Small Caps Live Weekly Summary

Macro STAF BSE NCYT SOM CMCX IGR MGP PGH SCE

A calmer week this week for news, but small cap markets were anything but calm earlier in the week. On Monday, concern over the situation in Ukraine plus inflation fears led to some big sell-offs in more popular small caps. However, Tuesday and Wednesday, saw a bounce back, presumably as everyone who panic-sold at the bottom on Monday bought back at higher levels. The latter part of the week saw further weakness. Investors can often be their own worst enemies when it comes to volatile markets. While weak markets can sometimes give us the impetus to evaluate non-core positions, most of the time, long-term investors are better off simply ignoring such market gyrations. Unless one has significant capital to deploy, of course.

We will discuss all this, plus more, on our first live video chat of 2022, at 9:30am Monday 31st on the discord server.

Macro Thoughts from WayneJ

Following on from last week’s discussion about how January tends to lead the markets for the year, my thoughts are:

During Covid we had an initial massive slow down in the economy due to:

people went home and hunkered down

businesses anticipated a period of slow / negative growth and so cancelled orders etc

The result of the above was a slow down in the economy AND as a result a slow down in the velocity of money

Then the government and the central bank (in many countries) acted with the same-ish recipe:

financial support of business by the government ie FISCAL support

increased government expenditure eg on healthcare ie FISCAL expenditure

increase government spending or reduced taxed eg cuts in VAT in the UK and 'eat out to help out' ie FISCAL stimulus

And at the same time we had central banks buying bonds (corporate or government) ie MONETARY support and cutting interest rates ie MONETARY stimulus. BUT what no one really countenanced was:

that with Zoom / Teams etc a lot of office work / productivity could continue i.e. office work did not collapse as much as feared

a combination of existing retail online platforms (eg Amazon) and rapid transition of other companies to online led to greater retail (and arguably commercial) recovery than was anticipated

a big sector of the economy is building / construction / home furnishing etc - spending more time at home led to more demand for everything from sofas, home furnishings, TVs, playstations etc to more space so extensions and a massive cycle of moving to bigger houses / out into the country / new builds to fill demand etc

So the relative collapse of the economy and the collapse of velocity was not as great as expected. But some of the spend shifted eg away from services (that train ticket for the commuter) into consumer products (that new iPhone) leading to massive demand for manufactured products from China / Asia etc. Combine that with an initial cancellation of orders and Covid outbreaks in Asian factories and we have the position we have now. So what next:

The market expectation is that the Fed will normalise by stop bond buying and increase rates i.e. by 4 x 0.25% this year.

Yet at the same time - in some countries e.g. the UK - we have also a normalisation of of VAT, a reduction of fiscal support and a reduction of govt stimulus. AND to complicate matters a hike in fuel prices plus a return to work (so more spend on commuting) means that household disposable income will fall.

BUT I just can't see how all the above items listed above can be reversed in one go this year. And in this context it is worth remembering that Covid is not under control in many countries, the UK is ahead of many in vaccination and some countries still have varying degrees of lockdown. In addition the traditional reason to raise rates was inflation. But there are various types of inflation ie demand driven or supply driven ('supply shock').

I would suggest that in the current case we had:

Early in Covid a demand shock as companies cancelled orders. Then a demand shock as consumers ordered via the internet and a supply shock as companies in Asia had staff off ill. And the same happened with oil and gas companies ie the 'rig count' in the shale patch collapsed. Plus ESG concerns deprived the shale / incremental sources of O&G of capital. Indeed, I am going to suggest this could be the first 'ESG induced recession' in history

Over the course of the next 6 - 18 months - as people become more confident and things normalise more people will be able to work (eg no more home schooling) so work force participation will increase - which will be a natural offset to the current low unemployment rates. A combination of high oil prices and Ukrainian / Russian concerns is also going to drive the US and others to do arm twisting to get extra O&G investment in 'safe' regions.

The big question for investors in tech is whether Covid / the last 24 months led to a step change in demand so we can project trajectories forward OR merely brought a lot of demand forward? And of course there was also 'one off' type demand eg if Edna the office PA always worked 9-5 from her desk in the office. Then she probably suddenly got a laptop for home at the start of the crisis from the company. She probably is not going to ever replace the laptop at home. And she uses a very limited number of apps (word, outlook, and a webbrowser) - so when she goes back to the office she will start using her existing desktop again.

