Small Caps Live Weekly Summary

BBSN CAU CAPD CRPR KMR OMG SDY

A quieter week again this week, as holidays and the nice weather dampen the animal (well, discussion) spirits. Here’s a selection of the news we looked at:

Brave Bison (BBSN.L) / Centaur Media (CAU.L) - Extension of Exclusivity

With exclusive negotiations between the parties with respect of the Acquisition well advanced and progressing towards finalisation, the parties have agreed to extend the period of exclusivity for a further seven days until 26 June 2025.

7-day extension sounds like it’s a done deal, and Brave Bison just need to finalise financing. We wouldn’t be surprised to see a small equity raise there, especially as recent share price strength helps get that away. Long-term this looks to be one of those rare sales where both parties are getting a good deal. Centaur get cash, which simplifies their business and enables them to maximise value from the rest and return cash, as major shareholder Harwood is no doubt pushing for. Brave Bison get a business they can grow and has cross-selling synergies with the rest of their business.

Capital Limited (CAPD.L) - Contracts Update

Lots going on here:

We are pleased to announce our new borehole drilling services contract at Reko Diq, which is a new revenue stream for the business, and further underpins our strong operating relationship with Barrick. We have also been awarded a number of new exploration drilling contracts…MSALABS, after a strong start to the year, continues its positive trajectory with the commissioning of the state-of-the-art commercial laboratory in Elko, Nevada and new contract awards and extensions.

While it sounds good to have another revenue stream, borehole drilling looks like another activity which is driven by maintaining close relations with an existing customer, and which requires specialist equipment which will be unsaleable and difficult to redeploy afterwards. Exploration contracts are better as they will almost certainly use existing rigs and crews and improve utilisation rates. This does expose the company to more cyclical business, whereas the focus more recently has been on long-term minesite contracts.

None of this was enough to get broker Tamesis to upgrade their forecasts, and it seems there have been recent downgrades from others. So there remains much to prove in order to show that things are back on track, especially in the Nevada mining part, which is not mentioned in this update.

James Cropper (CRPR.L) - Strategy Update and Capital Markets Event

The share price here has been strong lately on the news that they refinanced their debt (or at least rumours they were about to, as the price moved ahead of the announcement). Quite what was so exciting about not being able to afford their original banking payments, we are not quite sure. They also didn’t say what the bank has demanded in return. Presumably, a load of fees and a higher interest rate.

This week, they reveal a Strategy Update, which is intended to tell us how the banks (and pension trustees) will eventually be paid what they are owed. However, there must now be some worried pensioners and regional business bankers out there, because most of this reads like it was AI-generated. For example:

cross-divisional technical platforms and synergies…

improvement and value creation…

Balancing established market predictability with positioning in priority markets with long-term growth opportunities…

greater resilience through commercial and organisational realignment…

AI does sound a bit advanced for this company, so perhaps they merely had an A-level Business Studies student in for work experience, and they helped produce this guff. Either way, the further evidence that the new CEO may have had little involvement in creating this “Strategy Update” is the inclusion of the following phrase:

Disciplined capital allocation

Something that it appears he exercised little of in his previous role at Zotefoams, if the average returns of capital during his tenure and the subsequent actions of the new management team there are any guide.

Kenmare Resources (KMR.L) - Termination of Offer Discussions with Consortium

Kenmare supported the Consortium in its due diligence process and gave the possible offer extensive consideration, despite its early stage and unsolicited nature. The Board will continue to review all opportunities to create significant long-term value for all of our stakeholders, including our shareholders.

The Kenmare board sound pissed off with this. They rejected the initial indicative 530p cash bid as undervaluing the business, but granted Oryx access to due diligence. It seems Oryx then come back with a substantially lower bid (presumably due to the weaker global economy due to Trump, Israel, Iran, etc.). The board have now told them to get lost, and stop wasting everyone's time. Which, in a separate announcement, they’ve taken on the chin and wished Kenmare well.

When it was annonced the Kenmare shares opened down 30% and below the level where they started this process:

This seemed a little harsh, as it was clear that Oryx and the board view it as worth more than the current price, even if Oryx baulked at their original level. The market therefore bounced as investors took a longer-term view again. However, it is exposed to the global economy, though, and there may be some more merger arbitrage to unwind.

Oxford Metrics (OMG.L) - Interim Results

We can see why the market was less than enamoured with these results:

Management are at pains to point out that:

Overall, trading in the second half has started in line with the Board's expectations and our usual seasonal trading patterns.

However, this management team have form for claiming everything is fine well into the year before warning. At this time last year, they guided the broker that 90% of the revenue was in the bag and then warned in September because it wasn’t. Plus, the CFO appears to have largely sleepwalked the last business she worked for close to insolvency. So we can see why the market wants to see the proof.

After all, this sounds like a further risk:

As a diversified business, we are seeing improving activity for Vicon in South America, Asia Pacific and Europe, while recent policy change in the United States relating to the timing of approved funding is starting to impact our institutional and academic customers, a sizeable proportion of our US business.

