Small Caps Live Weekly Summary

LHA MWE GATC CAPD VTU

A relatively quiet week this week but with lots going on in ‘normal life’ meaning that we have tended to focus on analysing news on companies such as Vertu and Capital we already follow rather than new finds. In such times our coverage lacks breadth but, hopefully, more than makes up for it in depth.

In addition, there have been quite a few company presentations, which we tend to discuss live on the #live-events channel on discord rather than in the regular scl slots. There’s a list of upcoming presentations that we are likely to cover here.

Large Caps Live Monday 16th August

The following charts from the FT are an eye-opener:

I want to make special mention of Hapag Lloyd.

Making more money in 6 months than in 10 years is stunning. (And it trades at a PE of 11.) Compare that with a paragraph from a FT article on 1st July 2020:

The stunning thing is that the 1st July 2020 article mentioned overcapacity and that new vessels recently commissioner were equivalent to a 1/10th of the global fleet. You combine that with the collapse of GDP in the West in 2020 and you have to wonder what happened?

So this goes on to the question of whether inflation is transitory or permanent. Frankly, I don't have a clue. But I think it is reasonable to say that it will be different for different parts of the economy.

My favourite shipper is Maersk which owns SeaLand. The latter is discussed in 'The Box' which is a fantastic book on container shipping. Maersk is on PE 6.3

Malcolm McLean created the shipping container - the book is really about him. You need to get past the first couple of chapters but then it is fantastic. Also amazing is the cycles shipping went through - at one stage they built faster ships only to find that with the 1974 oil crisis IIRC no one wanted to pay for the speed. Another time they built the biggest ships only to find so did everyone else.

Maersk has an ROE of 28% and a P/TB of 1.93. The fact it is on a PE of 6.3 tells you that the market believes this is all transitory. If we extrapolate that then it implies inflation will be transitory. OR that Maersk will be a good hedge if you believe that logistics inflation is NOT transitory

The Emma class (which was the massive one in the last cycle) brought on excess capacity. The argument against excess capacity last time was that the smaller ships eg 10k containers (vs the Emma at circa 18-20k) were diverted to smaller routes eg intra-Africa or Europe to South America. I was never quite sure of the argument

I would also point out that part of the Chinese Belt and Road initiative involves building / investing in ports. Of course, the UK had a shipping industry and a port industry ...... once.

The only point I would make is that I prefer the big operators such as Maersk due to their scale and that they are less of a price taker as they are vertically integrated (own / control their own ports) and logistic chains. Also, the valuation of ships is volatile.

In 2009 - 2010 I made a lot by shorting Frontline at the time - which was the world's biggest listed oil tanker company. - Due to classic oversupply.

Also worth remembering that the widening of the Panama canal has opened up the US East coast to potentially Asian ships - it means that cargo is not restricted to Long Beach California and then trucked in. Was part of the reason years ago I looked at Kansas City Southern.

You can see from the above map that if ships from Asia go into the Gulf of Mexico then KCS has the rail lines to get the containers from eg Texas or Mexico into the heartlands of the US. And this is why eg Canadian Pacific is trying to buy them:

Anyway, the point of the above is that logistics matter. But just thinking about it there is a further point - generally shipborne transport is the cheapest cost so you want to travel as far as possible by ship. This means the widening of the Panama channel increases the number of cargo days on ships and so demand for ships.

So how can we make money?

What I am thinking is that high shipping prices are often associated with shipping delays. So it will increase the number of customers that will shift to air transport - especially as projects get delayed or in the run-up to Christmas. And that will result in air freighters having supranormal profits.

The biggest air freighter division I think is within Lufthansa. The chart is awful due to the passenger side but I think it is worth doing more work on the freight side.

Small Caps Live Wednesday 18th August

MTI Wireless (MWE.L) – Interim Results

MTI Wireless traded at a discount to tangible book value for a number of years as being an Israeli company listed on AIM was met with some scepticism from investors. In recent years, the company has experienced a rapid re-rating, as scepticism has declined and the company is operating in several “hot” areas: water management and 5G. Management also attended the last physical Mello event which helps to reassure investors that this is a company that does what it says it does.

