Small Caps Live Weekly Summary

Fertilser Stocks MORE GATC MPAC GDP CNKS CAPD

SCL Investor Meet 23rd March

The SCL investor meet is quickly approaching so this is your last chance to get your registration in for this high-quality in-person event in the West Midlands on the 23rd March.

The event is free to attend and easily accessible by Train and Car. Make sure you check out the final agenda and register here to get full details.

Large Caps Live

So here is an idea:

The EU is due to meet around the 21st to discuss agriculture.

I think they will reduce restrictions re fallow land etc and essentially farmers will be encouraged to plant where they can – I am not sure if it will be wheat specific or include sunflowers and rapeseed (my wife points out that rapeseed and sunflower oil can often be substituted for each other). So I think there will be an increase in agriculture volumes from now on in the 'west'.

The US will also ramp up its agro-exports – and ditto Canada - and in the US / Canada, the main driver is switching between crops and also adding extra fertilisers to increase yields.

The UK will follow once the paperwork is sorted out in about 20 years.

Turkey is the largest buyer of Russian wheat. I am not entirely convinced that there will be a ‘free flow’ of wheat to Turkey this year – at least until Turkey allows Russian ships through the Bosphorus Straits and recognises the failure of its ways (resupplying drones to Ukraine).

The big issues for agro are NPK fertilisers – nitrogen, phosphate and potassium. The key one is actually nitrogen which is derived from natural gas. So fertilizer companies with a captive supply of natural gas will benefit. Those that depended on Russian supplies or export from Russia / Ukraine will be screwed.

The planting season for Spring wheat is coming upon us. Clearly, this puts extra pressure on Ukraine to settle. I suspect it may also put some modest pressure on Putin.

I think the key question is whether wheat sales from Russia to Egypt, Tunisia, Morocco, Yemen are direct or via intermediaries. The biggest traders of agro commodities are the ABCs – Archer Daniels Midland, Bunge, Cargill – and you will note that they are all American and unlikely to be too enthused trading with Russia.

I do think that as long as Germany maintains an exemption in Swift for gas that there may be a push for an exemption for wheat but even then I think there will be lots of pushback and a desire not to trade. Also, there may be issues with Brazilian harvests NEXT year.

So I spent time trying to work out which fertilizer companies are going to benefit and have scale etc. It is hard to know – as each crop has its own mix of requirements, and harvests/planting / spreading fertiliser is always weather dependent. And I am an 'agro-tourist'

Therefore, perhaps the best way to play this is as a basket of stocks. Here is what is on my watchlist following this research:

1. K&S

This is a German company - focussed on salt (remember winter snows) and potash. Even though it does not supply nitrogen fertilisers I think it will benefit from some incremental volume-based potash sales. Also, I think it is worth remembering we have not had a really bad winter for a while in Europe - K&S benefits from the use of salt on roads. Valuation wise:

Less than 1x P/TB, ROE of 57%, you can see however from this that there is often a degree of volatility of revenue and earnings:

So that table summarises the 'joys' of the agro sector!

2. Yara

Yara is a Norweigan fertiliser producer. It focussed on nitrogen fertilisers - and clearly being in Norway it has a local supply. But it is exposed to the market price of natural gas:

But what concerns me is margins - and I can't see estimates for that:

3. CF Industries

CF does a mix of H2 and N2 based products. You can see its locations on this map and it should be clear from that why I think it is interesting:

So other than the UK their main production is in the US / Canada and clearly they have the advantage of 'cheaper' gas or more importantly availability of gas. If - and I hate to mention it - we compare it with eg BASF which obviously is subject to the availability of Russian gas. This is from the BASF website:

4. Nutrien

This is the merger of PotashCorp and Agrium. - PotashCorp used to be known as the Potash Corporation of Saskatchewan - and based in Saskatoon - where funnily enough we lived briefly when I was a kid. So I have some affinity for Nutrien. As you can tell from the history/names - one of the parents was particularly strong in .....potash.

