Small Caps Live Weekly Summary

GMS KINO QRT SOM WRKS

Straight into results this week:

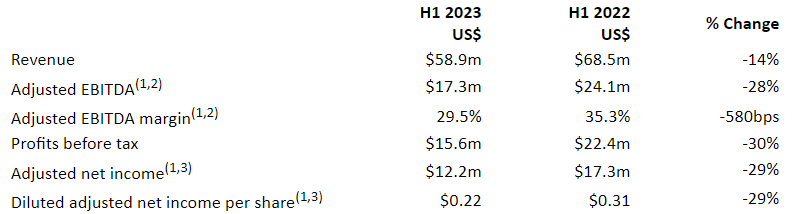

Gulf Marine Services (GMS.L) - Interim Results

Some positive moves here:

Although, strangely, they missed this bit from the table:

Net profit attributable to shareholders for the first half of 2023 amounted to US$ 8.7 million, reflecting a reduction of 34% year-on-year, (H1 2022 US$ 13.1 million), as increase in financing costs of US$ 10.9 million more than offset the results obtained from operations.

Do we sense a bit of a Partridging there? There is a small upgrade to EBITDA guidance:

EBITDA guidance for 2023 is projected to be in the range of US$ 77 - 85 million, being USD 2.0 million higher on both the lower and the higher ends of the previous estimate, supported by an improved forecasted utilisation for H2.

But of course, this means H2 guidance of US$32.7-40.7 EBITDA, between 8-24% lower than H1.

The cash balance went down in this half despite a $42m operating cash flow. And very little of it was spent on capex, which was just $2m. Here is where it went:

With $300m of debt remaining, they pay it off in 6-7 years (assuming interest rates don't increase significantly). Their depreciation rate suggests that their fleet has a 20-year life left on average. Which may be possible. Their oldest ship was built in 1995. The average ship age is around 10 years old. But it would be daft to ignore depreciation here. These assets are literally rusting away.

The problem here has always been that when you debt-adjust the P/E, it is around 20. The story that it will come down significantly as rates increase never seems to be reflected in reality. And with an ageing fleet, time is running out for this to happen. There is much better value elsewhere in these markets.

Kinovo (KINO.L) - Possible Offer

Potential bidder for Kinovo, Rx3, fill shareholders on their thinking about the pricing of any potential offer. On DCB Kent, they say:

The exposure is therefore not a contract relating to £4.3 million but contracts equating to £18 million and until these have all been successfully completed and the £14 million expected receipts from DCB's clients actually collected, it will not be known whether the provision of £4.3 million is adequate. Indeed, this figure has already been increased from £4.3 million in the 2022 statutory accounts to £5.3 million in the 2023 statutory accounts, with this figure offset by a yet to be agreed claim against DCB's structural engineers of £1.0 million.

On the market value of the shares versus the minimum offer of 40p:

Despite Tipacs2's significant support in the placing of Western Selection's holding, Rx3 understands it was a protracted sale process, taking several weeks to place the remaining shares. Tipacs2 was prepared to pay a premium to what it regarded as the real market value at the time in order to maximise its strategic holding at 29.89%. The difficulty that Western Selection had in selling down its c.12.0% stake, even with Tipacs2 taking the maximum amount of the order that it was able to accept, clearly demonstrates that the current share price does not reflect the true market value for a significant seller of the Company's shares.

Basically, they are telling other shareholders that they have bid the value of the shares up too high, given the major contract risks that remain, and the illiquidity of the shares. The point they are making is potentially valid: that they chose to overpay for the shares at 40p to obtain control, that no one was particularly keen to take the rest at 40p in July this year, and that the only thing that has changed since then is a certain amount of private investor exuberance for the company developing on Twitter/advfn. For example, there were results in July and a couple of framework announcements, but these didn't really seem to move the price.

However, this misses that the overhang itself seemed to cause the drop down to the low 40s, and the share price was approaching the current level prior to that. So, although 40p may be the clearing price for a large stake, the clearing price for the smaller investors that they want to vote for their deal is around 50p.

Individual investors like us can often be the least savvy investors, especially when it comes to assessing risks within a business. However, if Rx3 don't want to bear the risks of DCB Kent's contract guarantees, then they don't have to make an offer for the whole company. But likewise, if the largely PI shareholder base is happy bearing these risks, then they don't have to accept the offer.

