Small Caps Live Weekly Summary

THG LDG HFD RNO CBOX AGFX GYG BOTB PMP STCM

This week, Wayne takes a deep dive into the IPO prospectus of The Hut Group to see if recent falls are overdone. Leo was on holiday on Friday so there was no live event, so instead there’s a summary of our not-live discussions. Expect more of this next week, and maybe further into the future if it works well.

As always, readers are encouraged to join in the discussion on our discord server where the #general channel is always open for investment related ideas and discussions.

Large Caps Live Monday 8th November

The Hut Group

We particularly like a company that has a rant at the global cabal of shortsellers. You have to understand that in some CEOs’ minds shortsellers are a secret society, a bit like the Scarlet Pimpernel or perhaps the Justice League.

Anyway - let’s start at the beginning....in the IPO document, on page 10 of the pdf, we find:

(2) I cannot remember the last board of a multibillion company that I saw that had a ‘related party committee’ (page 88 of the pdf of the IPO doc)

(3) The demerger of a propco was both confusing and raised the question, why the company had a property arm? Especially as it seemed to own hotels amongst other things (page 41 of the pdf):

Details of the PropCo assets can be found on p81. Some of those properties are offices and industrial so I would argue that if they are critical to the company I would prefer that they are owned by the company. I know others like asset-light models but in my view, it is better to control your own destiny. And the relatively new lease accounting makes it even less sensical to do sales and leasebacks of property. Regarding the hotels, frankly in my view all the company needed to say was that it had a lot of staff going into and out of Manchester and came to the conclusion it was cheaper / more effective to own its own hotels.

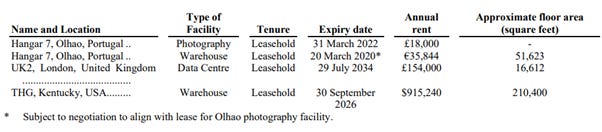

(4) Now onto something freaky.....Searching the IPO document for data centres we find that the company had 29 data centres as of 30 June 2020 (page 99 of the pdf).

BUT when we look at material property leases we find only one data centre is being leased….

I am not going to get too excited about that as it could well be that the other data centre contracts are for single racks and for short periods eg a rolling monthly contract (but I would be surprised). At a guess, I would guess that a company with a turnover of the size of THG and with 29 data centres would have several that it was paying annual rents of over £18k. The lowest rent we see in the property leases is £18,000 – and that is for a photography studio (though admittedly part of a bigger lease with the warehouse at Hangar 7).

Anyway, I am not going to get too excited but will observe that it is a tad peculiar. Note that THG Ingenuity infrastructure through the acquisition of UK2 has a hosting unit (page 64):

On page 102 we see that in May 2017 THG acquired UK2 for £58M:

And when we look at page 67 of the pdf we see:

We can see here that there was £42M of goodwill in the hosting business – so we have to presume that the UK2 acquisition anticipated substantial growth in hosting:

This is what they bought for £58m:

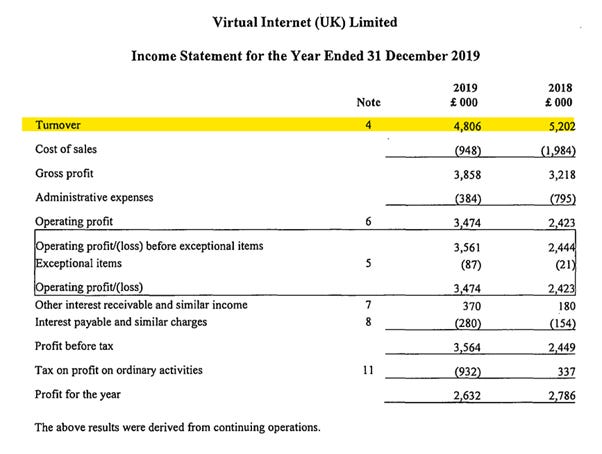

Whilst looking at the above I noticed this morning that there is a second internet hosting company controlled by THG – ‘Virtual Internet’. Jumping to their accounts in Companies’ House we see:

According to companies house, Virtual Internet (UK) Limited is controlled by Virtual Internet holdings Ltd, and UK-2 Limited controls Virtual Internet Holdings Ltd so it seems strange that the consolidated holding company has lower revenue than its subsidiary. Perhaps there is intercompany revenue and charges. The 2020 accounts for UK-2 and VI are subsumed in the parent group accounts so we have limited insight on this more recently.