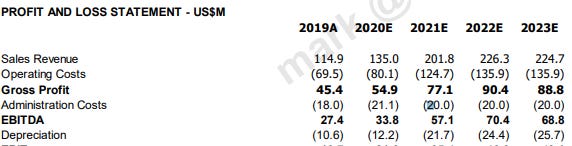

When we’ve looked at the company recently, we questioned whether being in these hot areas will actually lead to significant growth, though. The gross margin here is in the 30’s, which while not terrible, doesn’t scream high tech software, and at least some of their business is distribution and contract manufacturing. The 21Q1 numbers were lower than 20Q4 which doesn’t help with this perception. However, the management said this was simply due to seasonality. In this context, these interim results will reveal a lot. Here’s the headlines:

• Solid revenue growth, up by 9% to $21.3m (H1 2020: $19.6m)

• 13% rise in net profit to $1.73m (H1 2020: $1.54m)

• Earnings per share increased by 14% to 1.89 US cents (H1 2020: 1.65 US cents)

• Strong balance sheet with net cash at $9.7m as of 30 June 2021 (30 June 2020: $7.6m)

So not bad. And the good news is that the growth appears to be across the business:

• MTI Summit continues to benefit from increased government spending on defence

• Mottech opened a new, wholly owned subsidiary and office in Canada and retained key city centre contracts in Israel and internationally

• The Antenna division secured its first contract to develop antennas for use in space and the take up of 5G antennas is in line with internal forecasts

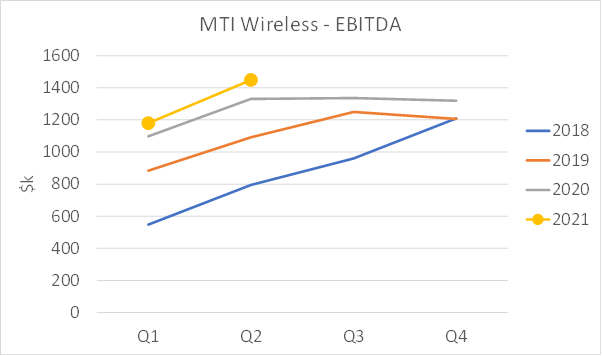

Many companies are reporting great growth in 21H1 when they are comparing against the covid hit 20H1 and getting growth company ratings, when the true comparison against 19H1 shows a decline. Not here, however, where their 2020 results were largely unaffected by COVID. We like to break out the quarterly figures from the results to get a true picture:

This is a graph we have shown before and shows the seasonality effect does appear to be real:

2020 perhaps shows the covid effect, with a flat Q3/Q4.

So what about valuation? After the Q1 results, we commented that:

At 71p, this is on a historical P/E of 24 & an EV/EBITDA of 15.4.

If Q1 trends continue, I can see that being a forward P/E of around 20 and an EV/EBITDA of around 14.

This is hardly cheap for a company growing at 5-10%, even in current markets. They say they are targeting low-teens revenue growth a few years out but this acceleration would appear to already be priced in at the current valuation. Although this is a family-run company with a long history, there are additional risks of being a foreign domiciled AIM-listed stock.

I’d expect this to trade at a discount to the market, not the premium it currently does.

In this context, the Q2 numbers are slightly above the assumptions we made at the time, but with the share price at 76p, these remain on a 14xEV/EBITDA forward multiple. And, while there is a lot to like, there are a number of additional reasons we think this rating looks excessive:

1. The revenue growth rate is still sub-10% overall. (The trend lines on the charts we've shown are linear, not exponential.)

2. There doesn't appear to be much operational gearing. With a 30% gross margin and admin costs rising then the operating profit again is not rising at a consistently high rate.

So, this is a surprisingly good company (especially given that it is foreign-domiciled listed on AIM) but, like many out there, the rating appears to have got well ahead of itself.

Gattaca (GATC.L) - Trading Update

We commented in March 2020 about how the recruiters exposed to contractors would release working capital if business declined and many of their costs could be furloughed, but we’d like to point to this comment here on 3rd April 2020 when the share price was 28.9p:

GATC [would] be daft to raise at 0.3 book - better to style it out - call the banks bluff - like STAF they could very easily by a zero, but if they are not then likely to be a 5x in a couple of years. I see the chance of a zero less than 50% given the pressure on banks to practice forebearance.

Gattaca also tightened up contractor payment terms and benefited from VAT deferrals, leaving them swimming in cash. As we highlighted ahead of time, the IT contractor part of their business was barely affected as most worked at home with little interruption. As a result, the share price did 9x in 14 months, rising to a peak of 272p a couple of months back. In contrast, Staffline were 18.37p on 3rd April and have “only” 4 bagged since. The quality operator, Hays, hasn’t even doubled.

In line with widespread reports of an exceptionally strong labour market, Gattaca’s business has continued to do well, as yesterday’s update showed:

Following our trading update announcement on 21 May 2021, we expect continuing underlying PBT1 and adjusted net cash (excluding IFRS16 lease liabilities) to be above market expectations for FY 2021

...underlying PBT for the full year to be in excess of £3m (market consensus £2.7m).

