Small Caps Live Weekly Summary

CAPD D4T4 EQLS HFD SCE WIX

It was a surprisingly quiet week for small cap news amongst the shares we tend to follow. And a strange week as well, since positive sentiment appears to have returned to at least some sections of UK small caps. The trigger appears to have been a strong positive reaction in the US markets to comments made by the FED chairman. Of course, it is slightly bonkers that these words should have a big impact on UK small caps, but then, in the short term, it is only investor fund flows that matter, and here it is sentiment that matters most. The other strange thing is that some of the biggest moves of the week are on no news. As frustrating as this can be if you don’t happen to hold this week’s investor favourite, it is better than the slow grind down in everything!

A lot of UK small cap investors, including many SCL contributors, are looking forward to attending the Mello London investing conference at the end of the month. Use code ML40X for 40% off.

In other news, the Value Trapped Podcast that Mark co-hosts has gained a a new co-host. Bruce has taken a sabbatical due to travel and work commitments, but Graham Neary has very kindly agreed to step in and discuss all things value. Here is a short clip from the latest episode:

Value Trapped is a premium podcast where listeners can subscribe here for a small monthly fee. For those not ready for the premium feed, there are a lot of great free investing podcast episodes on the Fund Your Retirement Platform. Check out them on the YouTube channel or on Spotify or other popular podcast platforms.

Here is what we did take a look at this week on SCL:

Capital Limited (CAPD.L) - Chrysos Corporation, Barrick Gold & MSALABS Partnership

MSALABS is pleased to announce that it has forged a partnership with one of the world's largest gold miners, Barrick Gold, and Chrysos Corporation (Chrysos), to deliver PhotonAssay™ technology to Barrick mine sites across four continents.

This is perhaps unsurprising as:

The partnership is an extension of an already successful relationship between the three companies at Barrick's Bulyanhulu mine in Tanzania and its Kibali operations in the Democratic Republic of the Congo (DRC).

Nor is the extended partnership starting where Capital have recently won a major drilling contract:

The partnership will commence with the deployment of three MSALABS contracted PhotonAssayTM units to the Nevada Gold Mines (NGM) complex in the United States of America (USA), with the potential deployment of up to 10 more PhotonAssayTM units to other Barrick projects by the end of 2025, subject to finalising due diligence.

Unsurprisingly, the market liked this announcement, with the Capital shares rising 5%. However, this adds just £8m to the market cap versus the £53m that Australian-listed Chrysos’s market cap increased on the same news. Of course, Chrysos are the IP owner. However, we doubt the economics of the deal are stacked anywhere near as favourably towards Chrysos as these numbers suggest, not least because Chrysos have committed to providing the majority of the capex for deployment.

D4T4 Solutions (D4T4.L) - Trading Update

They guide in line for both the half-year and full-year:

Results are expected to be in line with management expectations, with revenues of approximately £13.0 million (H1 FY23: £8.1 million) and adjusted profit before tax2 of approximately £0.2 million (H1 FY23: loss of £1.3 million).

The revenue growth is impressive, even if the absolute PBT is negligible. However, they were aided by some delayed orders from last year:

…the outcome was also assisted by the revenues related to the delays in contract signings at the previous year end, which were signed during this period.

These appear to be low-margin pass-through orders, as £4.9m incremental revenue has generated just £1.5m incremental PBT. finnCap are forecasting £5.3m PBT for the full year, so, as always, there is a massive H2 weighting if they are to deliver. Cavendish are keen to point out that this isn’t unusual:

Although they are a company where the broker forecasts are continually downgraded over time:

Even if they do hit these estimates, it still leaves the EPS below 2019 levels. Next year Rodney, next year…

Equals (EQLS.L) - Response to market speculation

…is conducting a review of the Company's strategic options. As part of this process, the Company has contacted a limited number of potential counterparties including Fleetcor Europe Limited and Madison Dearborn Partners, LLC to assess whether such parties could put forward a proposal that would deliver greater value to Equals' shareholders than pursuing a standalone independent strategy. Any such proposal could include an offer for the entire issued and to be issued share capital of the Company.

The strange thing here is that we haven’t been able to find any speculation prior to this announcement. They wouldn’t be the first company to make this sort of announcement to get the share price up as a bargaining tool rather than being forced to make a disclosure due to a press article or similar.