Due to the merger with Agrium they created a larger group with involvement in nitrogen and phosphate. They also have their own distribution ie outlets that sell to farmers - in the US and also I believe in eg Australia. The companies merged on 1 Jan 2018. I think that this is an interesting play as it is the first major demand cycle for the merged company

5. Mosiac

Again one that looks cheap on many metrics:

That should be a good starter for any further research.

Small Caps

Hostmore (MORE) - Final Results

Here’s the headlines:

As a restaurant chain, this is dominated by lease assets, so taking the pre-IFRS EBITDA is largely meaningless. Thankfully, they provide the pre-IFRS16 figure and we don't have to try to calculate it. This is of course still an adjusted figure, and looking at those adjustments, the big difference is listing costs. How on earth did it cost them £8.1m to list a sub £200m market cap company?! Smacks of the PE float/demerger that this was. At least these costs should be genuinely one-off.

These figures put them on a P/E of 13 and a EV/EBITDA of 5.6. This isn't crazy expensive, but isn't cheap either,

However, the FCF figure does look impressive. But the first thing to note is that this is not what we would typically call Free Cash Flow:

Free cash flow is calculated as the profit/(loss) for the period adjusted for depreciation, non-cash items, changes in working capital, tax paid and maintenance capex, and excludes cash used in financing activities.

This is not cash generated that can be used to pay dividends, buy back shares or reduce debt. To get to FCF from OCF they take off what they define as maintenance capex but not what they consider expansion capex.

Even putting aside that this split is open to considerable opinion, Mark considers this inappropriate because otherwise companies with significant growth capex, such as say Capital Limited, could claim that they generate great FCF figures. High-quality companies such as Capital don’t, of course, because that cash flow isn’t free, it is committed to growing the business.

Given the recent float, all the IFRS16 calculations, maintenance vs growth capex debate then we are disinclined to spend hours unravelling the details. The much simpler way is to look at net debt, which went from £28.6m to £12.2m; so a £16.4m reduction. However, they received £13.1m from their listing and didn't pay a dividend. So actual FCF was £3.3m.

Partly this was because they spent £8.1 on listing costs so it may be fair to add this back in. But they also received government payments in this time, although they don’t quantify this. About £1m of the FCF was due to working capital changes, so while we agree this is FCF it also isn't necessarily repeatable.

With the share price down this week, the market seems to have been able to see through the attempts to put lipstick on, what may or may not turn out to be a pig. Or it may simply be unimpressed by the outlook:

LFL revenues for the 8 weeks ending 27 February, adjusted for stadium venues, is c.3% lower than FY19

They have hedged gas and electricity costs:

Early hedging of gas and electricity costs, both volume and pricing, substantially reduced the negative impact on future margins, with recent hedging contracted prior to the start of the Ukraine crisis

But no indication for how long, and of course, labour inflation could well be challenging for them too. The CEO does say:

I am equally appreciative of the ongoing loyalty of our many guests that continued to support us by visiting our restaurants and indicated their appreciation of the improvements in quality and service which have resulted in higher and more consistent levels of guest satisfaction.

This suggests they are willing to address the fundamental issues with the business that have been evident for some time - that the reviews are poor for the core "Friday's" business, and that their offering is priced at a premium to other restaurants without offering a premium experience. Personally, Mark would much rather go to one of the independent local restaurants that provide chef-prepared food and nice wines for a lower cost.

This quote stood out to Leo:

With the combination of the permanent closure of somewhere between 15-20% of restaurants as a result of the pandemic and a growing acceptance from consumers that pricing has to reflect value...

What about an acceptance from TGIs that their pricing has to reflect value? Perhaps the Chairman could be part of the problem:

Having had responsibility for the stewardship of the TGI Fridays brand over the last five years as Chairman of Electra Private Equity PLC, I am now delighted to present the inaugural Chair's Statement of Hostmore plc as an independent listed business.

So this is good news:

It is therefore my intention to step down as planned at the Annual General Meeting in May.

However, this is a highly competitive sector, and nothing in these results changes our fundamental view: if we wouldn't eat at their restaurants then why would I buy their shares?

Gattaca (GATC.L) - Board Succession

This is perhaps a tame title for a company that has just lost its CEO and CFO!