Underlying cash flow and cash levels remain strong:

Adjusted Net Cash (excluding IFRS16 lease liabilities) is expected to be £20m2 (31 July 2020: £27m) largely driven by repayment of deferred VAT (£4.7m)

With these kinds of figures, it is easy to forget that Gattaca badly underperformed from 2014 to the end of 2019, having to make acquisitions just to maintain revenue, and suffering a fall in share price from over 600p to around 120p. So, what are the prospects from here?

Paul Hill writing for Equity Development sees adjusted EPS rising from 6.7p this year then 13.3p, 20.3p and 24.9p in subsequent years on net fee income that recovers and then sharply increases from then on. Liberum have similar forecasts, although they stop at 2023. So perhaps that should support the current share price?

The trouble is that we can’t establish any solid basis for these forecasts whatsoever beyond the first year, and claims that a 10x EV/EBIT multiple is justified for a company with this track record are frankly ridiculous.

Still, it was a strong update, so what was the trigger for the share price fall on the day?

We see that Paul Hill cut his 2024 NFI growth rate forecast from 15% to 10%, taking 5p off the EPS forecast. So perhaps that’s it, or perhaps it is just a recognition that the share price got ahead of itself.

Despite predicting growth many years in advance, the Equity Development NFI estimate for 2024 is still around 2019 levels. For much of 2019, the share price traded 120-140p range, as the Brexit outlook loomed large on the sector.

Regardless, picking growth numbers of 20%, 15% or 10% out of the air, which have no historical foundation, sticking them in a model and then applying a growth stock multiple is rarely a sensible way of valuing a company. And there is plenty that could go wrong. They still have an issue with the US government claiming they broke sanctions that could blow up or continue to incur high costs year after year.

Still, investors have done well here and in retrospect at least, a rise to 150p-odd was reasonably foreseeable.

Small Caps Live Friday 20th August

Capital Ltd (CAPD.L) - H1 Results

Here are the headlines:

The growth rates here are very impressive, and these exceeded my expectations which were for about 5 cents EPS and $27m EBITDA. [In this case, it is right to take the adjusted EPS figure, since this excludes investment gains. Although they have made another $8m or so gains on the portfolio since the end of June, then this isn’t sustainable in the same way that operational growth is.]

Although admin costs were slightly higher, the gross margins were much higher than we’d anticipated. This is partly due to the strong rig market, but a lot of the gain is due to operational performance, not price increases. This is a company that likes to treat its customers as partners, so will not price gouge them in a tight market. The flip side of this is they tend to win long-term contracts that mitigate the mining cycle, and that contracts often contain provisions to pass on material pricing increases if they occur. Something that may be of concern given recent commodity & transport inflation (see Larg Caps Live).

To get the numbers to work then the rig gross margin has to be around 45% and mining services 35%. Numbers that will be at all-time highs. The company themselves prefer to focus on EBITDA margins, which again are showing positive trends and nearing all-time highs:

The company say they are very comfortable with EBITDA margins between 25-30% going forward so looks like these will remain at these sorts of levels. They also point out how they consistently generate higher EBITDA margins than competitors throughout the cycle:

These graphs are from the H1 results presentation which they gave yesterday morning following results.

For anyone who missed it, they are also doing an InvestorMeetCompany presentation on 25th Aug 2021 at 9:00am BST.

In terms of forecasts, we turn to Tamesis, since we cannot access the notes from Berenberg etc. Tamesis note the beat of their expectations:

They are generally ahead of our forecasts although the company has already reported the operational parameters that have driven this along with an increase in its FY2021 revenue guidance to US$200-210 million (up from US$185-195 million). All parts of its business - drilling, mining, investments and laboratory work – look set to grow materially driven by a macro tailwind and astute corporate strategy.

We increase our TP to 135p.

House broker Target Prices have to be taken with a pinch of salt, but they clearly feel there is material upside here. However, the forecasts themselves look light to me.

Let’s start with utilisation:

For 2021 this works out to be c77 rigs. However, 81 were in use, on average, in Q2 and we know some of the new rigs were delivered late in H1 and 8 new rigs are arriving in H2, of which 6 are immediately going onto long-term mine site contracts. Even if we include some Q3 seasonal weakness in exploration due to the WA rainy season, then this seems conservative.

Same with ARPOR. Tamesis have this moderating to 175k in H2 which doesn’t seem to fit with the underlying narrative from the industry.

The company have guided $200-210m revenue for 2021 and Tamesis have gone for the lower end of that range:

In terms of revenue forecasts, this means that to get their numbers to add up then Tamesis have gone for an estimate of $18.4m of mining services revenue in H2. The company did $20.3m in H1 and we know Sukari is still ramping up and MSALABS is growing rapidly and adding new labs and new technology for improved throughput. So again, this looks light.

