Small Caps Live Weekly Summary

HOME SUP CRL TRD D4T4 KETL

Calmer markets this week. Perhaps, unfortunately, as many smaller cap companies failed to join in the large cap tech rally in the US. However, you don’t buy small cap companies because you want to closet trade interest futures. You do so because you believe you can gain an informational or analytic edge on the market. As always, our small cap analysis is focused on this endeavour.

Large Caps Live

This week, on LCL, WayneJ looked at the allegations made in a note from Viceroy Research about Home REIT. He found some of the Viceroy concerns may be due to misunderstanding, however, he did have concerns with the structure of Home REIT, and, indeed, the rest of the social housing sector. Here is his summary:

The Home REIT model is to rent out to charities on 20 - 30 year upward only rents with a cap and collar of 1% - 4%. The Charities are unlikely to have contracts of matching duration with local councils.

According to their own documents, they buy from developers who are required to ensure that the charities are funded for a year - this raises questions of 'round tripping.'

By their own documents, it appears that the rent increases may be higher than open-market rents.

By their own documents, they state that the charities get 2.25x more rent than is paid to Home REIT to allow for insurance, maintenance and mentoring etc. Yet, in the comparisons of value for money, they compare the rent that Home REIT charges with the rent of Bed and Breakfast and NOT with the rent charged by other local social rent providers or open market rents. And Viceroy has raised issues on the financial viability of some of the charities.

It appears that they may capitalise the rent growth to derive the current NAV though this is not entirely clear. If it is capitalised, then there are questions about the valuations.

The management team apparently visit each property (2,308 properties / 11,100 rooms) each year to check on suitable maintenance - but there is nothing to suggest that the team has the relevant qualifications or experience to do this.

The management team is able to do this - but Knight Frank, who one might consider has relevant experience, was not allowed to inspect the buildings internally for valuation purposes.

The Chairwoman is the CFO of a student accommodation company. The chair of the audit committee is also the chair of the audit committee of a student accommodation company. And I have long had issues with how student accommodation is also valued ‘from model'.

Small Caps

Supreme (SUP.L) - Half-year Results

The Group has made a positive start to H2 2023 and is now expected to trade ahead of expectations for FY 2023, driven by the incremental EBITDA from acquisitions and further gains in the core business.

This momentum of course, comes from vaping, which is now their strategic focus:

Our Vaping division delivered an exceptional performance in the Period, underpinned by a combination of strong organic and acquisitive growth. Revenues grew to £31.8 million (H1 2022: £21.7 million), a substantial increase of 47%, whilst the division's growth profit margin has marginally reduced to 38% (H1 2022: 41%) owing to changes in sales mix, with consumers purchasing a higher proportion of disposables and pods sourced from the Far East where margins are lower.

Leo has researched this, and pods basically combine the juice and heating element in a cartridge avoiding maintenance problems and allowing an instant refill. I would imagine they appeal to adults out of the house. Disposables particularly appeal to children. The gross margin is a bit of a red herring here as the cost per vape is higher than true refillables and so is the gross profit.

They don't provide like-for-like figures, but sales are up £3.55m, and they say the acquisitions of Liberty Flights and Cuts Ice contributed £3.4m of that revenue growth.

So organic growth was approx £0.15m. Or negative in real terms.

While vaping is now almost half of sales and is set to be over half in H2, historically, lighting sales would account for around a quarter of current revenues. However, this has been hit by what they describe as "overstocking". I think many investors are sceptical about this as it is difficult to see where the consumer demand is coming from for what is now a mature product with lifetimes approaching ten years. Still, they claim to see signs of recovery and expect sales to return to previous levels:

Lighting category now stabilising, with early signs of recovery in retail sales, likely to be reflected in FY 2024 orders

Shareholders will be pleased with an ahead statement. However, when your broker consensus trend looks like this:

Then it is easy to beat. Strangely, the brokers appear to have cut EPS. And for 2024 too. With a share price of around £1, then this is 10x P/E on 2024 estimates once you adjust for their small amount of debt. So not that expensive. However, not cheap either for a company where revenue is only growing by acquisition, and it is facing increasing regulatory scrutiny of its main products.