Having joined the Group in October 2018, it was Kevin's original intention to leave at the end of this year but he felt, and the Board agreed, that given the scale of further improvement required in the business, an earlier change of leadership was in the Group's interest.

"the scale of further improvement" does not sound good and suggests he was pushed. It is an internal replacement, which has pros and cons:

In line with the Group's succession plan, Matt Wragg, currently Chief Customer Officer, is appointed to succeed Kevin as Chief Executive Officer.

Who perhaps didn't rate the current CFO?

the Board believe that the business will be best served by a CFO who can partner with the new CEO for the long term.

It may, of course, be that the CFO was planning to go soon anyway, but boards often value continuity to a clean sweep, unless things have gone wrong significantly.

In light of this, look out for the kitchen-sinking to come soon, and then perhaps a gradual recovery under the new management.

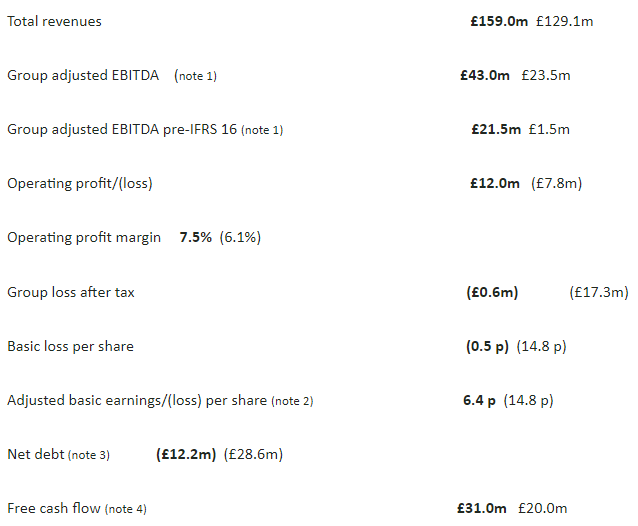

Mpac (MPAC.L) - Full Year Results

The headlines read well:

· Order intake of £117.9m (2020: £83.9m) contributing to a closing order book of £78.4m (2020: £55.5m)

· Group full year revenue up 13% to £94.3m (2020: £83.7m)

· Increase in operating margins, with underlying operating return on sales 9.3% (2020: 7.8%)

· Underlying profit before tax up 36% to £8.6m (2020: £6.3m)

· Underlying earnings per share of 39.7p (2020: 31.4p)

· Statutory profit before tax of £8.2m (2020: £2.9m)

· Basic earnings per share of 39.1p (2020: 20.8p)

· Cash of £14.5m (2020: £15.5m)

This is clearly a company that is performing well in a good sector. But this is also a company that likes its adjustments, so definitely not one where you should trust their headlines without diving into the details.

The first thing that stands out is the £2.4m of released deferred consideration. This is because Lambert hasn't performed sufficiently well for this to be paid out. It seems strange that this has been put through the income statement. We guess this is required by the accounting standards to make the accounts balance. However, we don't see the reverse - a company declaring a loss on the income statement since they agree to deferred consideration on acquisition. They did have it in the previous balance sheet, so must have been still expecting to pay it last year;

Although not all of the previous carrying value has gone through the income statement. So presumably they paid some of it, or for a different acquisition. Still, at least this "gain" is adjusted out in the underlying profit.

Anyway, with the rest of the adjustments, excluding acquired intangibles makes sense. Acquisition costs perhaps less so given that they are serial acquirers and are not providing like-for-like growth figures in their headlines. But this is fairly standard.

What doesn't seem right to us is that they adjust out pension admin costs. They have to pay for the pension administration and it is a real, ongoing cost. We can also safely ignore any moves in IFRS19 pension assets since the one that matters - the triennial - still has a deficit and they are paying recovery payments. These totalled £2.3m last year so we would adjust the other way. These payments may be reduced by the next triennial valuation but we can easily see the Pension Trustee saying you are a larger and more profitable company, we want higher recovery payments.

