Small Caps Live Weekly Summary

DOCS SOM ALU ACSO RAI LOOK NWT FUL CNKS

Wayne moved Large Caps Live to Tuesday this week due to a personal commitment, taking a look at footfall and Dr Martens.

In the small cap world, this week brought lots of results announcements so we did our best to look at as many as we could.

One of the worrying trends we are seeing though is the increasing power of share tips to move small cap shares. In the last week, we have seen Creightons, Northbridge Industrial and T. Clarke all have significant movements on no news because they have been tipped somewhere. There has always been a tip-effect in the market, but perhaps the worrying part is that, at the moment, these are tending to move the market far more than actual results, ahead statements, or upgrades from the companies themselves. By nature, tips tend to be very unbalanced analyses, since the tipster is either selling a service, (buyers of information often prefer certainty to accuracy), or worse, trying to generate undue excitement in their own holdings.

Tip buyers tend to be some of the weakest holders of shares, too. As the saying goes; “you can borrow someone’s idea, but you can’t borrow their conviction”. So hence, those who buy purely on tips tend to be net losers in the long term.

It is worth reiterating at this point that nothing we talk about here is a “tip” or advice. We try our best to provide balanced commentary, but we are not immune to biases or misjudgements. With that in mind, let’s look at this week’s news:

Large Caps Live Tuesday 7th September

Footfall

Everything I read says that footfall is still down on the high street. Examples such as the following:

Every time I go out I see some high streets and some shops busy. I will go even further: my wife and a friend regularly walk (ie sometimes daily, several days in a row) from our village to the next village to have a coffee and some pastry or granola and then walk back. The village in question has had several new coffee shops and restaurants (all non-chain) open. But despite being regulars, my wife and her friend found that during the hot summer they could not get seats or be served in some of their regulars without booking - and sometimes they were expected to book 2 -3 days in advance which is hard when you don't know if you will walk on a particular day or at what time.

I know that your mind can play tricks on you vs previous years but the reduced footfall does not seem to match my observations. So I have been thinking and I would like to make a few suggestions:

(1) Footfall on the high street is not the same as footfall through the high street.

Let me use a typical major London train station as an example eg Liverpool Street Station. I fully expect that footfall through that station is significantly down as people no longer commute to work. And that station has various shops around it so their footfall will be down.

(2) In comparison I am seeing small commuter towns and villages busier than normal as individuals and families shop and travel locally. But also places like eg China Town in London (ie around the theatre district / Leicester Square).

(3) Foreign visitors / tourists are clearly down. But again most tourists will be passing through eg the centre of London for tourist activities (eg see Buckingham Palace) and shopping will be incidental (but significant). But I think there are a lot more UK sourced visitors to central London.

(4) So if we put all the above together I hope you will understand why I distinguish between people passing through the high street (or a shopping mall) and those for whom the primary designation is actually the mall or shopping.

(6) An additional observation is that I read somewhere that the population of the UK may have fallen since the pandemic started – eg the following Sky news article states a fall of 1M. Though the ONS suggests there may have been a smaller increase than previous years instead.

(7) My thought is that if you are eg a European in London, you are here to work, party or be educated. Obviously, those are not mutually exclusive. But I have seen suggestions that London’s population may have fallen by somewhere between 300,000 & 700,000.

Now, let’s focus on the last set of numbers. If the population of London has really fallen by 700k on say a base of 9M that is a fall of 7.78% which is massive (and probably unlikely). But it is worth remembering that London has a massive university sector so it could include a lot of people now studying from home elsewhere in the UK.

(8) If we include that in the mix it would suggest to me that footfall in London might be down due to fewer people going to work, fewer tourists and fewer students. But that some of that population might pop up as footfall in smaller towns and cities and villages and be missed. I suspect the major footfall agencies do not cover the smaller high streets.

I want to particularly emphasise that last point. I have no idea on the methodology of the companies that report footfall but I suspect that they use sensors linked to the automatic doors or the security sensors in major retailers. BUT that as a result they are concentrated in major towns and major retailers.

Dr Martens (DOCS.L)

Dr Marten floated earlier this year and frankly, I did not pay much attention. It floated at 370p - rallied up and has drifted down. It is on about 25x PE but what caught my attention was the revenue growth:

This is a company which sells via its own shops, via third party retailers and via the web. But generally, I would suggest that shoes are one area where you want to try things on. Yet this company, with a March year-end, grew revenue from £454M in 2019 to £672 and then £773m. There are some quirks - eg they have taken control of their own distribution in a few countries. But frankly, that is all on the edge. They have also pushed D2C and internet sales.