The risk is that if they don't get an offer, then the implication is that the bidders didn't see the value or found issues in due diligence. We still wonder if the whole sector received an unexpected tailwind from the sell-off in sterling in late 2022 and if conditions are now normalising. Equals have done much better than Argentex, who lost a CEO under suspicious circumstances last week, to capitalise on the opportunity, but it still could be a sign that management is looking to exit to dumb Private Equity money at the top.

Halfords (HFD.L) - Investment in Avalyer

After some takeover speculation a couple of weeks back, the shares have been strong this week on the following news:

Bridgestone will acquire a 5% stake in Avayler for consideration of USD 3m, which will be satisfied in cash

Avalyer is their software business. So this news values it at USD60m on a read-through basis from the 5% equity sold to customer Bridgestone. The remaining 95% is, therefore, valued at just over 10% of the market cap. So, it's not particularly material in the grand scheme of things, but then you could argue the market was giving this approximately zero in their valuation.

They are also getting Bridgestone as a customer. However, it is not clear if this is part of the deal. It is described as a "Commercial Agreement" but may be at a discount rate or even free with the equity investment:

Under the Commercial Agreement, which has an initial term of 15 years (with certain break rights), Avayler will provide Bridgestone with access to Avayler’s in-garage and van software products as well as certain services to facilitate Bridgestone’s use of it, including services relating to maintenance, development, implementation and support. The Commercial Agreement provides for the roll-out of Avayler’s products across Bridgestone’s retail and van operation in the USA.

In other news, we are surprised Avalyer only lost £75k last year:

Avayler had gross assets as at 31st March 2023 of £3,054,618, and generated a loss of £74,662 in the financial year ending March 2023.

It seems actually quite low for a start-up, showing that they may well be on the cusp of independent profitability. However, there is considerable scope for Halfords to make this figure whatever they want.

Surface Transforms (SCE.L) - Trading Update

In the least surprising news of the week, it is another profits warning from Surface Transforms:

Whilst October sales of £1.0m was the best month of sales in 2023, it was lower than management had previously budgeted.

The good news is that:

The previously reported technical problems have now been overcome.

Which ones? There have been so many we’ve lost count. We guess they mean the kiln problems that they previously said were fixed and then turned out not to be. The bad news is that they’ve found a new set of problems:

However, we continue to face some challenges in our production line, including single points of failure and a learning curve on the maintenance of our new equipment.

The result of this is that they clearly flag further share issuance, almost certainly by the end of the year:

there remains the need to finance the working capital of the significant sales increase over the next few years.

Making it something like their 15th equity raise in the last 20 years of trying to get into mass production. This could be their most dilutive raise yet. For years, they defied gravity. However, with the shares down 30% in response to this week’s news and 60% since the 1st of August, some assessment of their terrible track record may be starting to be priced in. We say starting as the market cap remains £36m despite these falls.

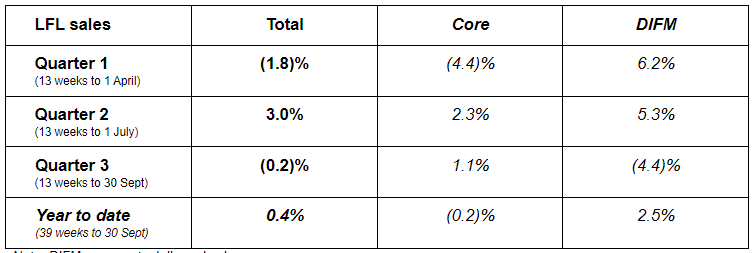

Wickes (WIX.L) - Q3 Trading Update

This is an inline statement:

Based on trading to the end of October, we remain comfortable with current market consensus for FY2023 adjusted PBT of £45.3-49.0m on a post-IAS38 basis.

And here are the sales figures given:

A sales decline doesn’t look particularly impressive, especially after a good Q2. You have to wonder if momentum is going away form them somewhat, especially in Do-It-For-Me. Although they do say:

Selling price inflation in the period was broadly flat, a position which we expect to continue for the remainder of the year and into 2024.

The broker consensus has been continually declining, though:

A P/E of around 9 isn’t expensive if you believe the decline has now bottomed and a recovery in their end markets will come eventually. With the company guiding that their dividend will be maintained and them currently yielding 8.3%, you also get paid to wait. Lots of similar companies in the same sector are equally cheap, though.

That’s it for this week. Have a great weekend!