An underlying PBT of £8.6m becomes £5.3m "real" PBT after adjusting for pension costs & payments. A rough pro-rata-ing makes the 39.7p underlying EPS more like a real EPS of 24.4p. So roughly this is on a "real" historical P/E of around 20.

This may, of course, still represent good value. Adjusting out the pension costs actually makes the underlying EPS grow faster. And there may be a time in 5 years or so when only the pension admin costs remain. Or if we get another decade of strong equity returns and rising interest rates, where MPAC may be able to get rid of the pension scheme altogether. As we repeatedly point out though, there are easier ways to gamble on high equity returns or higher interest rates, so this shouldn't be your primary reason for investing in MPAC. It should be because you believe a P/E of 20 materially undervalues the business.

The other positive for MPAC is that they have net cash. This has gone down from £14.6m to £13.6m during the period, largely due to working capital flows. We've pointed out in the past that the working capital position flattered the cash balance and with inventories and receivables still only just covering the payables, we wouldn't be surprised if there is some window dressing here.

Order intake of £117.9m (2020: £83.9m) contributing to a closing order book of £78.4m (2020: £55.5m)

There's no doubting that's strong. If the revenue does come out at the forecast £105m then that's 75% coverage, versus 62% and 59% of the eventual outcome for 2020 and 2021 respectively. Also:

the Group ended 2021 with both a strong closing order book and a healthy prospect pipeline, providing an encouraging outlook for 2022.

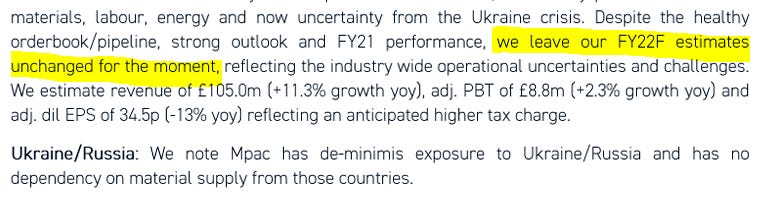

However, this must be seen in the contact of an economic outlook that has deteriorated significantly since their trading update in January. The inflation and interest rate outlook significantly deteriorated even before the invasion of Ukraine. The COVID situation has worsened overall, with UK cases now rising and China going into lockdown. The uncertainty and cost of capital are undoubtedly higher which is a particular problem for a company mostly making capital equipment.

On the other hand, the FREYR battery contract appears to be going to plan, with the main uncertainty apparently around the takeup of the particular battery technology they are working with. The immediate primary end-use of these batteries is to balance wind generation in Norway with demand, which is certainly on-trend. There is a potential explosion in requirements for grid storage in a few years when wind generation capacity will exceed off-peak demand, at least in the UK. They comment:

this project has the potential to open the clean energy sector to Mpac in 2022

Which is a very optimistic timescale for revenue and certainly not in current forecasts. Plus they have excess cash resources and there is always the potential for acquisitions. This is the best summary paragraph from them:

Our opening 2022 order book provides extensive coverage over forecast revenue, and we have again been successful in broadening the diversity of our customers and product range in the current order book. Notwithstanding the potential for ongoing uncertainties regarding Covid-19, and the Ukraine crisis, which we will continue to monitor closely, the orderbook, prospect pipeline, strong operational and management team, means the Group's prospects remain positive and the year has started on track.

Broker Shore say:

If it were not for the increased uncertainties we would likely have seen an upgrade today. But we think it would be too optimistic to assume that if things remain as they are an upgrade is certain. There will be an effect from covid/inflation/interest rates/war and there is always the chance one of their contracts could go wrong as they have in the past.

This leaves Shore forecasting flat PBT and falling EPS which doesn’t exactly scream buy for a company on a “real” P/E of around 20x. Equity Development have essentially the same forecasts but without the increased tax charge:

Given the outlook, and lack of forecast growth, the company currently looks overvalued. However, the pension deficit is not widely understood, so this is a stock that often presents training opportunities.