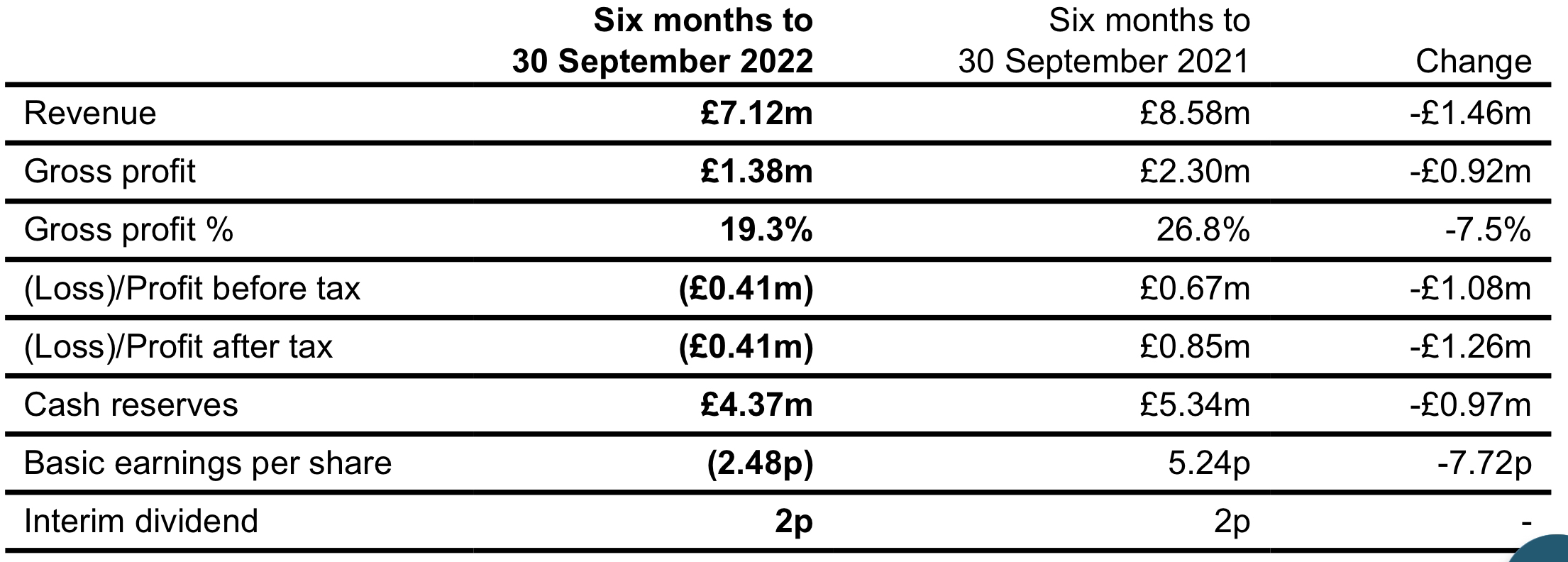

Creightons (CRL.L) - Half-year Report

With no brokers’ forecasts in place, a few scl contributors were estimating their expected EPS for the half-year. These came in at a range of 1-2p. So it is fair to say that this was somewhat of a disappointment:

The diluted earnings per share was negative 0.48p (2021: 2.61p).

This included some exceptionals, but the net result means they only just scraped into positive territory. The inability to pass on costs has done the damage, with gross margins dropping:

The gross margin averaged 40.4% (2021: 42.7%) reflecting the ongoing struggle to pass on significant direct cost increases to retailers, contract customers and consumers. We anticipate that selling price improvement now agreed will help the gross margin continue on the upward trend evident in recent months.

This is despite an increased proportion of higher-margin branded sales. This is partly because they had to stop supplying three major branded customers in the contract division due to customer credit lines not being granted. Operationally, they appear to have been very good at taking costs out. However, these gains tend to be of a more one-off nature rather than a continuous source of increased margin.

Going into these results, we were also concerned that they had ramped up their net debt into a downturn and that inventories looked stubbornly high particularly finished goods inventory.

Net short-term borrowings (cash and cash equivalents less short-term element of obligations under finance leases and borrowings) at 30 September 2022 were £4.7m (2021: £2.9m). This included the final payment for Emma Hardie Ltd of £1.4m and a share buyback of £0.6m.