You can see the change in eCommerce but it is not the full story. And the increase in stores:

This table suggests that the stores’ revenue fell by 40% but that eCommerce covered it. And wholesale - but the latter with include both other retailers and other online players. Also, I am not entirely comfortable in distinguishing between retail and eCommerce as I reckon the stores provide physical reminders of the brand and allow testing of sizes before you order online. So anyway that was the first retailer that caught my eye.

The Chris Camillo chatroom (Chris featured in the book Unknown Market Wizards) suggests that the driver of Dr Marten sales and the reason to buy is that the shoes are being adopted by 'Goth culture' and that there are increasing searches for Dr Martens as a result. I am not 'entirely' convinced by that.

Neither is Leo, who saw little evidence of Goth culture or DM’s at a recent festival.

Anecdotally, the quality has declined significantly in recent times, yet remains priced as a premium product. Is this the Private Equity ownership effect?

Small Caps Live Wednesday 8th September

Somero (SOM.L) – Interim Results

In July they told us that trading was strong:

Group H1 2021 trading has been stronger than previous years with trading in North America in the last two months of H1 2021 having exceeded our previous expectations.

This led Leo to forecast £53.3m for H1 and the brokers had £110m for the full year, leaving some H2 weighting, but lower than usual. In the end, however, the results were ahead of expectations:

H1 revenues were US$ 64.4m (H1 2020: US$ 35.3m) led by a very strong and highly active US market

o H1 2021 trading in the US was highlighted by accelerated activity from customers working to catch up on projects previously slowed by COVID-19 restrictions and by healthy demand for new warehousing

But it wasn't just the US:

Three of the Company's five international regions reported H1 2021 revenue growth over H1 2020 reflecting generally healthy non-residential construction market conditions and lessened COVID-19 restrictions compared to the prior year that enabled an increased level of activity

Followers of the company will not be surprised to hear that China was one of the two regions not ahead, however:

In China, H1 2021 revenues declined to US$ 1.7m compared to US$ 1.8m in H1 2020. Disruption from the COVID-19 pandemic and deteriorated US-China trade relations are two factors that have hindered near-term growth in this market, but the ultimate obstacle to meaningful contribution from this market is the lack of demand for quality concrete floors by Chinese building owners and end-users.

They have previously reported that China is profit-making however.

Gross margins were up, and operational gearing ensured EBITDA margins were significantly higher, up from 25% to 38%. Not unusually in today's market, H1 EPS came out similar to the whole of the previous year. Outlook remains strong:

…positive momentum is carrying over into H2 2021 with a positive outlook for the US market that is supported by an active non-residential construction market, extended customer project backlogs and continued strong demand for new warehousing.

One of the worries earlier in the year was that they were investing in headcount for growth but that it would raise costs in the short term, so this increased EBITDA margin is very pleasing.

Here's the overall guidance:

We maintain a confident, positive outlook for the remainder of 2021 and anticipate delivering record levels of revenues and profits to shareholders for the year. Although we recognize a level of risk associated with a potential resurgence of COVID-19 infections and from supply chain shortages that could slow our ability to fulfill customer orders for equipment in H2 2021, based on the remarkable H1 2021 results and an overarching confidence in the health and momentum of the business, the Board has raised guidance for 2021. The Board, taking a prudent approach to revising guidance in consideration of these factors, now expects full year 2021 revenues will approximate US$ 120.0m (previously US$ 110.0m), adjusted EBITDA will approximate US$ 42.0m (previously US$ 35.0m) as we anticipate slightly less of the benefits from increased volume and the leverage of support costs in H2. We also now expect year-end 2021 net cash will approximate US$ 36.0m (previously US$ 33.0m), a view that takes into account anticipated 2021 spending on the facility expansion project.

Accordingly, finnCap have upgraded FY revenue to £120m and EPS to 55c. Perhaps more importantly, they have also upgraded FY 2022 figures to be modestly ahead of FY 2021. Do watch out however, Arden has not yet updated their forecasts despite putting out a short note, so consensus on the likes of Stockopedia may lag reality.

We believe there remains some upside on the FY forecast given the strength of the outlook statement and that it currently implies a very unusual H1 weighting. Perhaps £128m revenue for FY 2021 is quite possible. That higher revenue probably implies EPS about 10% higher. So plenty of time for the fourth upgrade of the year. Converted into pounds, EPS forecasts are therefore around 40p, with 44p quite possible. This company has been traditionally fairly modestly valued and so the current 530p seems about right on a historical basis.

