Small Caps Live Weekly Summary

AUTG CAPD G4M SMRT SOS

A relatively quiet week for small cap news, which was overshadowed by macro & global events. The bear market in UK small caps continues with a vengeance. However, this is equally looking like an opportunity similar to March 2020. Of course, the timing of any bounceback is highly uncertain, and unlikely to be as rapid as in 2020. As always, it pays to be a stockpicker. Some companies seem to defy gravity. Increasingly, they are being found out, though, and the share price reaction has been deservedly brutal. Yet babies are also getting thrown out with the bathwater, and redemptions in small cap funds are making institutions forced sellers of decent stocks at knockdown prices. Our aim is to sort out one from the other.

Autins (AUTG.L) - FY Trading Update

Things seem to be going well:

The Group also continued to successfully control overheads and EBITDA (stated on an IFRS 16 Basis) is expected to improve by £2.1m to £1.0m (FY22: loss of £1.1m).

…until we reach here:

…the stability of its net debt and headroom level will put the Group in a positive position when engaging with its lending partners regarding covenants for March 2024 onwards.

And a quick check of their interims:

· EBITDA1 was a profit of £0.34m (H1 22: £0.35m loss)

· Loss after tax of £0.90m (H1 22: loss of £1.38m)

…shows that EBITDA of £0.66m for H2 is likely to be a £0.6m loss, and a £1.5m loss for the full year. To own this sort of loss-making company in this market you'd really want a big discount to TBV, and at 11p share price, it is bang on 1x TBV. Autins are in a commoditized sector, selling to price-conscious customers. It could be interesting if their "Neptune" product had the combination of a worthwhile patent and good technical performance. However, a quick check leaves some doubt as to who owns the IP.

Any number of struggling industrials or distributors are available sub-1xTBV. For example, Tandem, Northamber, Airea, Pressure Technologies, Titon, Tekmar, and Hargreaves Services currently trade below 0.8xTBV, to name just a few. All of these look better value if badly performing small industrial companies in a recession are your type of thing.

Capital Limited (CAPD.L) - Q3 Trading Update

This is the first time the company has separated quarterly revenue reporting into their business segments:

The story is one of strong mining revenue and good labs revenue offsetting weaker drilling results (mainly due to Perseus’ mine in Sudan remaining closed).

The growth in mining revenue is driven by this contract:

Mobilisation at our mining contract with Ivindo SA [Gabon] is progressing rapidly, with the majority of mining equipment now on site. The contract has a term of up to 5 years and will generate approximately $30 million of revenue per annum once fully operational. The contract involves both earthmoving and crushing services.

This may well be as forecast, but there's always scope for things to go a little or a lot wrong in country, so this is good news. Unfortunately, as we have been discussing, it isn't looking like the Sukari mining contract will be extended. As they rather defensively say:

the Sukari earth moving contract is expected to perform at steady state through the remainder of the year

This isn’t necessarily terrible news. We would rather this capital was deployed into more productive areas of the business, such as long-term drilling contracts or, given the big discount to TBV, share buybacks. In the last presentation, the company said the market for the size of mining equipment they had purchased for Sukari was pretty tight, and they implied they might even make money on selling them vs current book value. But any gain here is mainly by luck rather than management skill.

Regarding Sudan, they previously said:

we are in discussions with Perseus to return to operations in H2 2023.

This week:

...anticipation of resuming operations in 2024.

Broker Tamesis say:

Overall group revenue of $79.7m came in below our forecast of $85.2m

But it looks like maybe Perseus (Sudan) was in their forecast. So, given this was never going to be fully operational again in Q3, it was simply wrong or, at best, stale. In addition to the lack of Perseus drilling, there's definitely a weather impact there as ARPOR is lower as well as utilisation:

However, we can't really judge if the West African rainy season has been any worse than in previous years. So this certainly explains Q3 weakness vs Q2 but not versus Q3 last year.

Revenue for the first three quarters is $234m. Capital maintain their full-year guidance of $320-340m, so Q4 needs to be $86~106m. The top end of that now looks like a stretch, but the bottom end is well supported by new contracts that are becoming operational:

The two high-quality contracts at Reko Diq, Pakistan and Ivindo SA, Gabon began to ramp in the third quarter and will continue towards full operating rates as we progress through Q4 2023.

Tamesis has $324m as their revenue forecast, which appears bang on consensus in Stockopedia. The other good news is that, following the listing of Allied Gold, their investments are doing well:

The total value of investments (listed and unlisted) was $47.8 million as at 30 September 2023 ($42.1 million at as 30 June 2023);

Given the continued strength of gold and the positive outlook for the company, the consensus forward P/E of 5 looks simply too low. Especially as they increasingly have long-term contracts in place for the cyclical parts of their business and secular growth in the increasingly important labs part.

Gear4Music (G4M.L) - HY Trading Update

Here are the highlights:

A 6% drop in sales probably means a 15% or so drop in volumes, given inflation. But the message is one of focus on gross margin, not sales:

- FY24 H1 gross margin expected to be 27.1%, 80bps higher than last year (FY23 H1: 26.3%)

- Gross profit expected to be £17.0m (FY23 H1: £17.4m)

Still not particularly impressive. The reason you give up sales for gross margin is to increase gross profit, not to decrease it. Admin costs are running at around £19-20m, so this is a £2-3m loss in H1. However, they have sacked 20% of the workforce and saved £4m:

- £4.0m annualised cash savings implemented during FY24 H1 that will benefit FY24 H2 onwards

However, it is unclear how they have achieved this for a relatively small one-off cost of £0.5m. That looks too low to generate annualised labour savings of £3.5m by the time you have HR costs and even statutory redundancy. Some of the £1m non-IT savings will undoubtedly be lowly-paid distribution workers on insecure contracts. For the better paid:

§ £2.5m reduction in software development team annual salaries

The best explanation is that they had a very large contractor IT team that they have been able to let go without any payment beyond notice. However, last year they said:

Wages and salaries, social security costs, and staff pension costs of £5,205,000 (2022: £4,400,000) relating to software developers are capitalised and not included in the figures above.