You’d expect they would want to keep quiet about that share buyback that they executed close to the top of the market! However, looking forward, the going concern statement is re-assuring:

The directors are pleased to report that the Group continues to meet its debt obligations and expects to operate comfortably within its available borrowing facilities. The Group's cash on hand at 30 November 2022 is negative £2.4m. We have carried out a review of our cash requirements for the next 12 months…have therefore formed a judgement, at the time of approving the financial statements, that there is a reasonable expectation that the Group has adequate resources to continue in operational existence for the foreseeable future being at least twelve months from the date of this report.

The short-term debt of £2.4m on 30th November is down from £4.7m at 30th September. So good news on recent cash flow, but the following suggests that they were delaying restructuring and inventory purchases because of concerns over cash:

Similarly for cash flow, large negatives in the early months of the year have been reduced to a positive cash flow in November with positives expected in the future months of this financial year and beyond. The positive cashflow has been enabled by the realignment of buying and stock holding policy together with cost reduction measures.

So cash may have been tighter than they are letting on. However, they do have a breakdown of their debt facilities and the headroom they now have on their receivables facility, which is re-assuring:

The Group has access to cash by way of an invoicing finance facility that is currently in place and could support the cash position by up to a further £4.4m.

Inventories remain stubbornly high, however:

On the PI World management call, they said this was split around 50-50 between raw materials and finished goods. They are targeting four weeks of each, but it is clear they are way over that for both at the moment. On the call, they also said they had dropped about 75 branded lines. So these inventories are after selling on the obsolete stock.

In terms of outlook, they say:

We expect to hold our sales levels for the next six months before we start to build steadily again on a profitable business.

On the call, Mark is sure that Pippa Clarke included the word “broadly” in there, which experienced investors know means “slightly below”. What is clear is that the full-year results are also likely to be unimpressive. They still haven’t passed on all cost increases, although they are now getting close and threatening non-supply to those customers who won’t accept the new pricing. However, given that they have acquired revenue too, and passed on most of the costs, volumes will be down around 20% LFL.

It will take much longer for them to return to volume growth. However, if they hit their published targets for FY24, they could look cheap on earnings again.

The management call gave Leo confidence that this is now looking good value following the recent falls. Mark is less convinced - the H2 results are not likely to be great, and without news or broker forecasts anytime soon, the price could easily drift further. The market is not exactly short of investment candidates that will look cheap if they manage to pass on cost inflation, and the consumer outlook looks much better in 2024. Their strong long-term track record may make them a more interesting proposition at some point in the future though.

Triad (TRD.L) - Half-year Report

Triad head back into a loss for the half-year:

This is a stock whose price rose from around 40p to £1.60 during the cryptomania on the basis that they started to explore doing blockchain work. As far as we could tell, this enthusiasm for the crypto world never delivered any significant revenue and may well have been entirely limited to them hiring a man who’d written the word “blockchain” on his CV. Their strategic partner Stratis Group Ltd was filing micro-entity accounts without an income statement.

Unsurprisingly, the word “blockchain” or their “strategic partner” Stratis are not mentioned in these results. What is surprising is that this company hasn’t completed its round-trip back to a 40p share price! Net assets are just over £5m, and as a small recruiter/outsourcing company, a small premium to this is perhaps the most reasonable valuation. So with a £16.6m market cap, even after the 20% drop in response to these results, logic dictates that they have a long way to fall, particularly now that the crypto bubble has burst elsewhere.

What may be helping it levitate is the dividend is maintained. 2p for the half-year implies that they will maintain 6p for the full year. And why not, given that they still hold over £4m of cash. While it is better than them simply sitting on the cash pile, as they did for many years, an uncovered dividend can’t be maintained forever.

The outlook for the second half is pretty strong:

I am also delighted to say that the beginning of our second half year has seen a strong upturn in levels of new business wins and bidding activity.

But there is still a lot of sales work to do for a low GM business to turn that H1 loss into anything but a loss for the FY, and with no forecasts, this should be the central case assumption, in our opinion.