There are a couple of reasons why they always seem on a modest valuation. The first is that revenue doesn't have a clear upward trend: $85.6m, 94.0m, 89.3m, 88.6m from 2017 to 2020. However, the 2021 figure should be a record.

The other reason is that no single product or region has an obvious growth trend.

(Those are log scale graphs, of course.)

Somero continues to remain dependent on the US and Boomed Screeds, despite attempts at diversification. Line Dragon has been a successful new introduction in recent years, but SkyScreed remains unproven. It's hard to know if this represents the potential for the newer products to really take off, or a risk that US boomed screeds are going to be a downside risk going forward.

On the positive side, there is no obvious indication that older lines are fading away, although the above are broad categories that cover a number of different SKUs. So the real strength here continues to be the low capital intensity and high cashflow conversion rather than growth. Yes, there are opportunities to invest in both sales (they tell a good story around Australia this time) and incremental new product development, but there's little indication high structural growth is imminent.

It is also worth mentioning inventories. Partly because this might uncover supply chain effects and partly as they might indicate levels of expected demand.

So, some evidence of stocking up on raw materials. And they have significantly high remanufactured for sale. But finished goods are down YoY despite more product lines.

Our view is that there is still more internet warehousing left to build, as companies improve efficiencies by moving to larger or more modern facilities. Despite the concerns on the overall trend, and with new products yet to really gain serious traction, then this is on a forward earnings yield of c.9% where the vast majority of those earnings end up as free cash flow. New product development is entirely expensed so this potential has come at little capitalised cost. The gross margins and ROCE all remain phenomenal for the business area. And there is a chance for the fourth upgrade this year, as the H1/H2 weighting still looks slightly off in the forecasts.

The last time we looked at Somero we said that it didn't look like the time to take profits. With this outlook, it still doesn't.

Alumasc (ALU.L) – Full Year Results

This is a strongly performing company that we missed out on, having reviewed them at c.80p and at c£1.20 and both times being concerned about the valuation. What we missed was just how strong the outlook for their products was going to be, with a combination of positive factors at play:

A company already restructuring, improving margins etc.

The shock of COVID forcing further focus on costs

High operational gearing

A massive post-COVID bounce in demand

Yesterday they released their full-year results to 30th June and the headlines read really well:

· Double-digit growth in revenues from continuing operations: £90.5m (2019/20: £76.0m): +19.0%

· Group underlying operating profit £11.0m (2019/20: £4.2m): +162% reflecting both strong growth and the benefit of structural cost and efficiency gains

· Underlying operating margin: 12.2% (2019/20: 5.5%)

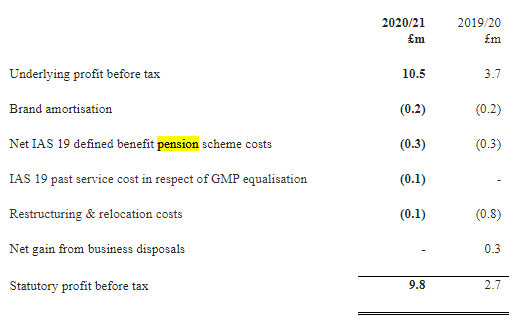

· Reported PBT £9.8 million (2019/20: £2.7 million)

These would look great apart from we just looked at Somero where the revenue almost doubled (albeit half-year results off the covid low point.) Operating margins also look weak in this context. But the EPS growth is the stand out:

· Underlying EPS: 23.7p (2019/20: 8.2p): +189%

· Basic EPS: 21.2p (2019/20: 6.3p)

This puts them on a historical P/E of c.11. So reasonable value on the surface. This is based on adjusted figures though and often companies like to exclude costs that are real and ongoing. Last week, we looked at how Mpac excludes pension scheme costs from their adjusted profits despite being an ongoing cost and this adjustment makes Mpac decidedly unappealing on a valuation basis.

Alumasc do a similar adjustment:

However, unlike Mpac these are actually non-cash:

Net IAS 19 defined benefit pension scheme costs of £0.3 million (2019/20: £0.3 million) are also non-cash charges. These relate to the Group's legacy defined benefit pension scheme, which was closed to future accrual in 2009. The value of the charge is determined by actuarial assessment and represents the notional financing cost of the Group's pension deficit.