Mark’s revenue estimates are for the upper end of the guided range with scope to surprise on the upside if the market for rigs remains strong. This makes their EBITDA estimate likely too low also:

Modelling this we get $63m EBITDA for 2021 and $80m for 2022 assuming 75% utilisation. The Tamesis admin costs estimate look a little light in here though, given H1 numbers, so we will aim to clarify with the company in the IMC presentation.

At the bottom line this comes out as 10.3p EPS for 2021 and 15.3p for 2022, which means a P/E of 7.7 falling to 5.2.

We can only think 2 reasons that would mean that the share price failed to respond positively to the very strong results:

The first is the debt increase and working capital outflows. However, we know from the company presentations that both now reversing, and the debt is largely secured financing of new capital equipment.

In another sign of strength, the dividend has been increased by 33% and with guidance that we can broadly expect a 1/3 to 2/3rds payout between interims and full year, this a 3%+ yield. While not exceptional, this is good for this point in the capex cycle and the company clearly have the capacity to increase this significantly if further high return capex opportunities don't present themselves next year.

The second reason is the impression that the mining cycle will shortly be on the downslope. However, here you have the management narrative that they expect 2022 to be stronger than 2021, that the mining cycle is just beginning and they will be looking to win the mine site contracts that come in the next 2-3 years from their clients whose exploration drilling is being undertaken today. Their strategy of high-quality partners who have a long life of mine and expanding services to those existing clients is now a proven one. For example, of the 8 new rigs expected in H2, 6 are going to existing long-term contracts and only 2 multipurpose rigs are going into West Africa exploration on spec.

The other aspect that matters with investing in companies that operate in cyclical markets is that the management doesn’t waste all of the cash investing at the top of the cycle. In Capital's case, skin in the game, plus an investment banking background means the company understands the capital cycle well. After all, they got most of their equity stakes by acting counter-cyclically and being willing to use their balance sheet to do drill-for-equity deals when no one else was interested in putting money into small cap gold miners. And it is likely that 2012-15 taught them a lesson in cycle economics.

So, in summary, we have a company:

That has beaten expectations.

Is likely to beat expectations going forward.

Is growing rapidly in a market where demand is outstripping supply at the moment.

Generates higher EBITDA margins than competitors throughout the cycle.

Has a younger fleet than competitors.

Has longer-term contracts than competitors so is less exposed to the mining cycle.

Has hidden value in a rapidly growing labs business and equity portfolio.

Trades at a material discount to the market and to listed-peers.

The price went down on the results.

This is what opportunity smells like.

Vertu Motors (VTU.L) - Trading Update

Ahead of the announcement of its results for the six-month period ending 31 August 2021, the Group is providing an update on current trading and a further upgrade to the full year outlook.

As commented above, this is at least nearly three weeks earlier than they usually issue the pre-close update.

The Group continues to experience strong used vehicle gross margin retention, driven by the exceptional UK used car market conditions. Consequently, the Group expects that it will deliver an adjusted profit before tax of no less than £50m in the six months to 31 August 2021.

The driver is once again used cars. They have proven themselves much more adept at getting stock than either their peers or the would-be online disruptors. This is not only good luck but good execution - they're getting the volume as well as the margin.

The Group's like-for-like new vehicle order take for the key month of September is currently running in excess of prior year levels

September 2020 was actually one of the less disrupted months with registrations down only 4.4% YoY, so this is a reasonable comparator. Industry forecasts actually imply a fall of circa 10% YoY for September 2021.

however, there is a risk that well documented new vehicle supply shortages will result in vehicle deliveries being delayed into future periods.

Neither registrations nor revenue can be recognised until the car is delivered. Potentially the industry will find itself in the same situation as the furniture retailers (e.g. SCS/DFS) - with a high order book but revenue being delayed. The upside here is that a higher order book improves visibility. In some cases, people can be put off ordering if there is a big delay, but in other cases, it can actually encourage people to get their place in the queue early. What's important is that your supply is at least as good as competitors. The diversity of dealerships should help here.

As a consequence of reduced new vehicle supply, used vehicle supply may also be restricted in the coming months.

This strongly implies there is no current restriction in used car stock.

Uncertainty also remains around the possible impact of COVID-19 from potential future restrictions and colleague absence.

You can be sure we'll be watching this carefully! The next warning sign will be the Scottish schools return. However, in my view car showrooms would be the last to close and this would only be required if the government deliberately lets things get completely out of control (again again again), and even then they'd need some bad luck such as new variants (again again).

