Small Caps Live Weekly Summary

Geoplolotics AGFX VTU HFD BWNG MOTR

A quieter week for news, as the rush to avoid suspension for failing to get results out by 30th September has passed. Small cap markets still remain weak. However, placings appear to be making a comeback, particularly in the low-quality, cash-burning end of the market. The discounts remain large, of course, but the willingness of investors to take speculative positions appears on the increase. There is even the odd IPO announced if they have a hot story. This willingness to speculate is also reflected in the biggest risers being companies close to insolvency since the high uncertainty over their future means that share prices move more easily on rumour and speculation. Although this may indicate positive sentiment returning to the market, this isn’t necessarily good news for speculators, as a strategy of picking up pennies in front of a steamroller is rarely a good long-term one.

On Stockopedia, Mark continued his Screening for Value article series for subscribers by looking at resource companies with high earnings.

On Large Caps Live this week, WayneJ takes a geo-political romp around the world.

Large Caps Live

This week, I thought it would be worth looking at the geo-political stuff:

Iran

Iran is an odd place to start but the situation intrigues me. Is there support / encouragement for the student protests from outside the borders - and if so, who from? Either way, it does seem to me that the protests are serious and credible. I think it is a watch this space item. If the regime falls, there will clearly be both short-term and long-term impacts on the oil price - which may be in different directions. Also of note - it seems Iran has been supplying Russia with some very effective drones and ammunition.

China

I get the impression that China may be starting to re-open. The clear and present danger with China is that it might invade Taiwan. But I think the other borders of China are currently the most interesting. There are a number of ex-USSR / CIS countries that border China - and some have resentment toward Russia. Some materials I have read have suggested that President Xi / China is trying to express its support for some of these countries as they express a different foreign policy to Russia. Of course, China treads a thin line as it sucks in a lot of Russian hydrocarbons. In addition, there seems to be a lot of surplus inventory in global supply chains, and that could have implications for Chinese GDP.

Japan

It has been in pursuit of inflation for about 2 - 3 decades. My suspicion is that the Japanese Central Bank is a tad too laid back. Generally, looking through history, when inflation starts to build it is hard to control and starts escalating fast. A weak currency with rising inflation is not fun. I do want to dig into the Japanese market and also their bonds but I am wary of the widow-maker reputation.

Pipelines / Falling out of windows

There has been a lot of debate as to who blew up the pipelines. I want to combine it with the propensity of Russian executives to fall out of windows or otherwise harm themselves. I think that all of this is about giving messages - the issue is to who, from whom and why? I once read an eye-opening book about factions in China. The bottom line was that there are various political factions in China, and each is essentially a bit like the mafia - skimming money, seeking power (and indeed, power leads to money) and control. I suspect Russia is very much the same.

Germany

The pipelines were also hit during a week when Germany was holding a vote on whether to send tanks to Ukraine (they decided not to). But to be fair to the Germans, they are at least promising to send lots of other kit.

India / China

My understanding of new LNG plants is that financing usually requires long-term customer contracts. And I am sure that India / China, and other Asian countries, are wondering if there is any point signing contracts with Russia if, as soon as the war is over, Russia will cancel and instead send the gas into the pipelines. So I am also wondering if blowing up the pipelines was a message to customers of Russia's LNG business that Russia really is committed to them so they really ought to sign long-term LNG offtake contracts.

Ukraine

Ukraine is clearly making rapid advances in Kherson. The worries / concerns I have are that there is some suggestion that the Iranian drones are quite effective below 3,000 feet. And that Iranian ammo for artillery is getting through to Russian troops. It also looks like the Ukrainians have changed their use of the Turkish TB2 drones from bombing missions to targetting / fire-control for artillery and HIMARS. I suspect that is more cost-effective and powerful (instead of having to have a TB2 fly back after each strike etc, one TB2 can direct artillery to multiple targets).

The question is obviously whether Russian reinforcements get there in time, how effective they are and whether Putin will fire a nuke. On the latter point - I think the NATO Gen Sec has none too subtly hinted that NATO will launch a massive conventional strike against Russian forces if there is a nuke. However, I am not sure that the message will get through, that it will be retained and that the factions / hubris will remember the message. Watching Russian TV is truly scary at the moment - there are a number of people who are clearly a tad unhinged.

