Small Caps Live Weekly Summary

KETL NWT PAY PEG POS QUIZ SDI STAF THRU TET TRI TON ZOO

Another week of very strong newsflow, so we dive right in:

Strix (KETL.L) - Pre-close trading update & CFO Appointment

Despite the continued challenging macroeconomic and geopolitical environment, Strix has achieved adjusted profit after tax for the full year of £20.6m on a constant currency and £20.1m on a reported basis.

A small miss on broker Zeus forecasts:

This is broadly in line with Zeus estimates and company guidance of £21.0m. Importantly, the operational performance by the Group, particularly in H2, has resulted in year-end net debt of c. £83.7m (2.15x EBITDA). This is within its debt covenant agreement of 2.5x and better than the Zeus forecast (FY23: £86.9m).

So this trading update is re-assuring on net debt, and it seems the market was wrong to worry about covenants not being met. However, this is a little underwhelming:

Strix is now focussed on delivering future profitable growth and the optimal resources required to achieve this. This will include a new internal reorganisation programme that will help the Group to continue to maximise cash generation and support debt reduction with a clear plan to get net debt / EBITDA to below 1.5x before the end of 2025.

As is the CFO appointment:

Strix is also pleased to announce the appointment of Clare Foster as Chief Financial Officer. Clare has over 25 years of experience working in international businesses, and was most recently the Group Chief Financial Officer at Trifast plc making her a valuable addition to Strix's leadership team.

Although we didn’t rate the previous Strix CFO, appointing someone whose only experience as a listed CFO appears to be presiding over the collapse in profitability at Trifast smacks of desperation.

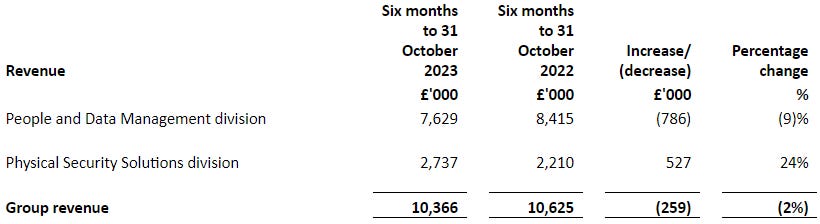

Newmark Security (NWT.L) - Half-Year Report

Poor results here:

· Revenue down 2% to £10.4 million (H1 FY23: £10.6 million)…

· Loss after tax of £0.1 million (H1 FY23 profit: £0.5 million)

· Loss per share of 0.54 pence (H1 FY23: earnings per share of 4.89 pence)

The claim that this would look better if they didn’t lose business:

· Underlying revenue up 11% after stripping out the impact of the anticipated loss of UKG in FY23. Underlying gross profit in H1 FY24 increased by £0.2 million

Well duh! And if this was expected, why didn’t they cut costs to maintain what little profitability they had?

They've been saved from a much worse result by Safetell, the supposedly non-core part of the business, doing well:

How on earth did this go from 50p to 90p in the last couple of months:

It shows the folly of buying into something because it is going up and assuming they know something you don’t. They rarely do.

It is always worrying when a company includes their net assets in the highlights:

Net assets of £8.0 million (31 October 2022: £8.2 million)

They miss out that vast majority of these are intangible:

Companies like this typically trade at a discount to TBV, which is around 12p per share. They claim a better second half is on the way, but their broker, Allenby, are unwilling to make any forecasts for the current FY24, let alone future years, even though there are only 3 months left of this year. Given the large debt compared to the market cap, it is not clear that the equity here has any value in its current format.

Paypoint (PAY.L) - Q3 Trading Update

In line for FY3/2024 :

A positive quarter with PayPoint Group on track to deliver c. £80m of underlying EBITDA, net debt below £70m and underlying PBT in line with expectations for FY24

There are a few positive points, including:

We are in advanced discussions with a number of other major carrier partners about long-term contracts to continue to grow volumes into FY25.