So in general, the income statement adjustments are reasonable. What isn’t non-cash though is the £2.6m of deficit funding that they have to make:

The deficit reduction payments are agreed between the Group and the scheme's trustees, based on triennial actuarial valuations. At the last review on 31 March 2019, Alumasc agreed to pay £2.3m annually under a seven year recovery plan. As part of its Covid-19 cash conservation measures, the Group agreed with the trustees to defer £0.6 million of deficit reduction payments due in financial year 2019/20. £0.4 million of this was repaid over financial year 2020/21, and the remaining £0.2 million will be repaid in the first half of financial year 2021/22.

So deficit recovery payments need adjusting out to get to the true underlying picture. In Alumasc's case, this represents around 25% of underlying PBT so this increases the rating to about 15x P/E.

As with Somero, the big risk is that the performance is a short-lived boom rather than a sustainable uptrend. In the last 10 years or more of following Alumasc, we have seen them go through these boom and bust cycles multiple times.

But fundamentally, why would you own Alumasc on 15x underlying earnings with a small net debt vs Somero with net cash, higher gross margin, higher return on capital and on 11x earnings with a higher dividend yield. Both are exposed to the same risks of construction cyclicality so I see little reason to favour the market dynamics of Alumasc to Somero. Indeed, Somero has perhaps better structural tailwinds with flat warehousing.

Accesso (ACSO.L) - Trading Update

Accesso were the king of EBITDA and from about 2018 onwards and with the price over £20, most sane commentators were saying a) the valuation was mad and b) why the hell didn't they raise some money to cover the negative cash flow? Eventually, this caught up with them and they were forced to raise in May 2020 at 290p.

That proved an excellent time to buy in, with the share price now back to 920p. The reason for this amazing recovery is both expected and obvious when you think about it. They provide services to theme parks including virtual queuing. When these closed they were in serious trouble, but when they started reopening, virtual queuing was clearly the way forward. In July they said:

accesso is pleased to report that since its AGM trading statement on 18 May 2021, the Group has continued to benefit from pent-up customer demand and the accelerating trend towards online commerce in its end markets. The Group has seen operators' need to manage capacity boost its online reservation activity, and its virtual queueing solutions have seen demand well beyond historic levels. This has resulted in year-to-date revenues in 2021 significantly ahead of expectations.

As a result, in the absence of major new impacts from the pandemic, the Board now expects full year revenue for 2021 to be in excess of $100m.

Following on from this we get a short further update today:

through July, August and the Labor Day holiday period, accesso has built on excellent first half performance and continued to capture high demand for its technology solutions. As a result, trading during this period was very strong. The Group's ongoing momentum now leads the Board to revise upwards its expectations for full year 2021 revenues to not less than $117m. This represents full recovery to 2019 trading levels.

Given that worldwide attendance levels are well below 2019 peaks, that their revenues are above, underlines a structural change. It also bodes exceptionally well for performance once attendance levels do fully recover.

This rapid growth in revenue alongside a slower return to normal operating expenses will result in Cash EBITDA being significantly ahead of current market expectations for both the half and the full year. The Group is currently deploying additional resources across technology implementation, product development and customer support to calibrate for the new demand. As previously signaled, these investments will have a limited impact on Cash EBITDA in 2021; their full annualised effect will be felt in the 2022 financial year.

People should be concerned about the ongoing emphasis on EBITDA here though. The good news is that they seem to have at least partially reformed themselves:

(That was from the FY 2020 results to 31st Dec.)

Some of that reduction in capitalised development costs will have been covid / lack of cash related, but it also means that EBITDA is a lot more meaningful than it has been in the past. We can't really value it however...too much is moving too quickly.

RA International (RAI.L) – Interim Results

RA International’s Interim Results were never going to be great given that they are still feeling the effects of COVID, particularly on getting staff into projects on the ground, plus the tragic events in Cabo Delgado costing $10m of revenue in 2021. And indeed they weren’t:

Revenue of USD 26.2m (H2 20: USD 29.1m, H1 20: USD 35.4m) and underlying EBITDA of USD 5.0m (H2 20: USD 6.2m, H1 20: USD 8.1m), in line with expectations for the first half of 2021.

This led to an EPS of just 0.6c. There continues to be cash outflow too:

Cash as at 30 June 2021 of USD 10.1m, reflecting a USD 7.5m decrease from December 2020 year-end, primarily attributable to working capital movements which are expected to begin to reverse in the second half of the year.