(5) The carve-out of the PropCo has raised eyebrows in the city , according to the Guardian.

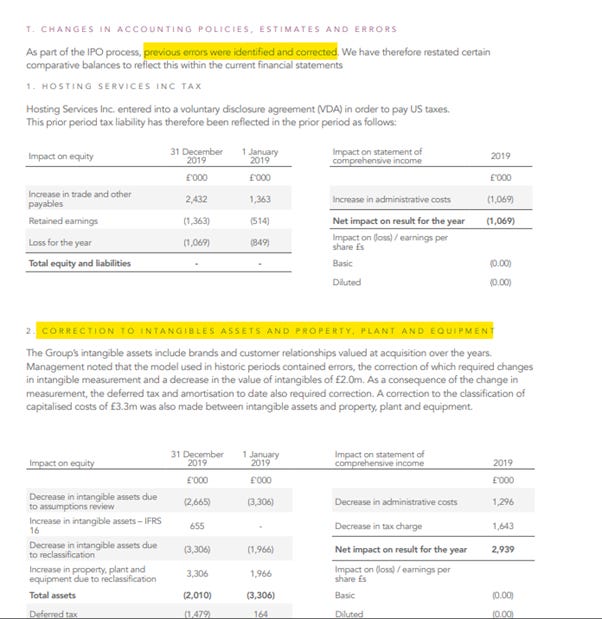

(6) The board has a number of accountants on it (page 84 of prospectus). We have the CEO, the CFO and the SID all being qualified accountants. So why do we find this in the accounts in 2020 (page 130 of 2020 AR):

There appear to have been so many corrections required, there is a 2-page summary table required:

(7) This is an incredibly complicated company to understand, not least since it has a wide variety of businesses and has done a number of acquisitions in its time; including more post IPO. The 2020 Annual report refers to the following post year-end:

Though I am not against acquisitions it can make it really complicated to work out what the heck is going on. It is not entirely obvious to me how a tree planting company or a film distributor fits in with the master plan.

Given all this, why take the risk? Despite the recent share price falls there is not a long track record of Free Cash Flow to anchor a valuation. This may be because cash has been re-invested into growth, but as an outsider, it is pretty hard to tell.

Small Caps Live Wednesday 10th November

Logistics Development Group (LDG.L) - Receipt of further cash payment

Logistics Development Group is an interesting investment proposition and one we hadn’t come across before, so thanks to @RM786 for highlighting it.

This week’s announcement is relatively straightforward:

Logistics Development Group plc, the AIM investing company, announces that it has received an additional payment of £2.2 million

This is dead easy to analyse since they say:

As at the date of this announcement, LDG holds no material investment assets, is debt free and has an available cash balance of approximately £134.5 million (approximately 19.12 pence per share).

So this is effectively a cash shell, managed by DBAY Advisors. The attraction is that this can be bought for c13.8p so a 28% discount to cash on the balance sheet. If the plan was to return cash to shareholders then you can imagine that this discount would be much narrower. Reflecting just the time value of money and the c£1m/year of admin expenses from running the company.

There are two risks that the market is pricing. The first is that DBAY overpays for an acquisition. The second is that they don’t find a suitable acquisition and end up delisted. DBAY are pretty smart operators, hold c.27% of the equity and have a long history of takeovers in the UK markets, and rarely overpay. So, if you are going to partner with anyone in this sort of game, they would be high up the list.

Other holders are Stobart, well-known investor Richard Griffiths who has had holdings in DBAY purchases before such as Telit, and, it appears, Future PLC via their Miura Holdings subsidiary. We would expect these to be supportive of what DBAY are trying to do.

Personally, we would love to control £134m of capital in such a vehicle. You could start with a c.20% premium offer for ScS, then gear it up slightly to return the whole investment as cash, and then do likewise to Zytronic and a few other cash-rich companies. Pretty soon you’d have a large diversified mini-conglomerate of cash-generative companies, mostly acquired using their own cash plus a bit of gearing at the subsidiary level.

Although the presence of such cheap shares in the market today is perhaps an argument to both hold LDG, and not hold. Why take the risk on an unknown acquisition when you can buy stocks where the value proposition is so compelling, without paying the takeover premium?

