Small Caps Live Weekly Summary

GEMD ZYT CAPD ANG JOUL MYSL WYN SMRT

A busier week this week with some updates from shared holdings, such as Capital Limited, driving debate. Mark also continued his Stockopedia series, starting to look at the details of companies highlighted by a “deep value” P/TBV screen. Stockopedia Subscribers can check out this and other articles by Mark here.

There was no Large Caps Live.

Small Caps

Gem Diamonds (GEMD.L) - H1 2022 Trading Update

A Strong Q2 leads to good results for H1:

57 075 carats were sold during the Period (H2 2021: 54 573 carats), generating revenue of US$99.6 million (H2 2021: US$97.3 million) and achieving an average price of US$1 745 per carat (H2 2021: US$1 783 per carat).

But there’s a profit warning for H2 in the form of costs 15-20% higher for the full year than previous guidance, due to rains plus supply chain disruptions. The company leave investors to work out the impact for themselves but it surely won’t be pretty.

They’ve cut capex in response, but this gives a mixed message, either it’s needed and simply delayed because they can’t afford it or was not really needed, in which case, why plan to do it at all? Neither is good news.

The share price dropped only 15% in response which looks like a lucky escape here for holders, particularly given that the SP had been strong recently so lots of positive expectations presumably built in. It is also possible that shareholders haven’t yet calculated what the impact of the higher costs will be and will get a nasty surprise later in the year.

Zytronic (ZYT.L) - Trading Update

This unscheduled update is a profit warning due to a weak H2, for the usual reasons. The fall in response to this has not been particularly large. It was probably expected by investors and already reflected in the price somewhat. The cash balance here also provides some downside protection. Although they are expecting working capital to build as the business recovers:

Working capital expansion is expected to continue in parallel with this resumption of activity and in response to the current operating environment. The Group anticipates maintaining a healthy cash balance at the year-end of approximately £6.0m.

There are also quite positive words at the end from a management team not known for their promotional activity:

With an improving log of opportunities and the ability to commit further resources to business development and project progression activities, management remains confident in the positioning, ongoing recovery, and longer-term growth prospects for the Group.

Mark sees no reason why they won’t return to pre-COVID trading eventually, but they certainly are taking their time to get there.

