Small Caps Live Weekly Summary

Bargain Shares Tips CTG CHKT HEIQ JSE ULTP XPP

Last week, the Investor’s Chronicle published its well-received Bargain Shares 2024 article. We are often sceptical about the longevity of tip-based share price moves. Market makers often mark tipped shares up on the open and, hence, are the real beneficiaries of such articles, not investors. With this in mind, our gut has long told us that the right thing to do is to sell into any spike upward caused by tip-buyers. After all, tip buyers are usually the least-informed market participants. But what does the data say? This week, we found a bit of time to find out.

We looked at the excess return of the IC’s “Bargain Shares” versus the FTSE250 (not the perfect index for mainly small-cap picks, but the one we could easily access the data for) after the articles were published for the years 2018-2023. Here is what we get:

We compared two averages, all years and just 19/22/23. The reason is that 2018 benefited from a commodity bull for several picks, 2021 a major small cap bull market and 2020 a big sell-off followed by a big reversal. Unless investors are expecting a huge small-cap rally in 2024, then the 19/22/23 average line is more representative. So what do we learn:

The bulk of the gains occur on the first day and may even occur before trading begins. Hence, the Market Makers are the big winners from these types of articles.

Our initial assumption that it is all over by the end of the day is wrong. Shares continue to gain, although at a much slower rate, for another week.

If you haven’t yet sold into the tip rally, then it isn’t too late, but you’ll need to be quick, as the shares will likely start to decline at the start of next week.

After this, the tipped shares are likely to decline for the next 30 days or so and give up most, but not all, their gains.

2024 tips have underperformed on average, so they may well give up all their excess return within 30 days. Although this may be due to the presence of some cash-rich stocks. For example, Oxford Metrics has risen about 18% on this tip, but the large cash balance means that the value of the operating business has risen 36% in a week. These sorts of gains, on no news, are by nature unsustainable.

In terms of actual stock-specific news, it has been a relatively quiet week on SCL. It is not so much the lack of announcements but a lack of materiality. There have been quite a few in-line trading statements, but they tend to be from companies such as:

Christie Group (CTG.L)

Where they say:

The full year result, before exceptional costs, is expected to be in line with market expectations which were revised in early December.

“revised” here, of course, means slashed. And they leave the door wide open by excluding exceptional costs:

As previously reported, the Group will report exceptional items as a result of the July 2023 Board changes, together with some restructuring carried out in its operations in both the PFS and SISS divisions during H2.

That makes them sound significant, and the idea that the best they can do is an H2 operating profit excluding these is rather underwhelming.

Or companies such as:

Checkit (CHKT.L)

better than expected

Means an “adjusted LBITDA” of £3.4m. That’s Loss before all the other real costs of running a business! It may have halved from the previous year, but it is still significant compared to a £12m revenue company.

Here are some things we did think were looking at in more detail:

Heiq (HEIQ.L) - Acquisition, Placing & Trading Update

This is billed as a placing to fund an acquisition, but underlying issues or to raise some cash on the side is a common trick. Particularly when the announcement also includes:

A profits warning

An auditor resignation

A change of year-end; and

A change of base country.

And, of course, they have to do a capital reorganisation because they are issuing (far) below nominal value. Just to recap on the auditors: Crowe resigned in 2022, having sent a letter under S520 of the Companies Act, which is usually bad, but their PR company ignored Leo’s request to send it to him. Deloitte did one audit highlighting several problems and has now resigned.

The big question here is why they are so much in a hurry to raise the cash that they can't wait for a GM and thus have an arrangement involving CLNs. This is the claim:

The Company was able to move quickly and, as a result, agreed a consideration of approximately €5 million (including taxes) for the Acquisition, which the Directors believe represents a significant discount to market prices for similar properties.

But they also say:

Cash as at 31 December 2023 was approximately $10 million having utilised additional headroom under the Company's current facilities, with net debt position, excluding liabilities from lease contracts, of $2 million at year end.

So either they are being very cautious, or they have actually run out of money and not revealing that part. It may well be that the debt facilities are about to be called. A previous audit found that:

It was determined that property capitalized as a right-of-use asset was owned by HeiQ Chrisal N.V. rather than leased - and the corresponding liability was that of a loan rather than a lease in nature.

So, it is probably safer to use this as the net debt figure:

Net debt including lease liabilities amounted to approximately $10 million (as at 31 December 2023).

Here's another idea of what might be behind this:

HeiQ has secured an initial EU/Portugal grant "Bioeconomia" up to approximately €10 million for investments in facility equipment, machinery and further R&D activities at its newly acquired AeoniQ facility.

So, this may also be about accessing that grant funding. The offer is at 8.7p, so at an all-time low, but at least the directors are putting in material amounts. Given the other issues, we are not tempted to follow them into the accompanying retail offer.

Jadestone Energy (JSE.L) - Response to Speculation

A big potential deal here:

The Proposed Acquisition would include Woodside's interests in the Macedon producing gas field and a cluster of producing oil fields collectively known at the Pyrenees Area. For reference, Woodside's net working interest production from the Macedon field and Pyrenees Area in the second half of 2023 averaged c.28,000 boe/d.

So big indeed that it would count as a reverse takeover, and Jadestone are now suspended until they are either out of the race or complete the deal. This is a shame because the market often dislikes uncertainty but rewards these types of deals as they turn out to be bargains. We don't think they'd enter discussions without some idea of financing, which means either an expanded Reserve-Based Lending facility or they will have commitments for equity. They won’t want to want to dilute at the low price they traded at before suspension; we can easily see them raise at a significant premium. They'd probably like to even get it done at the 45p level of the last raise. That may be a stretch, but at the end of the day, it depends on how compelling the deal for the assets is.

