Small Caps Live Weekly Summary

AVAP BMS CRDL DIAL DBOX NXR PAY VNET

A return to post-Mello form this week, with some more substantive discussions on our Discord server, summarised below.

For anyone new to the SCL weekly summary, these are summaries of the general consensus from multiple contributors on Discord. While Mark & Leo may be the backbone of many of these, and shape what gets summarised, they are not necessarily our views. The idea of the summary is to drive experienced investors to engage in discussions on the Discord server, especially if they disagree with the consensus. This means that we leave comments open here, but we are unlikely to ever respond to them. If you want to join the debate, then make sure you join us in the thread for that share on the server. There’s a help channel if you are totally lost.

Avation (AVAP.L) - Sale of aircraft

Avation PLC (LSE: AVAP), announces that it has entered into an agreement to sell a Boeing 777-300ER widebody aircraft, currently on lease to Philippine Airlines.

The reason given is that they prefer to focus on aircraft currently in production. However, the most significant part is that they say:

We believe that the market values for modern commercial aircraft are materially higher than our book values and we are experiencing favourable market conditions.

There may be a bit of opportunism with this sale. However, if narrow-body aircraft are selling at a material uplift to Avation’s book values, this suggests that the company will be trading at an even larger discount to NTAV than the current 52%. Given the rumours in the past, this may prove too large a discount for larger companies in the sector to ignore.

Then later in the week they announced a furtehr sale, this time of a newly delivered aircraft:

This aircraft is the second sale of a series of two aircraft originally announced in May 2024. The profitable sale of this aircraft releases around US$5 million in net cash proceeds.

This is a very good piece of business. $5m for writing their name on an order book a few years ago. And they have more to come:

Following this sale Avation has ten aircraft on order from ATR for delivery between the fourth quarter of 2025 and second quarter of 2028 and purchase rights to acquire up to 24 additional new ATR 72-600 aircraft.

Of course, like any commitment, it could have gone the other way, but they have been pretty good at calling which planes will be in demand on delivery.

Then we got a clarification RNS, perhaps suggesting they felt what they shared with analysts wasn’t in the public domain but should be:

the company advises that as at June 2025 the difference between 3rd party external desktop market appraisals and the Company book value of the fleet , excluding the Boeing 777-300ER, is favourable by approximately US$82 million (unaudited).

What the analysts at Panmure Liberum did with this information is calculate that the appraised market fleet valuation suggests a valuation of 390p. Some way above NTAV and much higher than the current share price.

The risk remains with the massive refinancing due October 2026, but to paraphrase Airplane, it looks like they picked the right year to give up their unsecured bond finance.

Braemer (BMS.L) - Investigation Update

There has been an ongoing historical issue here:

As disclosed in the Group's FY23, FY24 and FY25 Annual Report and Accounts, an independent investigation was conducted during 2023 that focused on several transactions dating back from 2006 to 2013.

We are not sure this is something to be pleased about:

The board is pleased to report that, following notification in late January 2025, the National Crime Agency (NCA) has today been granted an account freezing order

Braemar seems to imply that this could have feasibly been much worse:

The order relates solely to the separate bank account and the ring-fenced amount, and does not apply to, or otherwise impact the Company's trading or net assets.

Something we feel they may not have adequately communicated to shareholders in the past.

Cordel (CRDL.L) - Trading Update

It’s a profits warning here:

We have made excellent strategic progress in FY25 though are expecting to report a lower than forecast full year revenue result, hence this early update on the likely outcome for FY25.

Blamed on:

Economic uncertainty, particularly in the USA, has unfortunately led to protracted sales cycles and delayed revenue, which has impacted our normally strong second half revenue.

This had spiked up recently on contract win news, so presumably this is a big miss versus investor expectations. Their broker, Cavendish, take 23% out of FY25 revenue estimates and, more worryingly, 22% out of FY26, suggesting this is a fundamentally weaker trading position rather than just contract timing.

Considering the excellent gross margin, the impact on profits and cash from these revenue downgrades ought to have been larger in the new forecasts. Cavendish take only £0.1m out of adjusted EBITDA for FY25, and £0.6m out of FY26. They don’t really explain how they can magically take £1.1m out of their Opex estimates for FY25 with less than a month to go of this period. Presumably, the word adjusted is going to do the heavy lifting here. Cavendish are, of course, incentivised to be chief porcine make-up artist, as they will be the biggest beneficiary of any subsequent equity raise here.

We probably should have seen this coming when, a week ago, and three weeks before their year-end, they changed the vesting conditions for their chief revenue officer from being based on FY25 revenue to future sales bookings. It may be a coincidence, but it sure looks to an external observer that they already knew a profit warning was coming and hadn't informed the market. Perhaps they would argue that they’ve always missed their forecasts in the past, so market expectations should have been for a miss of market expectations!

