail investor to pin down the numbers without spending more time than I have

The Power business is recovering nicely. The company mentions moving more to power and defence - I am not convinced that is the right strategy as it means becoming a slower grower

Many of its competitors are parts of bigger groups eg GE or Raytheon or Safran. I could imagine that within the next 5 years Rolls Royce joins a bigger group in some shape or form.

So in 5 years time, I reckon you have a company doing (guesses) £15bn at say a 10% margin or within touching distance. I think the UK gets excited and puts it on 2 - 3 x sales.

Small Caps

Surface Transforms (SCE.L) - Trading Update & Contract Win

Normally the next trading update would be due in early January, so given the company's history, the arrival of a trading update on Tuesday didn’t portend good news.

The Board of Surface Transforms is disappointed to advise that despite considerable growth against prior year, revenue for the year ending 31 December 2021 will be below £3m, significantly short of market expectations. The shortfall has mainly been as a result of delays in the final commissioning of the upscaled production capacity at Knowsley (in relation to OEM Production Cell One) and the associated start of the anticipated upscaling of commercial revenues expected from December.

Oh dear, a supply problem. This appears to relate to their strategy flip-flopping. A couple of years ago, following a cash crisis and due to uncertainty over order flow, they decided to move to small modular manufacturing units. As they said in the FY 2020 results:

The Company's Knowsley site has a footprint that, with further capital expenditure, is sufficient for £75m p.a. sales made up of a £4m Small Volume Production Cell and five broadly equal modular OEM Production Cells.

Generally, we like this approach since it is inherently more scalable, has lower lead-times, and is lower risk and less capital intensive than building much fewer but larger units or trying to share equipment between them. It also provides opportunities to optimise one unit and roll out lessons to the others once you have it right. Not taking this approach tends to lead to sudden unexpected delays and escalating costs. We see this with everything from nuclear power stations to covid testing super-labs.

But, even when managed right, in the long run, it is more expensive and less efficient to do it this way. And if you make the units too small this can also be true in the relatively short term too. And so in September, they flipped back:

the Company will no longer build separate production cells but approach the project as a plant-wide "single production line" project…

Following advice from the furnace suppliers and internal evaluation the Company will now procure a smaller number of larger furnaces to support the sales capacity target for the Knowsley factory of £75 million p.a.

It is this last point that seems to have killed them:

Whilst this capacity programme progressed considerably during the year, a series of minor startup challenges has caused output delay, resulted in Q4 output missing target. By December, these issues have been narrowed down to an issue with one particularly complex furnace, which the Board believe will be fully resolved imminently.

Their "old" strategy certainly did not involve "one particularly complex furnace", it involved several small off the shelf furnaces, the first of which would have been in place and debugged six months ago. Anyway, what's the short-term impact:

Given December is a short month, the Company is unlikely now to recover the sales gap in this financial year.

It is important to note that these sales have not been lost, the key OEM customers have not seen any impact and the revenue gap, whilst proportionately large in 2021, is small in relation to overall 2022 volumes and is expected to be recovered progressively through Q1 and Q2 2022.

This seems unlikely, however. If revenue is lower that is because they have failed to deliver products to customers. Auto OEMs are famously Just In Time (JIT) and in stock and capital and so would not have been ordering masses into stock. Failing to deliver to auto customers on time can be a very expensive proposition. And they have badly let down their customers and reduced their future margin capability.

What makes this worse is that this is entirely a problem of Surface Transform's own making. This sounds like entirely predictable problems bedding in new unproven equipment rather than something where they can point to "global supply change disruption" or claim some formal or informal force majeure.

There's also a question of disclosure. On 13th September they said:

Production Cell One will be ready for the ramp up in sales forecast in Q4-2021

It is clear the problems started in October, and the share price has been falling since then. Here is the rest of the statement:

The Board recognise that the short-term effect of this is disappointing, but as noted above, believe these operational issues will all be satisfactorily resolved in short order. Accordingly, the Board intend to provide a further operations update in January 2022 and also to provide quarterly updates for a period of time to reassure the market in respect of revenue performance alignment with future market expectations.