I think that there will become a point where Russian troops start ignoring orders from Field Marshall Putin - the sense I get from various channels is that this is starting to happen in small ways (eg mick-take of Putin by Russian soldiers on videos, calls to family etc). I think rather than the Russian army being fully defeated in battle, we might get a Russian army that frankly does not give a damn, and either surrenders, deserts / goes home or gets drunk - with variations of all the above. As the army folds, there will come a point of maximum political pressure on Putin - and that is the point where there will be a nuke risk. I think the big issue will be Crimea. If / when Ukraine gets to Crimea - it will be clear whether the Russians will make their 'last stand' there or not.

There is a tendency for people to say that there has never been a successful coup in Russia - that is not entirely the right question or answer. E.g. there was an attempted coup against Gorbachev - it kinda failed but led to a trail of events that led to the breakup of the USSR. I think the possibility of a coup is non-zero - but it will have to be led by the armed forces. And I suspect it will be at the colonel / major or junior general level. The senior generals are political appointees, too carefully watched, neutered etc.

Turkey

Really interesting - hyperinflation and lowering rates. How the President remains in power defeats me. But he seems to consider himself a regional power - negotiating with Putin, allowing drones to Ukraine and hosting a lot of Russians who are temporarily 'holidaying'. At the same time, Turks and Russian / PMC face each other in Syria. I think Erdogan needs to position himself on the winning side and is probably quietly a lot more helpful to Ukraine than meets the eye.

USA

The 'mid-term' elections are coming on. My expectation is that the Trump-supported candidates may do less well than Orangina hopes. The question is whether and when will he declare himself for the 2024 election? If his people are neutered in the mid-terms, he will be out of steam. That will give Biden a mandate and a position to consolidate his position, and that is usually good for the US market. However, I am wary of having wishful thinking and acknowledge that Trump can upset US politics - if his maniacs get into the House and Senate, it might derail support for Ukraine. Recently, there has been some change of narrative from Trump, claiming he has all along been a supporter of Ukraine - clearly, he has forgotten the Hunter Biden episode where he held up support until the Ukrainians handed over info on him. I think that within the US, high energy costs are leading to a redistribution of cash ie to oil companies / Texas / Oklahoma etc rather than cash leaving the country. That is a massive difference between the US and Europe / Japan / China etc. Hence my suspicion is that US GDP next year may be a bit better than markets except; and Europe a bit worse.

EU

Various medium-term weather forecasts are suggesting we might be in for a cold blast. Though the EU has done extremely well re-filling up its gas reserves, I think it may be tight. So I expect in the core, ie Germany, that there will be energy rationing, so German industry might take an extended Christmas break.

I think that will have an impact on China (re demand for products). Furthermore, that implies that the Euro continues to weaken vs the dollar. However, I expect German politicians to start becoming more hawkish and grow a backbone. I think we are starting to see that.