So putting all the above together I would suggest that we have massive rotation from growth to 'experiences' ie travel / leisure / restaurants - but a bit like my discussion re tech there will be overextrapolation.

On top of all the above I would suggest that a lot of the 'new money' inflows into the US market were driven by stimulus / support checks (=cheques).

I have argued for a long time that the chairman of the PBOC ought to be on the board of the FOMC as long as the dollar and the Chinese currency are intimately linked. I have said it a bit in jest to make the point that the PBOC also influences global money supply. And I think that the relaxation by the PBOC and various concerns expressed by the Chinese re the Fed tightening are like the proverbial canary.

In financial markets you should always first look for canaries in the obscure areas ie SPACs, Emerging markets and Chinese property currently.

Small Caps

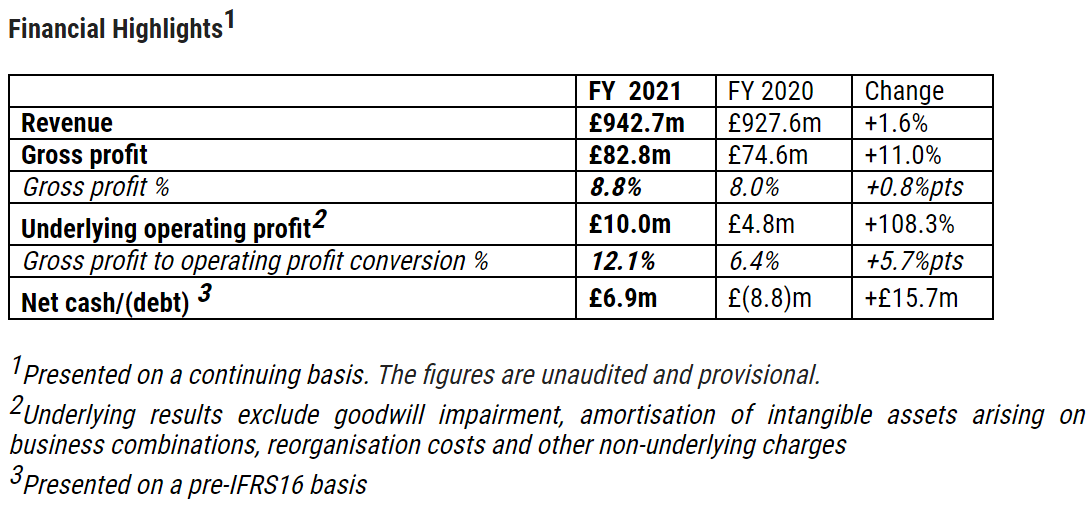

Staffline (STAF.L) - Trading Update

Here is the main summary:

Revenue is flat and, in fact, a miss against the single broker forecast of £954m from Liberum. But they are still recovering, and one of the things they are specifically recovering from is previous management's attempts to get them to £1bn turnover at all costs (and in order to claim their bonuses). Current management are fully aware that turnover is vanity and profit is sanity. And so it is good to see that underlying profit is up 108%. Management say this is 11% above market expectations.

In general, investors would be right to be sceptical about "underlying operating profit" measures, aka "profit excluding bad stuff". EPS is what matters to us. And you never know whether the company's metric is on the same basis as the forecasts and therefore whether they have actually beaten or missed. But in this case, there has been so much change and reorganisation and historical stuff that only adjusted figures make sense.

This part of the statement reads well:

Staffline's balance sheet was significantly strengthened during the year with the Group expected to report an increase in pre-IFRS16 net cash of £15.7m to £6.9m at 31 December 2021 (2020: net debt of £(8.8)m), despite repaying the majority (£40.7m) of its Deferred VAT Relief, with the remaining balance of £5.8m to be repaid on 31 January 2022.

Until you reach this bit and realise that all of the cash flow, and more, is due to an equity raise & timing benefits:

This substantial improvement was achieved through a successful equity raise of £46.4m (net of costs), and includes c. £10m of timing benefits, which are expected to unwind, alongside further improvements in trading cash flow and cash collections.

However, if you do the sums, the underlying cash flow in H2 isn’t bad:

On to the future;

All three of the Group's divisions delivered a strong performance in the year, as Staffline successfully leveraged its market leading positions in each segment to mitigate operational headwinds presented by the Covid-19 pandemic and widely publicised labour shortages.