Although these are in line with expectations, I had expected the market to take these badly. Stockopedia has expectations of 2.89c for the full year, so 28x forward P/E is not exactly cheap:

However, the news of a contract win at the same time seems to have had a bigger effect:

The contract with US Navy Facilities Engineering Systems Command Far East is a five year contract for design and construction services supporting their base on the island of Diego Garcia in the Indian Ocean. The contract ceiling for this award is USD 249m and RA International and ECC will compete for individual task orders with four other awardees.

There is no significant guaranteed revenue from this since it is effectively a framework agreement but management are assuming c$20m over 5 years net to RA International. So this is perhaps not as material as it may first appear, however, there is a chance of them winning much more than this. Many of these types of contracts have to go to US companies, so expect many more of these sorts of partnerships in the future. This is what they have with Cherokee Nation. The good news is that these often have similar margins whether they are prime or sub-contractors.

The order book has declined, given that they have excluded $60.5m from Cabo Delgado:

This is still good, considering it doesn’t include Danakali or Diego Garcia.

In terms of Cabo Delgado, they expect that Total could return within about a year or so which would mean they would begin to operate again in 6 months’ time. They are likely to move any high-value equipment out to Pemba for servicing and for protection of the assets from being stripped.

Management have confirmed that the FY21 forecasts are baseline and don’t include any significant new contract wins that may generate revenue in 2021 so there is a small chance of a beat. Although, at the current rating that isn’t going to make much difference.

We expect to see heightened levels of project starts by existing and new customers and, depending on timing, this could lead to a materially stronger performance in the second half of the year but, in any event, should bridge to a stronger performance in 2022.

More importantly, they are comfortable with the FY22 forecasts given the current order book (assuming no major travel restrictions are re-introduced.) Which means a forward P/E of 8. Which sounds much better value, particularly in the current market.

In summary, there is something for both the bulls & the bears in this report. The bears will point to a bad year and concerns that issues like this will keep reoccurring given the type of operations. The bulls will point to a very low 2022 rating and significant contract wins with some of the most prestigious clients in the world. I think fundamentally it comes down to how much you trust the management to execute as to whether this is a buy or a sell at the current price.

Small Caps Live Friday 10th September

Lookers (LOOK.L) - H1 Results

They had multiple accounting problems recently and also the balance sheet isn't so strong as our pick in this sector, Vertu, but of course, we follow them for read-across.

Yesterday they issued their H1 results to 30th June:

H1 trading exceptionally strong despite closure of the showrooms throughout Q1. Trading underpinned by robust consumer demand and an improved omni-channel customer proposition, resulting in ongoing outperformance of the UK new retail car market (+17.4ppts) and a market share of 6.7%. Excellent used unit growth (LFL +38.3%) combined with strong margins.

· Revenue of £2,153.2m (2020: £1,570.6m) with all divisions showing growth versus last year.

· Record H1 with underlying profit before tax of £50.3m (2020: Underlying loss before tax £36.5m). Statutory profit before tax of £50.7m (2020: Statutory loss before tax £50.4m).

These are in line with the trading update issued at the end of July:

Given the strong H1 performance and the Group's ongoing corporate responsibility agenda, the Board has voluntarily undertaken to repay all CJRS grants received for H1 (£4.1m) before the end of H2.

Now, this is interesting. While companies like UPGS paid this back ages ago, retailers who were shut down directly by the government response have been more willing to hold on to the cash. Vertu in particular have been insistent they'll hold on to everything despite record results. But note that this £4.1m is a small proportion of total government support. Not only was most of the CJRS received last year, but there was also very significant business rates relief. Still, we think it remains a risk for Vertu that they will have to repay something, especially as they start paying a dividend.

Strong cash generation with net cash of £33.0m at 30 June 2021 (31 December 2020: Net Debt £40.7m) driven by strong trading performance, continued working capital control and cost discipline. Property portfolio equivalent to 77.8p per share (2020: 80.4p per share).

This needs to be read with a pinch of salt. Their balance sheet as of 31st December 2020 was by no means strong, with net assets of £282m, of which £190m are goodwill and intangibles. The ongoing value of the latter is highly questionable given that the franchise model's best days are behind it. The market cap is currently £266m, so far in excess of tangible assets, even after the profit accrued in H1. Also, we believe they don't count vehicle stocking loans as debt until they start accruing interest. So you might want to add a chunk of their payables into that debt / net cash figure.

In addition to the revolving credit facility, the Group has stocking funding lines which were utilised at £210.0m as at 31 December 2020 (2019: £337.1m).