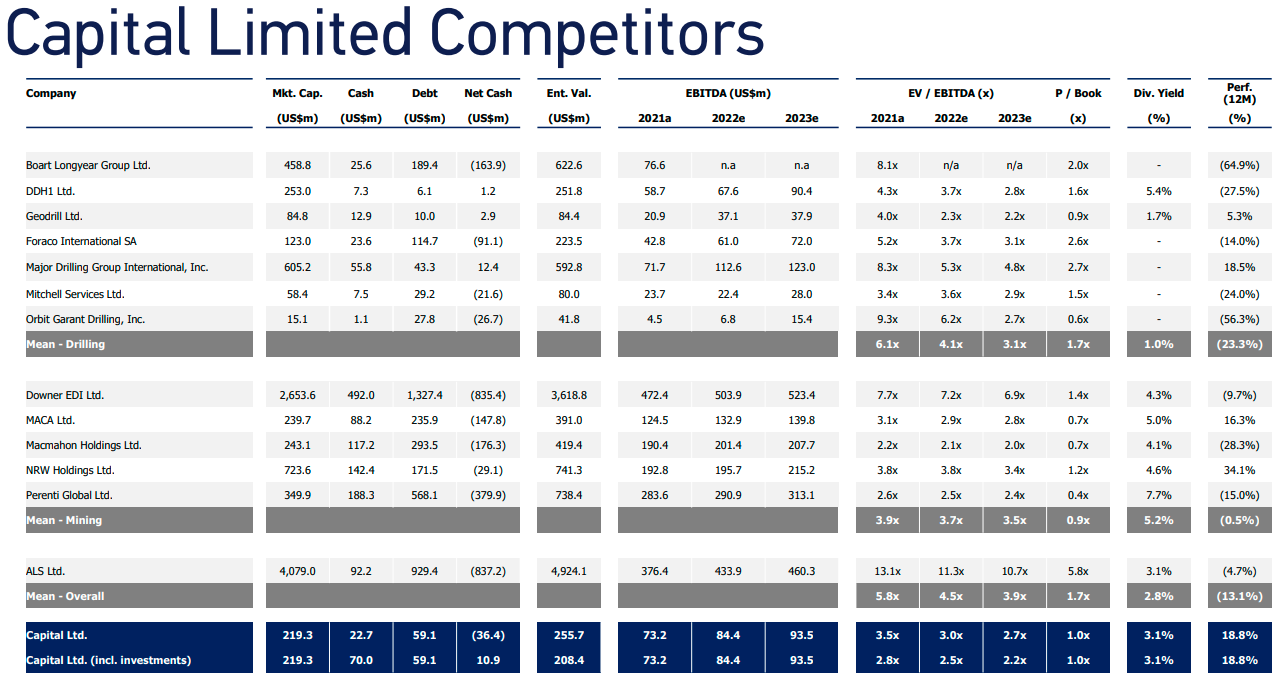

Capital Limited (CAPD.L) - Interim Results

EBITDA came in at $41.4m looks good considering Q1 was relatively weak. EBITDA margins of 30%, top of the guidance range. This shows they are managing any inflationary cost increases really well. Mainly because most of their contracts adjust for inflation. They also provide a small upgrade to revenue guidance:

Full year revenue guidance increased to $280 - $290 million (from $270 - 280 million);

The outlook is very positive, as followers of the company already know:

The underlying demand in the market continues to be encouraging, as is evident from the high utilisation rates the Group delivered in the first half. While there will be some seasonal slowdown through the third quarter, the tender pipeline remains buoyant across drilling, mining and laboratories and as a result of this strong demand, we are raising our revenue guidance for 2022 to $280-290 million.

But there is also good awareness that these boom times will not be forever:

In drilling we have taken advantage of the strength we have seen in underlying demand to focus on contract selection and rotate our portfolio. Through the period we have commenced operations at two more of Africa's largest gold mines, Kibali and Fekola, that are well positioned to operate consistently throughout the cycle.

Given this, Capital really should be on a premium rating to the sector. Yet their presentation shows that they remain at a material discount:

The capex guidance has increased:

We have also lifted our capex guidance to $50-55 million, which includes higher sustaining capex on the expanded fleet, and additional rigs to replace expedited rig replacements. In the strong demand environment we are currently experiencing, we have decided to further replenish our fleet to ensure both high reliability as well as a peer leading safety performance which remains core to our operations.

Some may not like this, although we view this as a fairly positive sign given that Capital are excellent capital allocators. Perhaps the only thing to criticise in these results is the lack of further buybacks announced. The overall returns to shareholders from a growth company at 3.7% dividend yield and 90bs of historical buybacks this year are not too bad. However, with the company trading at a forward EV/EBITDA of 2.5, then buying back shares is like winning new business at 40% EBITDA margins. Something they may struggle to do, even in these boom times.

The share price reaction to this small upgrade was minimal, perhaps because shareholders have got used to this company not moving even on excellent results. This does, however, mean that a significant valuation anomaly remains.

Angling Direct (ANG.L) - Trading Update

Another profit warning:

As a result of these market headwinds the Group now expects to generate revenues marginally below current market expectations for FY 2023. However, Pre-IFRS 16 EBITDA is now expected to be materially behind current market expectations for FY 2023 and in a range of between £3.0 million and £3.4 million.**

Usual stuff, plus hot weather and low-flow, polluted rivers not helping:

…there has been an inevitable impact from the ongoing cost of living pressures, declining consumer confidence and unavoidable inflationary pressures on trading. More recently, adverse fishing conditions caused by the heatwave and its resulting effect on river levels and fish health has also impacted trading in the usually busy month of August.

Understandably, the market sold off in response to this announcement but has now largely bounced back.

Net cash and cash equivalents as at 31 July 2022: £17.1m

A c.£25m market cap means that the EV here (Ex-IFRS16) is just under £8m. We suppose the market thinks they won't use that cash productively. However, a simple rollout of more stores would appear to be profitable, even in current conditions.