All competent recruiters with sensible broker guidance have been doing very well, so this can hardly be surprising. Of their three divisions both Recruitment GB and Recruitment Ireland are performing well, generating the vast majority of the group profit. despite being market leaders Recruitment GB has only about 10% market share so this has plenty of scope to expand. However, PeoplePlus is again causing problems:

An additional impact in the Skills division has been the discovery of incomplete records relating to 2019, which will require the repayment of c. £2m of revenue. Based on its legacy nature, this has been adjusted through reserves. Of the c. £2m, £0.8m has already been repaid in 2021, with the balance due for repayment in 2022.

Overall, we’d prefer it if they just dumped this division in its entirety. Here’s the outlook:

The Group has delivered an excellent performance in 2021, exceeding expectations in both profitability and cashflows, with upgrades to market expectations during 2021 against a backdrop of continued macroeconomic headwinds.

This momentum is expected to continue into 2022, supported by a strong new business pipeline, a lower overhead cost base and the expected post-Covid recovery of historically strong Staffline recruitment sectors, such as automotive, manufacturing, aerospace and travel. The Board remains confident in the growth prospects for the Group in the medium-to-long-term.

Zeus have initiated coverage here.

We believe the shares are undervalued and see an intrinsic value per share of 99p based on the current profile of the business, which does not include future potential M&A that could enhance this valuation. We see good reasons to suggest strong trading momentum will continue through 2022 and beyond.

Interesting that they also see M&A as an option despite the company statement being silent or even implicitly downplaying that as an option. They also mention share buybacks as a possibility. This seems a bit off considering they only raised capital from the market in May.

Zeus's 99p target is based on "DCF, risk-adjusted blue-sky earnings, SOTP" [sum of the parts]. They have based this on a WACC with a cost of equity of 9%. So, very explicitly, if you demand more than a 9% return on equity then according to Zeus, Staffline is not worth 99p a share. But, this is on very low growth rate assumptions. At the revenue level, they have just 5.3% YoY for FY2023, fading down to 2% in the long term. They also expect gross margin to start tailing off leading to minimal profit growth. In their sum-of-parts calculation, PeoplePlus looks way overvalued compared to Recruitment GB.

So, to conclude, after having stabilised financially, Staffline has demonstrated the ability to produce significant positive cash flow and to grow margins with only a minor hit to revenue. The update also represented a significant beat at the EPS level (4.8p to 5.33p) and significant upgrades for future years. Annualised dilution from the deleveraging fundraise and perhaps exhaustion of tax losses will result in EPS falling in FY 2022 before the trends seen in PBT result in a recent record EPS in FY 2023. PeoplePlus may do well in the short term but is sure to cause more problems in the future and needs to be broken out in any modelling. As the rating recovers, cash flow accumulates and the banks become more comfortable, there is every prospect of them resuming something approaching their previous acquisition-led growth pattern.

Base Resources - Quarterly Activities Report

The volume of ore mined was down slightly for the December Quarter but the increased grade meant that production of Heavy Mineral Sands increased vs the previous quarter. Sales were significantly ahead of the previous quarter due to a catch up of Ilmenite shipments that were slightly delayed into this quarter. These were in line with my estimates and the middle of the production guidance for the full year:

Kwale Operations production guidance for the 2022 financial year (FY22) remains at:

Rutile - 73,000 to 83,000 tonnes.

Ilmenite - 310,000 to 340,000 tonnes.

Zircon - 24,000 to 28,000 tonnes.

Although this is largely an operations report, Base give enough details on costs and sales to make a very good guess as to the financial results for the quarter.

Sales revenue per tonne declined but this was due to the product mix, with the less valuable per tonne Ilmenite making up a large proportion of the sales due to the catch-up. These were slightly below Mark’s estimates, partly due to the high volume of Ilmenite but also of the delayed rutile shipment, so this effect will reverse in Q3. The operating costs per tonne were reduced due to the increased production volume, although the higher production increased the overall cash operating costs to $18.1m for the quarter.

Overall this means that the quarter should have generated around $23m net profit from Kwale and around $37m of Free Cash Flow before movements in working capital. Net cash only increased slightly during the quarter, however, due to the timing of tax payments to the Kenyan government and working capital build due to the increased shipments during the quarter. Given the large cash balance, they are likely to fairly relaxed about any working capital flows but is worth keeping an eye on.

Looking forward, the supply dynamics continue to be supportive of HMS pricing:

Despite uncertainties in China relating to power cuts, environmental controls and COVID management policies, the TiO2 pigment industry and the main zircon-user sectors (including ceramics) in China remained strong through the December quarter. End user sectors for the Company’s products in all other markets continued to strengthen through the quarter. Further price increases for TiO2 pigment have been announced globally for early 2022.

