Small Caps Live Weekly Summary

FLO NWOR SCS SLP

A later and briefer weekly summary this week due to personal commitments. A reminder that all of these discussions happen mostly during market hours in the week, and everyone can join in on Discord. Not only that, but the channel acts as an up-to-the-minute aggregator of all the regulatory and many other important pieces of UK Stock Market news, so is worth checking out.

Flowtech Fluidpower (FLO.) - Trading Update

The market didn’t like this update, marking the shares down around 20%. They don't look terrible at first glance:

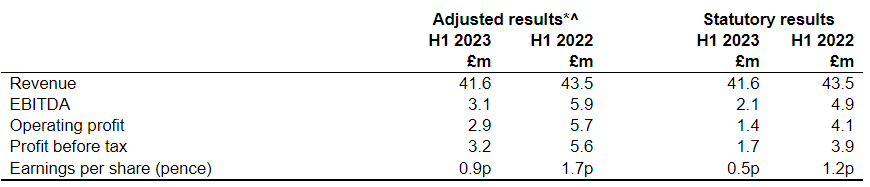

But it's a big, H2 and therefore full-year, profits warning:

There are however adverse market headwinds into HY2 with several OEMs citing a slowdown in project velocity and a more general cooling across the broader industrial markets. For these reasons the Board now expects the out-turn for FY23 to be significantly behind previous expectations.

Market expectations compiled by the Company prior to this announcement for the year ending 31 December 2023 were; Group revenue c.£119.4m; underlying EBIT of c.£9.9m, and profit before tax of c.£8.8m

Liberum cut 2023 EPS forecasts from 10.7p to 6.0p, and 2024 from 13.7p to 11.4p. That’s a big rebound but on largely flat forecast sales. So there seems to be a fair amount of hope in this recovery. As such, the shares do not look cheap. Perhaps the most interesting part is that the weakness in consumer & housing appears to now be affecting the industrial sector too.

National World (NWOR.L) - Half-Year Report

These are figures competitor Reach can only dream about:

Robust digital revenue growth, up 9% year-on-year to £8.9 million.

Although, these are not LFL:

Acquisitions. For the five acquisitions completed in the period, the Group paid a total consideration of £3.0 million, (£1.9 million consideration net of cash acquired) funded from its existing cash resources. Revenue of £2.0 million and EBITDA contribution of £0.3 million are reported in the first half, with the bulk of this flowing from 1 May.

Overall, these aren't particularly great results compared to last year:

However, they say:

In July revenues have increased by 2% year on year and the Company is poised to benefit in the second half from at least three of its key elements - the acquired businesses, new launches and relaunches of heritage brands and video and TV expansion. Therefore the Board confirms its view that the business will perform in line with expectation for the full year.

In line is a P/E of 7:

Plus, their £21m net cash is over 40% of the market cap. Again, the difference between an underperforming Reach on a debt/pension deficit adjusted P/E of 10 and a strongly performing National World on a cash-adjusted P/E of around 4 is stark.

SCS (SCS.L) - Full-Year Trading Update

An inline statement, which is quite impressive given the economic backdrop. Cash is down from £70.8m to £69.5m yoy. Again, that's pretty impressive, given they spent £5m on share buybacks in the period in addition to the high dividend yield.

The cash is almost certainly mostly customer deposits, given the strong order book, so we’d be surprised if they do another buyback. Of course, DFS spend this cash and more, but then they’ll go bust if we get an actual severe consumer recession.

In line is a P/E of 12.5, though, and given that we don’t think you can simply take cash off to get a low EV when they won’t pay this out, then this isn’t particularly cheap. Potentially worth holding for the 7.5% dividend yield, though.

On the day, the shares were down around 7% but with a large spread. We didn’t see much wrong with this trading statement, but the price had been strong in the run-up, so perhaps just buy the rumour, sell the fact?

Sylvania Platinum (SLP.L) - Q4 Results

These reported last week, but Mark only just got around to updating his model. The Q4 results weren't bad on the production side, with 19koz produced slightly above where he'd assumed from the mid-point of their guidance. This came from much higher plant feed on a lower grade, though, so may not be sustainable going forward. The average Gross Basket price declined more than he expected, though. And herein lies the problem.

If we use current spot rates, their basket price would be 21.3kZAR/oz, versus the 29.5kZAR/oz average for the last quarter. If these levels stay for the rest of the year, and we assume modest inflation in operating costs of 3% (if anything, too low for SA), then EPS will be just 2.6p for 2024. Brokers are forecasting 13.4p

The last time EPS was at this level was in 2018, the share price ranged from 13-18p. Which is a long way south of the current 70p that investors seem willing to pay. The company has more than $100m more cash on the balance sheet, worth around 37p per share. So you could argue that a similar low-point valuation is around 50p/share.

However, the company don't do anything with this cash, and such cash is rarely valued at face value in other companies that simply sit on large cash balances. So perhaps 35p per share would be the current fair value if the current PGM spot prices are the new normal, for a 50% downside.

Whichever way you look at it, holding the shares at 70p is a bold bet on PGM prices recovering fairly quickly. Any upside requires significant price strength on PGM in the medium term. They are in the lowest quartile for cost because they are not doing any primary mining but get the tailings from Sanamcor, so one argument is that others will cut production before them and then the PGM price will bounce back. Doing badly but less badly than the competition is rarely a strong argument for holding in the short term.

That’s it for this week. Have a great weekend.