UK

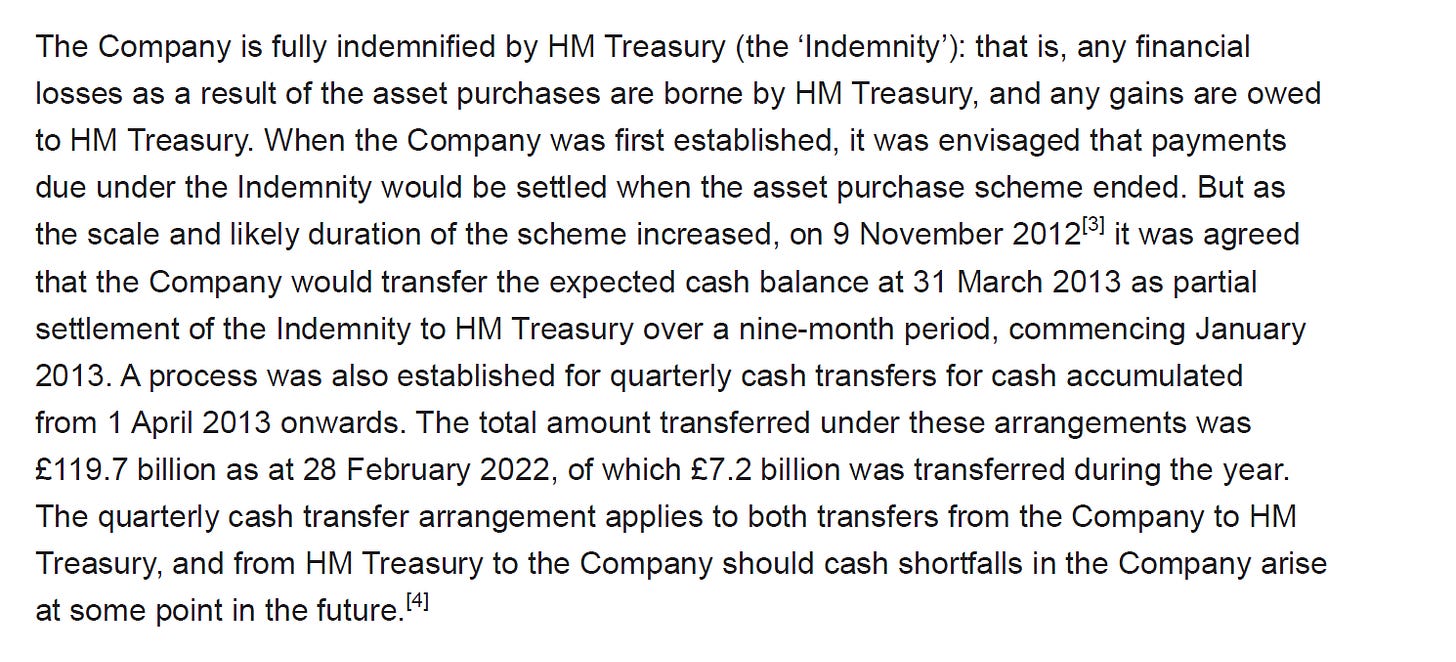

I did not realise that there was a new series of the Muppet Show. What can I say that has not already been said...well there is something...a kinda world exclusive - maybe…the Bank of England bought bonds for QE via a corporate entity - called Bank of England Asset Purchase Facility Fund Limited. You can read the accounts here.

The particular points of note are:

i.e. it is a company under the laws of England and Wales - so it has to file annual accounts and have the usual solvency checks etc

So, HMT has to transfer money from HMT to the APF to cover any losses.

Just sit back and think about that. In the weekend press, the Sunday Times said the BoE QE programme is currently showing a loss of about £200bn. So it seems reasonable that the treasury will have to, probably over a number of years, transfer £200bn to BOE APFF LTD. That is about 8.4% of the current UK national debt.

For other countries, as far as I can work out, the central bank deals with the QE losses by running the central bank with negative equity. Another point the Sunday Times made is that the QE program has delivered about £124bn to the HMT over the last decade and a bit - so roughly about £10bn per year.

(The extract above suggests £119.7bn of which £7.2bn in the last year). Going forward, another way to think about this is that if the £200bn losses are spread over about 10 years that will be about £20bn per year. So the DELTA for the govt will be about £32bn per year or about 3% of the govt budget.

Some of these may be held to maturity, but remember that before the Muppet Show tried its hand at the budget, the BoE was about to start QT where it was going to do about £80bn IIRC of selling gilts per year.

So what next from the Muppet Show? I expect a winter of strikes in the UK. The UK also lacks the gas storage capacity of Europe, and one deep winter freeze will see that revealed, and UK Gas prices are already far above many parts of Europe. The Govt has given a free call option to every gas trader. So they will distract, and I anticipate that in Nov they will claim that the IMF / IFS / OBR are discredited and they will threaten to privatise / sell off the NHS or introduce insurance or another genius self-funding scheme. So I think we are going to have lots of announcements between now and Nov - with Truss trying to gain the momentum and capture the masses - just like the remains of the 1st Russian Guards Tank Army. And I suspect Truss will be equally successful.

So, where does that leave us?

I am keeping a lot of dry ammo, but I am willing to take on short-term trades.

I think that the stress in the UK Gilt market has not yet properly fed through to UK Corporate bonds and loans - and I think that UK companies are about to face a lot of financing hikes / risks.

I think credibility takes a long time to build and is easily lost - and the UK has lost a big chunk - though interestingly, the Bank of England stepping in and 'saving' the economy may have helped restore some credibility for the BoE.

My suspicion is that though the market wants the BoE to hike 75 - 125bps the BoE may be getting real-time data which will make it more cautious. If there next hike is 25 - 50 bps that might lead to further pressure on the pound.

Small Caps

Argentex (AGFX.L) - Trading Update

Good news:

Argentex expects to report six month revenues of £27.4m, a 75% increase compared to the same period last year (H1 2022: £15.7m)* with costs remaining in line with management expectations. There has been continued strong client demand with the number of corporate clients trading growing to 1,393 (H1 2022: 1,241)*.

This leads to an ahead statement:

As a result, the Board is confident that the Group will exceed current market expectations for the period ended 31 December 2022.

The question is, which expectations? And why are they quoting for the period ending 31 December 2022 when their year-end is 31 March 2023?

Their previous NOMAD had forecasts of £42.8m and 9.3p EPS for FY23. They then changed NOMAD and broker to Singer, who issued a forecast of £39m revenue & 4.9p EPS. Management were evasive when we asked about this and some other issues on their last Investor Meet Company presentation.

