Small Caps Live Weekly Summary

ADF BBSN CAU CTA EMR SNWS

Here’s a selection of what we discussed this week:

Facilities by ADF (ADF.L) - Final Results

In line all around (with previously much-reduced forecasts), and interestingly, they manage to maintain their modest dividend:

Although it’s probably fair to exclude goodwill impairment from the figures here, it goes without saying that adjusted EBITDA is a completely pointless measure for this sort of company. This is not exactly promising either:

In the first few months of FY25, overall performance has been in line with the Board's expectations despite a slower than expected return to pre-Strike levels of activity, with Autotrak performing particularly well. Frozen budgets, reduced production spend, and rising costs have all combined to present short-term challenges.

Given that this is a sort of specialist plant hire company, P/TBV is probably the best metric. This is £13.3m vs a market cap of around £16m at 15p, so it still looks a little overvalued, but may start to look interesting if the price keeps dropping as it has recently.

Brave Bison (BBSN.L)/Centaur Media (CAU.L) - Mini-MBA Deal

Sky broke the story here. Brave Bison revealed the full details:

Brave Bison, the digital media, marketing and technology company, notes recent press speculation and confirms that it has entered into exclusive negotiations to acquire MiniMBA from Centaur Media plc for an enterprise value of £19 million.

It looks like a done deal, as the founder of this part of the business seems keen enough to put in £4m of his own money to make it happen:

Brave Bison intends to fund the acquisition consideration by way of:

§ Existing Group balance sheet cash, totalling £5 million at 31 March 2025 (unaudited)

§ A new Group bank facility of up to £10 million. Letters of support have been received from multiple UK banks

§ A strategic investment of £4 million from MiniMBA founder Mark Ritson who would, on completion, become a Top 5 shareholder

§ A placing of new ordinary Brave Bison shares to existing and new investors

This is what they are getting:

In the year ending 31 December 2024, MiniMBA generated net revenue £10.7 million, growth of 5% year-on-year. Should the acquisition complete, MiniMBA would be expected to contribute a minimum of £3.5 million in Adjusted EBITDA, increasing the enlarged Brave Bison pro-forma Adjusted EBITDA by 78% to £8.0 million.

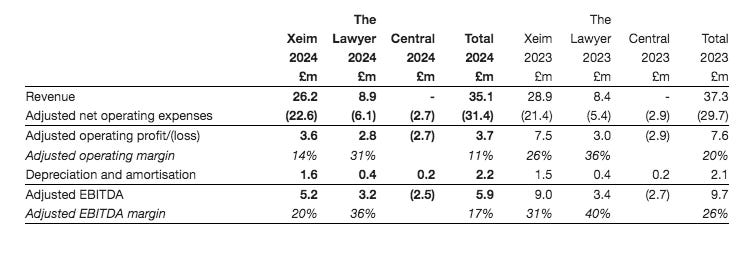

So, 5.4x EBITDA is the figure being discussed. This is what is left in Centaur:

The big question is how much of the central costs can be eliminated and how much should be allocated to the business units. If this deal completes, they will have around £28m in cash, versus a £45m market cap. The Lawyer has always been considered the jewel in the crown here, so if this deal finally marks the breakup of the group and they can get say 7xEBITDA for The Lawyer then there could still be value, despite a rise on this week’s news.

CT Automotive (CTA.L) - Final Results

Gross margin improvements offset revenue declines here:

We are not too worried about the revenue decline as this is largely due to customer scheduling, for which they have no control. Adjusted EPS of 11.8c looks a handy beat on the 9.4c in Stockopedia.

All eyes here should be on the outlook, and it is a complex picture so worth quoting in full:

Outlook

· Trading in the first quarter of 2025 was in line with management expectations benefitting from ongoing operational efficiencies and the commencement of new production programmes.

· Naturally, the outlook for the business has become more complex with the uncertainty caused by tariffs and the extent to which this may impact customer production plans and global supply chains.

· Importantly, the Group had already proactively near-shored a number of production programmes supplying the US, with products manufactured in its Chinese facilities transferring to Mexico.

· While tariffs present challenges, they also create opportunities. In Q1 2025, customers chose to relocate three new programmes to CT Automotive to be produced in our Mexico facility, primarily to mitigate the potential impact of tariffs adding approx. $10 million of annual revenue.

· CT Automotive will continue to focus on the factors within its control, remaining agile and responsive to commercial opportunities, while accelerating the rollout of AI, automation, and digitisation across the business. These initiatives are central to driving further margin improvement and establishing a highly cost-efficient platform to support future growth.

· Overall, the market environment has become significantly more uncertain however, the Board believes the business remains in a robust position and on track to deliver mid-single digit revenue growth together with further margin expansion in FY25.

