Small Caps Live Weekly Summary

ANG AUTG BKS MRK QUIZ THRU NXR SMRT SONG

Another volatile week with the LDI pensions issues rumbling on, plus the usual political chaos. It certainly felt as if at least some of the equity selling was due to the liquidity requirements of pension funds rather than fundament changes in the underlying businesses. As always, the first rule of equity investing is never to be a forced seller.

Large Caps Live

WayneJ looks into all of the BoE goings on, plus the impact on some more esoteric bonds. Check out the thread on discord here.

Small Caps

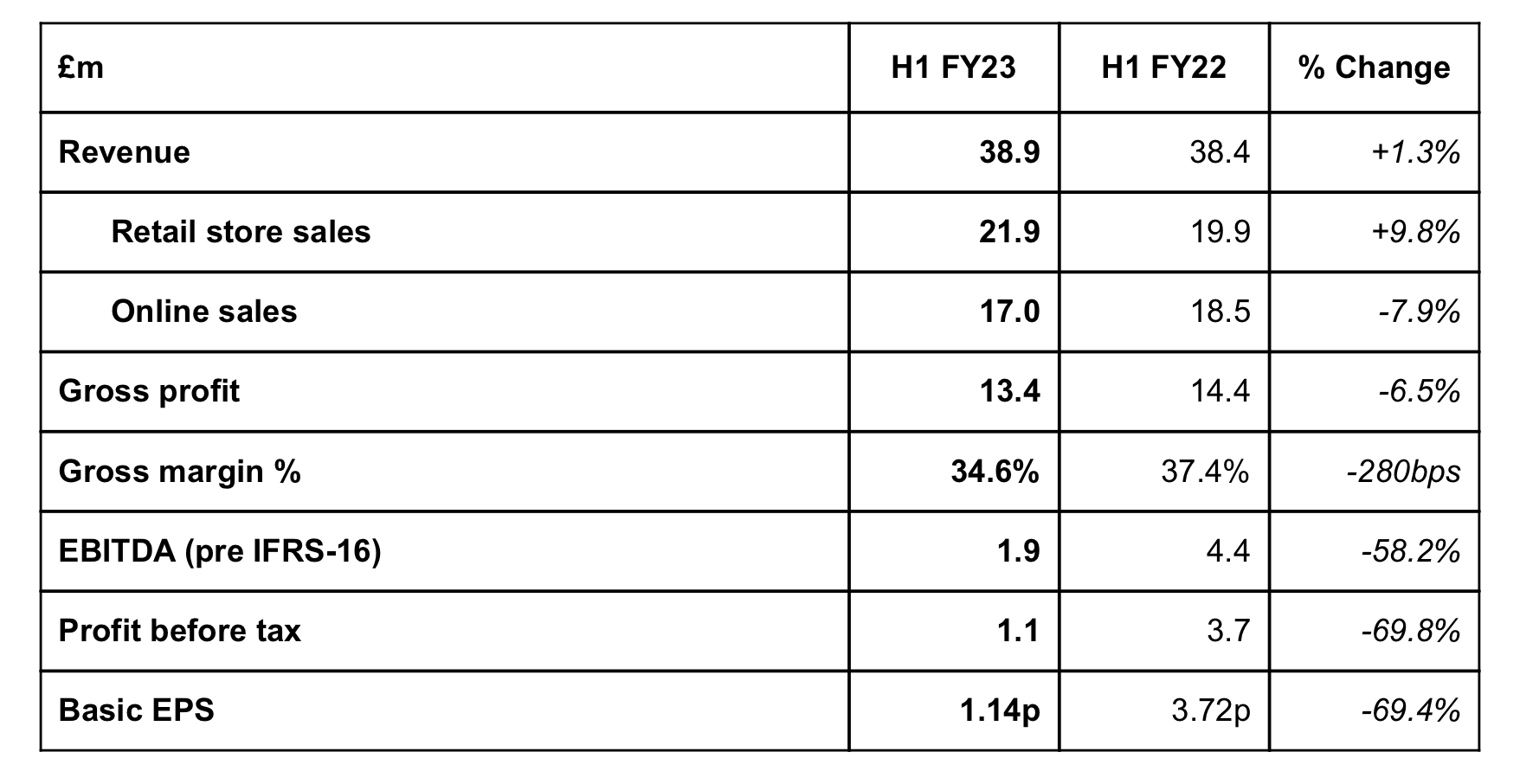

Angling Direct (ANG.L) - Half Year Results

Revenue is flat, but lower gross margin leads to a big drop off in EBITDA & EPS:

And there is a profit warning in the outlook:

Due to the challenging and highly volatile trading conditions the Company faces, and the difficulty in short term forecasting and trading, the Board believes it prudent to reduce its expectations for both revenue and pre-IFRS 16 EBITDA for FY 2023

But at least they quantify this:

The Board is confident that revenue and pre-IFRS 16 EBITDA for the year ending 31 January 2023 will be not less than £73.8m and £2.2m respectively

Not exactly great when EBITDA was £1.9m in H1. But Also, top marks for clarity here:

Angling Direct believes that consensus market expectations for the year ending 31 January 2023 prior to publication of this announcement are for revenues of £78.5 million and pre-IFRS 16 EBITDA of £3.0 million.

£17m cash is still 22p a share, so 1p EPS is a cash-adjusted P/E of 7 or so at 29p. This, perhaps, is why the initial sell-off on the day appears to have been bought into.

Autins Group PLC - Interim Results

Bad news. Lower customer volumes are continuing into 2023, which of course, we knew from tracking Vertu etc.

The unaudited EBITDA loss for H2 FY22 is expected to be in the region of £1.0m (H1 FY22: loss £0.3m).

Autins wisely conducted a placing in late 2021, which shores up their balance sheet. And their debt is Long Term, which buys them some time. Still a net debt position overall tho:

The Group ended the period with net debt (being the net of cash and cash equivalents and the Group's loans and borrowings, excluding right of use lease liabilities) of £2.4m (FY21 £2.7m). Cash and cash equivalents available to the Group were £1.5m (FY21 £1.3m).

Cash was £2.8m at the half year to 31st March, so they clearly can’t bear these losses for too long. Hence, today’s announcement of…

The Group has commenced significant restructuring actions in the UK and concluded a number of key commercial discussions that help to restore gross margins.

The problem is that any recovery in volumes will surely require working capital growth. Which will put further pressure on the balance sheet.

Beeks Financial Cloud (BKS.L) - Final Results & Contract Wins

Starting with the contracts, these are relatively small, but we much prefer several small contracts to a few big ones as there is less risk of cancellation or implementation troubles.

secured via a partner for deployments across US, APAC and EMEA.

In an ideal world, their services would be turnkey solutions that sell themselves, and they would receive the entire sales value. The real world isn't like that, which means they either need to employ lots of highly commissioned salespeople and customer success agents in regional offices around the world or they sell through partners.

Their transition from selling what were turnkey solutions that did sell themselves to small-time traders towards bigger fish wasn't entirely smooth, but looking back now, the revenue record is impressive:

And remains impressive in these results:

Revenues increased 57% to £18.29 m.

Annualised Committed Monthly Recurring Revenue up 40% to £19.3 m.

Gross profit up 49% to £7.94 m.

...but their reputation for continually missing profit forecasts is undiminished:

You'll see that 2023 EPS looks uncharacteristically flat from original estimates. But Progressive (presumably not included in the above) today cut forecasts from 4.8p to 4.2p.

Plus, you can drive a Megabus between the adjusted profits & the accounting ones:

Profit before tax was £0.66m (2021: £1.25m)

Basic EPS was 1.43p (2021: 3.07p)

It’s all pretty standard:

But that SBP charge suggests, at the very least, we should be looking at fully diluted EPS. They would have made an accounting loss without government grants or fx gains.