So even if they beat the 4.9p EPS by 20% and do, say, 6p EPS, they are still massively down on forecasts at the start of the year. It isn’t hard to beat if you get your broker to slash these first. This is looking a lot like a magic trick. However, the audience appears to have been wowed by the spectacle nonetheless, with the share price up around 20%.

It isn’t helped that forecasts in Stockopedia appear to have not been updated for the change of broker:

The real forward P/E is likely to be around 18, and EPS down on 2022. This looks expensive, particularly when management appears to be more interested in managing the share price than the business.

Vertu Motors (VTU.L) - Half Year Results

H1 6.5p EPS vs FY forecasts of 7.5p. That's lower than Leo expected, but they seem much more confident about H2:

The Board now anticipates that full year profits will be ahead of market expectations

Excellent news, then. This appears to be off the back of a strong September. With broker Zeus saying:

We are raising our FY23 EPS forecasts by 13% post these results

Zeus also downgrade revenue for both 2023 and 2024, as Leo predicted. However, EPS forecasts for 2024 are up from 7.2p to 7.9p due entirely to the reduction from 25% to 19% in expected corporation tax and some (but not the latest) buybacks, where they say:

The Board has agreed a further £3m buyback programme being announced today.

This isn’t their only option for capital allocation either:

The Group has the scale and firepower to take advantage of the considerable sector changes working in partnership with the Group's Manufacturer partners through accretive consolidation of this fragmented market.

…There is significant opportunity to leverage the strong balance sheet to provide firepower for acquisitive growth.

There is lots of good stuff in the commentary of today's update, including:

* Cost savings - which helps explain why so confident of H2 profits despite extreme uncertainty

* Building a platform - for the acquisitions which are very much still on the cards

* Further enhancements online

On the outlook, there is perhaps a small concern:

Manufacturer bonus levels on a quarterly basis reduced, due to the volume trends.

During covid, the scheme was suspended, and the dealers effectively paid anyway. You might expect something similar to be happen when manufacturers are restricting supply, and the fact it is not, suggests they see dealer margins as more than sufficient. Where we see:

September profitability was the third highest recorded for this month in the Group's history.

…A tight supply environment for new and used vehicles is anticipated to continue well into the next financial year. Margins are therefore expected to remain strong and used car pricing robust.

There is caution on demand but no mention of interest rates.

Leo has repeatedly warned that there is no long-term future for the franchise model. Yet they hold franchise assets on the balance sheet as indefinite life intangible supported by their ability to earn profits. This is what the company have to say about the first of these moves:

A number of the Group's Manufacturer partners are actively involved in consulting on the introduction of agency models for the sale of new retail cars. These models change the nature of the profit and loss account for these sales and reduce working capital requirements. Mercedes-Benz will be the first major Manufacturer to make this transition on 1 January 2023. The Board does not currently anticipate a material change to overall profitability from these changes.

Clearly, manufacturers will not want to rock the boat with initial specified margins, but Leo is much less optimistic than Vertu about the long-term impact on profits. There are a variety of agency models, but those that see the manufacturers own the customer contacts will make some of the current investments redundant. At the very least, the inevitable write-offs of those dodgy franchise intangibles won't look good.

There is a good interview with straight-talking CEO, Robert Forrester. And a full presentation here.

We are sceptical about the value of the intangibles and believe the company-claimed Net Tangible Asset Value, including the IAS 19 pension surplus from 31/8/2022 of 71.2p, should not be used. However, this still leaves an NTAV of around 70p/share compared to a share price of 46p. This looks far too cheap, especially since competitors have been taken over at multiples of book value.

Halfords (HFD.L) - Acquisition of Lodge Tyre

Halfords continues to acquire in the tyre fitting space:

…the acquisition of LTC Trading Holdings Limited and its subsidiary Lodge Tyre Company for total consideration of £37.2 million with £33.2 million paid on completion and £4 million paid in FY25 subject to performance.

The benefit they are getting is scale:

The directors of the Group (the "Directors") believe that the Acquisition is both strategically and financially compelling, delivering on Halfords' objective of further evolving into a business more heavily weighted towards motoring services, which provide more resilient, needs-based revenue streams.

However, the price paid seems to be high at c8x EBITDA:

Lodge Tyre generated pro forma EBITDA of £4.7 million on a pre-IFRS 16 basis (1) in the year ending 31 March 2021. The Group expects to deliver incremental synergies worth £3.8 million (EBITDA) by year 5.

Even with those synergies, this is not obviously cheap:

The Consideration reflects a 4x multiple of year 5 EBITDA (post synergies).