Rutile is the standout, where they say:

Rutile prices increased through the quarter and substantial price increases have been secured for the March quarter.

This bodes well for the rest of the year. With this pricing strength, Mark is estimating free cash flow of around $125m for 2022 from Kwale before any tax payments, central costs or inventory build. It is frustrating to see that no progress has yet been made on Toliara, but this does free up cash flow to pay dividends in the meantime. $60m was paid out last year for a 22% yield on the current price. The current production profile and pricing mean that this level of payout would be very affordable again. However, it may be wiser to hold back resources for the eventual expansion of operations. If possible, Mark would prefer them to keep enough cash to go it alone on Toliara rather than agree to a JV since the economics there are so compelling. Although, a JV may have other benefits such as lowering the risk profile or long-term off-take agreements that make it more favourable.

Novacyt (NYCT.L) - Trading Update

Looking at the chart here you could be forgiven thinking that that camel has stopped vomiting and has keeled over dead, or perhaps it is simply a sleeping dragon:

FY2021 EBITDA before exceptional items is expected to be above £36.0m (FY2020: £176.1m), i.e. a margin greater than 37%, in line with management guidance of approximately 40%.

We have no idea how sustainable this EBITDA is going forward, so what we really want to know is how much cash they have, and what they intend to do with it.

The Company's cash position at 31 December 2021 was £101.8m, compared to £91.8m at 31 December 2020 and £77.2m at 30 June 2021

That's £1.44 a share. But we also know they are owed money from the disputed contract with the DHSC. At H1 they said:

Payment for the £49.0m invoiced remains outstanding

Looking at the detail, there doesn't seem to be any question of having to repay anything to the DHSC, so there is no negative cash impact. In fact, at H1 they said:

Value Added Tax balance of £8.3m at 30 June 2021 relates to VAT paid in the UK on sales invoices in dispute with the DHSC. As these sales have not been recognised in accordance with IFRS 15, the revenue, trade receivable and VAT element of the transactions have been reversed, resulting in a VAT debtor balance…

In January 2021, the Company paid £19.5m UK corporation tax for what it believed to be its outstanding liability, this has subsequently changed primarily driven by the late impact the DHSC dispute had on the 2020 results. In Q1 2021, the Group made the first quarterly instalment of its projected 2021 UK corporation tax liability, paying £10.0m to HMRC prior to the impact of the DHSC dispute being formalised. This £10.0m resides on account with HMRC and the Group will look to see if this can be refunded in the near future as, based on the 2021 interim results, no corporation tax was due for H1 2021.

So if they fail to get the £49m then they should get £18.3m back in VAT and tax. So that is a minimum of £1.76/share vs a share price around £1.88 following this trading update.

Of course, a share price close to or even less than cash isn’t unusual if a company is burning cash. However, in the short term, they are probably cash-flow positive, thanks to:

o Private laboratory revenues increased by 98% year-on-year from £28.3m to £55.9m, which includes £10.5m of revenue from NGOs

o Private testing accounted for 58% of FY2021 revenue at £55.9m, compared to 10% in FY2020 at £28.2m

Growth of new markets for private testing, including travel, sport, film, media, and workplace settings

There are a few problems, however. The first is they don’t seem to have learnt their lesson:

In the UK, additional uncertainty around product availability has been caused by the implementation of the UK Health Security Agency's Medical Devices (Coronavirus Test Device Approvals) (Amendment) Regulations 2021 ("CTDA"), as previously announced. Whilst Novacyt has so far been successful in receiving approval for one product and having two added to the temporary protocol, eight products remain under review.

The second is that the UK has announced an end to all travel testing and others are likely to follow suit. And finally, there seems to be little commitment to returning any of the cash, and an increasing focus on spending it:

Paul Oladimeji has assumed the newly created position of Group Head of Research and Development (R&D), effective from 1 January 2022. Paul is a specialist in nucleic-acid amplification technologies and a neuroscientist by training.

In such cases, a discount to cash is fully warranted and Novacyt is more Dead Camel than Resting Dragon.