D4T4 Solutions (D4T4.L) - Half-year Results

A loss-making half, as the lack of one-off license sales, impacts their revenue. However, this is in line with their recent trading statement, so it shouldn’t be a surprise to the market. The good news is that ARR now makes up a good chunk of their revenue, and they are confident of hitting market expectations. The bad news is that the Gross margin has dropped significantly. Part of this is the revenue mix;

Own-IP license revenue, which is high margin, was down to £1.0m (H1 FY22: £1.8m). License revenue is recognised for the full year in the month of sale or renewal, so the lower number for the current period simply reflects the lower level of new sales and the multi-year renewals achieved in the period. Conversely, the third-party products revenue, which is low margin, was higher at £1.9m (H1 FY22: £0.7m).

Doing the maths, if we make the most generous assumptions that licensing is 100% GM and 3rd Party 0%, then their own products’ GM has fallen from 44% to 40%. Not the end of the world, but not what you’d really want to see from a software business, either.

These are the forecasts:

So they think they will do £20m in H2. Normally we would be calling this out as daft. However, they have hit this massive H2 weighting in the past. Part of this will be the timing of booking ARR business, but this shows how reliant they still are on 1-off license sales, despite trying to become a fully ARR business over the last few years.

The cash balance is up significantly, but due to upfront license payments rather than trading profits. This is one of the strengths of their model, though: they get paid a lot of cash upfront. And they are not shy about using it to buy back shares either, which helps support the price.

This, plus the confidence the market has that a big H2 weighting isn’t a closet profit warning, means that the market is unmoved by these results. Perhaps also helped by the announcement of a contract wins:

The first contract, a new three-year Enterprise License Agreement, converts many of the subsidiaries and divisions from perpetual licenses to term licenses

So not a win then, but a renewal. However, it does have more characteristics of a win than many renewals you see reported as wins on the RNS feed - they were previously running an older version and could have stuck with that indefinitely, presumably paying the annual support fees. Instead, they have chosen to upgrade to the latest version, paying a license fee, initially agreed for three years. How that fee is different to the old support fee is unknown, but D4T4 imply that the main ARR uplift will come from greater use, not the different contractual arrangements:

...allows the bank to expand the platform to new markets easily, thereby increasing the ARR of D4t4.

And the second contract win is pretty much with the same customer, so is it really a different contract? They say it is with a different division, but it seems a bit of a coincidence both were announced at the same time. The good news, however, is that it is for their new(ish) FDP product which appears to have been struggling to gain traction.

The two contracts have a combined total contract value of USD 6.0 million and incremental Annual Recurring Revenue of USD 0.6 million per annum.

So is that ARR on top of the $6m or part of it? Either way, they seem to be struggling with their stated goal of shifting to recurring revenues. Even if they hit their full-year targets, they are on a P/E of 30, so this will only attract those that believe those recurring revenues really can be delivered eventually.

Strix Group (KETL.L) - Completion of Acquisition and Trading Update

Another profit warning here:

As a result of lockdown situations as described above and continued macroeconomic and geopolitical uncertainty, not only in China but across a number of its key export markets it now anticipates adjusted profit after tax for the full year to be approximately £23m.

Stockopedia had £28.7m forecast, so the initial 25% fall in share price is in the same ballpark as the drop in profit expectations. More worryingly, though:

The Board recognises that these uncertainties could continue into 2023.

So the 2023 numbers look out of date too. Here’s how Equity Development reacted to this news:

So they take a similar chunk out of 2023E, which is perhaps how the share price ended up down almost 40% by the end of the day. However, they are now just below where there were trading in mid-October, although many small caps bounced on no news since then. However, the company is still profitable and has a high market share in a niche business and looks relatively cheaply rated if you believe the new Equity Development numbers.

They do have debt, and as the share price falls, it makes up a greater proportion of the capital structure. This has helped them maintain an excellent ROE over the years, but it also adds risk in these more difficult times. The current ratio at the last balance sheet date was over two, so there are unlikely to be any immediate insolvency concerns. The vast majority of the debt is long-term. And they are still profitable, so covenants are unlikely to need waiving.

The risk, of course, is that the China situation gets worse before it gets better.

That’s it for this week, have a great weekend.

Intersting names. Worth noting that all supreme divisions ex lighting have organic growth so that should fix itself soon.