The fundamental problem with the business remains that it is highly capital-intensive. There has been negative cash flow every year, and is forecast to be negative in both 2023 and 2024. EBITDA forecasts have actually been raised today, but depreciation and amortisation estimates have been raised more.

They generated £845k of incremental EBIT with £12,092k of incremental capex, giving a ROIncrementalIC of 7%. Surely that is below their WACC, which must be 20%+ as the capital is all equity. (Nobody invests in a risky small cap placing for a bond-like return.) This calc clearly doesn’t account for timing effects - until the recent placing, they were capital constrained, so the spend was probably late in the year. However, EBIT going forward needs to increase by at least £2.5m without further capex just to make this investment add any shareholder value at all.

Apart from capital intensity, the other problem here is that the business doesn't appear to scale. Or rather, admin costs are scaling with sales. Sometimes this is caused by hidden investment, but not here:

In a normal market, we’d say that Beeks looks overvalued by a factor of around two. You can't ignore that revenue growth and the possibility that it will continue and the business will start to scale. But in today's market, they look more than three times overvalued.

Marks Electrical (MRK.L) - Trading Update

Strong trading period, with revenue growth of 15.1% to £43.1m (HY22 £37.5m), sequentially improving against the 13.7% revenue growth in the first four months of FY23 and against a particularly challenging market back-drop

Competition from the likes of Currys has affected margins:

We retained our disciplined focus on profitable market share growth in the first half against a backdrop of heightened levels of competitor discounting and marketing. While this put pressure on H1 margins, we expect this to ease over H2 given reduced competitor discounting in recent months, our rigorous cost control and improved operating leverage during the peak trading period

This sounds suspiciously like a profits warning. Broker, Equity Development have:

2023 EPS cut from 5.3p to 4.3p.

2024 EPS cut from 6.3p to 5.7p

More surprisingly, revenue forecasts have also been cut. Equity Development retains its 150p SP target but now increases its EBITDA multiple to get there. We don't see how it is possible to conclude they are genuinely valuing them on a P/S or EV/EBITDA basis. This is just the sort of thing brokers say because they have always said it.

These forecasts largely just catch up with her the rest of the brokers had got to anyway. Hence the lack of share price reaction to this news.

Quiz (QUIZ.L) - Trading Update

This reads surprisingly well, with revenue growing again in each area:

The cash balance is healthy too:

As at 30 September 2022, the Group had total liquidity headroom of £12.7 million, being a cash balance of £9.2 million and £3.5 million of undrawn bank facilities (31 March 2022: total liquidity headroom was £6.5 million, being a cash balance net of bank borrowings of £4.4 million and £2.1 million of undrawn bank facilities).

30th September has to be a seasonal low for working capital, though. They probably ordered Christmas stock but not paid for it. Hence why they mention headroom, not just cash.

The £3.5m of bank facilities available to the Group will expire on 30 June 2023. There are no financial covenants applicable to these facilities.

Normally, these sorts of things want to have at least a year to run, but in this case, perhaps they simply won’t need them in this period. £9.2m cash vs a market cap of £14m looks good, even if it isn’t average cash balance.

An increase in GM is nice to see too:

The gross margin generated in the Period benefited from stronger demand for full price products and was ahead of comparable periods in recent years. This reflects the success to date in recovering higher product costs which, along with other costs, have been subject to inflationary pressures through the Period.

Surely they know what this is, though, so why not simply tell us? Overall, they say in line, which would be a forward P/E of 5, which seems low considering at least some of that cash is probably unencumbered. The company does have a habit of clutching defeat from the jaws of victory, however!

Thruvision Group (THRU.L) - H1 Trading Update

Thruvision now expects to break even in 2022, which looks like quite a significant beat to Brokers’ forecasts. However, this is all due to customs orders. So we wonder how sustainable this profitability is into next year. It sounds like it will be highly dependent on further orders from US customs, which have proven very lumpy.