Goldplat (GDP.L) - H1 Results

We last looked at this microcap gold recovery specialist following its H1 operational update so the operating profit figures were already known. Here are the rest of the highlights:

• Doubling of net profit from continued operations attributable to owners of the company to £2,071,000 (31 December 2020:£1,013,000);

• As a result of increased performance, the fully diluted earnings per share for the six-month period doubled to 1.19 pence per share (31 December 2020: 0.59 pence per share), and;

• The group cash balance (net of overdraft) remained strong at £1,640,000 (30 June 2021:3,459,000).

Good to see net profits benefitting so much from the higher operating profit. Both admin costs and finance costs are below H2 last year showing good cost control. Taxation is increased but this is, of course, due to higher profits. The non-controlling interest has reduced significantly since they bought out a large proportion of their BEE partner’s interest.

Mark has a bit of an issue with them declaring the cash balance net of overdrafts but not net of overall debt. They actually have net debt of about £1m. This is because they took out a loan to spend £3.8m buying of the BEE interest, so is understandable. He just would have preferred a different presentation. Post period end they sold $450k worth of the shares they held in Caracal Gold so even without any future working capital moves, net debt will have been reduced.

Another weakness here is that net cash flow from operations is only £225k. And Mark is disappointed that they don't provide this calculation in the accounts. We know what all the figures are, so again this is just a presentation issue, but it doesn't reflect best practices. Essentially the reason operating cash flow is weak, is working capital build, where they say:

Inventories increased from 30 June 2021, by £2,601,000 as result of an increase in precious metals on hand of £3,080,000 set- off by a decrease in raw materials of £720,000. The increase in precious metals on hand and in process was driven by high turnover volumes in Ghana as well as delays we are experiencing on some of the shipping routes, whilst the decrease in raw material was as a result of higher cost per ton material processed in South Africa during the period.

Trade and other receivable balances also increased from 30 June 2021 by £3,590,000 again driven by increases in turnover, specifically in Ghana.

Trade Payables has gone up by £3.3m offsetting the trade receivables. So the real move is in inventories. Still, the bulk of this inventory (£7.4m worth) is gold being sent to refiners. This is as good as cash, (better than cash, some would say in the current environment) so isn't a concern. There are some challenges with shipping, the same as the rest of the world, so perhaps we can't expect this to reduce anytime soon.

However, we are now almost 3 months into H2 and we know from the quarterly operational results that both operations have considerable momentum, plus the gold price has been strong. Apart from a tailings dump that is planned to be but isn't yet being re-processed, Goldplat doesn't have its own resources - it is a waste clean-up specialist - so doesn't benefit from gold price rises as much as a miner. It still benefits though, as it does from sector tailwinds in the same way that Capital does: more mines = more waste = more waste processing demand.

In terms of outlook they say:

Whilst the Group's trading expectation for the remainder of the year is currently unchanged, it is worth noting that the impact of the Russian invasion of Ukraine is posing a significant challenge to the global supply chain industry. Whilst Goldplat has no activities directly connected with Russia or Ukraine, the long-term effect of the conflict on the Group is uncertain.

Broker WH Ireland haven't made any changes in their note this morning, which is simply a summary of the results. So presumably this is the 1.5p EPS from the previous note. This now looks too light, however, given the 1.19p EPS delivered in H1. Currency moves can have a big impact here due to intercompany loans, and perhaps this is a (rare?) case where an adjusted EPS calculation would be more useful. However, it isn’t hard to believe that H2 will be at least close to H1 in earnings performance. A c.2.4p EPS would mean a forward P/E of 3. This would make Goldplat one of the cheapest shares on the market, although also one of the riskiest given its sector and area of operation.

One of the disappointments of these results is the lack of dividends declared. This is something they have been flagging as a potential outcome and it is a shame not to see at least this commitment reiterated. This is understandable given the business still has net debt from the BEE buyout, and also has big working capital swings for the size of the market cap. However, if H2 shows good trading performance, the working capital flows reverse and the debt is cleared, then shareholders will become rightly impatient if a sizable dividend isn't prioritised.