Somero (SOM.L) - Trading Update

When discussing Somero on our discord server last week, we felt that, despite the last trading update coming close to the end of the financial year, there may be a further upgrade to come here. This was prescient since this week we get the following statement:

The Board expects the Company to report revenue of approximately US $133.0m (+50% v 2020) ahead of previous guidance of US$ 130.0m, annual adjusted EBITDA of approximately US$ 48.0m (+83% v 2020) ahead of previous guidance of US$ 45.0m, and ending cash of approximately US$ 42.0m (+18% v 2020) ahead of previous guidance of US$ 39.0m.

That the estimates are all up by c$3m means that sales have slightly beaten expectations, costs have come in slightly lower than expected and the extra sales haven’t required any exceptional working capital build. So all good news. Since Somero pays a proportion of cash above a certain level as a special dividend, the cash build should support a further dividend increase slightly above the increase in EBITDA.

Overall, it means that admin costs are probably up by some $2m in H2 vs 21H1 and some $3.4m above 20H2. However, we knew they were adding customer support headcount as the business has scaled significantly. In addition, they have launched three new products recently:

Somero describes them as “revolutionary”, which we feel may be a bit of a stretch. They do say , however:

In 2021, the Company completed development of the S-PS50, a large boomed-screed that provides a mechanical alternative to the traditional manual process used to level concrete in tilt-up panel casting applications. Also in 2021, the Company completed development of the S-28EZ, the next generation large boomed-screed that replaces the S-22EZ.

Apart from the ability to do “tilt-up panel casting”, these are mostly incremental innovation of existing machine types, rather than completely new products. However, that means they don’t require changes to working practices for construction sites to use them, and hence are much more easily sold. Given that they have already launched more revolutionary products such as the SkyStrip and SkyScreed recently, the overall pace of innovation is impressive.

The company provide more geographical breakdown in this trading update. The US & Australia are the stand-out performers, although Someroo, as they once jokingly called it, is from a low base. Europe is flat half-on-half, but then H1 itself was very strong overall. China is the problem child but this is just an acceleration of the trend of China to prefer cheapness over quality in their warehousing. China was always profitable in the past so they were happy to just let it run. We are guessing that is no longer the case:

In light of current market conditions and recent performance, the Company plans to reduce the cost structure of its China operations to begin 2022

In terms of products, Boom Screeds remain the top performer, driven by US non-residential construction. They say:

The robust 2021 performance in this product category reflects a high-level of large footprint, non-residential construction projects in the US that includes new warehousing required to support the rapid growth of e-commerce activity, factors that translated to an all-time record in unit sales of the Company's largest boomed-screed, the S-22EZ, in 2021.

That US construction is potentially facing labour shortages, and they have just launched an even larger and more advanced boom screed than the S-22EZ, the S28EZ bodes well for this going forward. In terms of outlook, they say:

The Board is pleased with the strong finish to 2021 and looks forward to 2022 with confidence based on the strength of the US market, positive market conditions in Europe and Australia, targeted opportunities for growth from the other regions, and opportunities for growth from new products.

…With a combined view of these factors, the Board expects 2022 will be a highly profitable year with healthy cash generation, modest revenue growth, and EBITDA comparable to 2021 that reflects the planned investment in resources for future growth and the full-year impact of 2021 staffing additions required to support the growth of the business.

Broker finnCap seem to be cautious though and have Adjusted EBITDA dropping slightly due to increased costs on slightly increased revenue:

Too cautious perhaps, given that Somero made very similar comments in their trading statement last year and finnCap interpreted that as a 2021 adjusted EBITDA estimate of $27m vs the $48m actually delivered. That is some 78% higher after multiple upgrades during the year. It is worth noting that the share price has only advanced about 50% during that time, making Somero relatively cheaper today on an earnings basis.

CMC Markets (CMCX.L) - Q3 Trading Update

A terse statement from CMC markets this week:

The Board is confident of achieving net operating income within the range of £250 million to £280 million for FY 2022 consistent with prior guidance.

Compared to previous updates this doesn’t tell us how they will generate that net operating income, the split of leveraged on non-leveraged business, or the net client income retention, for example.

This is good news of sorts, however. It could be argued that the current price had started to price a miss here. Based on Q2 performance this range had started to look like a stretch. Although it may be a rather daft tendency of CMC markets to follow the rest of the financial sector down when you get periods of high volatility. This is daft, of course, because CMC Markets generates higher net operating income in periods of higher volatility, as the following graph from discord contributor Doctor888, comparing reported revenues to the average VIX level, shows:

The average of the VIX since 30th September is around 24. So if this sort of relationship holds then H2 net operating income would be somewhere above £150m and the guided NOI range would be beaten. Given that the CMC markets share price is down in the dumps because they forecast a NOI range early in the year, that ended up being far too high and then had to reduce it significantly, perhaps they have learnt their lesson on underpromise and over-deliver?