Profit protection revenue expectations to be flat:

As we stated in our announcement of 22 September 2022, the economic situation has become more challenging for retailers since our April update. This has resulted in our Profit Protection equipment revenues for H1 being unchanged at £1.0 million (H1FY22 £1.0 million), despite the strong overall growth as described above.

Regarding their recent new customer, which we will refer to by the codename D.H.L., this is big news:

This customer has placed an initial order for a dual-camera walk-through lane for a high profile site in the UK and we now expect to sign a global supply framework agreement with them.

Walk-though was always the objective of Thruvision, but it took a while to be realised. Looking back, it is an indication of the fundamental demand that inferior solutions did so well over the last couple of years. The Group is entering a new phase in its development.

Progressive have updated forecasts, and revenue is now right back to where Leo’s were before this latest flurry of updates, albeit with a different composition. They forecast EBITDA as slightly positive and EPS as slightly negative. OCF is forecast to be negative, leaving £4.0m cash at the end of FY2023.

We think they are being somewhat pessimistic about the opportunities for miscellaneous other orders in H2 to the end of March 2023, although clearly, things are about to go quiet on the warehouse front as they batten down for Christmas. On the other hand, there is always some risk that US Customs recognised revenue could slip.

There appears to be no visibility and, therefore, no forecasts for 2024. Another large order could precipitate the need for a fund raise, but this is likely to be well received, even in the current market.

Norcros (NXR) - Trading Update

With all the issues surrounding pension funds this week, and the size of the scheme here, it is wise to start with this statement:

Notwithstanding the recent volatility in financial markets, and in particular the movement in gilt yields, the Group's UK defined benefit pension scheme obligations continue to be well managed and we expect the scheme to continue to be in an accounting surplus as at 30 September 2022.

At the last annual report, they said:

The net position relating to our UK defined benefit pension scheme (as calculated under IAS 19R) has improved to a surplus position of £19.6m at 31 March 2022 from a deficit of £18.3m at 31 March 2021, primarily as a result of an increase in the discount rate driven by market factors The Group has reached agreement with the Trustee on the 2021 triennial actuarial valuation for the UK defined benefit scheme and on a new deficit recovery plan. Deficit repair contributions have been agreed at £3.8m per annum from 1 April 2022 to March 2027 (increasing with CPI, capped at 5%, each year). Both the Group and the Trustee regard this as an appropriate outcome.

It is now becoming apparent that the signs of a serious problem with LDIs are the claims to be fully hedged against liabilities while still holding risk assets (the only way to achieve this is with gearing) and losses as equities and gilts fell in tandem earlier in the year. In Norcross's case, the pension is relatively highly exposed to risk assets, and this may flatter the reported triennial valuations, and they have LDIs.

But the evidence, in this case, is that they were taking the same sort of gamble that most here take with their SIPP, and it has paid off. The presence of LDIs in the portfolio raises the possibility that there were margin calls, but, unlike elsewhere, at worst, this is likely to have been only a temporary liquidity problem resulting in minimal or no loss of assets.

However, we would have preferred a more detailed update on the pension today, and all it really guarantees is that they have lost no more than a net £19.6m from the pension scheme in the last 6 months. They do not confirm that either the LDIs have been closed out or there is no significant gearing within them, which is where every pension scheme has been told they need to be by the end of the week - this suggests some level of denial continues in the industry.

Compared to pension fund movements, trading pales into insignificance. Nonetheless, the trading update reads well:

UK was down YoY, but was it really credible to expect covid to cause a permanent step-change in the number of bathrooms refitted? The increase over 2019 is the key figure to look at, and these are like-for-like. In addition, we have:

Following its acquisition on 31 May 2022, Grant Westfield has been integrated into the Group and continues to perform strongly in line with the Board's expectations.