They seem to recognise that more disclosure is now needed to maintain confidence. As perhaps is the intention of this additional news:

Progress on OEM 8

As previously notified, the Company won a lifetime £27.5m sales contract with an expected maturity level of £8m sales per year, commencing, (later than planned) in 2022, with a customer described as OEM 8. Again, as previously announced, the order intake for this car has greatly exceeded the customers original volume expectations and they have been in discussions with all the supply chain to explore the capacity availability for significant volume increases. These discussions are being finalised with all suppliers, with updated contract volumes expected early in the new year.

But which also raises the questions: Do they need to raise more capital for this? Without a scalable production strategy can they deliver?

Despite the miss on 2021, house broker, finnCap, retain their 69p target based on the factory filling to capacity over time and a discount rate of 9%. Of course, a discount rate of 9% is utter nonsense for this sort of company. Something like 20% would seem to be a more realistic figure given the risks involved. And whatever it was before the change in manufacturing strategy, it should be higher afterwards since the profit projections benefitted but the risk is higher.

After a rather shaky start to the week, things did get better for Surface Transforms on Thursday with the following contract announcement:

Surface Transforms plc (AIM:SCE) is pleased to announce that it has been notified of its selection as a tier one supplier of a carbon ceramic brake disc on the forthcoming launches of three cars of its existing customer, previously described as OEM 6…

The carbon ceramic disc will be fitted as standard to both axles on all three cars. The lifetime value of these contract wins is more than £45m - bringing the overall Company order book to in excess of £115m.

Clearly these are not volume cars, and even the total order book for the company is currently modest compared to the valuation. But the "standard equipment" gives higher volume certainty versus cases where they are only on the top model or as an option.

These contract wins are in addition to the previously notified vehicle selection with this customer. The first car is a limited-edition special model with start of production (SOP) in late 2023 with a short series production period. The second two models (the base car and a derivative) have an SOP of mid 2024 and will be in production for at least six years. In total, these three new selections by OEM 6 are expected to generate approximately £0.5m of sales in 2023, increasing to approximately £4m in 2024 and to approximately £7m in 2025 and thereafter.

Medium-term revenue visibility is useful for building cash flow models to determine under what circumstances they will need to raise more cash. After Monday’s announcement, we noted that the combination of delayed 2022 revenue, higher implied costs and a major new order was not positive for cash flow. And in the last statement, they made no mention of cash. I suspect they have received the same feedback from others as they now say:

These wins were anticipated in our recent capacity and cash flow planning scenarios and were included within the "prospective carry-over" projections described during the February 2021 fund raising.

And they are keen to promote their credentials as conservative forecasters of profit:

However, consistent with our policy that we only forecast contract wins, they were not included in any previous market guidance or analyst forecasts and can therefore now be added to these projections.

Unfortunately, they have no such credentials, having a long track record of missing forecasts, including this year when predictable delays led to a massive profits miss. However, they do make some good points:

We are delighted to be deepening our relationship with OEM 6 including moving from tier 2 to tier 1. We also note that this is now the third example of demonstrating our ability to win carry-over contracts after having won the first award.

And as previously commented, delayed revenue from FY 2021 will flatter FY 2022 if achieved:

We expect to win further contracts in the new financial year across our range of existing and new customers in parallel to moving into profit and operational cash generation in 2022.

There was also a director buy yesterday. Standard practice here is to use the title "Notification of PDMR Transaction". But instead, they decided to use the title "Michael Cunningham purchase of shares". This immediately makes us think that the purpose is not to quietly buy cheap shares, but to promote the shares as supposedly undervalued with the hope that they will rise. Michael Cunningham is the FD, and you have to feel a little sorry for him as he apparently can only afford £11,340 to spend on these "amazingly cheap" shares.

Despite the rather promotional RNS title, Leo retains a small position, because he expects more than "the factory filling to capacity over time". Mark prefers the much more certain prospect of large fees generated from Surface Transforms by their broker finnCap from any future placing.

Joules (JOUL.L) - Pre-close Trading Update

When we last looked at this in June we noted that brokers forecasts were for an increase to 18p EPS in FY 2023 from 12.5p in FY 2022, so was a potential growth stock. However, at the time the P/E was 30x so this growth was already more than priced in and was against a difficult sector, saying:

They are clearly executing well, but in a very difficult area. When other multi-channel retailers are struggling, going bust and Joules themselves are closing stores to retain profitability, why pay up as if this is a structural growth area, rather than a company battling hard to swim against the tide.