IG Design Group (IGR.L) - Trading Update

This was down a whopping 58% on Wednesday on news that operating margins are halving and they will only break even due to cost pressures & the need to pay expedited freight costs. Presumably, they may have had to air freight items?

On Monday’s Mello, Mark discussed Card Factory on the BASH panel where he was concerned that last week’s Profit warning was not the last to come there. This news from IG Design reaffirms his resolve to be very careful investing in the card and gifting sector in the short term.

IG Design have never looked particularly cheap on near-term earnings forecasts which perhaps explains the magnitude of the intra-day drop. However, unlike Card Factory which carries significant net debt, IG Design is forecasting $40m of net cash at year-end which works out to be about 30% of the new market cap. On the surface, this should give them considerable financial flexibility to see them through this difficult period.

However, as with many companies, their year-end is a favourable time for working capital. Given their seasonality, IG have large working capital requirements peaking in October which will need to be debt-funded. As we're now being told that adjusted operating profit will be breakeven, there is a risk (depending on the calculations) of breaching the covenants and requiring a waiver. This looks unlikely to be a genuine going concern issue but requiring a covenant waiver is not a great look, and potentially adds significant debt costs.

The clear answer is to these challenges is to order products earlier, but if they are paying FOB then this puts further pressure on their working capital position. With the share price falls, their working capital requirements are now large compared with the market cap which prevents raising equity instead of debt. They should be able to raise prices in the medium term though, they can't be the only company facing these margin pressures. At the moment, this looks to be another example of the folly of going after revenue growth at all costs.

In summary, all of the issues here are probably fixable, and it now trades on 0.55 Tangible Book Value where the majority of the assets are working capital, which looks good value. It is not a net net, however, due to the presence of bank debt. In addition, there is the potential for banking covenant breach and no indication yet if they can pass on their cost increases. Similar to Card Factory following their latest profit warning, the short term looks biased to the downside, even if the potential for a medium-term recovery looks high.

Director sales at IG Design also tell a story. Since 2019, over £27m of shares have been sold by directors and just £60k bought. Perhaps one to consider only when it is clear that the business has stabilised and the directors finally see value again.

Medica (MGP.L) - Trading Update

Trading had been recovering here, but then:

As previously communicated, Elective scanning activity had recovered to pre-pandemic levels by summer 2021. However, the emergence of the Omicron variant in late November 2021, whilst less impactful than previous waves, negatively affected Elective reporting volumes towards the end of the last quarter. This was largely due to a higher-than-expected number of doctors and healthcare workers being unavailable to work.

Basically, the NHS collapsed, again. However, now they say:

Elective reporting volumes are now rising swiftly again, and the NHS has made funds available to support the management of waiting lists and to provide increased capacity for scanning of elective cases.

Fortunately, UK elective scanning made up a minority of revenue even prior to covid, and in FY2020 fell to just a third. Of a historically similar size and with higher margins is their out of hours service:

Our NightHawk service continued to grow throughout 2021 driven by demand for urgent imaging of patients during out-of-hours. In Q4 2021, Medica secured net growth through 2022 via new clients, in addition to the renewal of several key contracts generating revenue for the longer term.

Ireland has managed covid rather better and therefore it should not be a surprise that demand here remained high. Their newly acquired business in the US relates to clinical studies, something that has had even lower priority than treating cancer etc. in the UK. So it is good to see it is recovering:

In September 2021, we reported that during the first three months of our ownership (April-June) of RadMD there had been some instances of clients delaying patient recruitment into new clinical studies due to Covid-19. However, the growth rate increased in the second half of 2021 due to the resumption of trials that had been put on-hold. This, combined with new contract wins, led to an overall increase in our order book and backlog, providing a platform for growth in 2022 and beyond. The new senior management team is now in place supporting the founders to drive new opportunities and to scale operations to meet client demands.

So, we have the NightHawk business that has been steadily growing, UK Elective which has considerable bounce-back potential in FY2023 (and at least in theory, catch-up revenue), and Ireland with catch-up and the US with a recovery, at least. This is against a backdrop of a shortage of radiology staff and increasing healthcare demand from an ageing population. So it can be no surprise that revenue is forecast to be significantly ahead in FY 2022, indeed, the 17% in Liberum's note today seems fairly conservative.