This is perhaps one reason why the fall this week looks like a massive underreaction to this news. The other possibility is that when something is valued on assumed growth way outside the forecast window, then it is largely a matter of faith rather than reason, anyway. After all, their customer list is impressive, even if their delivery isn’t. Still, you’d think the possibility that they may have misled the market for several weeks would erode that faith quite significantly.

Diales (DIAL.L) - Interim Report

The narrative here always reads so well. For example, here is the outlook:

• Utilisation continuing at 2024 levels.

• Higher enquiry levels across the business in Q2 and flowing into Q3.

• Real time management information tool being rolled out in H2 FY25.

• New strategic Marketing and Business Development plan now in place.

• Upgraded CRM package to be installed in H2.

• Successful hire of two new testifying experts in the period to bolster the expert witness team.

We almost believe them, until you realise every single number has gone down

When they say:

• The Board expects the Group to deliver full year results in line with market expectations.

This is currently 1.5p EPS, which they may beat with a strong H2, at least on an adjusted basis. However, H2 appears to have been loss-making last year. In terms of valuation, we just don’t think one can justify a 17x P/E for a company with this track record, even if it comes out a little lower if we cash-adjust it. Management has regularly told us they need that cash to balance big working capital swings.

First, this was a recovery play, then there was hope that COVID would generate dispute work, then that pent-up demand after COVID would come through, and now, Episode 4 - A New Hope:

The prospect of changes in global tariff policies has generated unprecedented commercial challenge for businesses around the world, and we believe our expertise and track record makes us well placed to assist our clients in mitigating and resolving these issues.

They did 5p EPS pre-COVID and had c£7m cash. But, if they were going to have any chance of recovering to those levels again, surely there would be some signs by now?

In more worrying news, their TTM DSO are nudging up again to 126 from 118. These were meant to be improving by exiting slow(never?)-paying Middle Eastern business. While we haven’t had to deploy Anexo’s metric of Years Sales Outstanding, these are still above normal commercial terms, suggesting ongoing issues with either revenue recognition or getting paid for the work they do.

DigitalBox (DBOX.L) - Completion of Acquisition

This is the key bit:

After a period of successful testing of the assets on Royal Insider, and a positive trading performance across Digitalbox's wider portfolio during H1 2025, the Board made the decision to progress with the Acquisition. The Board expects the Acquisition to be earnings enhancing in FY 2025.

Positive H1 trading and earnings enhancing. Especially as this hasn’t bounced with the wider micro cap market, where similar companies are up 20-50% in the last month or so.

The issue is perhaps that, following the strategic review forced upon them by a major shareholder, they didn’t sell the business but instead concluded that they should accelerate their growth. This means that forecasts show a jump in revenue and profitability in FY 2027, and extrapolating forward another year, their entire market cap would be covered by cash by December 2028, and that's before the upgrades they imply are incoming. However, in the short term, the investment required led to a big drop in FY25 EPS forecasts.

It seems that investors are less than convinced by this transition, and uncertainty is certain due to the exceptionally low quality of the content and the dependence on fickle search engine and social media algorithms. However, with the market perhaps fearful of a further cost increases ahead of revenue growth, and hence a further drop in near-term expectations, having positive trading confirmed seems more positive than the share price reaction. That said, the vast majority of investors shouldn't even be considering investing in a £5m market cap company due to illiquidity and governance risks.

Norcros (NXR.L) - Final Results

This is another one where the exceptionals look suspicious on first glance - how could they have maintained true underlying profit with a chunky revenue drop and presumably inflationary cost increases?

But actually, this is mostly explained by the sale of Johnson Tiles, which was operating at breakeven anyway.

There's been a long-running issue with the pension here, so this update is welcome:

1 April 2024 pension valuation agreed at an actuarial deficit of £11.7m (1 April 2021: £35.8m) with deficit repair contributions of c.£4.5m p.a. to end after June 2027

To be clear, this is a proper triennial valuation. Although the end may genuinely be in sight (apart from the longevity risks), it appears that in the short term, contributions will rise as:

The Group's cash contributions to its defined contribution pension schemes were £3.8m (2024: £3.9m).

With the company's apparent earlier strategy of outgrowing its pension deficit via acquisition successful, perhaps it is now time to focus on optimising what they have, and recent disposals seem to be consistent with that. Furthermore, they say:

The Group has also now confirmed a capital allocation framework of 1) Organic investment; 2) Ordinary dividends; 3) Complementary acquisitions; and 4) Supplementary distributions. Alongside this framework are investment guardrails of maintaining leverage below 2.0x underlying EBITDA and dividend cover of c.3.0x in addition to the strategic objectives of cash conversion above 90% and a ROCE target of 20% in the medium term.