Halfords (HFD.L) - H1 Results

Although technically a mid-cap, we think this company is worth following. This week we got H1 results.

As you would expect, the six months to 1st October 2021 are strong, with revenue up 19.2% versus 2019, including 8.8% in cycling, though note that these are two year, not annualised growth rates. Exceptional growth in specific areas such as Autocentres, Group Services, online and B2B suggest these are from a low base and may have a considerable distance to run while making up a greater proportion of the whole.

As ever, it is the current trading and outlook we are most interested in:

Inflation, labour shortages and supply disruption will continue to impact the business. We believe demand for our products and services will remain healthy and that we will be able to manage and mitigate the operational challenges through H2 and into FY23. Our strong first half performance gives us the confidence to continue to invest in price in Retail Motoring, where early volume uplifts are encouraging, and in our Group transformation, investing for the longer term.

Taking the above into account, we are upgrading our FY22 full year profit before tax range to £80m - £90m. That compares to a PBT of "above £75m" reiterated in September.

We do not expect the extreme levels of inflation seen on freight spot markets to be sustained, and we expect supply and demand of labour markets to stabilise, but certain inflationary aspects of FY23 are already known, including National Insurance, National Minimum Wage and energy costs. We are confident that our established efficiency workstreams and hedging polices will, in part, mitigate some of these costs. We also see some positive aspects looking forward; foreign exchange and rental markets are more favourable, cycling supply should stabilise, and our initiatives from FY22 will begin to build momentum, contributing further to revenue growth.

Note they are saying they don’t expect the inflation to be maintained, which is very different from saying they don’t expect current prices to be maintained. Without knowing how careful the company are with words or being on the analysts call to clarify, we would assume that they actually mean current prices - nobody is expecting 500% pa inflation to be sustained!

Halfords looks a potentially interesting investment due to the new growth areas not apparently dependent on covid, and well worth further research. For example, on their B2B side - it clearly doesn't take many years of 33% pa growth for a segment that was 18% of the total to become a significant growth driver of the whole business. And the P/E ratio was only 8.9x yesterday and it is up 15% today.

Renold (RNO.L) – Interim Results

Interim Results from this industrial chains manufacturer read very well:

100% increase in EPS is not inconsiderable, even if it does come off a covid-depressed period. The adjustments here seem reasonable too, being currency and £1.7m of US Payroll Protection Program (PPP) loan forgiveness offset by £0.5m of dilapidation charges relating to closed sites. And the outlook seems positive too:

Group order intake in the period £113.0m, up 48.8% YoY as reported (54.9% at constant exchange rates).

Orderbook at 30 September 2021, £72.1m, is a record high for the Group (30 September 2020: £46.5m).

A brief mention of inflationary pressures being, perhaps, the only negative point:

With a record order book at the period end, coupled with the strategic initiatives previously implemented, we approach the second half with confidence, but cognisant of the very volatile and inflationary world we operate in.```

Net debt is decreasing too:

Cash generation in the first half was strong, with net debt reducing by £4.5m from the position at 31 March 2021, to £13.9m.

The current ratio is 1.8 and this is 0.6x adjusted EBITDA so seems perfectly reasonable. In the past, there seems to have been a limited amount of seasonality in their results which means that, with first-half EPS of 2.3p, the stockopedia consensus of 2.7p for the full year looks like it should be easily beaten.

We’d noticed that Renold had appointed finnCap as joint broker recently. Since Renold don’t have an immediate need to raise cash and their existing broker was the larger Peel Hunt, this seemed a strange move. However, it becomes clear today why they added a joint broker, since finnCap has resumed research coverage

It is clear that the quality of the finnCap research, and their willingness to make it available to all, has won them a client here. That Renold appears to prefer finnCap research to their existing coverage from Peel Hunt does seem like a vote of confidence. This is one of the reasons that finnCap can grow and take market share in the broker space and bodes well for the long term growth prospects for them.

This is what finnCap have forecast:

So 3.3p for FY22 which still looks like it could be beaten. This means Renold is on a forward P/E of just 10 which does seem good value for a company rapidly recovering and growing EPS.