However, given that it is debt funded, it clearly exceeds the cost of debt. They also claim the IRR exceeds their WACC:

The deal will be EPS accretive in the first year of ownership and will deliver an IRR that exceeds the Group weighted average cost of capital.

Earnings enhancement used to be a given. Companies would buy earnings with debt paying 3% interest, and as long as you don’t pay more than 30x you’ve got an earnings-enhancing acquisition. Not so easy in a high-interest rate environment. This is not going to be an issue for Halfords, but maybe for some of the more highly-rated sketchy roll-ups that were popular with private investors over the last few years.

It also may be that Halfords underestimate their cost of equity when the market values their current business at around 3xEv/EBITDA. The alternative use of this capital could have been to buy back their own shares, which still look cheap, despite a recent bounce.

N Brown Group (BWNG.L) - Half Year Results

Weaker H1 revenue here has led to a big drop in EBITDA & profits:

Net debt has reduced by £24.8m but remains relatively high at £243.5m vs a £112m market cap. However, this is financing a large customer loan book. Net tangible asset per share has increased to around 73p, and the vast majority of the assets are customer receivables. So it really matters if they are being paid! And there doesn't seem to be any abnormal move here:

We will continue to closely monitor customer behaviour and provide support to customers. We are expecting a steady move back towards pre-pandemic arrears rates. We have yet to see a significant change in the performance of the debtor book as a result of the macroeconomic environment.

This has always had a relatively large level of impairment & forbearance:

The overall outlook is weak, however:

We have seen significant volatility in trading trends in the second quarter and into the third quarter of FY23, including both pre and post the 19th September bank holiday. This, combined with other macroeconomic conditions, makes visibility on revenue trends difficult. Based on the assumption that macroeconomic uncertainty and inflationary pressures continue through the second half of the year, we have revised our assumptions for H21 product revenue and now expect it to decline in line with the year-on-year decline seen in Q2 and September.

And this is effectively a profits warning:

As a consequence of the above factors, we now expect FY23 Adjusted EBITDA in the region of £60m before growing again as the Group's strategy is executed.

Previous forecasts from Shore were for £86.8m EBITDA so this is a fairly large downgrade. They'd still be profitable, however.

The share sold off around 20% first thing on Thursday, but then bounced back to down just 11% - a mere flesh wound in the current markets. The c0.3x TBV presumably providing support. Given this is largely a receivables book and it would take monumental write-downs to see this wiped out, this looks too cheap if investors willing to take the long-term view. Given the headwinds, it may be too early to call the bottom on trading or the share price, though.

Motorpoint (MOTR.L) - Half Year Trading Update

Motorpoint are a second-hand car supermarket, but their focus on "nearly new" clearly overlaps with franchise dealers' used car operations. Here’s what they have to say about current trading:

Increased market share of the 0-4 year old market to 3.6% (H1 FY22: 2.9%) - reaching a record high in June of 3.8%

That's a pretty fast growth rate, but it is not LFL. Still, market share gains will hurt competitors in the used car space, especially at a local level.

Opened 18th location (Edinburgh) at end of September and 19th location (Coventry) due to open at end of October 2022…

the Group invested an incremental c.£4m compared to H1 FY22 to grow market share through price leadership and new openings

As a result:

Profit before Taxation ("PBT") for the period is c.£3m. This PBT is significantly lower than H1 FY22 (£13.5m) and reflects the increased strategic investment (c.£4m)...

This collapse in profits is far worse than Vertu has seen on the used side. Apparently, Motorpoint are chasing volumes, not profitability, which is bad news for competitors. As we already discussed, Vertu reported weak used demand in September, but they have (at least) two other legs to their strategy, and so this wasn't so material. With Motorpoint, it is their core business, and so they go into more detail:

in September volumes were down c.9% caused in part by adverse economic news flow and political uncertainty which continue to undermine already fragile consumer confidence.

Chasing growth and volumes at the expense of margins in a weak market leads their broker Shore to cut forecasts by a massive 50% in the current year to March 2023 and 60% next. Interestingly, they think forecasts out to 2025 are also worth publishing, and these have been cut to show growth from the lower baseline. The bull case is now apparently that these forecasts "may prove cautious".

Incredibly the share price is only down 16% and still trades on 15x 2025 "forecasts" and nearly 4x tangible book. All this really just goes to show that there will always be a threat to serious operators trying to make money from those chasing volumes and their deluded investors. The threat to motor dealers from internet-only competition has faded but remains on the hybrid side.

That’s it for this week, have a great weekend!