Small Caps Live Weekly Summary

Mello Trump BMS CYAN DBOX HUM KINO SNWS TRD

By now, I’m sure many will have their tickets for the UK’s best investor show - Mello - which, for its 10-year anniversary, is going back to Derby on the 19th/20th of November. If anyone is undecided, do come along. You’ll get to see some companies, meet many fellow SCLers, and watch Mark do a talk. We even have a discount code if you need something to sweeten the deal. Use code Simpson50 at https://melloevents.com/mello10tickets/

Another rather bonkers week in politics with the US election. US markets have enjoyed the Trump win, presumably assuming that a heavily-geared real estate developer is going to lower taxes and interest rates at all costs. However, many of his other ideas, such as tariffs, could have wide-reaching effects that are hard to predict or mitigate. As such, uncertainty may be far higher than investors would like to see, which would be reflected in much higher risk premiums for equities.

For those new to the SCL weekly summary, the following is a summary of the debates we have had this week on our SCL discord server. These are an amalgamation of many viewpoints, and while Mark & Leo are probably the most active, there are other voices in here, too. This means that these views should not be attributed to one person, and indeed the aim is to provide a balanced opinion (unless something is obviously a poor business on a high rating when we’ll say so.) The aim of these summaries is to encourage knowledgeable investors to join in the debate and generate contrary viewpoints. So, if you disagree, great - come and join the debate on Discord.