The weak point is the corporate issuance of Love2Shop vouchers. I suspect the earlier surge was down to the end of COVID and an exceptionally tight labour market rather than being sustainable growth and won't be easily fixable:

In Love2shop Business, the number of retained clients was up 6% but order values were down, resulting in weaker billings than expected in December and reflecting the broader caution from large businesses and the overall challenging economic situation. We have proactive and focused plans in place to end the year strongly.

The detailed breakdown reconfirms that the real-term falls in overall LFLs hide significant growth in new business amongst the falls in energy prices and removal of the support scheme.

The big falls in debt aren't forecast until FY3/2026, but if that direction of travel continues to be forecast then investors have no need to worry about it and can focus on the EPS and DPS. FY2025 is forecast at 72.6p and 42.0p respectively, which could easily support a share price of 726p (a P/E of 10x) and still give a 5.7% yield. If growth accelerates then even Liberum's 1100p target could be achieved in a reasonable period.

Petards (PEG.L) - Trading Update

Misses all round:

Revenues for FY23 are likely to be around 3% lower than market expectations which will have an effect on the FY23 reported results.

Some may have expected worse, though, because there was a forced seller here recently that only got 2.5p for their shares. The cash balance is reassuring, at least on a pro forma basis:

Total net funds¹ at 31 December 2023 of £1.2 million with no bank debt (FY22: £1.7 million)…

Cash balances were slightly below the Board's expectations, due to a customer payment of £0.3 million expected pre-year end but not being received until 2 January 2024.

They look very cheap on FY24 forecasts, given the cash balance, but this week’s news introduces significant extra doubt that they will be met. It is largely academic, though, as this stock is so illiquid it barely trades.

Plexus Holdings (POS.L) - Update & Overview of Licensing Deals

This is an RNS Reach, so really just an attempt to explain recent news rather than material changes to trading. We do note, however:

The Licence Agreement fee provides Plexus with a US$5.2m cash lump sum, which will be used in part to build new inventory for the Company's historical core jack up exploration rental wellhead and associated mudline hanger sales business, which is a sector Plexus has re-entered in co-operation with SLB.

We suspect this has been communicated before, but we’d not picked up on it. This is largely a rental business and, hence, fairly capital-intensive. The point is that there should be a big valuation difference between a rental business with some interesting tech and a tech business that sells licenses for IP. Rental businesses tend to be valued on Tangible Book Value.

Hmmm.

Quiz Clothing (QUIZ.L) - Christmas Trading Update

As a reminder, net cash on 30th September was £3.5m, and on 4th December, it was £0.9m. An update to that figure isn't directly given but it appears to be £1.4m as of yesterday. Calculated as 2.0 - (4.0-3.4) from the numbers below:

As at 22 January 2024, the Group had total liquidity headroom of £5.4 million, being a cash balance of £2.0 million and £3.4 million of undrawn bank facilities (31 March 2023: £8.3 million, being cash net of borrowings of £6.2 million and £2.1 million of unutilised bank facilities). The Group's £4.0m of bank facilities available will expire in June 2024.

It appears they drew down more of the bank facility so perhaps at some point over Christmas they were net debt. Apart from any quarterly rent, now is likely to be close to the cyclical high point. All credit card payments for Christmas and the bulk for January sales will have been received as cash, but salaries for January and any monthly rent will not have been paid.

The good news is that results are in line with current market expectations, but given that these are for ongoing losses, the weak cash and the lack of progress on debt refinancing or the strategic review should be the focus.

SDI (SDI.L) - CEO Change

When the new COO was appointed, we commented that Mike Creedon looked to be on his way out, and the COO sounded like the CEO designate. And so it turns out:

Stephen Brown, previously SDI's COO, succeeds Mike as CEO. Stephen joined the Group, and the Board, as COO in September 2023.

It also explains why Creedon was unwilling to buy back any of his shareholding that he completely sold, despite the share price collapsing since. He was thanked, but the “with immediate effect” sounds like he may not have had a lot of choice in the matter. It may just be that his heart wasn't in it anymore.