Unfortunately, they only forecast one year out, but surely a minimum of 10%pa top-line growth should be expected in the medium term. On the downside, this company has proven very capital hungry:

In terms of our FutureTech programme, we are on-track to launch our new PACS reporting system in Q1 2022, which we expect will deliver improved productivity over time and a better user experience for our radiologists, as well as improved functionality and workflow improvements. This is the first major deliverable in our £6 million investment programme that will continue throughout 2022 and 2023.

They have previously spent large amounts of money on in-house IT hardware that was subsequently underutilized. Still, this is certainly cash flow positive: Liberum are forecasting a dividend of 2.7p / share over FY 2022 and an increase in net cash of a further 2.5p / share. So things look interesting here: A profitable, cashflow positive growth share, with a good chance of a FY2022 beat and defensive characteristics.

There are two problems:

1) Valuation: At 161p the forward PE is 17x and cashflow yield is 3%. Not cheap.

2) Very high exposure to a single customer: a government with a record of instability and high levels of corruption.

To take that kind of risk Leo would want a much cheaper valuation. The sort of valuation you might get with an African miner. Scenarios that were unthinkable a few years ago such as cancellation of contracts regardless of consequences, forced-renegotiations or back-door nationalisation now seem possible, either by getting on the wrong side of this government or by a far-left government elected in desperation.

Personal Group (PGH.L) - Trading Update

Personal group first appeared on our radar when Mark spotted that it had failed to recover post-covid despite its financial performance being unaffected in the short term. When Leo modelled it in detail, however, he found that the gap in face-to-face client recruitment would take a couple of years to fill back in. Looking that far forward seemed unwise given the medium-long term uncertainty over the viability of their business model. The employee benefits platform side of the business that is the most attractive part to Mark, was unable to take up the slack in the short-to-medium term. This led to both Mark & Leo selling their positions for a profitable, if un-remarkable gain. The market, however, took a different view, driving it from 200p to 385p by November:

A year on, this update should start to give some insight about who was right.

Overall trading for FY 2021 was in line with market expectations with revenue of approximately £75m (2020: £72m) and adjusted EBITDA of approximately £6m (2020: £10m).

This is a revenue beat but a considerable EBITDA miss against Leo’s model, made when there were no broker forecasts for FY 2021 in place. It is also a revenue miss against broker forecasts issued in March 2021, but EBITDA is in line. Personal Group has significant pass-through revenue in some of its newer business lines and so this is also a less useful metric than it was in the past.

Robust balance sheet with cash position in excess of £22m as at 31 December 2021 (2020: £20.2m).

Which is strange, because the broker and the balance sheet show £17.6m cash at the end of 2020. The difference is explained by £2.587m being recorded as "Financial assets". The notes of the annual report confirm that this is all:

Bank deposits, held at amortised cost, are due within six months and the amortised cost is a reasonable approximation of the fair value. These would be included within Level 2 of the fair value hierarchy.

Anyway, cash looks like a beat since the broker only had "cash" cash increasing by £0.2m YoY back in March.

A strong return to face-to-face insurance sales activity in H2, with good momentum from the Group's return into Royal Mail Group in line with the contract signed in the second half of 2020.

This is good confirmation that their archaic face-to-face model isn't dead yet. And of course they are working on direct sales.

Our consumer technology benefits business, Let's Connect, held up well in challenging circumstances around stock availability.

This is where people borrow to buy things, mostly tech, with repayments taken directly from salary (or wages). Traditionally there was a tax benefit, but the main attraction now is relatively low cost credit.

Sage Employee Benefits platform continued to go from strength to strength, with the number of SME clients rising from 30 to c1,500 over the year, delivering an increased gross Annual Recurring Revenue of £1.6m.

Without knowing how much is pass-through revenue, this is meaningless.

Despite a longer than anticipated lockdown in H1 and continued uncertainty throughout the year the Board believes that the Group's performance in FY21 is testimony to the resilience and continued relevance of the business model and growth strategy. Solid progress has been made in achieving the Group's strategic aim to widen its footprint to multiple sectors of the UK workforce, alongside continued investment in digital channels, putting the business on track for future growth.

You'd have never known from the share price that the H1 lockdown lasted longer than expected! Whether they have made useful strategic progress will only be known with hindsight, unfortunately. We are surprised there was no commentary on impacts from Omicron in late December. This might be because there are normally fewer face-to-face sales meetings at that time of year. Certainly, we can't imagine everybody in a Royal Mail sorting office downing tools and watching a sales presentation in the middle of the Christmas rush.

