Small Caps Live Weekly Summary

Mello Birmingham CAPD CLIG MEGP OMG SNX

Our understanding is that ticket sales for Mello Birmingham continue to be strong.

The Early Bird deadline has been extended for a week until 4th March, and there is a reason to get your ticket early, and it is not just the discounted £49 rate. The more investors who are signed up early, the more persuasive the team can be in getting companies to come out and present. The last Mello saw a step-up in the quality of businesses willing to come out and meet investors, and we are expecting a further upgrade with this event. This bodes well, not just for the event, but for UK small caps in general.

We can also confirm that we will be meeting for pre-event drinks on the evening of Tuesday, 21st April, from 7:30 pm in the Old Joint Stock. Any SCLers are welcome to join us.

[We’ve chosen it because it's a nice venue that will make a change of scene, including a view of the cathedral, while only being a few minutes’ walk away. It is a Fuller's pub, which may help assuage any homesickness from regular Mello Chiswick attendees; there’s an opportunity for research/shareholder discounts, and of course, the name fits.]

Here’s a selection of what we discussed this week. (Remember this is a summary of many opinions, and isn’t the view of any one commentator; check out the actual discussion on Discord if you want the nuance of the different opinions.)

Capital Limited (CAPD.L) - Contracts Update

This is a surprise. Waste stripping at Sukari is back. Even more surprising, they still had equipment left on site that they hadn’t managed to sell or ship to Pakistan:

o This contract will utilise our existing equipment still on site supported by a number of newly purchased trucks and additional ancillary equipment

o The contract term is 18 months and is expected to commence in Q1 2026, with our existing equipment, followed by the new equipment phasing in through Q2 2026

This underlines how much the original contract was to defend their position in drilling at Sukari, rather than on standalone economic terms. We expect this to be similar, although bolstered by the fact that they had equipment still sitting around doing nothing.

The rest of the wins adds long term contracts, which is good, generally:

Capital has been awarded a 5-year grade control drilling contract with Montage Gold at its Koné Gold Project in Côte d'Ivoire

MSALABS has been awarded a 5-year commercial laboratory services contract with Equinox Gold's Valentine Project in Newfoundland, Canada

However, we have been arguing for several years that the market had been undervaluing the business for a long time because it was assuming cyclicality. Whereas they were signing long-term minesite contracts that would protect them if the cycle turned, unlike the shorter-term explo contracts they entered the last downturn with.

The problem is, far from turning, so far, the gold price has gone ballistic. But their long-term contracts don’t see the upside from this. To generate higher profits, they have to buy more rigs and deploy them to new contracts. The reality is that ARPOR has been static for years, and probably has declined in real terms.

Yet the share price has doubled on the shift in sentiment to the sector, without any significant change in profitability, making the forward rating double what it was when we were arguing this was cheap.

We also think they should have been deploying their old rigs on short-term, high-rate exploration contracts and decommissioning them at the end of the cycle, rather than getting rid of them over the last few years.

However, it’s not all doom & gloom. MSALABS looks like it is now delivering, after a year or so of consolidation/growing pains. Plus, the equity portfolio has been going great guns, and the market finally seems to be viewing this as an asset, not a liability. So, we were unsurprised that the market liked this update. However, the shift here has largely been one of sentiment so far, and an expectation that a strong gold price will eventually be reflected in much higher profitability. Something has proven less predictable than we would have liked in the past.

City of London Investment Group (CLIG.L) - Half-Year Results

They have the same outflows that are currently plaguing the industry:

Client rebalancing, asset allocation changes, and capital needs led to net outflows of $853 million for the Group over the period, led by CLIM Emerging Markets (EM), International Equity and KIM Growth Balanced strategies.

Although rebalancing tends to be more of an issue than sentiment-driven outflows here, and their strong investment performance continues to more than offset these. This led broker Zeus to upgrade EPS by 10.7%. Although dividend is held, at least it is now forecast to be covered by EPS, making it more secure.

This company often attracts income seekers, although it’s a bit too boring for many, when a lot of the sector is much cheaper and has much bigger upside if a cyclical recovery eventually happens. In this vein, we were hopeful that when we read:

Cooper’s first CEO statement on page 7 of the full interim report begins to outline our priorities going forward.

However, after reading it, we are none the wiser on how he will transform the company as he sounds like a man of continuity, rather than change.

This is a stock which often moves in a trading range, despite the stability of the underlying business. This means that investors may be able to enhance the returns from investing in companies that give relatively pedestrian returns overall by trading these swings. However, we have to question whether a stock that occasionally goes from £3.50 to £4, and back again, is really the best trading share, especially when some of the moves are ex-dividend, and the spread is sometimes up to 5%.

There are times when this sort of stock would be an attractive hold in its own right; perhaps when the rest of the stock market is pricing in boom times, such as mid-2021. However, the attractiveness is much less at a period when a lot of other small caps are so cheap they could double with even minor good news.