June pretty much ended up being the peak for the share price, which had been weak prior to today's update, perhaps anticipating the headwinds they faced. This brings us to today's update:

Lot's of details in there which is good to see. However, here lies the rub:

...full year profit before tax and adjusting items is now expected to be below current market expectations and in the region of £9m to £12m notwithstanding any further significant covid restrictions.

The reasons given are:

Global supply chain challenges are expected to remain during at least the second half of the Group's financial year and there is increased consumer uncertainty as a result of the emergence of the Omicron coronavirus variant.

Which makes sense. These seem to have been particularly acute in November, with them saying:

The well-documented global supply chain issues have resulted in some higher costs and stock delays during the Period. In addition, labour shortages in our third-party operated distribution centre (DC) have resulted in extended product delivery times to online customers, stores and wholesale partners. These factors were particularly acute in November, including the Black Friday period, which alongside weaker year on year online traffic contributed to performance during this month being below expectations.

And this has had a big impact on first-half performance:

Considering these factors, Group profit before tax and adjusting items for the Period is anticipated to be in the range of £2.0m - £2.5m (FY21: £3.7m).

This looks quite poor. To be so much lower than last year, which is a period where November had a national lockdown, is not a good sign. So you can see why the shares opened down 30% on the day.

This leaves a lot to be done in the second half. And although Christmas falls in H2 the overall buying patterns this year were for people to buy early to avoid stock issues, and to buy late last year after the November lockdown ended. They now have Garden Trading too, however, and that is likely to be significantly H2-weighted which may partially save them.

Still, Mark sees the lower end of that range as more likely given the headwinds. £9m PBT would be an EPS of around 6.4p on a normal tax rate which means that this is potentially on a forward P/E of 23, even after today's fall.

Of course, the story here was never solely about FY22, and potentially if pressures ease FY23 could see a strong recovery. However, house broker Liberum have also cut future forecasts and their FY23 forecast EPS is now 11.7p which is down significantly from the 18.1p they previously had for FY22. Liberum's FY24E EPS comes in at 16p, now below their previous FY23 forecast. They say:

We lower our TP to 300p reflecting the downgrades. Disappointing, but the drivers are industry-wide factors and we continue to be optimistic on Joules’ medium-term outlook.

Brokers are, of course, paid to be always optimistic. However, given the way that these things work, another profit warning cannot be ruled out, which would further dent confidence and lead to a further de-rating. Joules is a well-run company and it is likely that it will be a potential buy at some point. But it will be when the market hates it, has given up and it trades at a big discount to the sector, not the premium it currently still enjoys.

BooHoo (BOO.L) - Trading Update

Boohoo has seen gross demand growth in the Period exceed that achieved in each of the first and second quarters of the financial year, however expectations for the financial year ending 28 February 2022 will be lower than previously guided.

The recent share price performance suggests that they were already lower. Here is the reason given:

This is as a consequence of significantly higher returns rates impacting net sales growth and costs, with continued disruption to our international delivery proposition impacting international demand, and significant ongoing pandemic-related cost inflation.

The mix is seen as the culprit:

Net sales impacted by returns rates that are 12.5 percentage points higher than last year, and 7 percentage points higher than pre-pandemic levels driven by an exceptionally high dress mix

It makes sense that lockdown loungewear is far less likely to be returned than "going out" clothes.

The other thing they talk about is high international delivery costs. A major concern over the last year or so has been competition from Shein. And that the counterargument was that Shein has high international delivery costs / long delivery times and that these would hardly be improving.

Now we know that historically boohoo had also been delivering to the US from the UK, but we thought this was no longer the case and that most deliveries were local now.

It is the view of the board that the factors currently negatively impacting the business are primarily related to the ongoing impact of the pandemic and are, therefore, transient in nature.