Ultimate Products (ULTP.L) - Trading Update

This starts off sounding like a profit warning caused by complacency over those air fryer sales and delays in inventory normalisation:

During the period, unaudited Group revenues decreased 4% to £84.0m (H1 2023: £87.6m), with supermarket ordering held back by overstocking issues, strong prior year comparatives bolstered by the exceptionally strong demand for energy efficient air fryers in H1 2023, and some modest revenue deferral at the end of the period due to the recent disruption to global supply chains.

But higher margins save the day. All three brokers have stuck with their previous EBITDA and profitability forecasts, but this is a definite sales miss. Their sales guidance has always been based on percentage YoY growth, so it is not surprising that there are cuts for next year and the year after as well. However, unusually for this stage, they are guiding +8% rather than the standard +6% for FY7/2025 over FY 2024, suggesting a small amount of catchup and perhaps reflecting higher inflation.

As well as a trading update, we get the change in capital allocation:

The Board's intention is to maintain the net bank debt/adjusted EBITDA ratio at around 1.0x.

This seems perfectly financially prudent, given their working capital profile. All this is doing is financing part of their receivables. The important thing is to keep tight control over their inventories in any downturn, but they never had any problems with that in the past, even without the level of branded sales and online channel they have now and despite prior high-to-extreme customer concentration.

However, we’re not sure it is quite so prudent in terms of the effect on the share price and their ability to do deals. Shareholders have fairly regularly freaked out in the past when trading has turned down or looked like it might, and one of the reasons is their level of debt and, in particular, short-term debt/adjusted EBITA.

The excess cash is going on buybacks. They require a white-wash waiver, so at the moment, this is merely an intention rather than a reality. But is buying back shares on a forward EV/EBITDA of 6.7-7.1x (depending on whether you take peak debt or period end) really the best use of capital here? They obviously feel their shares are cheap, but are they really the best judge of that? Prior to COVID, they traded on a P/E of 9, and today, they are on the same rating.

Of course, shareholders aren't going to complain if the price goes up (and they do the wise thing and sell shortly before the buyback ends), but it seems like a poor capital allocation decision unless there really aren't any acquisition opportunities going for sub 6x EV/EBITDA.

XP Power (XPP.L) - Trading Update

Looks like a major profits warning here:

The Board has concluded that there is likely to be a shortfall in revenue in 2024, leaving the outlook for 2024 significantly below market expectations. This is based on recent order intake, revenue performance and discussions with customers, particularly within the Healthcare and Industrial Technology sectors, which confirm unusual, temporarily soft demand conditions and destocking. These softer trends have also emerged within our direct industry peers.

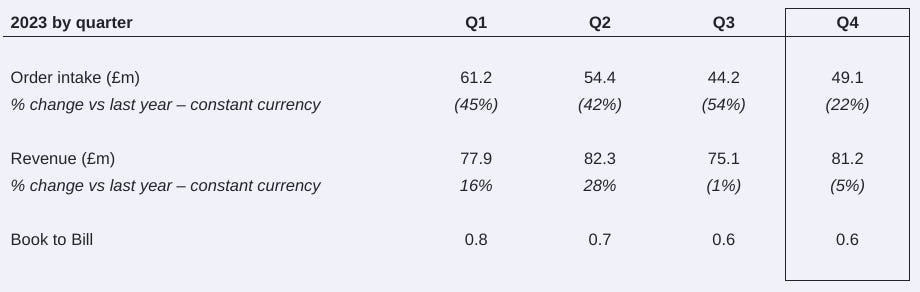

We were surprised Edison didn’t cut 2024 forecasts when they issued a positive trading update for FY23, with Q4 ahead of expectations just 5 weeks ago. The book-to-bill last year suggested it was just a matter of time:

Today, 7 weeks after the period end, they have just realised these will miss by £4m:

Our year-end financial close processes have identified some capitalised product development costs that needed to be amortised or impaired, adding £4 million to costs.

They claim this is non-cash, but of course cash was originally spent in the development, possibly in the current year. So, we did know about the cash already; what we didn't know was that it went down the drain.

Underlying operating profit for full year 2023 absent these costs was in line with our expectations.

So they're adjusting this out. It must be a one-off, then? But then they say:

Approximately half of this is one-off in nature.

We’re confused because they seem to be saying they are excluding all of these costs from the underlying figures, not just the exceptional part. Meaning that the underlying figures are not to be trusted.

We are also not 100% convinced they have taken the necessary inventory write-downs and have de-capitalised all the required development spend. So we don't particularly trust the unadjusted P&L either.

Still, there are reasons to focus on cash, and the news here is good, albeit only relative to previous expectations:

The Group's cash generation toward the end of 2023 was ahead of expectations ... and we expect this to continue in 2024 with net debt below our prior assumption.

But there is no hiding that debt remains too high. They raised less cash than we thought they needed, and they remain one more cash stumble from further serious problems:

net debt/EBITDA at 31 December 2024 at or below 2.5x versus a covenant limit of 3.5x.

They also have forecast an H2 weighting, which could easily fail to materialise or materialise too late for cash.

Institutions have the right to feel aggrieved here. They appear to have been talked into putting fresh cash in at a premium last year, presumably in order to not have to mark down their existing holdings. Only to have the whole lot marked down today.

That’s it for this week. Have a great weekend!

Thanks guys, interesting read as usual. :)