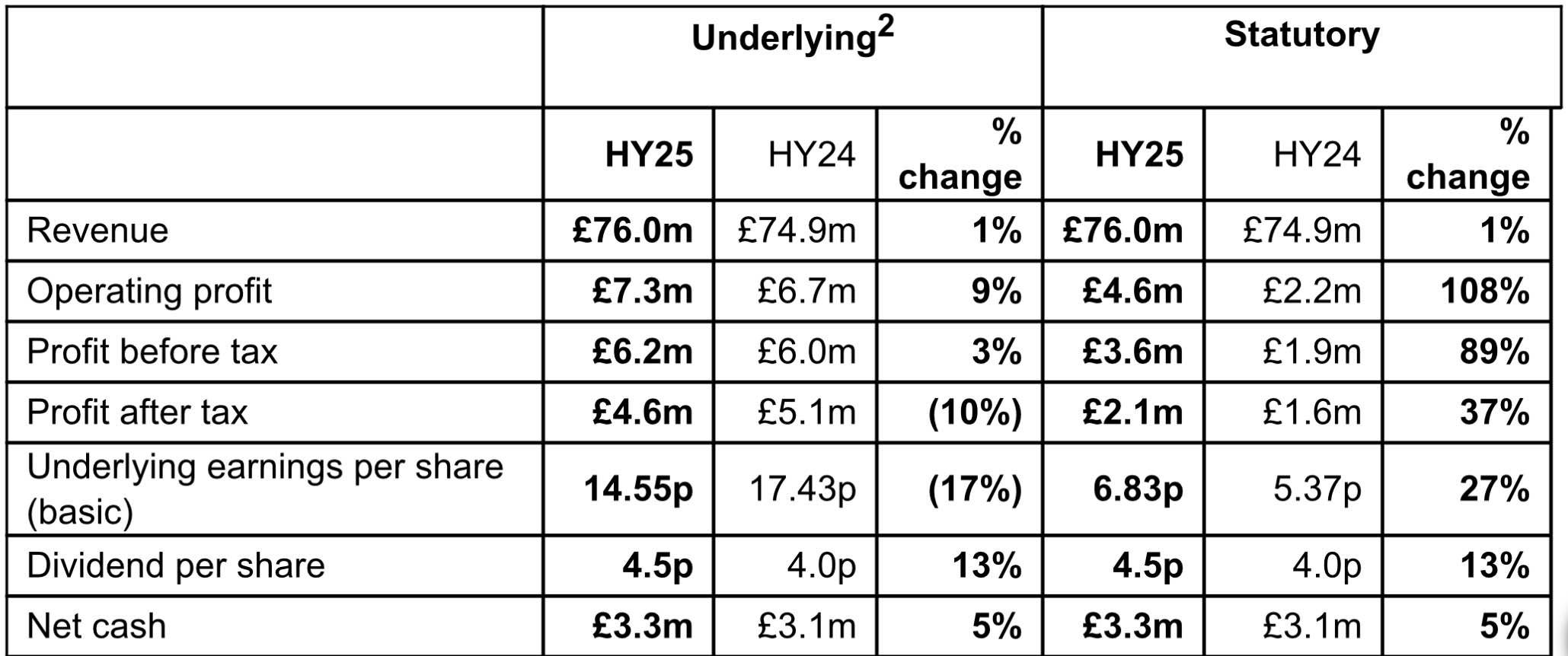

Braemar (BMS.L) - Interim Results

These look like a steady ship, operating profit is up, but EPS is down:

Perhaps somewhat a relief to shareholders who have been a bit underwater here recently due to the FT naming Braemer as one of 37 companies allegedly not doing enough to clamp down on Russia’s shadow fleet of oil tankers.

The (uncovered) transactions also show how lawyers and shipbrokers, including London-listed Braemar, facilitated the purchase of the vessels, which led to the enlargement of Russia’s fleet.

And, brokers cut forecasts just prior to these results for the Employer’s NI increase. The company now say:

Braemar remains on track to meet its stated objective of doubling FY21's underlying operating profit on a sustainable basis and is on course to meet market expectations 1 for FY25.

With:

Solid growth in the Investment and Risk Advisory segments more than offset a weaker Chartering segment, helping to drive overall Group performance and deliver HY25 revenue 60% higher than HY22 when the strategy was implemented.

However, in this week’s update, they say they are trading in line on the basis of:

Consensus at the time of this announcement: Revenue £152.7 million (£150.8 million - £154.7 million), Underlying operating profit (before acquisition-related expenditure) £17.8 million (£17.4 million to £18.4 million)

Whereas on 19th September, they say they were in line on the basis of:

Company compiled consensus as at the date of this announcement: FY25 revenue of £153.2m and FY25 underlying operating profit (before acquisition-related expenditure) of £18.1m

So basically, they have been walking down forecasts to remain in line. The suspicion is now that they sneaked in the effects of chartering revenue weakness into the profit downgrades they blamed on the budget. Management seem to be consistently “delighted” by these results, which seems a stretch given the forecast trend.

These downgrades are made worse by the ability to drive a bus between the adjusted and statutory measures:

The Group has separately identified certain items that are not part of the underlying trading of the Group. These specific items are material in both size and/or nature and the directors believe that they may distort the understanding of the underlying performance of the business. Specific items included within operating costs mainly relate to the impairment of a right-of-use asset relating to an unused portion of the Group's leased office space following the termination of the related subleases.

Acquisition related costs are primarily employment costs relating to the treatment of the consideration for the acquisition of Southport Maritime Inc. (USA) and post contractual costs relating to the Madrid team. Other items include a gain on the revaluation of the embedded derivatives and a foreign exchange gain relating to the convertible loan notes issued on the acquisition of the Naves business.

Acquiring teams and paying up-front bonuses is the way of the industry, but it seems that excluding these costs as exceptional may be a stretch as teams switch between brokers regularly.

The market didn’t seem to mind the downgrades, as the price was modestly up. With Edison having them on a forward P/E of 6, if you trust the adjustments, it may well be that the market was fearing much worse. They also gave a nice interim dividend increase with these results, which many UK investors tend to use as their primary valuation metric.

Cyanconnode (CYAN.L) - Interim Results

We don’t know this particularly well, as it has been loss-making in the recent past. However, these results are surely a disappointment for something expected to grow so rapidly:

· Revenue of £5.6m (H1 FY 2024: £5.8m)

· Operating loss of £2.1m (H1 FY 2024 loss: £2.2m)

Broker Zeus keep their £34.5m FY revenue forecast which means the company have to do £28.7m in H2. Over five times what they did in H1!

The company says:

CyanConnode's order book has demonstrated strong growth, more than doubling during this period from 6.3 million units at the start of the year to 13.1 million units. Our current backlog stands at 9.7 million units yet to be deployed, having increased substantially from 3.5 million units at the end of March 2024, with a significant portion of this expected for delivery in the second half of FY 2025. Historically, our revenue recognition is heavily weighted toward the final quarter of our financial year, as order completions and deployments often peak near year-end. We expect this seasonal trend to continue, with a substantial proportion of this year's revenue materialising in Q4.