Joules (JOUL.L) - Trading & Business Update

Jouls had bounced strongly recently on the news that Next was considering a strategic investment. However, trading continues to be very weak:

As a result of the recent softness in trading and the current weak consumer sentiment set out above, the Board expects a significant loss in the first half, followed by an improved performance in the second half as the benefits of business simplification begin to be realised. In light of this, the Board currently expects the Group to deliver a full year loss before tax, and before adjusting items, significantly below current market expectations.

Their finances already looked stretched and now need a covenant waiver:

The Group expects to require a waiver of certain covenants on its facilities and is currently in positive discussions with its bank in this regard.

The Group also continues to have positive discussions with its bank on its medium-term financing, including a review of covenants to enable progress on the previously announced business simplification and cost reduction measures.

Next are still in the frame:

Further to the announcement on 7 August 2022, the Group continues positive discussions with Next Group Plc about both adopting its Total Platform services to support its long-term growth plans and a potential equity investment. There can be no certainty that these discussions will lead to any agreement, and further announcements in this regard will be made if and when appropriate.

However, you have to wonder if they would be better off following the strategy that Frasers often prefer - buying the whole company from the administrators, minus the debts.

Mysale (MYSL.L) - Takeover Offer

Frasers don’t always buy from administrators it seems, as Mysale gets the takeover offer that was always expected since Frasers took their large stake in the company. But they still rarely overpay - the offer is at a 25% discount to the share price before the announcement.

Shareholders who bought just before Fraser’s picked up their stake will have done well. However, recent takeover speculators will have taken a bath, since, with the existing stake, this looks like a done deal.

Wynnstay (WYN.L) - Fundraise

They successfully raised money this week - £10.6m or 9% of the market cap at 560p vs 620p share price prior to the raise. They are a little vague on the reasons for the raise apart from signalling “opportunities”. Of course, the company has reported great profits recently, but not great cash flow since a lot of the gains are due to the way FIFO accounting works for distributers in an inflationary environment. Perhaps the reality is that they felt the balance sheet little stretched and may be calling the top of their share price in the near term?

SmartSpace (SMRT.L) - Trading Update

Net cash is the number that matters most here:

The Group had gross cash of £2.3m as at 31 July 2022 (30 April 2022: £2.3m, 31 January 2022: £2.8m) and net cash position of £2.0m (30 April 2022: £1.9m, 31 January 2022: £2.4m)

Quoting both net and gross cash avoids the concerns that we have had about these statements in the past. As you can see, cash burn stopped for the last 3 months, which is great news for shareholders. Virtually all their borrowings have been on a mortgage, i.e. low cost and backed by property, so it is reasonable to take the gross cash figure for most purposes. Commentary on cash:

We finished the period with strong revenue growth, and £2.3m of cash, the same level disclosed at the end of April 2022. This was helped by the increase in cash inflows from Naso, as sales grew and continued cash generation within SwipedOn.

The risk here is that the level of cash is not sustainable over a longer period. For example, we know costs have a seasonal aspect, and they may have taken an axe to marketing. Also, until we see the accounts, we don’t know the working capital position. Working capital was negative in the past, which isn’t abnormal for a software company, but means that if they are growing revenue, the cash may be generated from working capital flows, not trading profits.

The market might not like this:

ARR is expected to be lower than market expectations reflecting the updated ARR calculation methodology

What has changed?

ARR and ARPU calculation methodology has been updated and is now based on customers' latest charges....Previously ARR and ARPU was calculated based upon charges which can be invoiced at a customer's renewal date when existing discounts are due to expire.

As Leo has frequently said, getting discounts is frequently just a matter of asking for them, or rather telling them you don't have the budget. So the safest assumption is indeed that discounts will continue. What mostly matters is LFL performance;

Group recurring revenue expected to be approximately £2.4m up 49% year on year (31 July 2021: £1.6m)

And:

The Board expects to deliver revenue and profitability results in-line with current market expectations for the full year

The company is looking more interesting than it has done in the recent past. Although the cautious will want to see those accounts before making further judgments.

That’s all for this week. Have a great weekend!