Just to return to the pension for a moment: in retrospect, the deficit would have evaporated by itself just by avoiding investment in gilts and waiting for rates to normalise, but at points over the past few years, the pension had the potential to drag the company under. The only real option in this scenario is to grow the company to a point where it was big enough to fund it. Whether or not this was their reasoning, they focused on growth rather than margin targets over the last few years and took on higher levels of debt than we would normally be comfortable with. But they have executed very well (or perhaps pretty well and been lucky with South Africa). Perhaps now they can relax a little and consolidate their financial position.

If the pension deficit has truly gone and they let the debt reduce, they would deserve a far higher price/earnings multiple than 4.5x. The bear case is the same as every other DIY/tradesman stock at the moment. The question should be if they are cheap compared to Kingfisher, Wickes, Luceco etc., on an EV basis, adjusting for pension recovery payments, not just cheap vs the general market. In this case, they trade at a similar rating to most of these, so would make sense to hold as part of a sector play.

Norcross is a manufacturer, of course, but the economic exposures in terms of demand are almost identical. Kingfisher and Wickes are better businesses in an inflationary environment in that they simply pass on cost inflation on a cash basis, so should trade at a premium to a manufacturer. The geographic diversity in South Africa is a plus, but then investors can easily get geographic diversity at the portfolio level, so isn’t worth paying a premium for.

Smartspace Software (SMRT.L) - Half-year Report

When we last looked at Smartspace, following their trading update at the end of August, we thought they looked more interesting than in the past as the cash burn appeared to have moderated. However we said:

…until we see the accounts, we don’t know the working capital position. Working capital was negative in the past, which isn’t abnormal for a software company, but means that if they are growing revenue, the cash may be generated from working capital flows, not trading profits.

This week we have the detail on that cash burn improvement:

Reduction in cash consumption in the period with cash used in continuing operations amounting to £0.22m (31 July 2021: £1.33m) as trading losses reduce and a net positive movement in working capital occurs

So, could that working capital movement reverse?

· Cash balance at 31 July 2022 of £2.32 million [similar to 30th April 2022] (31 July 2021: £3.37 million) and a net cash position of £1.97 million (31 July 2021: £2.97 million)

· Cash balance at 30 September 2022 of £1.92m

So they burnt through £1.0m in 12 months and then £0.4m in 2 months. Pretty consistent with £0.2m/month burn.

The working capital position doesn’t look great even if you adjust for the £0.4m post-balance sheet normalisation:

So excluding that cash, their working capital is negative £3.3m. Being a software company, they get paid up front licensing, so assuming the business doesn’t face any downturn, they can exist with this negative WC position quite comfortably. They still have to support customers, however, and if they run this too tight, then customers will not want to install collaborative tools if there’s a chance the support will disappear. And new customers refusing to sign would then presage the downfall.

However, the increase in contract liabilities (advanced SaaS payments) is in a similar proportion to revenue as last year. There is no evidence they have been chasing longer contracts at greater discounts to preserve cash. Payables are actually below levels 6 months earlier.

On trading, ARR is up from £5.17m to £5.65m in two months, which seems very positive. So no sign of demand dropping significantly. They have always focused on ARPU (revenue per user), and this is also positive:

· Monthly Average Revenue Per User* ("ARPU") increased by 44% year on year to £84 at 31 July 2022 (31 July 2021: £59) and has advanced further to £91 at 30 September

Our priorities remain focused in continuing to deliver strong growth in ARR, growing our new international geographies and becoming cashflow breakeven towards the end of FY23, to maximise value for shareholders over the coming years.

It remains a close thing about whether they have enough cash to keep them going until then without dramatic cuts, which would slow growth. The debt is mostly a mortgage. As income is mostly received monthly, they could potentially operate with £1m of cash. So they have 4 months left at the current rate. Here are Leo’s best and worst-case predictions:

This week, they also announced Canaccord as NOMAD and sole broker. Previously Singer was their NOMAD and Canaccord joint broker. So this looks like a cost-cutting exercise rather than an obvious prelude to a fund raise. However, given that the market for placings in more speculative stocks appears to be ramping up again, they may be wise to protect the downside and take the money sooner rather than later.