But the metrics here are confusing, and it has even confused their house broker, Zeus, who say:

The company remains confident in meeting revenue expectations since its backlog has risen over the period by 177% to £9.7m.

Of course, a £9.7m backlog doesn’t really dent the H2 revenue expectations. However, it is 9.7m units, not £9.7m, and given they have historically been priced at around £13/unit, this isn’t so far-fetched. Other companies would presumably call the backlog an orderbook. Cynaconnode’s definition of an order book appears to be total orders, including those already delivered since company inception. Which is, of course, a bonkers way of looking at it.

Their units presumably look like this from a quick Google search:

I.e. full of electronic components with various lead times. So why is there no increase in inventories if they intend to deliver 5x the number of units in H2 than they did in H1?

Shipping 5 times the product would surely have other implications for the company's working capital, dwarfing the current £3.7m cash balance. All in all, it raises significant questions about their ability to deliver the number of units they need to meet their forecasts and break into profitability.

DigitalBox (DBOX.L) - Acquisition

…agreed to acquire certain online assets, including all associated intellectual property, of the Entertainment Group of GRV Media Ltd ("GRV"). A three-month transitional services agreement with GRV comes into effect from today to support the integration process.

No figures are given, apart from 3% of DBOX’s revenue, so about £80k. With that minuscule turnover, you’ve got to hope the associated 8 employees are part-time! This is non-core and probably loss-making for the sellers. So we’d guess any payment will be in the form of a future profit share, hence the lack of any figures mentioned in the announcement.

This is exactly what DigitalBox like to do - add a load of cheap niche sites to their ad stack and immediately generate a revenue uplift. However, even if they are successful at this, this acquisition is immaterial. And so it should be. The board shouldn’t be signing off on any acquisition expenditure or commitments during a period when two of the major shareholders are clearly after a short-term exit at a significant premium to the current price and have forced a strategic review to get it. Anything that doesn't help them get that exit should be off the table.

Hummingbird Resources (HUM.L) - Q3 Results & Debt-for-Equity swap

Lender Coris Bank Coris has finally lost patience with Dan Betts and called an end with a debt-to-equity swap at 2.67p, as is their right when a company can’t make its scheduled repayments. The Q3 update shows why:

The Group recorded an adjusted EBITDA loss of approximately US$3.83 million for Q3-2024, marking an improvement from the US$16 million loss in Q2-2024. This recovery can be attributed to higher gold sales and price, increased production at Kouroussa and enhanced operational efficiencies at Yanfolila.

If they can’t make money with $2700/oz gold, then there are very serious problems. Despite this outcome, Mark still thinks this was worth the punt, as it was by far and away the most geared play on the gold price out there. If they had managed to meet the mine plan, this would have been a 5-10x return versus what looks to be a 60% drop from here. Management simply couldn't deliver operationally, and they and shareholders have paid the price.

Kinovo (KINO.L) - Trading Update

I am pleased to report on a robust first-half trading performance, with strong bottom-line growth and a resilient topline performance when considering the deferrals to some of our planned works.

They had to bring out both the “R” words. Robust and resilient, oh dear! Revenue down 3%, EBITDA up 10%, mainly due to higher gross margin.

Stockopedia has £71m forecast for the FY, meaning they have to do £41.5m in H2, which looks like a stretch. Some of this may be timing booking revenue:

The previously deferred planned works are now also coming onstream and our pipeline of new works remains strong. Consequently, and whilst revenue outturn will partially depend on resultant mix of works, the Group's trading for the full year nevertheless remains in line with the Board's expectations.

But it sounds like they are setting us up for the possibility of disappointment, even if they are not yet disappointing us.

Smiths News (SNWS.L) - Final Results

Financial performance across FY 2024 ahead of market expectations

Which is a beat of 3% on revenue, 3% on PBT, 1% on EPS, the latter affected by rounding. Cash beat by £2m, and the closing position was a better indication of the average than last year due to timing considerations. In addition to the regular dividend, there is a 2.0p special costing £4.8m.