It was interesting to hear in the recent PI World presentation that customers are happy to test drive without a salesperson in the car. This bodes well if the aversion to protective masks in the UK leads to a ban on accompanied test drives. So, overall, I'd say any winter resurgence in covid could, if anything, benefit car dealerships as other opportunities to spend money reduce. The current UK wide labour shortages, high vacancy levels and upward pressure on employment costs remain a risk for the business. This was commented on in the recent PI World interview, as well as being reflected in wage growth figures and unemployment rates. Labour supply for car salespeople will be less directly affected by the failures of policy in issuing visas following Brexit than other industries though.

The Board remains cautiously optimistic and is upgrading the estimate for profit before tax for the current financial year to be in the range of £50m to £55m (previously £40m to £45m).

As highlighted at the start, this is the second time in 4 weeks that they have issued a new guidance range that is disjoint with the previous one. That's not how ranges are supposed to work. It was very clear that the ranges were far too tight given the high levels of uncertainty and that the risk was on the upside. The 90% confidence interval likely continues to lie far outside £50-55m.

As a result of the strong performance seen in the financial year to date, the Board intends to re-establish the payment of dividends to shareholders upon finalisation of the interim results.

Like many companies, Vertu has been cautious about being seen to make dividend payments in the same year, or so soon after receiving government support. Some repaid all support so they could make a divided. IIRC Vertu has not, finding a middle way like repaying business rates for months when they were open, while keeping furlough and other rates relief. Therefore, we were not expecting dividend payments this calendar year, but it now looks like they will scrape through.

Likewise, we were cautious about the prospects for share buy-backs this year, although it was very clear from the PI World presentation that they were keen to do them. And today we get confirmation that they will do just that.

The Board remains very confident in the prospects for the Group, which is strategically well placed to capitalise on the changes and opportunities in the UK motor retail sector.

This is a reminder that this was a strong company before covid struck, and will come out stronger due to opportunistic acquisitions and cost-cutting through technology. Although FY 2022's profits are clearly going to be exceptional, the following years look pretty good too.

The share price of the Company for some time has traded at a discount to the tangible net asset value and in the opinion of the Board below the intrinsic value of the business. As the Company has a low level of debt and is considerably cash generative, the Board considers it appropriate to allocate some capital to buy back shares.

...an initial amount up to £3.0 million, between now and 28 February 2022

This seems rather modest set against a market capitalisation of £174m at yesterday's close. Looking at the Rule 26 declaration on their Investor Relations website, shareholding concentration is low and free float/liquidity seems likely to be high. Therefore the demand for shares seems likely to be relatively elastic and so a small buyback like this will have a limited direct effect on the share price.

The debt capacity of the Company and positive cash flow is such that we will continue to consider acquisition and investment opportunities as part of the pursuit of the ongoing growth of the business.

They recently commented that prices of acquisitions were likely to be too high right now to consider and that capex demands from brand-holders were if anything abating. But they are keeping their options open and making it clear they have the capacity.

As is usual, purchases will be made by their broker at arms-length, allowing them to continue during the close period. They probably brought forward the trading update to avoid the risk that the share buyback was started in a false market. And they probably wanted to get on with the buy-back.

While a further trading update in two weeks time cannot be ruled out, they will have no obligation to do so and the next update is likely around 7th October with the H1 results. In the meantime, it will be particularly important to watch statements from other dealers on different reporting cycles and, of course, September's car registration figures. The share price continues to trade below pre-covid levels, despite excellent progress and a suspension in dividends:

But this has always been a cheap share. But given the medium-term prospects and the levels of net tangible assets they have accumulated, in Leo’s opinion, the current valuation is somewhere on the scale between crazy and insane.

Zeus title their update "Capital allocation specialists". That really underlines the impression Leo got from watching Undercover Big Boss: CEO Robert Forrester comes across in many ways like an investor, which is obviously going to appeal to us, rightly or wrongly.

Vertu has delivered another earnings upgrade driven by strong ongoing used car margins, in what is effectively an early delivery of the H1 pre-close update.

The shares look too cheap to us even on 2023/24 EPS [6.2p] backed with a current forecast yield of 3.6% and trading below net tangible assets per share of 50.2p.

They've gone straight for the top of the guided PBT range, but apply a slightly higher tax rate than Leo, to come out at 11.4p EPS for this year.

The Group trades below its net tangible assets per share of 50.2p and below our assessment of intrinsic value in excess of 80p

The broker also flags possible upgrades to FY 2022 onwards following the H1 results and conclusion of the buyback.

That’s it for this week. Have a great weekend!