Actually, it looks like even interest-bearing stocking loans are excluded from debt. In contrast, Vertu are much more conservative in their treatment. And haven't had to just restate to years worth of previous results. Yet another reason why we would strongly urge people to look at balance sheets rather than rely on company claims or Stockopedia summaries.

Of course, it is the outlook that really matters here:

Trading during July and August remained strong, exceeding expectations, primarily driven by unprecedented used vehicle margins. Order take also remained robust and the Group has a strong order book for September and the remainder of 2021.

We've highlighted this before about order intake - if people are still willing to get in the queue despite a long wait for delivery then the revenues will come through eventually, it is just a matter of timing. Lack of supply should just result in delayed revenues, not loss of revenue. This is what we've also seen at ScS, incidentally. But while we're used to looking at order intake / backlog for furniture companies, this is not a usual metric that car dealers report...until now.

We’re quite optimistic about this as it should mean improved revenue visibility and markets may not recognise that in valuations. So, is there an upgrade since the end of July? Vertu have had two.

Given the ongoing and well documented new and used vehicle supply restrictions, combined with uncertainty resulting from COVID-19, there remains considerable variation in vehicle delivery dates and availability and in this context the Board believes it is right to retain its cautious approach.

Notwithstanding this, the Group remains well positioned for the remainder of 2021 and beyond. Therefore, current expectations for underlying profit before tax for 2021 remain unchanged after having committed to fully repay all CJRS grants received for the current financial year before the end of 2021.

So, effectively, we have a FY upgrade of the CJRS amount, namely £4.1m. Adjusted PBT forecasts remain at £53.1m according to Zeus. So that's less than an 8% upgrade. It also implies an underlying H1-H2 split of £50.3m / £6.9m. This seems relatively cautious and is also in line with what Vertu expect, although the latter's reporting cycle is shifted 2 months later.

Just before we finish on this, August's SMMT registration figures were slightly disappointing since they appear to imply industry FY forecasts set in July will now be missed. The noises out of the manufacturers also seem to have worsened. So I think things continue to deteriorate on the new car supply side.

In any case, as we have hopefully made clear, we much prefer Vertu in this space.

Newmark Security (NWT.L) - Final Results

Newmarket presented at one of the physical Mello events a few years ago and had an exciting story of a business transitioning from products to data services that caught the attention of some of the attendees.

For these results, they claim that:

Overall performance across the Group during the year was ahead of management's expectations

But that surely is just a case of very low expectations. Here are the headlines:

• Revenue was marginally behind last year as communicated in the year end trading update announced on 9 June 2021 at £17,658,000 (2020: £18,767,000), a decrease of 5.9%

• Gross profit margin decreased to 37.5% (2020: 39.7%)

• Operating Profit before exceptional items was £79,000 (2020: £604,000)

• Operating loss after exceptional items was £38,000 (2020: Operating profit £305,000)

When we looked at Newmark Security on 9th June 2021, Leo commented that:

I am sceptical that I will agree it was a profit once they issue the full results. They have such a long history of exceptionals that I wouldn't adjust them out.

Also, in FY 2020 they recognised a tax credit on the basis they expected to make profits in future. In my view this was a bit premature.

In any case, don't be fooled if Stockopedia claims 0.24p EPS last year - it isn't true.

Prescient, it seems, since it is continued exceptional items that allows them to post a positive operating profit:

Redundancy costs often should be considered one-off, but in this case the habit of having to close down or downsize unprofitable operations means this is stretching the one-off nature. Likewise, it is a tax credit of £297k that allows them to post 0.04p EPS. Although some of this is R&D which had led to cash payments for tax credits, adjustments to prior periods have helped them out again:

On a cash flow basis, working capital flows, the “exceptional” items, plus R&D means that they see £600k of cash outflow for the year.

A current ratio of 1.8 doesn’t seem to indicate any immediate balance sheet distress, but the fact that they mention the going concern statement in the chairman’s commentary means that not all is well in this area:

We are in a good position following COVID-19, although cash remains a key focus, especially with the challenges we face managing our inventory levels and dealing with the global shortage of components we need to build our products. We continue to work closely with our bank (HSBC), through which we have our CBILS facility. Post the balance sheet date we have agreed a temporary £200,000 extension to our overdraft facility until 1 November 2021 and are currently in discussion with our primary bankers to increase our UK invoice discounting facility and introduce a US invoice discounting facility. We have also renegotiated our covenant on the CBILS facility in light of our investment for growth.

Invoice discounting tends to be the sort of financing of last resort since it is often expensive.