The implication of his leaving is that trading is not going well. The company could have taken the opportunity to re-assure on trading but did not. It seems academic, though; the valuation is looking very stretched even if they meet expectations.

Staffline (STAF.L) - Trading Update

Trading was resilient in the core recruitment business, as we expected. As ever, the problems are mainly with PeoplePlus, which we have consistently described as a terrible business:

In PeoplePlus, political uncertainty, low levels of unemployment and the impact of new contract revenue streams only flowing from 2025/6, will reduce short term profitability by around two thirds, in 2024, versus expectations.

The good news is that it is being progressively shut down:

The division is, however, now transformed with a more efficient cost base and new management, focusing on its two core markets, Justice and Employability, where it has good market share and strong prospects.

As a result of the PeoplePlus outlook being even worse than expected, Zeus say:

Our estimates for FY24 underlying EBIT and underlying diluted EPS decrease by 24.8% and 29.2%, respectively

Going back to the current year, the new guided profitability is actually 5% below Zeus, even ignoring £1.8m of previously unexpected restructuring charges. Understandably, the company chooses to focus on the cash:

Net cash (pre-IFRS 16) of £3.8m (2022: £5.0m), ahead of market expectations by £6.8m; strong trading cashflow supported £5m share buyback programme during FY 2023

We don't think the cash beat is material, and some of it will come from the revenue miss. Compared to more conservative forecasts from Liberum, 2023 profitability is a beat, thus the claim to be in line with consensus. The gap in optimism between Staffline's joint brokers widens further for FY 2025 at 4.0p versus 5.2p. The relatively minor share price reaction to some big downgrades underscores how low expectations were here and that the shares remain cheap.

Thruvision (THRU.L) - Sales Progress Update

It seems strange to issue this RNS now. This doesn't fit into the normal pattern of Thruvision updates, being neither a scheduled trading update, which occurs at the start of April, nor a major contract win affecting forecasts:

These orders total £1.3 million, all of which is expected to be delivered in the second half of the Group's financial year.

This makes it sound like they are currently in H1, which they are not since the year-end is March. Guidance with the H1 results was for £4.6m in H2, so this is material but not massive like US Customs orders have been.

These recent wins, together with our current sales pipeline, underpins our confidence in meeting our full-year revenue expectations.

Our normal assumption would be that a placing was on the way which they are trying to shore up. But they raised very recently. Maybe they think the share price indicates the market fears a miss, and they wanted to reassure. Perhaps they have decided this is a good time of year to update going forward? But they deliberately did not title this as a trading update.

Progressive keep their forecasts, although these are the ones that were slashed in September last year, and they are not brave enough to even think about next year's trading. The forecasts they are hitting look unimpressive, with revenue and profits going backwards:

You’d think they wouldn’t want to highlight this!

Treatt (TET.L) - AGM Trading Update

As one regular contributor points out, vague but positive is the remit of an interim CEO suffering from difficult end markets. An interim CEO, who might well be auditioning for the permanent role, would not endear himself to the rest of the board by downgrading, nor misleading investors. Which means this week’s outlook statement looks like this:

We continue to focus on cash generation and we are on track for further improvement in net debt during the course of the year in line with management's expectations.

Whilst we are mindful of ongoing macroeconomic pressures, we are encouraged by current trading, underpinning our confidence in our trading performance for the year ahead.

So, net debt is in line, but it is less clear that revenue and profits are. Even if they meet forecasts, these are for single-digit revenue and EPS growth, meaning that the company trades on 21x Forward P/E.

It is tempting to think that with these metrics, whoever the new CEO is, they are in for a big share price fall either way. However, this company is so loved by private investors that the CEO could intentionally run over a shareholder's dog, and they’d thank him for it. As SDI has shown recently, this sort of love-in rarely lasts through a few trading disappointments, though.