Going back to March broker forecasts. These were a halving of EPS and dividends to 11.7p and 8.8p respectively. With no certainty that things would get better in the short term, and certainly no forecasts beyond 2021, 260p certainly seemed very expensive on this basis, and indeed the share price did fall back. There were no changes to forecasts following the H1 Update in July, and no FY 2022 forecasts were introduced, but bizarrely, Cenkos upgraded them from "HOLD" to "BUY" as a recovery play. Which brings us to Cenkos's update for today, where they comment:

Inflection point for Insurance book now reached: Face-to-face Insurance visits resumed from June, with positive initial traction, such that the company’s sales teams are now fully booked to at least the end of the year. Conversion rates remain equal to, or exceeding, those seen prior to the pandemic, as insuring one’s health has gained greater resonance with employees. Therefore, this should see new policy sales greatly improve from H2/21E and alongside continuing strong retention rates, lead to policyholder growth from H1/21A’s inflection point. This rebuilding of the Insurance book is expected to see premium income return to pre-pandemic levels over the medium-term, given the c40% larger pool of potential policyholders available to target, following the recent wins of Royal Mail, Kingfisher and Homebase amongst others.

This summarises the bull-case very well. The business model of selling over-priced hospital plans to blue collar workers tricked into attending sales meetings by employers under the guise of it being an employee benefit is alive and well. Profitability will lag increases in policyholders as sales costs are amortised, but recovery looks to be significantly faster than we foresaw, albeit from a lower profitability base. While FY2022 forecasts are in line with Leo’s January 2021 projections, the angle of ascent is significantly faster.

30p EPS for FY 2024 now looks quite possible. If their business model continues to hold up then they could continue to grow from there, aided by higher interest rates. But this remains a poor quality business with regulatory risks and many competitors: If they are allowed to continue making these margins from end-customers then the competition for intermediaries like Royal Mail will become ever more intense, with ever more free services / kickbacks being thrown in, eroding margins.

Surface Transforms (SCE.L) - Trading Update

Surface Transforms has been falling recently, albeit perhaps no more than inline with other speculative stocks. Last time we looked at this they were suffering self-inflicted "production hell". They assured us that no customers would be harmed despite revenue (and therefore shipping) delays, and that everything would certainly be sorted by the end of 2021. This is what they say this week:

The Company is pleased to announce that, at the end of January, daily assembly volumes reached the initial management targets in the production plan required to reach market revenue expectations for 2022. The Company has addressed the specific production issue on the particularly complex furnace described in the 14 December 2021 announcement. Several satisfactory production batches having now been produced in late December and January.

For 2021, they said:

Revenue for FY2021 grew 20% to £2.4m (2020: £2.0m).

Which compared to an £83m market cap But they spend most of the paragraph talking about cash:

Cash at 31 December 2021 was £13.0m; however, this includes a £3.1m irrevocable letter of credit in the name of a furnace manufacturer which will be progressively drawn down, by the supplier, as furnace manufacturing milestones are met. Other interest-bearing loans and asset finance totalled £1.8m (2020: £0.7m), the increase primarily reflecting the Company's acceptance of a local government loan on attractive terms, as described in the Company's announcement released on 24 March 2021.

So £8.1m net cash. They raised £20m in January 2021, so, on a simple historical extrapolation, £8.1m isn't enough to see them through 2022. As cashflow is now coming through, Leo thinks they actually do have enough cash for FY 2022, but will still raise if the share price is strong and/or they win further contracts that need investment.

The Company also intends to invite shareholders to see the new equipment on-site on a capital markets day to be held shortly after the FY2021 results have been announced. Further details will be provided in due course.

Capital Markets Days can be an ominous sign, however, this sounds more like a "here's what we did with your money" rather than a "give us more money" event.

Looking at the update from Zeus, they point out FY 2021 revenue was on the low side of guidance: £2.4m versus "under £3m" guided. Also that production batches were only "satisfactory". And that January production had only "generally" reached targets. They make no changes to forecasts.

For a long time, Surface Transforms core product sales appear to have been shares to investors. In Mark’s opinion the jury is still out on whether their diversification into selling disc brakes to auto OEMs will be equally successful.

That’s all for this week. Have a great weekend and remember to join the video chat on Monday.