We are not sure about that; if they want to compete with Shein then they need local distribution. UK growth however remains massive:

Exceptional UK demand, validating the strength of our business model where our leading proposition across price, product and service continues to resonate strongly with customers across our brand portfolio

o UK gross sales up 58% vs FY21; 102% vs FY22 [sic]

This is incredible given the strong comparatives. It would not be unreasonable to forecast that these rates could continue or possibly even be exceeded next year. And, accepting that there are new brands, this is in their most mature market.

UK net sales up 32% vs FY21; 78% vs FY20

o Net sales impacted by returns rates that are 12.5 percentage points higher than last year, and 7 percentage points higher than pre-pandemic levels driven by an exceptionally high dress mix

So they seem to be saying there is a catch-up on dresses. That is, not only are dresses much "higher" than during the pandemic, but they are "higher" than pre-pandemic. But doesn't the lower net sales versus gross sales percentage growth in FY20 suggest increasing returns is a long-term trend?

The Group continues to invest in building a distribution network capable of supporting in excess of £5 billion of net sales, with our first US distribution centre expected to go live in 2023, and we are considering options to expedite this process.

This could cause a performance bump at that point. But here's the real kicker:

For the year ending 28 February 2022, the Group now expects net sales growth to be 12% to 14%, compared to previous guidance of 20% to 25% growth. This reflects our expectation that the factors impacting our performance in the Period persist through the remainder of the financial year, and recent developments surrounding the Omicron variant could pose further demand uncertainty and elevated returns rates particularly in January and February.

This is very late in the year to be saying this. They have previously repeatedly beaten guidance late on in the year. Many investors will have assumed that this is because forecasts are conservative. This downgrade suggests that it is more about their performance being highly unpredictable.

Adjusted EBITDA margin for the year is expected to be 6% to 7%, compared to previous guidance of 9% to 9.5%

It is even later to be saying this. Very concerning. They have consistently enjoyed very high margins compared to competitors and previously investors had given up questioning it. But perhaps now they will.

The Group expects to incur cash exceptional items for the year of around £33 million, compared to £22.5 million previously guided, primarily due to warehouse and new brand restructuring.

Likewise, there will be less tolerance for this kind of BAU growth spend being exceptional type of nonsense.

As a result of this update, Broker Zeus have adjusted EPS for FY22 dropping to 5.2p from the 8.7p they did in 2021. They have also halved their 2023 EPS forecasts from 13.8p to 7.3p. Cuts to forecasts like this make the c.14% share price fall on Thursday look light, but of course, this fall in EPS had been largely anticipated by the market. Here is where we end up:

Pros:

UK growth suggests there is a massive runway ahead here worldwide

Temporary factors will unwind

Historically low valuation multiple of 16x 2023 earnings

Cons:

Evidence of structurally increasing return rates

It will take some time for confidence and their rating to recover

Heavy investment in distribution required

ESG issues have abated only slightly

Cineworld (CINE.L) - Update on Litigation

They say that the pandemic have accelerated many trends that were already in place or inevitable in future. For example, old people were forced into internet shopping and grocery delivery. Online meetings became the only option (outside of politics) and as we have seen, when things returned to near-normal, private investor meetings didn't.

But cinema is a bit of a strange one, being on a long-term downtrend in the UK since 1.64bn admissions in 1946. People will probably blame television for that, yet the medium-term trend has actually been broadly upwards since 1984, with admissions rising from 54m to 177m in 2018 despite the average TV size likely growing from around 12" (visible) to 50" in that time an at least equivalent improvements in picture and sound quality. LoveFilm DVD, iPlayer, NetFlix, Love Island, Breaking Bad Binges: none of these supposed megatrends towards home screen time made much impact on this resurgency.

A small fall in cinema attendance in 2019 could easily be put down to the almost complete lack of major original films that year. But the pandemic killed attendance stone dead, and worse still, fundamentally broke the exclusivity that cinemas had always enjoyed for new releases, something that was already weakening but could have otherwise persisted for another 5, 10 or 50 years.

A restart also proved very difficult, with studios not wanting to release films without enough cinemas and cinemas not wanting to open without enough films. Digital distribution, global promotion, pirating and social media mean that the days of launching in different markets months apart are over - a problem when the world can't agree which covid wave we are in.