ME Group (MEGP.L) - Delay in FY25 Audited Accounts

This is highly embarrassing for a main market listed company, even if they have a shorter timeframe than AIM stocks:

As a result of the delay, the Company expects that its shares will be temporarily suspended from listing and trading from 2 March 2026 until the audit is concluded and the 2025 annual report and accounts are published, which the Company expects to be by no later than 13 March 2026.

This also delays the buyback, which has been one of the reasons for a small bounce here. Coming on the back of a secondary placing, this further undermines confidence, although they say that no audit issues have been raised.

We also get a trading statement:

In respect of the year ending 31 October 2026 (”FY26”), the Company confirms that the year-to-date performance is in line with expectations.

The moat here seems to be non-existent in the laundry business. The photo booth business is even worse; zero moat, and it's obviously being disrupted. It's like a Kodak vending machine, in an era where people can use their own digital photos for passports. But equally, that argument has seemed logical for at least ten years, and yet they keep growing and throwing off dividends. Maybe some network density advantages for servicing, procurement in laundry, and a first-mover installed base advantage.

Around these dynamics is a share price that goes through cycles of what appears to be undue pessimism and optimism on very little change to fundamentals. It seems closer to pessimism than optimism at the moment. Perhaps justified, though, given the inability to get their accounts out on time.

Oxford Metrics (OMG.L) - AGM Statement

Lots of words but very little detail. No actual revenue, order book or pipeline, beyond quantifying a couple of contract wins:

During the period, Vicon, the Motion Capture division trading brand, secured two large Entertainment orders totalling £2.7 million from customers in Eastern Europe and Japan, further stage extension orders in China and two turnkey Life Sciences contracts in India. In the United States, the opportunity pipeline and market activity is similar to the same period 12 months ago.

Perhaps not necessarily out of place for an AGM statement, which tend to be vague at the best of times.

In this case, it seemed so wishy washy that the market interpreted it as tracking slightly behind expectations and hoping for the pipeline to convert, even if the broker left forecasts unchanged. A sentiment we agreed with.

Capital allocation decision seems to have been pushed back to later in the year:

As previously indicated, the Board expects to set out the Group's refined strategy, including detail on capital allocation within the three-year framework, within FY26 and will provide further detail in due course.

Some are hoping that this strategy will include a special dividend or capital return, given the cash balance. However, the signs aren’t great on this front. On the recent IMC presentaion, the CFO comments were around the dividend needing to be covered by EPS long term. With little sign of EPS growing, the only way this can be interpreted is as a dividend cut.

Even if that dividend is slashed, this may still be a good value with £50m of high-margin sales available for a £30m enterprise value, meaning upside if they can get EBIT margins to where they should be.

We’d be a lot more confident in this if the management appeared to have a better handle on the business and didn’t keep ignoring our questions during the results presentations. After all, Vicon is exactly the sort of business that faces a significant AI threat if not handled correctly, so weak management presents a particular risk here.

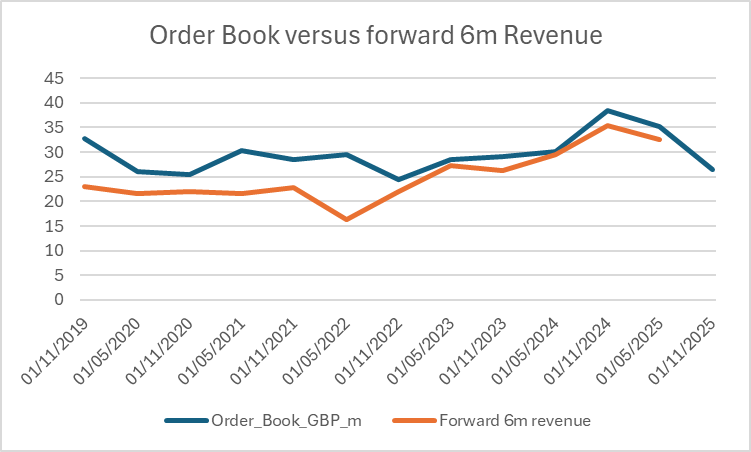

Synectics (SNX.L) - Ongoing New Business Momentum

The market took fright recently at the low level of the order book at Synectics. Our analysis suggests it was right to do so. The correlation between orderbook and the following 6m revenue figure looks very high:

The forward 6m revenue has very closely matched the order book in recent times, and never exceeded it. So £26.5m order book versus a £70.5m FY revenue forecast makes it look like they will miss the FY revenue, unless they deliver significant sales pretty soon.

In light of this, this week’s RNS looks particularly ominous. There are contract wins mentioned:

Synectics has signed an agreement with a Southeast Asian government department to enhance and maintain a traffic monitoring camera system in-country….

In addition, Synectics has secured a further two contracts to supply its COEX camera range to a flagship renewables project in the Netherlands…

But no monetary figures mentioned, no timescales for the energy projetcs and no impact given on the order book that looked so weak in the last update.

These are said to be an:

….important validation of our ongoing focus and strategic intent.

But strategic intent doth butter no parsnips.

That’s it for this week. Have a great weekend!

Thank you for the review of CLIG. One I hold.

If there are small caps that could double, why not list those? This column is so gloomy most of the time!