So that’s £5m of IT salaries that didn’t appear as admin expenses. When we see the accounts, it is worth checking that they haven’t just generated these savings by simply capitalising more IT spend. With the savings included, they say:

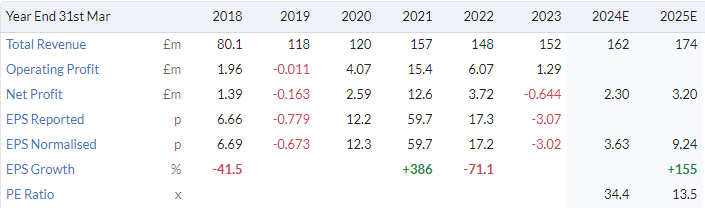

Full-year outlook remains in-line with consensus market expectations

These are given as:

…revenue of £161.7 million, EBITDA of £9.8 million and profit before tax of £1.2 million.

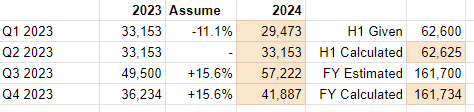

But are they currently tracking towards these revenue expectations, which would mean +6.3% yoy? Based on the evidence we have, the answer is clearly no. However, there could be evidence suggesting they can hit these, which they have chosen not to disclose. For example, if Q1 were down 25%, then Q2 would have been up 14% on an equal baseline. Accelerate that to 16% for the other two quarters, and they've met their target:

Here's another way of meeting the target:

So, either we have an undisclosed 25% drop in Q1, or a hope that at least 16% growth for the rest of the year will drop out of a clear sky. Neither seems a likely scenario to us. Nor perhaps to broker Progressive, who say:

Group revenue consensus stands at £161.2m, an increase of 6% over FY23. With H1 group revenues declining by 6%, the shape of our forecasts may be recast when the more detailed interim results are published on 14 November.

Even if they pull it out of the bag, this isn’t cheap on FY24 forecasts:

You have to believe in further progress out in 2026 to make them look even reasonably priced. So, this company appears to have been bid up over the last month or so by a combination of hope and momentum:

With this trading statement, that hope has now been dashed on the rocks of reality, with the momentum about to join it shortly.

SmartSpace (SMRT.L) - Interim Results

Here's the ARR table:

So ARR growth recovered to 23% pa in the last two months from 27% in 2023H2 and 15% in 2024H1. SwipedOn made a pre-tax profit, which feels like progress. But here's the main new news:

Cash balance at 30 September 2023 of £2.0 million [vs £2.2m 31st July]

This looks like a positive step towards cash flow breakeven but then they did receive £1.15m from selling A&K:

They put investment flows together in order to imply they are cash flow positive both before and after investment, but on a continuing basis, they are likely still burning cash.

This time, they only had a £150k benefit from working capital, so the current six-month cash burn rate is likely to be c.£650k, assuming no further W/C benefits. Overall, the current working capital position hasn't materially changed, which is good news, but of course, they only have net cash because they are getting paid upfront license fees by customers. This is the nature of software businesses, and can continue indefinitely as long as sales don't decline. This means that they have at least a year of cash at the current cash burn rate, and we don't see them raising any time soon.

However, this (relatively) positive step on cash burn comes from cutting costs, not rapid sales growth:

Canaccord are predicting £0.2m cash burn FY 1/25, so surely FY 2026 will be cash flow positive. The growth assumptions from Canaccord are modest too:

The current 2xARR valuation looks about right, so there is little opportunity for either the bulls or the bears at the moment.

Sosander (SOS.L) - Trading & Strategic Update

This is a major change of strategy from this company that was previously pursuing rapid growth in order to scale into profitability. They are now stopping promotional activity to focus on profit and physical stores. They claim that:

The Company has spent much of Q2 FY24 trialling the planned reduction in promotional activity in order to validate its assumptions on consumer behaviour and the associated KPIs.

But given that they didn’t announce this in advance, we have no way of knowing if it is simply an excuse for current poor trading:

So, there is no real growth and a ballooning loss. The low growth is forecast to continue:

The Company expects revenue to grow by 10% year on year for FY24 to £46.8m and to remain in profit during the transition. It expects revenue in the year ending 31 March 2025 ("FY25") to grow by 17% year on year to £54.6m with an upward trajectory in profitability

They say "upward trajectory", not actually “profitable”, so it could still be loss-making. The problem is that there is no shortage of low/no-growth clothes retailers that are struggling at the moment. By way of comparison, Quiz Clothing is on a rating of just 0.1x sales, following a very similar omnichannel strategy. If we put Sosander on a similar Price-to-Sales, this would be just a £5.5m valuation. Although Sosander has £7m cash vs c.£3m for Quiz, so the comparative value is probably more like £10m. This leaves a long way down from the current £28m market cap, despite an almost 40% fall this week.

That’s it for this week. Have a great weekend.