So you have to feel sorry for Cineworld around the timing of their last trading update on 15th November, just before Omicron struck, when they said:

Since reopening our estate in April 2021, performance and attendances have steadily grown and this has resulted in revenue growth as seen in the table below. Customer demand has been particularly strong in a number of the Group's markets, in some cases even above the levels experienced in 2019...

There are still major blockbusters to be released in 2021 including "Ghostbusters: Afterlife", "Encanto", "Spider-Man: No Way Home", "The King's Man", "Sing 2" and "The Matrix Resurrections", which we anticipate will perform very well subject to there being no deterioration in the COVID-19 situation.

So today's update will not be welcome to investors:

On 6 July 2020 Cineworld confirmed that Cineplex had initiated proceedings against Cineworld in relation to Cineworld's termination on 12 June 2020 of the Arrangement Agreement relating to its proposed acquisition of Cineplex (the "Acquisition"). The proceedings alleged that Cineworld breached its obligations under the Arrangement Agreement and/or duty of good faith and claimed damages of up to C$2.18 billion less the value of Cineplex shares retained by Cineplex shareholders.

Now, why would somebody try to terminate an acquisition of a cinema chain in the middle of a pandemic, I wonder? Cineworld defended these proceedings on the basis that it had terminated the Arrangement Agreement because Cineplex breached a number of its covenants. Well, indeed, going ahead would have been like proceeding with a banking mega-deal in the middle of a financial crisis. But:

[Cineworld] counter-claimed against Cineplex for damages and losses suffered as a result of these breaches and the Acquisition not proceeding, including Cineworld's financing costs, advisory fees and other costs.

That seems a bit much. But, of course, that's what lawyers advise when somebody sues them: sue them back harder. In this case, it apparently didn't help:

The Ontario Superior Court of Justice has now handed down its judgment. It granted Cineplex's claim, dismissed Cineworld's counter-claim and awarded Cineplex damages of C$1.23 billion for lost synergies to Cineplex and C$5.5 million for lost transaction costs. Cineworld disagrees with this judgment and will appeal the decision. Cineworld does not expect damages to be payable whilst any appeal is ongoing.

Oh dear. This is rather unfortunate given that Cineworld only has a market cap of £600m. Though, of course, this is mostly the bank's problem given an EV of £7bn. There is perhaps some irony in the fact that claimed synergies usually never materialise. An award of C$1.23bn, however, seems pretty loonie.

Hummingbird Resources (HUM.L) - Updates on Yanfolila and Kouroussa

It has been a bad news-good news kind of week for Hummingbird Resources. On Wednesday, they gave an update on the Yanfolila mine:

As noted in the 29 November 2021 release, t he Company advised that the full year production forecast would be below the bottom end of the 2021 guidance range. Current gold poured for the year is currently over 82,000 ounces ("oz") (unaudited). Due to the above circumstances, the Company now expects full year 2021 production of 84,000 to 89,000 oz at All in Sustaining Cost ("AISC") range of US$1,490 to US$1,590 per ounce

They previously announced an issue with protestors blocking mine access. However, this was fairly quickly resolved;

mining and processing operations have recommenced, having ceased operations for approximately six days

So really doesn’t account for the drop in their production guidance from “the lower end of the guidance range of 100,000 - 110,000 oz” at the end of October to “84,000 to 89,000 oz”. The reality was that the share price was already telling us that they were going to miss this. Here is the reason given:

Furthermore, in relation to the Company's mining contractor excavator availability issues detailed in the Company's Q3 2021 Operational and Trading Update, the Company notes that two of the larger excavators, of a fleet of seven, that were unavailable for most of September, are back online. However, the mining contractor's excavator fleet is failing to perform consistently to the scheduled mining volume rates.

What we don’t understand is how they can appoint a contractor who isn’t performing but don’t seem to have any ability to hold them to account. Indeed, it is Hummingbird who are ending up:

o Carrying out a detailed review of the overall contractor equipment maintenance procedures and equipment status

o Seeking to bring in additional excavators to increase availability, optionality, and allow better maintenance of existing equipment. One additional unit is expected to be delivered and operational before year end

So this should be mitigation going forward but Hummingbird themselves seem to be on the hook for the costs. So potentially poor contract terms here. Overall this mine has been barely profitable in H2 on a All-in-Sustaining-Cash Cost basis.