Presumably, the 56p mooted price was calculated as a 40% premium to the 40p price they bought at last month, which may be reduced as they do their due diligence on the current state of the DCB Kent contracts. So despite the partial logic of the Rx3 position, this bid as a scheme of arrangement looks doomed to failure. Rightly or wrongly, smaller investors simply value this company more highly than Rx3 does.

Rx3 probably realise by now that they won't get the 75% for a scheme of arrangement too and will have to make a normal offer if they want to proceed as they also said the following in their announcement:

Rx3 has not determined whether any offer, if one is made, will be made via a scheme of arrangement or a contractual offer, and Rx3 is considering all options available to it. In the event any offer is made via a contractual offer and is successful, any remaining minority shareholder should be aware of the implications of being a minority shareholder of a company under majority control and the control such a majority shareholder would have.

This is obviously the stick part of their attempt to get shareholder compliance. If they get more than 50% either from those accepting the offer or by buying in the market at or below the offer price, then they could make some aggressive moves. The first is probably to remove the board and put in their own representatives. There is no dividend to cancel here, so that is unnecessary. But they could have a large rights issue, thus forcing the holdouts to put in a lot of extra cash so as to not to be diluted out of their position. If they get to 75% acceptance, then they will delist, of course.

They will also have to bid without the current board’s consent, as on Friday, the company announced that:

The Directors have concluded that if the Possible Offer of 56 pence per share was made by Rx3 they will not be recommending it to shareholders. The Directors have undertaken a process of consultation with certain key shareholders and considered direct shareholder feedback in reaching this conclusion.

Larger shareholders that can easily put in a few million pounds more to back their position, and are willing and able to hold a delisted stock for as long as it takes, may then be able to find out whether their assertion that this is worth much more than the mooted offer price is correct. Everyone else may just end up capitulating to a hostile offer eventually.

The other thing to consider is what Rx3 may do if they don’t choose to bid or a bid fails to get 50%. They may just keep holding, but with the price still above what they consider fair value for a non-strategic stake, they may just flip the shares they bought at 40p for a nice turn. Especially since their DD on DCB appears to have yielded a worse situation than they initially thought. If they choose that route, it is unlikely that the non-institutional shareholder base could absorb all the selling and still see the price rise, and with the share price becalmed in the 40s for a couple of years, most will have got bored and moved on. They may even be able to buy back more sub-40p at various points when equity markets are weak. Come 2025, the risks of DCB Kent's contracts will have been resolved, and they may be able to make the offer again at the same price with lower risk. All in all, this doesn’t seem to be a great situation for anyone.

Quarto (QRT.L) - Half-Year Results

Mark is a little disappointed with these results. LfL sales are down 10%. These are definitely tricky markets for anything consumer-facing, but the adjusted PBT for H1 has halved:

There are no market forecasts, but if these trends continue into H2, we can expect the historical P/E of 5 to look more like a P/E of 10. The outlook is vague, but it looks like there are tailwinds that may see an improved H2:

As we move into H2 we expect the challenges seen in H1 which have been impacting trade sales to continue. With the expected fall in inflation across both the US & UK, we should start to see a softening of the cost-of-living crisis and more buoyancy in the market.

Some of the H1 weakness was timing in US custom sales, too:

Foreign language sales are expected to hold firm, with strong orders in the pipeline and Custom sales whilst down year on year, are expected to recover during the second half of the year.

Lower freight costs should give a benefit:

After the recent period of volatility in freight in terms of lead times and costs, we have seen significant improvement in both areas. This will allow us a greater number of options when sourcing our print, enabling us to be nimble whilst ensuring competitive pricing.

So, together with a seasonal H2 weighting, perhaps we can expect an EPS of around 25-30c for the full year, overall? This will still be down on FY22, but not as much as H1 taken in isolation would imply.

In contrast, free cash flow has been excellent at over $10m inflow in the 6m period versus a $60m market cap. The bulk of this has come from the better collection of receivables, but these now match payables in size, and there is still $20m of inventories, so this doesn't look like an unsustainable move in working capital. They haven't achieved it by cutting back on book development either, as investment here matches amortisation. This cash flow means that they have paid down all long-term debt and now have $9.3m net cash, completing the de-risking exercise started by the current management team.