There is an elephant in the room, however – the pension deficit. And it is an elephant. It comes in at a massive £100.3m deficit, or £77.8m net of the deferred tax asset. In comparison, the current market cap of Renold is £75m. So, a simplistic analysis would say that you have to double that market cap to calculate a realistic rating. Suddenly a P/E of 20 doesn't sound great value.

There are two ways of adjusting for pension deficits - the first is as above, on the asset side. The second is on the income side - adjusting the EPS for the cash pension recovery payments.

Over the last few years, they have made about £4.5m payments per year as cash pension recovery payments. They have a triennial valuation due next year but since the deficit is similar I expect the payments to be similar, or even higher if the company is in a better position to afford them. This is perhaps why finnCap are predicting no dividend to be paid in the next few years. This may be a covenant issue, but may just be because they won't be able to afford them.

2022E adjusted earnings are £7.5m so almost 2/3rds of that is going on deficit recovery payments. The proportion reduces as they expect them to grow adjusted earnings and be about half of the earnings in 2024. But still, the outcome is similar to the asset level analysis: you should halve the EPS and double the rating when assessing this company. And, again, this doesn't make it look particularly cheap.

There is a trend amongst investors to ignore pension deficits. Perhaps this is reflecting hopes of rate rises, or perhaps it is simply the increase in investors who don’t understand such matters. So with Renold and similarly large pension-deficited companies such as Mpac, there may be a "greater fool" strategy to play, where unsophisticated investors will bid this up on the headline numbers and hence you should buy on that basis. However, with the pension deficits often preventing any takeover offers, significant cash flow taken by recovery payments, and no dividend forecast for many years from Renold, this is a risky strategy.

Cakebox (CBOX.L) - H1 Results

Cakebox is a retail franchise of egg-free cream cake shops, founded in 2008 and floated in June 2018. They run a centralised baking model with cakes assembled and finished in-store, allowing CakeBox to retain more of the margins while lowering the barriers to entry for franchisees. (Just a reminder that the Admission Document is essential reading for AIM companies and can be found here.)

Many newly listed companies experience a stumble within the first 18 months, but Cakebox has done very well, at least in investors minds, not even dipping below the listing price of 108p in the depths of covid pessimism. More recently it has gone from strength to strength, breaching 400p.

Looking at the operational performance there was some weakness in H1 of 2020, and it is unclear whether they would have made the numbers to end-March 2020 without covid, but they didn’t miss by far in any case. The upgrades started in June of this year when the annual results were published.

On Monday they published their H1 results. The first thing that struck us was they are comparing with the year before which included most of the first lockdown. This is highly disingenuous and a big red flag.

However, to be fair to them, they have grown the estate considerably since 2019 and so that would hardly have been a fair comparison either, also they do also give some like for like figures for the last four months. With some reliance on badly-hit shopping centres, it is unclear whether these are quite fair either, but practically speaking they’re the best we’re going to get. Both revenue and profitability are up 50% on this basis.

Strong cash flow is reflected in strong dividend growth. Dividends might now be 7.5p for the year, a yield of well over 7% on the 2018 IPO price.

The outlook is strong - franchisee LFL sales growth of 14.4% is given for October, and although the last week in October 2020 may have been affected by reduced footfall over covid concerns, this suggests the stores are working well for the franchisees. Visibility is excellent due to the intrinsic nature of the business model and deposits received for new openings.

There are a significant number of related party transactions which appear to be to franchises owned by directors and their families. Earlier on in the company’s development, there was a risk that these together with those run by extended family and friends could make up a significant proportion of revenue. However they are now of a scale that I am not worried about this, and in fact, it is a positive that they will receive immediate feedback from a franchisee's perspective through these relationships.

So this is a real AIM success story. The question is: What is this growth worth? Clearly, a rating of 26x earnings for a smallcap in the current market means much of the value is dependent on future growth. This depends on a fundamental analysis of their business, something which is very difficult to get right. We would highlight questions like:

Size of the addressable market. How many stores can the model support? Will franchisees get overexcited and overreach resulting in a bust, will they hit a wall, or will growth gradually slow? We understand their target is 250 vs 170 currently, but the temptation will undoubtedly be to push that higher if they can.

Natural attrition of franchisees. As they get larger this will provide an increasing downwards pressure.

Labour market. High wages not only reduce profits for franchisees, but a strong labour market reduces the supply of franchisees, stereotypically people who have lost their jobs with large redundancy cheques.