Better news, on Thursday they announced that construction was commencing on their Kouroussa mine:

Mobilisation of equipment and personnel has begun to enable construction to commence in early January 2022 by the Projects' construction and engineering firm WACOM, inline with the Project schedule and targeted first gold pour by the end of Q2 2023, as detailed below.

With a market cap of just £55m, this is incredibly low for a company that has successfully built a 100koz mine (when operating correctly) and is fully funded for a second one. However, the operational problems at Yanfolila keep coming up and each time you think that trust in the management competence can’t go any lower, they manage to find some way of making it sink further. This makes Hummingbird an investment only for the very very brave (or perhaps foolhardy!)

Hunting (HTG.L) - Year End Trading Update

Trading during the final quarter of 2021 has remained in line with management's expectations, with a broadly break-even EBITDA result anticipated for the full-year.

Broadly break-even at an EBITDA level shows how tough it has been for oil service companies. However, the outlook for 2022 is looking much better:

The Group's order book has strengthened by c.20% in the three months to 30 November 2021 with a significant uptick reported in North America and Europe. The order book will increase further in December following strong contract wins by Hunting's Subsea business, coupled with a general increase in successful bidding within the Group's US and Asia Pacific businesses.

This bit is also good news since Hunting Titan produced almost all the operating profit during the last period of oil price strength 2017-2019:

US onshore activity continues to strengthen, benefiting the Hunting Titan operating segment whose results remain ahead of expectations.

This is good news since Hunting Titan produced almost all the operating profit during the last period of oil price strength 2017-2019.

The Group's balance sheet remains strong, with a cash and bank position of $77.2 million as at 3 December 2021. Capital expenditure outflows remain low and management continues to closely manage working capital as market conditions stabilise. Further, the Group is now likely to conclude the arrangements for its new Asset Based Lending facility in the coming weeks, as due diligence is completed by the lending group.

So cash is down $6m from 30/6/21 but given that they spent $5m buying a stake in Cumberland Additive Holdings in the period, this is actually impressive resilience.

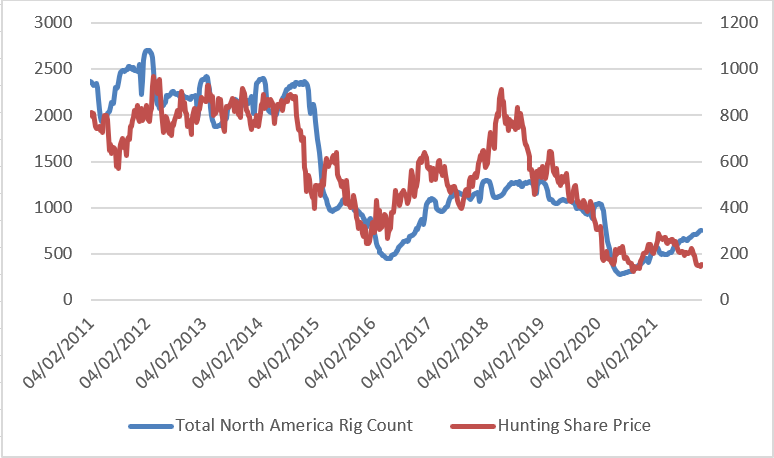

As we have argued before - the movement in rig count is much slower than past cycles, presumably from lack of capital and the need to re-invest current high cashflows rather than borrow against future ones:

Although the correlation is noisy, the recent weakness in the Hunting share price seems to be unjustified by the rig count moves (at least in their largest market of NA):

Following further due diligence, the Board has also decided to postpone its plans to launch a level two American Depositary Receipt programme, however, this decision may be revisited at a later date.

This isn't great news since Hunting is a bit orphaned on the UK market with no real comparators, so is likely to be under-researched. A US ADR would at least raise its profile to more natural investors. Although with O&G persona non grata with investors at the moment not sure it would make a big difference.

Still, the investor here is getting £1 of, largely liquid, assets for 50p which can overcome a lot of negative sentiment with enough patience.

That’s it for this week, hope everyone is having fun getting ready for Christmas!