On top of this they are facing supply chain issues:

One of the biggest challenges we have faced during the year has been on the supply side. The supply of components like semiconductors has been affected by various socio-economic factors, not least of which have been freight restrictions due to the global pandemic. Even without that, we have seen enormous price hikes in certain components, and we have limited opportunities to pass that on to the market due to contractual obligations where the price is fixed.

This situation appears likely to continue, which means that our margin will become increasingly squeezed. This further highlights the need for our business strategy to balance capital sales with a subscription model, as that makes margin at the point of sale much less relevant.

So the need to hold higher inventory, sales may be restricted and margins likely to be squeezed further. This sounds like the risk here is very much to the downside.

They do have the option to sell the Safetell business, though. Since there is no synergy between divisions. Service revenue here has been impacted by access issues due to COVID, but the growth in product revenue is good to see:

How much they would get for what is largely a steady but ex-growth business remains to be seen. The bigger problem is that we have little faith that they will use this money wisely. They have been investing heavily in new product development, yet the new Janus C4 appears to be failing to get traction in the market. Sateon Advance revenue halved in the year too. Only the legacy business held up:

This follows the pattern of recent years.

But what about the Net Assets of £8.29m compared to a market cap of £5.27m. Perhaps there is asset value?

Unfortunately, most of their net assets are intangibles, and ones we'd be very dubious about. Also, there is lots of inventory that could get written down, and receivables that might not get paid.

But the most obvious problem here is that market cap of £5m. For a non-growth company, let alone one that includes an unrelated division that should probably be sold, this is just far too low to be listed.

With severe short-term issues and little credibility for the long-term growth story, this remains uninvestable for us.

Fulham Shore (FUL.L) - Trading Update

A very strong trading update:

Since the Group's Final Results announced on 17th August 2021 Group revenues have continued to grow. In the three completed weeks since (up to 5 September 2021), Group revenues for all restaurants have increased 27% compared to the equivalent period in the 2019 calendar year.

Note however that these are not LFL figures. However, it is despite headwinds:

This represents a marked acceleration from the 8% average increase for the eight weeks ended 15 August 2021 announced in the Final Results. The Group's 17 restaurants that are located in the West End of London and city centre office locations, although still down on 2019 levels, have, in these three weeks, continued to see a week-by-week improvement in footfall and revenues as tourists and office workers have started to return.

And it continues to grow:

So far, during the Group's current financial year ending March 2022, we have opened two Franco Manca and, most recently, our 20th The Real Greek in Norwich. This Chantry Place location has opened with strong trading serving an enthusiastic local audience. This takes the total number of restaurants operated by the Group to 75.

Since 17 August 2021, fitting out works have commenced on two new Franco Manca pizzeria, in Blackheath Village and on Baker St in London. 15 more potential sites are in solicitors' hands for both Franco Manca and The Real Greek.

But this is the least of it, in their FY results they said:

From our current base we have identified over 125 more locations for Franco Manca in the UK and 30 more for The Real Greek. With steady expansion in the medium term, this should bring our total estate to over 230 restaurants in the UK. To this end, and supported by the Group's current trading performance, a further 12 sites are in solicitors' hands.

And:

Over the last few years we have fielded many enquiries regarding opening our restaurants outside the UK. The Board has previous experience of successful expansion outside the UK at PizzaExpress and Gourmet Burger Kitchen and has commenced investing in an experienced team to capitalise on the opportunity to establish our brands overseas.

So, despite the lack of LFL figures, it does feel like they've got considerable momentum behind them. They also have some great experience in property with David Page, formerly of Pizza Express. Potentially, conditions to expand could now be very favourable. As they said at the full year:

Analysts believe that the UK restaurant market in terms of numbers of locations in 2022 could have diminished by as much as 20% compared to 2019. This will perhaps mirror the contraction of retail space. Over-expansion, paying ever higher rents that were unsustainable and chasing market share were all to blame.

The CVAs and closures that have ensued across the sector have enabled both of our businesses to obtain sites at favourable rent levels and lower capital cost per site. Rents have halved in some cases, and we have opened some sites for less than £500,000 rather than the average of £650,000 which we were budgeting in 2019. Both these reductions should improve our return on capital over the next few years.

However, we see two particular problems for investors:

High valuation - Current market cap is £113m, but net assets are only £35.5m. That means that the goodwill with brand and landlords and operational expertise is quite highly valued.