Competitors - old, new and emerging

So, while not quite Leo’s usual style of investment, he is very tempted to have a more detailed look. For those without time to do more research, here’s a comprehensive-looking article Leo found during his research.

Argentex (AGFX.L) - Interim Results

This had been weak recently as a couple of high-profile investors bailed, and presumably their followers were keen to crystalise their losses. The reason given was the likelihood of a profits warning. The interim results read well though:

· Gross Foreign Exchange ("FX") Turnover: £8.3bn (HY 21: £5.0bn) - up 67%

· Revenue: £15.7m (HY 21: £11.8m) - up 33%

· Underlying Operating Profit: £4.7m (HY 21: £3.7m)* - up 27%

· Underlying Operating Profit Margin: 29.9% (HY 21: 31.4%)

· Profit after tax: £3.3m (HY 21: £2.7m) - up 22%

· Highly cash generative, with 79% of revenue converting to cash in 3 months or less

· Earnings per share: 3.0p (basic); 3.2p (underlying) (HY 21: 2.4p (basic); 2.5p (underlying))

· Interim dividend: 0.75p per share

One of the big questions was around why the revenue was only up 33% when the gross FX was up 67%. On the surface this looks like large margin erosion. However, the answer was that clients were choosing to close out swaps early hence generating more volume but little extra revenue.

So what about the profits warning? Well they didn't directly address market expectations in the results, or in the subsequent call in IMC. The house broker did trim forecasts slightly post these results:

Which suggests management weren't entirely comfortable with these. In the InvestorMeetCompany presentation management came across as very knowledgeable and professional (not something you can always guarantee in the FX space!). The did dodge a couple of Mark’s more difficult questions which left a slightly poor taste in the mouth.

They are on a quarter of the rating of competitor Alpha FX, though, and with higher ROCE. On the call they said that Alpha were a good company and where they expect to be in a couple of years time. That would be an 8-9 bagger if they received a similar rating. Alpha FX are considered more of a “fintech company” hence the high rating. And we believe former co-CEO, Carl Jani, was very much the "not a fintech company" proponent, whereas from the comments in the IMC presentation then going forward Argentex do see the value in having better tech systems for some customers, so we may see more movement into this space, and hence a higher rating.

They said their competitors are still the high street banks and they don't have to work too hard to be cheaper and provide a better service, so there is plenty more market share to go for. Fundamentally this just seems too cheap for the growth potential.

Small Caps Not Live

GYG (GYG.L) - Large Contract

The Board also reiterates that, after further thorough review, it is confident that the Group can meet its working capital requirements and repay its borrowings as they fall due providing that the Nobiskrug situation is resolved before 31 December 2021, which the Board fully expects. On this basis, the Board does not believe that the Company will need to seek additional funding from shareholders in the foreseeable future to maintain operations or to meet its obligations.

Previous statement:

The administration at Nobiskrug had a material, detrimental short term effect on the Group´s working capital position. Not only did the Group not receive payment for the outstanding amounts due, €2.8 million (net of VAT), but there was also a subsequent delay of revenue that had been expected while the three Nobiskrug projects remained suspended. This exacerbated the normal seasonal trading profile of the business.

This was covered by a loan from a shareholder who had made a takeover approach for the company. This loan matures on 31st December 2021. That shareholder then pulled out of the takeover, reportedly saying "that now is not the appropriate time to progress a potential offer". Offer was at 92.5p, which was clearly too high given subsequent issues. Order book is strong and with the share price below 50p, the P/E is shown as 6.3x on Stockopedia. A special situation for people who like that sort of thing.

Best of the Best (BOTB.L) - Trading update

Trading now appears stabilised and inline. House broker finnCap has 53.3p EPS for 2022 and 64.1p for 2023 for a forward P/E of around 10.

The Board remains confident about the prospects for the business, both in the second half of the financial year and beyond.

This seems to bode well for that being met. On the 13th August they have cash on the day before as "in excess of £6m". That is before the immaterial final dividend, but after the special £4.7m dividend. Surely cash is well in excess of £7m at this point?

Very interesting investor psychology on twitter. Many people complaining they didn't give figures, but BOTB never have given figures, the same as the majority of companies. The finnCap note is free to read and so guidance isn't exactly a secret or hard to find. In terms of detail, it has everything that you might want, or at least I can't see anything missing and nobody had actually said what is missing. This perhaps reflects the number of people who were taken in by the hype and badly burnt by the subsequent fall.