Hipgnosis Songs Fund (SONG.L) - Share Repurchase Programme

Leo has highlighted before that there was a massive conflict of interest between the company and the investment manager here, leading to costs that were far too high and the overwhelming imperative to grow assets regardless of the interests of shareholders. Further that they'd probably start loading themselves with debt and eventually blow themselves up.

They are now well down this path with the following result:

This is despite the value of song assets rising over the period, not least due to them themselves chasing valuations higher.

Before we get into the detail, here's today's announcement:

…the Company has appointed Singer Capital Markets Securities Limited to manage an irrevocable share repurchase programme (the "Share Repurchase Programme") to buy back ordinary shares within certain pre-set parameters. The Share Purchase Programme will commence today and will run until 8 December 2022.

This is presumably in response to a weak share price, which demonstrates a misunderstanding of how investors value incoming generating assets and will only make what already looks like an over-geared balance sheet worse. So, how did it get to this point?

From the original Prospectus:

The Company may incur indebtedness of up to a maximum of 30 per cent. of its Operative Net Asset Value, calculated at the time of drawdown

This was apparently moderated at some point because when they increased the debt facility, they said that:

In accordance with Hipgnosis' investment policy, any borrowings by the Company will not exceed 20 per cent. of the value of the assets of the Company less its liabilities.

But, just a month later:

The Board, following discussions with major shareholders, believes that it is therefore appropriate to adopt a new borrowing policy under which the Company may incur indebtedness of up to a maximum of 30 per cent. of its Net Asset Value, which would represent an increase from the Company's current borrowing limit of 20 per cent. of its Net Asset Value.

There is always the motivation for management to grow the gross value and revenues of a company regardless of the impact on EPS / NAV because larger companies pay higher board salaries. But when they control the management, which gets a percentage of gross assets, the lure of groth becomes virtually irresistible.

A month later, on the 16 June 2021, they announced a placing. And with the scene set, things started to go wrong.

In February of this year, it transpired that Hipgnosis didn't actually control the songs they claimed to own when Neil Young withdrew his from Spotify. Although fears that other artists would follow proved unfounded, this uncovered a fundamental flaw in their business plan, and we don't know to what extent artists retain veto rights over songs that Hypnosis claim to own. Accordingly, the NAV was left highly uncertain.

Russia's invasion of Ukraine then increased risk premia, which of course, is exaggerated when you have gearing in place. The gearing we expect to be long-term debt, potentially partially securitised, and partly fixed-rate (not all, because that would potentially cause problems de-gearing if required).

However, it is not clear how much they had fixed, potentially causing some worrying times with rising interest rates. They have recovered the situation somewhat in the last few weeks with this announcement:

From 3 January 2023, the company has entered into interest rate swaps to hedge $540 million. Of this, $340 million is hedged for the duration of the RCF (until 30 September 2027) at a fixed rate of 5.67% (including debt margin); a further $200 million is hedged until 3 January 2026 at a fixed rate of 5.89% (including debt margin). The balance remains unhedged to provide flexibility in the operation of the RCF facility.

Hence why they perhaps feel they can buy back shares. However, this rate is likely higher than they have been paying in the past, and the song valuations used to calculate the Operative Net Asset are based on a DCF, which will be sensitive to discount assumptions:

Value figures are based on a discounted cash flow model, which incorporates assumptions that are subject to significant judgment by the independent valuer, the Investment Adviser and the Directors.

So the conflicts of interest, high management fees, questions over NAV and undisclosed covenant levels remain. And, of course, that yield looks much less attractive than it once did.

That’s it for a volatile week, enjoy the more calm waters of an Autumn weekend!