Small Caps Live Weekly Summary

AGFX MRK AO. CAR DIS DLAR NXR SNWS TET TIDE

Another understandably quiet week for UK small cap news. However, it feels like the markets have been anything but quiet. Illiquidity has meant some larger-than-average moves on no news, or tips. In such times, it is worth keeping one eye on the markets or at least setting some price alerts. These can be great times to take advantage of a clumsy seller or an uninformed tip buyer.

Argentex (AGFX.L) - Final Results

We’ve been critical of this company in the past for what appears to be an unnecessary year-end change, and for getting brokers to halve their EPS forecasts shortly before then announcing that they were going to beat them. This smacks of a company far more committed to managing their share price than the business.

However, the revenue growth rates here are impressive:

Group revenue increased by 63% to £41.0m compared to the same period last year2 (FY22: £34.5m)

EPS growth is much less so:

Earnings per share (EPS) of 6.2p basic and 6.8p adjusted (FY22: 6.6p basic and 7.0p adjusted)

The shift of year-end means that these figures are 9m vs 12m, though. We can’t see any comparator on EPS for the FY, so it is hard to objectively assess. The shares reacted negatively to these results, though, so shareholders were presumably unimpressed.

Lots of talk of growth but also growing headcount:

To further accelerate our global growth strategy, we will continue to invest in people, doubling the footprint of our UK, European and Australian headquarters during H1 2023 as planned.

Like many people businesses, the staff will probably take the lion’s share of the rewards here.

Mark’s Electrical (MRK.L) - FY23 Trading Update

Looks like a beat.

After an improvement in profitability in the third quarter, we continued this trajectory with improvements in gross margin and operational leverage, allowing us to exceed our full year targets on profit and cash conversion, even as we grow market share.

They also talk of a positive start to April. Equity Development say:

Marks Electrical enjoyed full year 21.5% sales growth in FY2023. Momentum remained strong throughout the final quarter, with a 21.5% gain in March 2023 as well. Margin gains were complemented by improvements in working capital and inventory management, which resulted in strong cash conversion. The closing net cash position was positive to the tune of £10m.

However, they also say:

our forecasts include an expected half point reduction in gross margin in FY2024

And have cut EPS forecasts by 7.1%. The EPS cut is despite what looks like an upward inflation-related adjustment to revenue forecasts. They left both 2023 and 2024 forecasts unchanged after the January update, and indeed 2024 was last adjusted in October. If you take the view that the consumer outlook has worsened since then, I can see why a 2024 downgrade once 2023 was (pretty much) known would not be a surprise. Canaccord raised 2024 EPS forecasts from 4.6p to 5.1p (versus ED dropping from 5.7p to 5.3p), further suggesting ED were behind the curve.

Still, a last-minute (albeit well-flagged) beat for 2023 doesn't alter the fact the company has significantly and repeatedly cut forecasts since coming to the market. An upward trend would better support the current forward PE of 17, which looks expensive in the current climate.

AO World (AO.L) - Trading Statement

Hot on the heels of Mark’s beat, we have one from AO also:

The potential adverse effects from trading risks, continuing macroeconomic uncertainty and tough consumer environment that we anticipated at 28 February have not materialised to the extent envisaged and as such we are updating our profit guidance to around the top end of profit guidance issued at that date.

On margins and costs:

Consistent with the themes set out in the trading statement issued on 28 February 20231, we continue to see positive traction from our initiatives to reduce costs and improve margins.

That trading statement said:

Consistent with the themes set out in the trading statement issued on 10 January, we continue to see traction from the initiatives taken by the business to reduce costs and improve margins.

It was not clear from previous trading statements much of the hoped-for margin increase was expected to come from increased prices and how much from lower costs, but based on the market share numbers, it looks like the increased prices / lower share element has mostly run its course, whereas from the commentary that cost-cutting is continuing to proceed. Which is bad news for competitors.

Also bad news from competitors is the availability of capital, e.g. for exceptional costs from closing excessive infrastructure:

The Company's £80m revolving credit facility has been renewed with HSBC, NatWest, and Barclays, extending to April 2026. At the period end we expect to be holding a modest net funds position on a pre IFRS16 basis, reflecting an improvement of circa £20m from our interim position at September 2022.

So it seems that AO. shares should have bounced significantly from the lows where it looked like they would continue full speed into bankruptcy. The low was around 38p, now around 68p. That potentially understates the improvement in the prospects,. However, they still have a large exposure to expensive mobile phone contracts and terrible value extended warranties.

The mobile contract issues stem from providing consumer credit without disclosing the APR. Although it would be difficult to calculate the APR as the contracts typically include an in-contract RPI+ increase not just on the airtime part (which is subject to some inflation), but the credit part, and also rely on consumers forgetting or not realising that much of the monthly cost was repayments for the phone and continuing to repay after the contract is over.