In light of this, the 30% drop in the share price that was the market’s reaction to these H1 results looks like a bit of an overreaction. Although it’s certainly possible that the market has decided that the fair value P/E is always 5 for this stock and the price has dropped back to where it trades on this sort of rating (assuming we are right about H2 being stronger and them doing around 25c EPS). There are risks here, particularly around the presence of controlling shareholders. However, even in these small cap markets, this looks like a lowly rating for a company that isn't in financial difficulty.

Somero (SOM.L) - Interim Results

Profitability is down around 30% versus the prior year, although in line with previous guidance (after it was updated earlier in the year):

They maintain their previous guidance, and we can confirm there has been no stealth downgrade via their broker:

As such, the Board remains confident that 2023 results will fall in line with market expectations with revenues of approximately US$ 120.0m, EBITDA of approximately US$ 36.0m, and year-end cash of approximately US$ 32.0m.

The implied 51% H2 revenue weighting is by no means unusual and lower than the pre-covid average. Furthermore, the H2 weighting had been trending upwards, reaching 56% in 2019. Only in 2022 was H2 the weaker half in terms of revenue. As well as the specific product reason they have given:

The Company anticipates improvement in H2 2023 trading in our home region compared to H1 2023, driven in large part by the increased availability of the S-22EZ.

…higher residual inflation should also support H2 being higher. If anything, FY revenue forecasts look modest.

The trend for profitability is an exaggerated version of this, as you would expect. For EPS to reach forecasts, the gross margin needs to be retained, and other costs grow by less than 5% over 6 months. Indeed, they did half of their forecast EPS in this half year. The difference between the half-year figures and the finnCap estimates appears to be the tax charge. If this really does come in lower than forecast for the FY, then we could well see a EPS beat on the stronger H2, even if they are in line on revenue and EBITDA.

The problem here is the lack of visibility into FY 2024. They report:

Our US customers continue to report a high level of activity and a diverse range of projects ranging from large footprint manufacturing facilities, data centers and warehousing to smaller footprint retail, schools, and medical centers, and maintain extended project backlogs.

In the US, we do not see any indications of fundamental changes in the non-residential construction market, and the factors that have impacted the pace of work have not caused project cancellations and have not changed the direct feedback we receive from customers regarding their project backlogs.

But they are unwilling to provide any guidance beyond the next 4 months. In contrast, in 2019, the forecasts for 2020 were introduced via the same broker in March.

Looking at the product level numbers, the first thing that stands out is that no SkyScreed products have been sold for two consecutive halves. Indeed, only 16 have ever been sold. As we know, by far and away their biggest earner is boomed screeds in the US, but these collapsed by 38% in revenue terms. Part of this is the lack of S-22EZ availability, but the problem also seems to be the US's dependence on Europe for a fifth of its cement. Europe continues to be hit by higher energy costs, and it seems the US industry is unhappy about paying a premium to import. Increasing production in the US could take years, especially with uncertainty over environmental taxes, but this irrational behaviour surely cannot persist for much longer. Logistical problems, including labour shortages, are also cited as a cause.

In the worst case, surely any wider US economic downturn (which we would argue the shares are priced for) would remove the concrete shortage, releasing pent-up demand and helping enable subsidy-driven spending. Still, US boomed screeds seem to be ex-growth, with the $27.0m sales in 2016 only higher in real terms during the internet warehouse boom years of 2021/2022.

Outside the US, they are likely to have problems repeating the 2022H2 performance, which was supported by pent-up demand after supply improved. This seems to be the main short-term risk, although there is underlying growth there, which will continue for a few years even in the face of increasing competition. Despite some headwinds, buying the market leader on a P/E of 8 and a yield of 8% doesn’t seem a crazy idea.

The Works (WRKS.L) - Preliminary Results

This is another company where sales are up but profits down:

On outlook, they say:

Trading during the first 17 weeks of FY24 (to Sunday 27 August 2023) has been in line with expectations, with store LFL sales growing by 5.4% and online sales declining by 18.4%, resulting in overall LFL sales growth of 3.1%.