They do say profits warnings always come in threes:

This level of hate is attractive to the contrarian investor. However, it does mean investors can’t rely on a multiple re-rating to drive the returns since it will take a few years for investors to get over the recent disappointment. Which means you are reliant on them hitting next year’s numbers to generate your returns.

And here there does seem some uncertainty. This is a company that has faced increasing competition from well-financed rivals and significant headwinds from normalisation of lockdown trends. Those who feel those trends are reversed and the company can return to a more stable growth path will find value here, but it does come with risks attached, given the company’s recent past.

Portmerion (PMP.L) - Trading Update

We note the widespread press in recent weeks on energy intensive industries. We have made significant progress in recent years in reducing our energy usage and will continue to invest in 'green' initiatives as a core part of our strategy. As a central part of our business, our ceramics factory in Stoke-on-Trent buys energy under long term contracts. In the first half of 2021 we extended those contracts until early 2024. As a result, we do not expect to be materially impacted by the latest rising energy prices.

It is not immediately clear how these contracts have been accounted for. They have not appeared in annual reports in the past, despite apparently it being their longstanding policy to buy ahead. Although these contracts have gone "right" so far, it is very easy for such contracts to go "wrong". For example, if a drop in demand or increase in competition led them to reduce production then they would have to pay for the difference between the energy they bought ahead and the spot price.

When investors aren't too busy complaining about IFRS 16 or companies not including guidance figures in RNS statements, a favourite moan is about ESG reporting making annual reports too long. For example, for 2020 Portmerion spent an entire two pages talking about energy.But actually this has turned out to be quite useful:

So we know pretty much exactly how much energy they must have hedged, and we can take a good guess at the price and the profit. Leo estimates that the remaining forward gas contracts cost them £1.4m and today have a fair value of £2.7m. This compares with a market cap of £96m and a forecast adjusted PBT of £10.0m for FY 2022 and £11.8m for FY 2022.

The share price has not reacted to the sales ahead announcement and confirmation that energy is largely on fixed price contracts. But then it is on 18x forward earnings so is pushing its normal valuation range anyway, and largely has a return to pre-pandemic trading already priced in.

Leo’s analysis of H1/H2 seasonaility leds him to believe that Portmerion were being conservative, and previously estimated revenue could be up to £103m. But recently they have clearly run up against headwinds. Although, he still expects the resulting revenue to be closer to by £103m than their previous £90m guidance. Portmerion have lots of tailwinds behind them and revenue should continue to beat over the next few years.

On the other hand, EPS forecasts always assumed greater margin improvements than Leo could evidence, and still do going forward. There were no EPS upgrades today due to cost headwinds, and hence, we would take the 66.9p EPS forecast for FY 2023 with a pinch of salt. If they beat on 2022 but miss on 2023 the market may not react kindly, given the heavy reliance on earnings growth beyond 2022 to get the bull case to stack up.

Steppe Cement (STCM.L) - Dividend Statement

This is a business operating in a very high risk location, but where the attraction has been the payment of very generous dividends from cash flow. The price had been weak recently as more astute investors realised that they would normally have declared an interim dividend by now and, presumably, became worried by the lack of declaration. Today we find out why:

After careful consideration of the changes in certain government regulations in 2021 in Kazakhstan and having taken independent accounting advice, the Board has been made aware that an Interim Dividend may attract a 15% Withholding Tax when paid to a foreign holding company.

The position of the Kazakhstan Tax Department is that dividends can only be declared from post-tax profit once the accounts are audited and the Annual General Meeting has approved the audited accounts.

The Board is of the opinion that paying the 15% Withholding Tax and hoping to recover it in the summer represents a significant risk and has therefore decided to pay the Dividend for 2021 only after the Annual General Meeting.

It certainly makes sense to delay payment if it avoids a 15% tax. We would guess that shareholders are already aware of the significant regulatory risk of their operating location, or it wouldn't be on a 13% prospective dividend yield and hence this announcement is much more likely to re-assure than worry investors.

As a reader point out, however, that there is a possible read across to other companies based in Khazakhstan, such as Central Asia Minerals, who normally pay both an interim and final dividend.

That’s it for thisweek, have a great weekend!