Small Caps Live Weekly Summary

CAU DLAR NXQ VANL

This summer has been quite brutal for many small caps. It may just be illiquidity, but the enthusiasm of a few months ago seems to have given way to a more pessimistic market. Companies trading in line are no longer bought but sold. In some cases, this is because the shares have risen too fast, too soon, driven up by short-term traders who exit as soon as the price stops rising. However, we are also seeing a number of unexpected profit warnings, with company management struggling to explain why the demand for their products has been so weak. Although the headlines are reporting decent GDP growth in the UK, the recovery appears to be patchy, making navigating these markets particularly tricky.

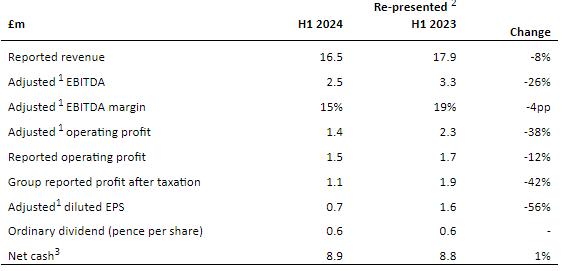

Centaur Media (CAU.L) - H1 Results

This is another set of poor figures:

They suggest we should be expecting a H2-weighting:

The investments will gather pace in H2 2024 with accelerated product development rolling-out in The Lawyer, MW Mini MBA and Marketing Week, as well as implementing new capabilities for customer-centric product innovation across the Group

And...

I am pleased that our future growth drivers, MW Mini MBA, Marketing Week subscriptions and The Lawyer have performed well, although the Xeim H1 performance in some parts of Econsultancy and Oystercatchers has been negatively impacted by sector headwinds. This reinforces the importance of our investment in insight and learning expertise. With the greater weighting of revenue in H2, we expect to return to growth in the second half of 2024 and look forward to driving the delivery of our BIG27 strategy over the next four years.

However, their broker Singer confirms this is the profit warning that it sounds like. And a significant multi-year one:

We update FY24 revenue from £39.0m to £36.0m to reflect a partial recovery in H2, as the April Mini MBA course sees some revenues recognised in H2, and the Festival of Marketing has all of its revenues in the half. Meanwhile EBITDA moves from £10.0m to £7.1m to reflect this slower top line and also higher investment. We see this investment continuing into FY25, as the group continues to improve its offering to attract more subscribers and enhance its upsell and cross-sell opportunities. We see this culminating in stronger returns, FY26 onwards.

It would have been nice if they had explicitly said this, rather than making the broker break the bad news. EV/EBITDA is now 5.6x on the revised forecasts, so it's not bonkers but not bonkers cheap either, making it tricky to know how to react to this disappointment.

De La Rue (DLAR.L) - Full Year Results

Bad results are one thing, but when combined with debt and a huge pension black hole, this is nothing short of disastrous. Here we have here with revenue, profits/losses falling and net debt rising:

The going concern statement is qualified. The biggest problem is that the RCF expires, and it seems that banks are not keen to renew it:

The Group's Revolving Credit Facility (RCF) expires on 1 July 2025. The cash flow forecasts for the Group indicate that it would not have sufficient liquidity to meet the obligation to repay the RCF on or before 1 July 2025. As detailed in the Chairman's statement, various strategic options are being pursued which would allow the Group to repay the RCF on or before 1 July 2025. The most progressed of those is the sale of the Authentication division.

The solution they have come up with is to sell the Authentication division, but are entertaining offers for both operating divisions. The scale of the pension deficit seems to be unknown as the Annual reports don’t mention the triennial valuation. What is known is that the company has agreed to pay around £121m of recovery payments until 2029, although it has deferred some of these to later years because they can’t afford them in the short term. Also, the scheme will not have been a significant beneficiary of higher rates due to the presence of LDI assets. In 2020, the deficit was £190m, and the asset performance has been relatively weak since then.

Pension Trustees are notoriously jumpy when it comes to agreeing asset sales. Since this leaves them exposed, they could easily demand the lion’s share of any asset sales. Between the deficit and the debt, the company will probably need to generate £300m+ after costs from selling the divisions for shareholders to see any return whatsoever and £500m+ for them to make a profit on the current buy price for the shares.

Nexteq (NXQ.L) - Trading Update & Board Changes

Horrible profits warning here:

FY24 revenues 15%-20% below market expectations.

Leading to:

adjusted profit before tax to be 30%-40% below market expectations

Apart from the persistent seller over the last couple of months and the usual reliance on H2 weighting, we are not sure there were any obvious signs here. Blame is put on destocking, plus:

…some specific larger key Quixant customers have recently indicated lower demand, partly reflecting the timing of new product releases and challenges in specific regional markets.