They say in line, but overall, these seem weak. Particularly a precipitous drop in online trading. But the real issue here is the material uncertainty in the going concern statement. As ever, it is worth looking at the scenarios. Firstly, the base case:

Store sales (which represent over 85% of total sales) during the first part of FY24 are above the Base Case requirement but online sales are below it

There is some chicken counting:

The Base Case gross margin percentage reflects the expected full year effect in FY24 of targeted price increases applied since the beginning of 2023 and also significantly lower ocean container freight costs.

Notably:

The plan makes provision for dividend payments.

On to the "Severe but plausible Downside Case scenario". As usual, the main thing we are looking for is whether their definition of "severe" matches what an objective observer may think.

Store LFL sales are assumed to be 5% lower than in the Base Case from October 2023 until January 2025.

We can infer that the base case LFLs are around +6%, so their "severe" is for +1%. As we have seen with other companies, it is patently nonsense to describe this as "severe".

In this scenario online sales are assumed to be lower than in the Base Case during FY24 despite the Group's attempts to increase them, but show recovery in FY25.

Again, nonsense. Recovery in 2025 is not a "severe downside scenario".

The product gross margin assumptions are the same as in the Base Case

Again, unrealistic. Their only concession is a direct consequence of lower LFL sales, not a separate factor:

...other than in January 2024 when it is lower, to allow for the clearance of stock which is assumed would have accumulated due to the inability to reduce stock purchases immediately in response to the lower sales level.

Under this allegedly “severe scenario” they would lose access to bank financing during FY2025 and might run out of cash:

For example, if sales decreased by a further 1% during the going concern period compared with the Downside Case, a small borrowing requirement could arise.

When we have this in the going concern, then the next thing to turn to is the balance sheet:

Overall, this is not terrible. They largely just get inventories on supplier credit, and with £280m revenue they turn them over every 46 days on average. £10m of cash is real cash with no debt. However, the big risk is that they have £98.2m of lease liabilities and just:

The accounting of leases is always complicated, but Mark’s simplistic view is that they have about £30.7m of expected losses where the value they are getting out of the leases doesn't match what they expect to get in for those stores. And this is over 4 years, if current to non-current lease liabilities gives an accurate indication of lease length. Presumably, the lease asset calculation is done on a "base case" scenario, not the "severe downside", let alone a real severe downside scenario for trading.

Perhaps the glimmer of hope with this is that net lease liabilities are down from £34.5m the previous year, which was a stronger year of trading. So, despite the weaker FY23 for profitability, the lease position is improving. They clearly will be looking to negotiate reduced rents or move stores as rents come up for renewal, which is why they are relatively active here:

This year we continued to optimise our store estate with 14 new store openings in great locations and are pleased that these new stores are trading ahead of expectations. We closed 13 stores and relocated a further three, trading from 526 stores at the end of the period. We also invested c.£1.4m in 34 store refits and continued to improve the store experience for customers by enhancing layouts, optimising the space utilisation across categories, and introducing clearer navigation and signage, supported by the evolved brand.

Plus anything they can do to improve the trading of existing onerous stores has a big impact, hence:

Sales densities in our stores remain relatively low and we believe there is a significant opportunity to increase this through winning new customers, better ranging and customer experience, space optimisation and improved product availability, all supported by a new labour structure put in place at the start of FY24. Whilst the priority in the short to medium term is to improve the existing store estate to realise its potential, in due course we will also consider whether to reintroduce a measured roll out programme, as we believe there is scope for the brand to trade successfully from at least 600 stores in the UK.

The other good news is that they clearly think a dividend is affordable, although at a reduced level:

Taking into account the foregoing and, in seeking to achieve a reasonable compromise between returns to shareholders and prudence, the Board will propose at the forthcoming AGM a final dividend for FY23 of 1.6 pence per share (amounting to a £1.0m total payment).

And they are trading in line with market expectations for a c11% rise in EBITDA:

The Board is comfortable with the compiled estimate of the market's forecast for FY24, an Adjusted EBITDA of approximately £10.0m.

And expect to increase the dividend in line with this performance. This is a 5.5% yield for this year and 6.1% for next year. Sadly, this yield is not exceptional amongst UK small caps, nor is a P/E of around 16, which is where we are on FY24 broker forecasts if we treat the net lease liabilities as debt. At a c.30p share price, this just isn't that cheap, especially when severe downside risks remain.

That’s it for this week. Have a great weekend!