Capital structure - They just don't have the finances to expand quickly. From the FY:

It is the Group's intention to re-finance its banking facilities in the second half of the current financial year ahead of March 2022 when one of our facilities will fall for renewal. The Group's bankers, HSBC, continue to be supportive. We have a current combined facilities limit of £24.27m. This is made up of £14.25m revolving credit facility ("RCF"), £9.27m Coronavirus Large Business Interruption Loan ("CLBIL") and £0.75m overdraft facilities…The Group intends to fund its expansion programme thereafter from operating cash flow and the utilisation of its bank facilities.

Does that preclude an equity financing? Or does the "thereafter" imply that they could use equity to help refinance debt? They already raised £2.25m at 6.25p in August 2020. But we can't imagine those institutions being upset if they went on to raise more at, say 12p. They have the motive, means and opportunity to raise more equity and small investors are likely to be largely excluded. Combine that with apparent overvaluation and they look too risky in the short term.

They finished today's statement with:

The Group will hold its AGM on Wednesday, 29th September 2021 at 9.00am. On that day, and because of evolving market conditions, a further trading update will be provided together with a statement on the first six months of our financial year which will have ended on 26th September 2021.

This might be the right time to announce any fund raise.

Cenkos Securities (CNKS.L) – Interim Results

When we looked at the Cenkos following their last set of final results we were distinctly underwhelmed. Despite the strong headlines, there were a number of issues. We said:

H2 corp finance revenue was up from £9m in H1 to £13m. This was slightly less than I expected from the strength of their transactions. Market making exceeded my expectations generating £3m revenue in H2. However, the real problem is that staff costs went up form £7.4m in H to £15.2m in H2

So you have around £7m incremental revenue in H2 but almost £8m incremental staff costs.

The standout figure initially appeared to be the cash, up from £18.3m to £32.7m. But a lot of the cash was due to increase payables of £10m, [the vast majority of which is staff bonuses.]

So this week’s results make for interesting reading:

Corporate finance remains strong dropping to just £12.7m, and execution moderates slightly to £2.4m. So on the revenue side, these are good results. Particularly since our deal tracking showed that they had a quiet few months early in 2021.

Staff costs aren’t as bad as 20H2 coming in at £11.8m. Payables have reduced but not back down to the 20H1 levels but they are much more in line with receivables which have increased slightly too. So it is probably fair to conclude that the £24.0m cash balance is real this time. Not all of this is surplus due to reg cap requirements but thankfully they specifically break this out:

At 30 June 2021, Cenkos had a capital resources surplus of £17.0 million (H1 2020: £15.8 million) above its Pillar 1 regulatory capital requirement.

This works out to be about 31p per share. On an earnings basis, their profit figures work out to be 3.1p EPS for H1.

On the outlook they say:

Since the end of the period, the completion of 2 IPOs and a further 8 fundraisings further demonstrate the ongoing strength of the business and its pipeline. Whilst we cannot always assume favourable conditions within equity markets, by continuing to lay the groundwork for growth and through our tenacity and long-term partnering with clients, we see reasons for optimism for the remainder of 2021 and beyond.

So that is positive. Since we often track these transactions we can say that Cenkos has been one of the more active brokers over the normal summer lull.

H2 is likely to contain bonus payments, and given the big jump in staff costs in 20H2, it is not entirely how they accrue for this. In this case, doubling H1 EPS is probably a good estimate for FY figures. This means that, at 90p today, Cenkos are on a cash-adjusted P/E of 9.5. Sounds pretty cheap, until you compare to the sector, where finnCap are likely to be on a 6-7x P/E, and Numis on a 7-8x P/E, both on a cash-adjusted basis

The market is clearly pricing in significant long-term mean reversion for the sector, and if that’s true Cenkos will not be immune. Both of these competitors are much higher quality businesses, so it is hard to argue that Cenkos deserves that premium rating, too.

They do point out the amount they have returned to shareholders as dividends since inception:

…since being admitted to AIM we have returned the equivalent of 180.8p per share of cash to shareholders.

But a lot of this was in the early years when the company was enjoying much more successful operations. The currently proposed dividend looks a bit miserly compared to both earnings and the cash pile:

The Board proposes an interim dividend of 1.25p (H1:2020 1.0p) per share.

If we follow recent trends we think a final dividend of c.3p could be on the cards, making 4.25p for the full year.

Shareholders are getting a 4.7% yield. This is in line with broker forecasts for finnCap, but we wouldn't be surprised to see this beaten. All things considered, finnCap remains our pick of this sector given its discount and potential for structural growth over the next few years.

That’s it for this week, enjoy your weekend.