However, it is Densitron that faces the largest fall in sales:

Within the Group's brands, we expect to report that Quixant revenue is down 10% to $30.9m (H1 2023: $34.3m) and Densitron revenue down 22% to $17.3m (H1 2023: $22.0m).

They do say:

Pleasingly, the robust gross margin performance seen in 2023 has continued into 2024 at record levels, ahead of that achieved in FY 2023, benefitting from customer and product mix and the ongoing focus on higher quality revenues. This increased gross margin coupled with effective cost management ensured that the Group continues to operate at double-digit adjusted profit before tax margins.

But we wonder if this is part of the problem. They significantly raised operating margins in Densitron in 23H2 by raising prices. Fewer customer orders may be the delayed reaction to this change. Part of this may be intentional, and they are doing the right thing of prioritising gross profit over volume, but then they probably have their sums wrong if it has cost them a 40% drop in PBT expectations.

This is followed by the news that the Chair, CEO & CFO are all leaving:

Francis Small (Non-Executive Chair), Jon Jayal (Chief Executive Officer) and Johan Olivier (Chief Financial Officer) have informed the Board that they will step down from the Board and leave the Group in the coming months. Francis, Jon and Johan intend to continue in their roles until successors have been identified and to facilitate an orderly handover.

We can’t remember another company where almost the entire board leaves at the same time. Nick Jarmany, founding Director and Deputy Chair, is likely to step up in the short term to lead the quite extensive executive search required.

Understandably, the share price took a large hit. So big that the asset value may be providing support. We make it £50.6m NTAV = $82.3m Net Assets - $14.2 intangibles - $3.0m deferred tax assets / 1.289 FX / 66,360,788 shares = 76.3p.

They have added $9m cash since year-end = 10.5p/share, but they say:

The Group generated healthy cash flows in the first half with net cash at 30 June 2024 of $36.9m (31 December 2023: $27.9m), with positive working capital movements as stock levels reduced and strong cash collections continued.

Which sounds like it was mainly working capital rather than trading profits. So we can’t just add this together. Their broker, Cavendish is forecasting NTAV to be around 80p at year end. They also have 11c of EPS forecast, which would still put the company on a P/E of around 5 after adjusting for the cash balance.

It is tempting to think that this makes the shares a buy. However, history tells us that the first cut in EPS following a profits warning often doesn’t reflect the new reality. Not least because an incoming management team is incentivised to kitchen sink everything first. It will be some time before the new management can make productive use of that cash as well.

This company was one of Simon Thompson’s “Bargain Shares” for 2024, and many SCLers successfully traded this, selling into the spike that tip generated. Writing following this update, tellingly, Thompson only appears to have been able to muster a hold recommendation, not a buy. Nor did the price respond to this, suggesting the institutional seller is still going.

As such, despite possible undervaluation, it seems that the share price will likely bottom some way below the current price, and the recovery will be slow and patchy due to the management overhaul.

Van Elle (VANL.L) - Final Results

Revenue is down, but EBITDA is up; this doesn’t make its way through to operating profits, though, due to increased depreciation:

Then, higher tax rates mean that EPS is down a fair amount. This is explained as:

The effective tax rate in the year is 25.1% (2023: 12.9%). The increased effective tax rate in the current financial year is as a result of the change in corporation tax rate from 19% to 25% in April 2023 and the cessation of the super capital allowances scheme in March 2023. The Group benefitted from super capital allowances in the previous financial year resulting in an effective tax rate lower than the corporation tax rate applicable at the time.

Broker Zeus says this is ahead of their estimates, though. The market didn’t like this update. The outlook said that they expect challenging markets to continue in the short term, but the order book is growing. Given that the shares had been strong into this update, perhaps some shareholders had priced in a faster recovery. However, for those willing to look further ahead, there is significant potential. The shares still trade at a discount to TBV. This week, Progressive initiated coverage of the company, and they say:

The share price is currently 14% below its current year high of 43p. On a PER basis, it is trading at 8.7x FY25E, falling to 6.0x our FY27E estimate (which we believe to be conservative). The FY25E dividend yield is 3.5%, rising to 4.9% in FY27E. Strong forecast cash generation indicates EV/EBITDA should fall to 1.3x, based on our estimates(page 24). Ground engineering and foundations are the earliest stages in construction –and especially required in the UK’s national priority sectors of housebuilding, water and power infrastructure.

We take anything that forecasts out to 2027 with a massive pinch of salt. Especially from paid-for research. However, the possibility of an EV/EBITDA of 1.3 on stated conservative forecasts shows why Rockwood/Harwood is interested here.

That’s it for this week. Have a great weekend!