The market leader in the terrible value extended warranty market is Domestic and General, who feature regularly in financial agony aunt pages. Recent stories have included (the likes of) a 90-year-old lady who has been paying £10 a month to insure a £200 VHS video recorder for the last 20 years so she can keep watching videos of her grandchildren who have moved to Australia, but when the video recorder breaks D&G tell her they can't replace it and wouldn't have been able to do so at any point in the last ten years. Another case involved a widow who was without a fridge for two months after they kept failing to replace it. It would have been more than two months, except the lady died, with some suggestion stress was a factor.

So, in short, a large exposure to things overdue for regulatory action, albeit industry lobbying may prevent action before the election, and there is quite a long list.

Carclo (CAR.L) - Trading Statement

Quite a detailed update, where the crux of the matter is:

…the overall full-year profit performance is anticipated to be below the previous year. As a result of the new focus on cash generation, the Group expects to deliver an improvement in net debt compared to the position at the half year, whilst having continued to make significant pension deficit repair contributions.

Forecasts were already for lower EPS, so it’s really hard to work out if this is good news or another profits warning. However, the market has certainly taken it as the latter. There is little good news in the rest of the statement. Not all banking covenants appear to be waived yet:

Discussions are continuing with HSBC regarding the setting of appropriate covenants for the forthcoming financial year.

And no resolution on the cancelled manufacturing agreement:

We previously announced the dissolution of a significant manufacturing contract and are engaged in ongoing discussions with the customer to reach a commercial agreement for this contract.

So either way, very significant risks remain, and it is not clear that the equity has any value.

Distil (DIS.L) - Trading Update

With the gin craze well and truly over, the spiced rum market saturated, and their duty-free brands (led by Bladvod) never quite recovering after covid, even before Russia invaded Ukraine, it is not surprising they are having a difficult time. The trouble is that in the good times, all the cash generated went on more marketing. A least that gave them something to cut back on.

· Volumes decreased 40%

· Revenues decreased 37%

· Investment into advertising and promotions decreased 66%

The trouble is that a change to distribution arrangements obscures the true underlying picture, which the narrative suggests is much better. We are sceptical. Despite taking an axe to marketing, cash is down from £1.6m to £0.5m in 6 months.

Progressive points out that Q4 was better than Q3. Given that Q3 includes the run-up to Christmas, that would seem to be a positive for a drinks company, especially if they cut marketing. Again, it is all about the channel.

Speaking of which, Blackwoods Gin has sunk without a trace. It wasn't a bad gin for general drinking and was often good value in supermarkets. A quick Google search suggests it is no longer available anywhere! Another quick Google shows Red Leg to be widely discounted to £16 from a typical price of £20.50 in 2018.

Assets are dominated by a complex interest in Ardgowan Distillery Company. This is a convertible loan note with benefits, but with an interest rate of just 5% and bullet repayment in 10 years, it is difficult to take the valuation at par seriously. Following today's profits warning, the claimed value of the investment in Ardgowan is likely to exceed the entire market capitalisation of Distil, and so a detailed knowledge of it is vital. Here they say:

Progress remains positive at the Ardgowan site, with internal renovation works to the gin building complete, and the still due for installation in May. The team is working closely with Ardgowan to design the visitor experience, with plans to invite trade later this year once works have progressed further across the wider site.

How much is a distillery with no still worth? The risk is off the scale here.

De La Rue (DLAR.L) - Trading Update

Another profits warning here:

For FY23, De La Rue expects full year adjusted operating profits to be a mid-single digit percentage below market expectations

And they are setting up for one in 2024 too:

The downturn in Currency, impacting both De La Rue and the wider industry, is causing a significant degree of uncertainty in terms of outlook for FY24. The demand for banknotes has been at the lowest levels for over 20 years, resulting in a low order book going into FY24.

At least net debt is in line:

Net debt as at 25 March 2023 is expected to be in line with market expectations.

However, the balance sheet looks shaky here, even before considering the massive pension deficit.

The board here are under-pressure from activist holder Crystal Amber, who ae seeking to oust the Chairman. Even they are expecting a raise here. In their own update this week, they say:

…the Fund intends to retain sufficient liquidity out of the Initial Consideration to continue to fund growth at GI Dynamics and protect the value of its holding in De La Rue.

Last time De La Rue ran out of cash, a strong update saw the share price rise from 40p to 160p and a £100m placing at 110p. No such luck this time. This week’s miss puts them firmly in Rights Issue territory.

Norcross (NXR.L) - Trading Update

South Africa is weak; the UK is strong. Giving an in-line statement overall. Of course, the reason this is on a forward PE of 5.2x is the size of the pension fund and the policy of aggressive debt-funded expansion in an attempt to outgrow it.