Although manufacturing in Mexico is not without tariffs, it’s currently a lot lower than for China. Customers near-shoring to Mexico makes sense, and the most pleasing part is that customers are giving them new business (moved from competitors) in Mexico due to the lower tariff rate. They said in the last presentation that they could treble production in Mexico without significant capex. The big worry was that tariffs were going to make this investment wasted, whereas the reality appears to be that this has been a real boon for the company.

They appear to be taking a novel and tech-led approach to their business, including an AI-generated video in the RNS. The only downside was that AI Simon came across as a little unenthusiastic in comparison to his AI host. He should have created an enthusiastic AI version of himself for the video! However, it shows that they think differently to convention, and that appears to be paying off in a highly competitive industry.

Given all of this, the company just seemed far too cheap assuming that PBT doesn’t collapse, let alone grow, and all signs point to modest PBT growth in difficult conditions. The market came round to this view eventually, and the shares were up around 50% on the week. Despite this, they are only on a P/E of 4 which still looks bonkers for a company with good medium-term growth potential. There’s a bit of debt, but this is simply funding the normal working capital moves of such a company.

Empresaria (EMR.L) - Possible Offer

It is a possible 60p bid here, versus an undisturbed share price of 25p, but this looks much worse on reading the details:

The Possible Offer, which is subject to confirmation of funding and completion of due diligence, is payable as follows:

· 10 pence per ordinary share of 5 pence each in the share capital of Empresaria (the "Ordinary Shares"), paid in cash at completion of any offer ("Completion"); and

· 50 pence nominal per Ordinary Share, to be settled in unsecured loan notes redeemable for cash on the third anniversary of Completion. Such loan notes would attract an annual interest rate of 2.6%.

So, most (50p) is in 3-yr loan notes from the director of their Indian offshoring business:

…unsolicited indicative offer from an entity to be incorporated and controlled by a consortium of individuals comprising Peter Gregory, Nigel Marsh and Ashok Vithlani (the "Consortium"), to acquire the entire issued and to be issued share capital of the Company (the "Possible Offer"). Ashok Vithlani is a director and shareholder in Interactive Manpower Solutions Pvt Ltd. (a subsidiary of the Company), the Group's Offshore Services business based in India.

Is this like them getting a cheap option on the business? It is not beyond the realms of possibility that they get three years to see if the business is recovering and pay 60p for it, if not, default on the loan note. In this case, the business probably goes into admin and they only lose 10p/share. In light of this, we’d want to discount those loan notes at an annual rate of around 30% or more, making the NPV30 of the offer around 30p, not much different to the 25p share price before this “offer” was announced. However, given the state of the balance sheet here, this may actually be the best option for shareholders.

Smiths News (SNWS.L) - Half-Year Report

These results are in line:

But to reiterate what we have said in the past, this is pretty meaningless:

Major contract renewals now secured, with 91% of existing publishers revenues to at least 2029, underpinning both short and medium-term revenues and the expansion of our early morning supply chain activities

The 91% is of customers weighted by current revenues and refers to the exclusivity of distribution. 91% of revenues are absolutely not secure, as there is nothing in the contracts about minimum revenue levels, which is entirely dependent on sales and pricing outside of Smith's control. Also, 2029 is around 4 years away, whereas the company is trading on a PE of 5.8x. However, this is another example of the irrelevance of "2029" as renewals of materially all contracts are fairly certain.

Accordingly, second only to one’s opinion about the speed of the upcoming collapse of their core business, this is the most important part of the outlook:

Growth initiatives are progressing well across all three key target verticals, supported by Smiths News' unrivalled expertise in warehousing, reverse logistics and early morning final mile services

We have consistently been impressed with management’s ability to take costs out of their core business, and consistently unimpressed with their diversification efforts. However, they continue to come up with ideas to trial:

Accordingly, in February 2025, Smiths News commenced a trial with global greetings card experts, Hallmark, to deliver greetings cards to independent retailers. The trial has started well, and we will review progress and traction from our retailers throughout the second half of 2025.

However, we are much more sceptical about this:

We have entered a small-scale trial with a number of providers to deliver engineering and manufacturing specialist parts to customers along our existing routes, leveraging our in-depth knowledge of the unique dynamics of the final mile market and our well-established high-density network.

These sound like high-value custom-picked goods, nothing like newspapers dumped on the pavement in a bundle. The risk is that the early bird gets the free high-value engineering part, as it were. However, we are reassured by the careful and gradual way they are rolling out each of their initiatives. They still need that great idea that works after physical newspaper distribution finishes, rather than acts as a complementary service, though.

That’s it for this week. Have a great weekend!

These posts always manage to add an important layer of insight on the reported figures and statements. Always worth a read.

In my view the demise of Smiths is overdone, newspapers & magazines are here to stay maybe less volume, their distribution expertise has enduring value