Cenkos Securities (CNKS.L) - Annual Results

This is another company where the level of reporting via the RNS system leaves something to be desired. Although they do have the accounts in the RNS, we have to go to the annual report to get the notes, to see, for example, the revenue split between business units. But first, here are the headlines:

These have been well received on Friday with the share price up around 15%. Here is the revenue split from the AR:

So corporate finance transactions being up is the main driver of the increase in revenue. Unlike last year, they have managed to keep Staff Cost increases to below the rate of revenue increase, and hence the operating profit increases significantly.

Basic earnings per share have increased to 7.1p and the dividend to 4.25p. Stockopedia doesn't have any forecasts so we can't see if this is a beat or a miss. However, as strange as it seems to say this, at 9.7x P/E this is one of the most expensive brokers in the sector on earnings. Finncap is on a P/E for the year about to end of around 6, Numis on a historical P/E of 5.4 and a forward P/E of 8.8. Perhaps only WH Ireland is more expensive on earnings.

The dividend represents a 6% yield, which is good but again in line with the sector.

One of the headlines with Cenkos is the large cash balance as a percentage of the market cap at £33.5m vs a market cap of £38.9m. But this is skewed by staff bonuses accrued at the year-end but not yet paid:

So, the real cash balance is likely to be closer to £20m. Still a significant portion of the market cap but not as out of line from the sector as an initial look may suggest. On a similar basis, adjusting for working capital, Mark is expecting finnCap to have £20m+ cash at year-end vs a £50m market cap, for example. But these are businesses that have to hold significant cash balances for regulatory capital plus to survive the inevitable downturns. And with Cenkos, and others, showing a lack of willingness to return their cash balance this is largely a risk-reducing factor rather than a valuation one at this stage. And Mark would not use this to justify a higher earnings rating than the sector.

Where Cenkos do appear to be outperforming the sector though is on their outlook:

Despite the macro-environment, we remain confident in our business model and our track record of successful fundraising at every stage of the market cycle. Indeed, we have started the year well having already completed three IPOs, four placings and two M&A transactions in the first 10 weeks of 2022.

This is certainly impressive given market conditions. These IPOs have clearly been in the pipeline for some time but to not be cancelled by current market conditions is very good. Here is what they are from the transactions page on their website:

So we count that as 2 IPOS and 5 placings but have not looked into details as to why the discrepancy. Having companies listing in commodity or energy space is clearly a good place to be at the moment. We are not sure we can expect this to completely shield them from the market conditions, however. And as such, Mark is not willing to pay the current premium required to own Cenkos vs the higher quality or more cheaply-valued players in this sector.

Capital Limited (CAPD.L) - Investor Presentation

We would normally comment on a presentation following a large write-up last week, this one did reveal some interesting extra details:

On margins: EBITDA margins surprised them to the upside. Reasonable margins in strong markets is more like 25-30% - more in the higher end of the range in 2022.

On FY22 Capex: $45m capex = $5m head office and MSALABS, $25m sustaining capex, $15m growth capex in drilling, any mining services win would be additional on top of this.

On net debt: without mining services win, reasonable to assume net debt will halve in 2022. They are comfortable with up to 1xEBITDA for net debt - assume $80m EBITDA and with that they could finance a Sukari size mining services win without going to the market.

On MSALABS: Medium-term revenue target now moved up to $80m from $50m.

This last point is quite important. When Mark did a follow-up on Capital at Mello Monday in November, he focussed on two possible ways of valuing MSALABS:

The “Competitor” methodology was taking the future potential of the business and discounting it back to the present. He got a $66m valuation by taking $50m revenue in 2024, 25% EBIT margins, 10xEBIT multiple and a 12% discount rate.

Taking the now $80m potential, say 4 years out, 30% EBITDA margins then you get about $24m EBITDA. According to the appendix to the Capital results presentation, competitor ALS is on 11.4x 2023E EBITDA. Applying the same multiple gives about $270m for MSALABS in 2025 or about $175m today if we discount it back 4 years at 12%. 12% may be a bit light for the area of operation so that would be $132m if you want a 20% discount factor. So that is potentially a material increase in upside valuation that was announced in this call.

That’s it for this week, hope to see many of you at the SCL Investor Meet on Wednesday next week.