Inline outlook according to the statement, and we note:

91%*** of existing publisher revenue streams secured subject to contract to 2029, providing the Company with stability of and visibility over revenues across the medium term

Versus 6 months earlier:

Major contract renewals with 74% of existing publisher revenue streams secured until 2029

However, as they imply, their medium term is just 4-5 years, and they don't have a long term. Regarding updated forecasts, they have been reduced for the NI changes, but the impact is less in the second year, suggesting greater cost savings (maybe lower pay increases) than previously expected. Cash forecasts reflect the special dividend but appear to support the continuation at around the 2.0p level, barring acquisitions or heavy new investments. A 2027 forecast has been introduced, showing stable to slightly increasing profitability, but of course, the real question is what happens with volumes and renewals as we approach 2029.

Objectively the £140m market cap will be too much for a newspaper distributor in a few years’s time. It seems the company plans to remedy this by returning much of that as cash dividends before physical newspaper production and distribution becomes unviable, which Reach recently said they expected to be around 2032.

Smiths aim to have diversified their business into something else by then. While we are consistently impressed with their ability to take costs out faster than the decline in revenue. We are unimpressed with their ability to diversify their business away from newspaper distribution so far.

While Reach and National World have obvious ways of diversifying and have been aggressively pursuing these avenues (with mixed success), so far, Smiths has managed to find a minor sports drink to distribute along with the papers. As Tandem shows, the market for large warehouses that are not custom-built for the big distribution players is minimal.

Objectively, this should be on a lower rating than Reach or National World, which have obvious diversification out of physical newspapers. However, that it trades at a premium to National World probably says more about the significant undervaluation there, than overvaluation here.

Triad (TRD.L) - Half-Year Report

Some decent growth here, and a welcome return to profitability after many years in the wilderness:

Management are…

…extremely enthusiastic about the outlook. Our interim results reflect the Company as it currently stands, without being run 'hot' in the pursuit of short-term profit. The level of spare capacity is carefully judged to enable new business to be accommodated quickly, as soon as it is won. We have no hesitation in acquiring the finest new staff and covering their salaries and costs in anticipating future growth.

However, the Executive Chairman always is, so perhaps the best that can be gleaned from this is that costs are going up. The reality is that this is an IT recruiter/contractor and, as such, should be nowhere near the 2-3x Sales or 30+ P/E that the market currently rates it at. Especially as it is not exactly a beacon of corporate governance, with family members of the Chairman the main non-exec hires in recent years.

That’s it for this week. have a great weekend!

Thanks for publishing these - very interesting. I've been lurking on Substack for a while but am only now starting to get to grips with it.

CYAN Your summary on CYAN - and especially the question - what's up with the inventory? Great Question. Has caused me to spend many hours down a rabbit hole. And I came out with some interesting findings. At least I think so.

Short answer [1] CYAN outsourced manufacture. [2] Inventory is primarily long lead components (US chip) [3] previous end of life buy for old gateway chip was expensive [4] now shipped and inventory holds more much less expensive new chips [5] some of H2 demand has been advance manufactured - 567k units shows up in current contract assets. I estimate they probably made 1.2m units in H1 with 0.6m shipped (comparing order back logs and new orders) and that H2 mfr production needs to be around 1,3m units - based upon a £10,/unit price for a round number. Which still may too high - I suspect more like £7 or £8? But thats a guess. Likely they are paid for modules separately from deployment of meters and commissioning of network. Then moves to service revenue at low level but high margin,.

Note that if FY26 orders arrive at the anticipated volumes they will need to keep advance manufacturing so still a squeeze on working capital - and need to commit to volumes in time for their manufacturing partner to install additional production lines to meet contract deadlines. Tough balance - esp as end customer for all these meters is the Indian government. Not noted for rapid payment - but also desperate for the networks so eventual payment you can take to the bank (factor)?

I added more details to this rabbit hole on my CYAN post on the recent interims not sure it shows up in searches yet - link is

https://substack.com/@illiswilgig

Apologies - I am very slow generating readable thoughts and my substack is primarily for my own benefit and I am unaccustomed to publishing. Hope to get more practice soon,

Seems to be a good substack small cap community developing - long may it continue,

Mark (Allery) @Illiswilgig

I really enjoy these weekly updates, thanks for publishing them :-)