Unfortunately, the issue here is now one of valuation. Firstly, on assets, although it is trading at a little over 1x book, but three-quarters of those are intangibles, and both working capital and debts are high, increasing risks.

On earnings, Zeus make no changes to forecasts apart from assuming net debt will be around £6m higher than previously assumed going forward. Which means forecast adjusted EPS growth is flat for FY26, then rising about 8% in FY27. The possibility of ongoing acquisitions makes excluding goodwill amortisation a dubious choice, but perhaps there will be less activity going forward.

We think a fair treatment would be to add back in half of the acquired intangible amortisation (given the track record of buying businesses and selling them for a loss, but with the expectation this will lessen), and half the pension fund contributions (given the end is in sight). That's £4.1m after tax, or 4.6p a share, leaving around 28p forward EPS. That actually leaves them looking pretty good value at 258p. However, there are cheaper stocks with this kind of debt level, but if you are positive about the prospects for a recovery in UK R&M spend, then this looks interesting.

Paypoint (PAY.L) - Final Results

Here’s the headlines:

They also say:

further significant steps towards delivering £100m EBITDA by the end of FY26.

Although there are ways they could achieve this, other than growing the core business. For example, by slowing the buyback and doing an acquisition, the net debt is only £97.4m. The share price is hardly on a demanding rating, but perhaps this will be disappointing after several years of stronger growth:

we have now established new targets for the Group for the next three years to the end of FY28, underlining our confidence in the future growth prospects of the business: achieving net revenue growth in the range of 5% to 8% per annum across the Group;

But EPS will grow faster as they leverage up further from 1.1x last year:

delivering a reduction of at least 20% of our issued share capital through an enhanced share buyback programme, consistent with a prudent capital structure and leverage in the range of 1.2x to 1.5x.

The allocation of capital to the buyback also explains why dividend growth is so anaemic - 19.6p final versus 19.2p last year. Here, they say:

The Buyback Programme will be increased with a plan to return at least £30 million per annum to shareholders and will be extended until the end of March 2028, with the target of reducing our equity base by at least 20% over that period. We will continue to review the Buyback Programme based on business performance, market conditions, cash generation and the overall capital needs of the business.

This sounds positive, but then they appear to be saying that they will buy back shares whether they are undervalued or overvalued, hence will happily destroy shareholder value if they get the chance! However, in a company of this size, institutions carry the can for poor capital allocation decisions. Smaller investors often want the company to aggressively buy back shares when they are overvalued, with a view to exiting at a higher price than they otherwise could have.

They were defending two legal cases. Here's the update:

On 14 May 2025, PayPoint and Utilita came to a settlement such that Utilita has withdrawn its claim against PayPoint. As part of this settlement, the two parties have agreed to a new 5-year contract for over-the-counter prepayment services. PayPoint’s position in relation to the claim by Global 365 remains unchanged – it is confident that it will successfully defend the claim at trial. The trial at the Competition Appeal Tribunal started on 10 June 2025.

This didn't end well, as expected:

The Group’s £15 million investment in Judge Logistics Ltd was purchased in three stages (£10 million on 21 June 2024, £3 million on 31 July 2024 and £2 million on 30 September 2024). Judge Logistics Ltd is the parent company of Yodel Ltd, a customer in the Group’s e-commerce parcel business...

The fair value ... was £2.2 million, with the £12.8 million loss recorded within adjusting items .

We’re not sure this should be in "adjusting items". If they had not bailed them out, then they would have lost the business, and that wouldn't have been an exceptional item. Another way of looking at it is that some of the parcel revenue was simply their own money recycled. This is a big loss in such a short period, almost like they threw the cash over the hedge because they couldn’t be bothered to ring the doorbell.

We also don't like their attitude in these losses:

Net corporate debt7 of £97.4 million increased by £29.9 million from opening position of £67.5 million, reflecting previously announced investments and the ongoing share buyback programme

