Small Caps Live Weekly Summary

Mello 2026 PAY PMP RFX RCH

A reminder that to avoid wasting our and SCLers time with spam bots, the only way for new members to join the Discord server is via the Small Caps Live website. This will be instead of direct invites via Discord. All genuine investors are still very welcome to join in the discussions.

A short and late summary this week due to travel, but just time to remind everyone that hot on the heels of a successful Mello Birmingham, the best UK investment conference for meeting company management (in our opinion) returns to Chiswick next month, on Tuesday 2nd and Wednesday 3rd June. The lineup is already looking very good:

Many SCLers will be making the effort to be there. Tickets are currently on General sale and will move over to Final Release on 12th May. Even better, we have a 25% discount code for you: SIMPSON25

Here’s a selection of what we discussed this week. (Remember this is a summary of many opinions, and isn’t the view of any one commentator; check out the actual discussion on Discord if you want the nuance of the different opinions.)

Paypoint (PAY.L) - Resolution of Claim

This sounds like bad news:

The CAT has:

Found PayPoint liable for an historical infringement of competition law, which ceased in 2018, concerning certain contracts under which it provided energy OTC prepayment services;

However, this is the last of two legal cases resolved, and the amount awarded is small:

Awarded damages of £169,334

Especially compared to the initial claim:

Importantly, the CAT’s findings confirm that PayPoint’s past contracts with energy suppliers were not a significant factor in G365’s lack of success. G365’s initial claim was for £172.2 million – meaning that PayPoint defeated more than 99.85 per cent of G365’s claim value.

So this usefully removes a risk factor.

As they were found liable, Paypoint are unlikely to recover any legal fees, but these have been expensed as incurred, probably a minimal amount in the current period. We wonder if they have to pay the other side’s fees, though:

The tribunal may apportion costs based on issues won or lost, rather than awarding 100% of costs to the overall winner, as seen in cases where a party only succeeds on specific grounds.

So hopefully they only have to pay 0.15% of the amount.

Portmeirion (PMP.L) - Preliminary Results

Given our previous commentary, we immediately scroll to the going concern statement:

Given these factors the Directors also acknowledge that conditions outlined in the going concern scenarios represent a material uncertainty which may cast doubt over the Group’s and the Company’s ability to continue as a going concern

As background, covenants for the RCF were set in August 2024, breached, relaxed in September 2025, then breached again in March 2026, delaying the results. A waiver has now been agreed for March/April 2026, with a formal relaxation from May 2026, allowing results to be published on a going concern basis.

However, these covenants will again be broken if revenue is more than 9.5% below target, with damaging cost-cutting at the -7.5% level. We usually see stress tests relative to the previous year or other known figures, but here the target is unknown, with no clue from their broker, either.

However, surely the government will have to support this sector given multiple recent failures. Given that Portmeirion has helpfully fixed their energy costs before the attack on Iran, it is unclear whether they will benefit from any assistance, but what would be ideal would be a low-cost liquidity loan so that they can restructure without undue time pressure or being bled dry by the banks.

The investment risk here still looks very high. It is a relief that the covenants have been relaxed, although clearly this could have happened sooner and would not have caused a delay in the results. There are a number of actions that should improve liquidity, also mentioned in this week’s update:

Inventory write down £2.9m (& being carefully managed so the product doesn’t get dumped in Korea & ruin one if their best markets)

US Tariff claim of $3m

Potential sale of Wax Lyrical (with the potential to wipe out the debt)

Potential sale & leaseback of Trantham Lakes property valued at £11.7m (on books for £5.2m)

So, unless faced with a liquidity crisis, the asset backing should ensure good returns for lenders and equity holders from here.

Ramsdens (RFX.L) - Trading Update

It seems the 18th March update was indeed conservative when they said:

the Group now expects its profit before tax for FY26 to be at least £24m* and, if the favourable gold price and trading conditions continue, potentially up to £28m.

Despite the gold price immediately falling and never fully recovering, they now say:

the Board now expects its profit before tax for FY26 to be at least £28.5m* and, if the favourable gold price continues and summer currency volumes are in line with last year, potentially up to £31.5m.

Cavendish calculates this to be a 19% EPS upgrade, but this time they have also applied it to the following year:

Given the continued strength in the gold price combined with the strength in the underlying business, we increase our FY27E PBT forecast by 19.1% on higher precious metal and pawn broking profitability, but – given the prevailing gold price – we see further upside risk to this and our FY27 forecasts, which assume a nine-carat gold price of £32/g, which is materially below the prevailing price of c£42/g.

So we now have a current year forecast of 63.2p falling to 44.7p the following year. We should be very cautious about assuming that 44.7p, or even 2025’s 36p, represent normal earnings in a flat gold market. This statement from the broker doesn’t really fully describe the dynamics here:

While much of this upgrade is due to the purchase of the precious metals business, which has benefited from prevailing gold prices, we note the continued strength in the jewellery retail and pawnbroking businesses.

In fact, the other two strong sectors have been very significantly benefiting from the gold price, and all three will suffer (after varying lags) when it stabilises or substantially falls:

Much of pawnbroking uses the value of gold in items as security. Obviously, more will be lent when customers suddenly have more security to give. And in a significant number of cases, pawning something is a direct substitute for selling it, paying a fee for the effective option to buy it back for economic or sentimental reasons.

Much of the jewellery sold contains gold, and so for the same number of units/weight sold, revenue will be naturally higher. Furthermore, profits will be higher because significant amounts of second-hand jewellery are bought at a significantly lower gold price.

This is also problematic from the broker:

we believe that a sum-of-the parts approach represents the fairest way of valuing Ramsdens

In fact, this is a highly integrated business. Most obviously, cash FX would be loss-making and worthless if it had to bear the store costs alone. Sales staff can push customers toward pawning jewellery or selling it; the former virtually ensures the customer will return, giving an opportunity for another transaction with the same or another item, whereas selling it offers a much greater, but one-off, benefit. Management can decide how much jewellery bought is retained for sale at higher margins or melted down for a quick profit. Only the FX card business conceivably has standalone value.

This makes the company exceptionally difficult to model from a valuation perspective, but here’s one possible way:

Share Price 445p

FY 2026 63p FY 2027 50p

Effective share price 332p

Sustainable EPS 30p => Underlying PE of 11x

This doesn’t make the company expensive, but it also prices in either further significant gold price rises or ongoing growth from their store roll-out, both of which have risks as well as opportunities.

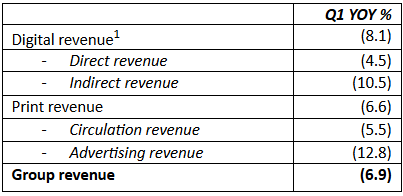

Reach (RCH.L) - Trading Update

This is an in-line update:

We remain confident in delivering the reduction in operating costs, and are on track to deliver in line with market expectations for the full year.

However, it contains scary LFL revenue trends:

So we are not surprised to see the market take fright as digital revenue falls faster than "legacy" print revenue due to Google’s AI transition, and despite economic uncertainty hitting print advertising revenues.

That’s it for this week. Have a great weekend!