The Group remains in a strong financial position with net debt (on a pre-IFRS 16 basis) at 31 March 20231 expected to be circa £50 million (2022: net cash of £8.6 million). The year on year movement principally reflects the acquisition of Grant Westfield.

The Group has extended its £130 million multicurrency revolving credit facility ("RCF") for a further year. The facility has a three year and seven month term to October 2026, with a further year extension available. It also includes the option for an uncommitted accordion facility of £70 million.

Nothing is said this week about the pension, but much of the detail was disclosed in November. And overall, this means they are on a cash flow yield of around, 10% even taking everything into account. This makes them reasonable value but not exceptional in these markets given the risks of operating in South Africa, plus the debt and pension deficit.

They flag up a further exceptional cost coming up too:

It is with regret we have commenced the closure of Norcros Adhesives, a small but loss making division with the loss of 70 jobs...costs relating to the closure of circa £5 million (of which circa £2 million represents the gross cash cost) will be separately reported as an exceptional item

But as the cash payback is less than a year, the impact on year-end 2024 debt will not be significant.

Smiths News (SNWS.L) - Contract Renewal - News UK

We’ve been critical of the market reaction to these sorts of contract renewals in the past. Given the regional monopolies in a declining market, it would only really be noteworthy if contracts weren’t renewed. And, of course, these say nothing about pricing, which falls on the retailer.

However, this one is potentially good news compared to other contract renewals. We believe News UK do their own distribution in Greater London, which is, of course, the densest (and therefore presumably the most profitable) part of the regions to distribute newspapers to. That News UK isn’t expanding their territory and is keeping Smiths News for the rest of the regions reduces one of the risks. (Although, this doesn’t drive any more sales just keeps the sales declining at the same rate.)

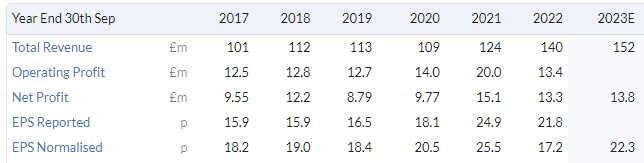

Treatt (TET.L) - Half-Year Trading Update

· Record H1 revenue with 15% growth (8.5% in constant currency) to £75.9m (H1 2022: £66.3m)

· Profit before tax and exceptional items growth to at least £7.1m, up by c12% (H1 2022: £6.3m)

In the context of the food and beverage inflation seen in 2022, 15% revenue and 12% adjusted PBT growth doesn’t look particularly “strong”. They must have faced volume declines from manufacturers though, so a credible performance in this respect.

Trading in line with the Board's expectations for the full year

If the board’s expectations match the brokers’ forecasts, in line means 29% growth and could justify their 28x forward P/E. However, viewed in a longer-term context, this is just a bounce back from a poor 2022, and it seems to be simply pass-through cost increases taking time, so not really underlying organic growth. Indeed, hitting 2023 forecasts would mean that EPS has only grown 22% since 2017. At best, in line with inflation.

This suggests that this perhaps is more deserving of a single-figure P/E. We’d perhaps be a little more generous than that, given the defensive nature of their business. However, the current rating appears to be investors getting carried away with a story that never seems to appear in the numbers.

Crimson Tide (TIDE.L) - Preliminary Results

· Revenue increased by 30% to £5.4m (2021: £4.1m)

· Annual Recurring Revenue (ARR) increased to £5.75m (2021: £3.8m)

The ARR growth at +51% catches the eye, so we’re not sure why they didn't present it as a percentage. Unfortunately, they didn't even make fake profits, with a small EBITDA loss. Cash burn was £2.1m (36% of revenue). The last fundraise was £6m gross in April 2021.

When Leo looked at them in the past, he concluded that Luke Jeffrey, Product Director, has built a nice product. That just wasn't gaining traction. The business model looked real enough, although extraordinarily high director pay cast doubt on whether it was a genuine company from an investor perspective. Since then, the pressure to improve productivity has increased, and some of the conservatism toward automation has reduced, but competition has also grown. Since their April 2021 fundraising, the business model has looked more suspicious.

At the current share price, the ARR multiple is 3.5x. In the past, there were people who would argue that alone made it cheap, but that was never a view we subscribed to, and we haven't seen anybody arguing that P&L and cash flow are irrelevant for SaaS companies for a few years now.

With the world moving to SaaS, investments into technology are unlikely to be one-off, though integration/configuration elements will have some element of that. People are probably actually easier to get rid of than the SaaS subscription nowadays. There is some clue about what would happen if they cut marketing (which for SaaS companies often includes a large element of ongoing support) at the end of the statement:

Crimson Tide's Annual Recurring Revenue (ARR) contracts are typically on an initial 36-month subscription basis, with many extending and expanding significantly beyond the initial contracted date.

For those who are in just to enjoy the ride, the key question is when they will next need to raise cash.

That’s it for this week. Have a great weekend!