Trifast (TRI.L) - Trading Update

Here's the good news:

we predict to effectively reduce leverage below 1.5x and Group net debt to be below our target of £25m.

However, some of this may be working capital unwinding and so consideration should be given to whether their ability to bounce back will be impaired by a lack of capital.

Here is the bad news:

Disappointingly, performance in December 2023 was impacted by significantly lower than forecasted volumes in both our Asia operations and global distribution sales channel. Whilst we had anticipated both of these areas to see a recovery from subdued activity in H1, demand conditions and excess customer inventory levels have pushed this recovery further into 2024 and we now expect these challenging conditions to persist through to the end of the financial year.

The bottom line from Zeus for 2024 is:

a c. 45% decline in PBT to £6.0m.

Shareholders following their historical performance less closely would be forgiven for being surprised how much a single month's weakness could affect results for FY2024 and FY2025:

This reduces profitability by 37.5% and 39.2% to £10.1m and £13.2m in each year, respectively.

Still, the thesis now must be that new management have now kitchen-sinked results and brought forward cost cutting. But why did it take them so long? This will also be a blow to Rockwood Strategic and its portfolio of similar turnarounds, such as Flowtech Fluidpower and Titon. Speaking of which…

Titon (TON.L) - Annual Financial Report

Oh dear:

Then there is the outlook:

· Operating profit in the first quarter of the current financial year to 30 September 2024 in UK and Europe was in line with the Board's expectations, but sales were lower than Q1 FY23, reflecting a slowdown in the new build market, with profit performance mitigated by an improved gross margin and careful management of overheads.

· We anticipate that the macro-economic backdrop in our UK and European markets will continue to be uncertain and challenging in 2024 and that consumer demand for home improvements will remain subdued.

· We do not expect that trading in South Korea will materially improve in 2024. However, we are working to streamline the corporate structure and operations which will reduce costs.

The risk is that Rockwood may have taken over the mantle from the dearly departing Downing Strategic as the owner of businesses that take longer than they anticipate to turn things around. Although to be fair, they have only just started to change the management team here. It does seem that the investors who bought into this business simply because of Rockwood’s involvement may have underestimated the turnaround required.

Zoo Digital (ZOO.L) - Trading Update

A further profits warning, here:

However, it is now clear that the completion of entertainment products is taking longer than expected. This will result in Q4 revenue being significantly lower than anticipated leading to a greater loss than previously expected for the full year.

We had previously commented that it did seem wildly optimistic to assume that the pipeline of work would suddenly appear as soon as the writer/actor strikes ended, which it appears it didn’t. Good news on the orders to enable profitability in 2025, though:

The pipeline is consistent with current market expectations for FY25 and a return to profitability.

They still have net cash:

On 31 December 2023, the Group had net cash of $8.9 million and expects to maintain a positive balance with unused debt facilities available at the March year-end and an improving cash balance in the first half of FY25 due to the recommencement of orders.

However, broker Singer are expecting further significant cash outflow before year end:

FY24 results are expected to be significantly below expectations and ZOO will no longer be breakeven in Q4. While a return to profitability is expected in FY25, we downgrade FY24 Net Cash to $1.5m (from $6.6m) but highlight ZOO has c.$5.25m in unused debt facility available.

It looks like they won’t be able to afford the Japanese acquisition they raised money for anytime soon, and uncertainty over the 2025 outturn remains:

The Board expects further clarity on the timing of projects and therefore revenue for the rest of the year in the coming weeks and will update the market further as necessary in due course.

However, they have proven to be overly optimistic about these things in the recent past. The reliance on orders from a single customer should be ringing alarm bells as well. As the last Annual Report says:

Customer concentration reduced during the period with the revenue contribution from our largest client falling slightly to 74% of sales (FY22: 78%)

It is perhaps not the board and the shareholders who control this company.

That’s it for this week. Have a great weekend!

I hope we don't have to wait too long to get an update from a UK smallcap that makes watching the sector anything other than a waste of time.