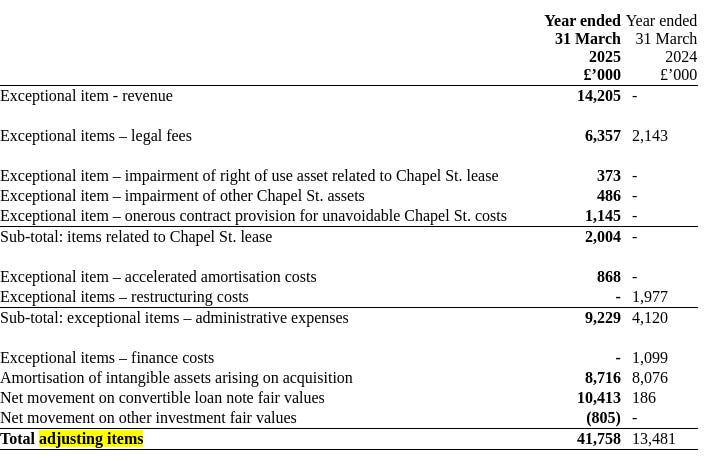

Throwing £12.8m away is not an "investment", and we’re not sure it was"previously announced". And this is just the start of the "adjusting items":

There are legal settlements and costs, and an ongoing lease for Chapel Street where they have exited the premises. There is £868k of ERP system amortisation. Who'd have thought an ERP system implementation would go wrong to the tune of nearly £1m? (Us, dear reader, us.) So rather than being…

…another year of progress for PayPoint...

Instead, it seems to have been a year of multiple avoidable mistakes and poor prior decisions coming home to roost. I think it would be prudent to assume that the nature of the business and further exceptionals will be incurred in future, with the remaining legal claim looking higher risk than previously appreciated.

The good news is that the underlying cash flow is much better than the YoY change in corporate debt suggests, which should be supportive of a buyback.

The key driver of growth is their parcel business, which is fortunate as revenue in the other segments fell in real terms. Here's the headline for parcels, which they call "E-commerce":

divisional net revenue increased strongly by 39.0% to £16.4 million (FY24: £11.8 million)

LeoInvestorUK — 08:34

That sounds great, but:

Last year it was up 61.6% YoY

Quarterly growth is +4.9% versus +16.1% the year before. YoY growth in quarter revenue (our favoured metric as there is a seasonal element) has fallen four quarters in a row, down from +80.0% a year ago to +19.4% now. Collect+ network size (dimension 1 of growth) is only up 2%, the third quarter of declining growth. Parcels per store (dimension 2 of growth) has started to fall back (both QoQ and YoY), which is bad in itself and suggests that the scope for network growth is reducing. Revenue per parcel (dimension 3 of growth) is up QoQ and YoY, but the longer-term pattern appears to be flat. Accordingly, we don't believe that their growth aspirations are supported by current trading.

Unusually, forecasts appear to include buybacks which have not yet been carried out, with Panmure Liberum saying:

…we increase our FY 27 FD EPS by 5% due to the buyback. We increase our FY 26 Net Debt (excl. leases) estimate from £89m to £145m (1.4x EBITDA), principally to reflect the buyback

Clearly that a 5% uptick in EPS is not a fair exchange for that kind of debt / leverage increase. Mostly this is because the word "principally" is doing a lot of heavy lifting - a lot of the debt increase is due to the exceptionals we detailed above, but also underlying profits are now expected to miss previous forecasts, driven mostly by lower e-commerce (parcel) growth.

But the valuation needs to be done relative to other investments, not relative to previous forecasts. FY2026 EPS is now forecast at 75.5p, rising to 90.2p the following year. That makes 785p look superficially cheap for a FTSE 250 company in the current market. The trouble is that:

The debt

Likely ongoing exceptionals or slipups

Ongoing structural decline in payments

Unsupported growth aspirations in banking and shopping

Risk of a reversal in e-commerce

It seems that with these results, PayPoint may have transitioned from a cheap growth company with a track record of beating forecasts to a financially engineered mess.

Vianet (VNET.L) - Final Results

From the way they describe it you’d assume they had grown revenue 20%:

Revenue Growth: Total revenue increased to £15.27 million, up from £15.18 million in FY24, highlighting the company's ability to drive sales amidst evolving and yet challenging market conditions.

As they don’t provide the percentage, we’ll do the maths: 0.6%. I.e. much lower than inflation

Cost-cutting, or at least declaring more of them as exceptional, and a lower tax charge, has got EPS up to around 3p, though. And capitalising less intangible asset development than they amortise means they generate cash, and net debt is down to just £0.38m.

However, Cavendish forecast EPS to fall in 2026. Making this look 2-3x overvalued at a 23x P/E. We wonder if they have got the decimal point in the wrong place in their price target of 210p. 21p would seem a better fit with the current EPS and long-term prospects for the business.

That’s it for this week. Have a great weekend!

Thanks for the Paypoint appraisal. A patient and amusing deconstruction of the company accounts.

I love this description, 'chief porcine make-up artist'. A worthy addition to my lexicon. A colleague once told me that you can't polish a t**d, but that you can sprinkle glitter on it..