One possible translation: Our key market has had its funding withdrawn, and we are desperately trying to find other customers to offset this.

We would not be at all surprised to see a further warning on the way, after all, they say they need order conversion at historical rates, in an environment that is anything but normal, to hit current forecasts.

Still, even if one considers the management team here poor, they have been gifted a shedload of cash. If we cash-adjust current earnings forecasts, then they look cheap. And there is always the chance that markerless takes off, at high margins.

Even if they miss, and a markerless is a dud, while they keep throwing cash at the buyback, the share price will likely be supported around the current levels, which means the optionality looks to be to the upside from here. In these results, they say:

The Board has approved an additional £4m extension of the share buyback programme to take it up to £10m in aggregate.

But with current cash levels, they could keep the buyback going for a few years beyond this.

One of the risks here is that the market thinks the motion capture is going to be destroyed by AI. However, there are large parts of the motion capture business that probably can’t be replaced by AI, such as Life Sciences, Entertainment and Engineering, where they actually need to capture whatever is moving accurately.

As elsewhere in the market (cough, RWS), the AI risk appears overblown. Big companies want someone with a strong reputation, such as a market-leader, to implement AI-led solutions, not just throw it to some start-up and hope it all turns out ok. Sure, there will be some solutions that claim to AI-capture accurate motion from footage, but again, if you have mission-critical applications, you'll go for Vicon or their markerless technology, even if it is more expensive. Their strongest moat is probably their reputation and long-standing customer relationships, not their technology per se.

So, despite the concerns we’ve listed, the risk-reward at current levels looks good. However, we can see why investors who like strong management teams and/or revenue visibility would avoid this.

Speedy Hire (SDY.L) - Final Results

Even on their preferred measures, things don’t look great here:

But it is even worse, when you realise that the company falls into losses after non-underlying items. The breakdown of these is slightly different than last year, but the total is similar:

It looks like "Other professional..." is entirely recurring, and they admit that "transformation costs" will continue, with little to show for it yet:

Transformation costs

Our Velocity strategy is split into two distinct phases through to 31 March 2028, being 'Enabling Growth' (years 1 to 3) and 'Delivering Growth' (years 1 to 5). The investment in implementing our Velocity strategy and executing our transformation programme represents a significant cost to the business and will continue to do so throughout the 'Enabling' phase to March 2026. The anticipated cost (including those incurred in FY2024 and FY2025) of this phase is between £20m and £22m, with £15m to £17m expected to be non-underlying, primarily relating to incremental people costs. The remainder of the costs either represent underlying costs to the business or are capital in nature.

How on earth do they get away with claiming that adding headcount in order to try to grow the business is a non-underlying cost?! Also, how are they spending £22m on "enabling growth" without actually growing?

It would be prudent to assume "non-underlying" costs will continue at elevated levels indefinitely and flatter reported profits.

They maintain a 2.6p dividend, for a very generous yield, but it is uncovered, even by adjusted earnings, and is paid largely out of increasing their debt levels. Hence, net tangible assets decline. Despite this drop, the shares trade at a small discount to TBV. However, the big risk here is that the value of these assets are overstated. They have admitted two prior errors (failing to count stock and recording intangible software as tangible), but today they assure us:

At 31 March 2025, no indicators of impairment were identified in relation to property, plant and equipment (2024: none).

Yet, don’t the consistent losses on disposals of hire equipment indicate it is overvalued?

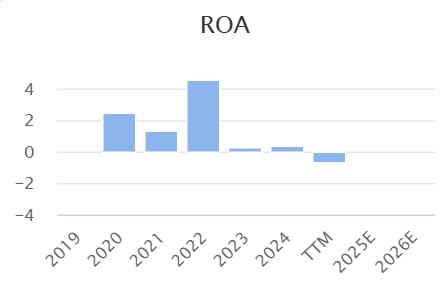

The other sign that there may be a valuation gap between book and market value is the consistently low return on assets:

It would appear that there are three options:

Management lack the competence to generate an acceptable RoA,

The business is a fundamentally poor one to be in, or

The market value of the assets is lower than book value.

None of these suggets that investors should want to be an equity holder here.

That’s it for this week. Have a great weekend!

I love the honesty of your weekly summaries and look forward to reading them. Thank you.

Do you produce a summary of businesses you think are worth investing in? How do i contact you privately (I believe you have my email)?

FWIW CRPR have two important underlying factors to consider. First the Cropper family are still very active in the firm and are hardly likely to give up their birthrights without a prolonged struggle. That could be bad, it could be good. There may still be Quaker blood in those veins! Secondly they occupy some of the most expensive real estate outside London. They could convert the mill into holiday lets and live off the profits for many more generations yet. Again, i am not sure if this is a positive or a negative. Overall too unpredictable for me, but I remain a fascinated observer.