Small Caps Live Weekly Summary

ARB SMRT HAT NBI BOTB

Large Caps Live Monday 9th August

We had a special guest again on Large Caps Live - The Boatman Capital joined us to talk through their latest report on Argo Blockchain.

While we don’t always agree with everything that sceptics write, a sceptical view is often more valuable than the usual unquestioning commentary from brokers and the like. The basics of the report are:

(1) Frank Timis was an early shareholder of Argo Blockchain.

(2) Argo bought some land in Texas. There is some degree of vagueness as to whether it was 320 acres or 160 acres or 160 + options on 160 acres.

(3) The land came with a deal to provide about $100M of debt - but that debt appears not to have been drawn down.

(4) The land appears to have an appraisal value of around $168k - not the multi-millions it was purchased for.

(5) The seller is DPN LLC - which is a Delaware company and we cannot tell who the beneficiaries are.

(6) But there is a hint that the ultimate beneficial owners of DPN may be shareholders of Argo depending on the interpretation of an SEC filing.

Here’s what The Boatman Capital had to say:

Argo's Texas land deal raises all sorts of governance issues. Not least of which is, who benefited? It is scrubland in the middle of nowhere. We thought it a little odd someone would pay up to $17.5m for it. So we got some formal appraisals done and, sure enough, Argo appears to have overpaid a bit. Like by 100x.

There is an electricity substation next to Argo's plot of land and that is why they are building the mining facility there. I believe there is a wind farm nearish to the facility and the argument is that Argo will be able to use excess capacity.

[For sceptics]…the big fly in the ointment will be the proposed 3rd quarter 2021 US listing. Do you believe the land deal will scupper the US listing cos if it doesn't and bitcoin is flying being short ARB is surely fraught with danger knowing how absolutely crazy US investors are? The listing will go ahead. It's only ADRs. This company needs to keep pushing out the good news because it's not doing much mining.

According to H1s released today, Argo's prepayments for mining rigs was £35.4m. Revenue was £31m. These are unsustainable businesses. About 40% of the fleet is leased from Celsius Network, which seems to be quite a big player in the crypto sector. Argo was also managing Celsius's own fleet. But that arrangement has gone sour. Lawsuits alleging breach of contract and seeking damages. These machines have a 2-3 year lifespan so turnover is very quick. That's a lot of CAPEX going obsolete very quickly. Even with record bitcoin prices earlier this year, none of the miners were making much money. It's an arms race.

Concluding:

I think until that US ADR listing is out of the way, Argo is a really dangerous short. I've no doubt it is a con and have felt that way for a long time (I took part in the IPO, funnily enough, before dumping them all at 20p sadly!) But timing is key, and with US ADR's soon upon us, they will be pulling out all the stops to raise as much as they can to keep the farce going on. And if US investors buy the story, which no doubt they will if Bitcoin is still high, then Argo could easily rise a lot further from these levels. Hopefully, will be much easier to get a good borrow then. After that, all bets are off and it becomes a great short based on everything you have in that report along with the crypto bubble bursting.

Small Caps Live Wednesday 11th August

SmartSpace (SMRT.L) - Trading Update

When a couple of investors presented this at a recent Mello Monday event, they were very keen on the growth in recurring revenues and the possibility of management repeating the trick of increasing ARPU that IIRC they were successful in doing at DotDigital.

One nice thing about recurring revenues is that you can take the terminal month's value, and the attrition and get a base forecast for the following year. In the H1 trading update SmartSpace do this for you:

Forward looking Group Annual Recurring Revenue ("ARR") as at 31 July 2021 up 28% in the 6 month period to £3.8m (up 51% since July 2020)

The interesting thing though is that this is the first time I've seen them do this. From the last update:

· Full year revenues expected to be approximately £4.6m (FY20: £5.1m)

So the spin here seems to be accelerating, a bit of a red flag.

Half year revenues expected to be approximately £2.5m (HY20: £2.3m) of which 63% is recurring revenue (HY20: 45%)

So, revenue is hardly up. But some of this is low quality/margin hardware revenue, so perhaps not a concern. What I do find concerning is the lack of growth in customers and locations.

Locations up to 7,003 (31 Jan 2021: 6,741) and customers up to 4,747 (31 Jan 2021: 4,735) as SwipedOn target higher value multi-location customers

Clearly, they're pushing us towards looking at locations. This is also what I first looked at a year or so. I was not impressed and the situation has got worse:

Note this is not a log scale, so In percentage terms, it was already decelerating, now it is decelerating in absolute terms. So, what about ARPU?

Monthly Average Revenue Per User ("ARPU") up 22% in the six-month period to NZ$111.8 (£56.1) (HY20: $85.3 (£42.8))

Given that the number of locations per user has increased, this doesn't seem very impressive.

An analysis of the markets they operate in suggests they are an also-ran in a crowded market. So, I'm not sure they have scale, nor are they likely to gain it. So even if they get APRU to 100s of (NZ) dollars then they are going to struggle.

Cash as at 31 July 2021 totalled £3.4 million (31 January 2020: £4.5 million).

So, loss-making, growth slowing and losing market share, you'd still pay 1 x Sales for this company right, which gives an upside of.....<checks stockopedia> -90%....oh! This looks like it could get quite nasty from a share price perspective, especially if they need to raise more money.

H&T (HAT.L) - Interim Results

Profit before tax £4.7m (H1 2020: £5.0m), a robust performance against a background of Covid-19 related trading restrictions from January to April and reduced high street footfall throughout the period

That looks pretty impressive on first sight. Although Q2 2020 was closed completely, whereas Q1 2021 might not have been quite so closed. Really, 2019 should be the comparator. In the 2019 H1 results they said:

Profit before tax up £0.5m, 7.9% to £6.8m (H1 2018: £6.3m)So, normalised earnings are perhaps much higher than 4.7-5.0m.

But:

The net personal loans book reduced significantly to £3.4m (H1 2020: £10.0m) in line with our plans. Other than a small sample of loans written as part of the s.166 review, no High Cost Short Term ("HCST") loans were written in the period. Non-HSCT lending continues at modest levels, with £1.0m lent during the period (H1 2020: £3.3m).

So, some of that 2018/2019 profit was from effectively outlawed lending and won't come back. And this could still come back to bite them:

As previously advised, the Group has been working with the Financial Conduct Authority (FCA) to undertake via a skilled person, a review of the credit worthiness, affordability assessments and lending process within its High Cost Short Term loan (HCST) business since 2014.

Amigo Loans got into serious trouble in this area.

FX profit reduced to £1.0m (H1 2020: £1.3m). Transaction volumes were down 56% and aggregate transaction value reduced by 45%. Transaction volumes in the period were at c23% of pre-pandemic levels with signs of a modest recovery during May and June. We expect this recovery to continue as foreign travel begins to re-open over the summer.

The big question is whether it will ever recover to pre-pandemic levels. Well, actually, the big question is why you would buy significant amounts of foreign currency cash before going on holiday anyway. Everywhere takes cards nowadays and it is often cheaper to use a cash machine there, even without a specialist FX card .

The other question is whether it is possible to move upmarket on the jewellery side:

Since the relaxation of restrictions progressively during April, retail sales have significantly outperformed in terms of volume, value and margins. Online originated sales in May and June have grown in line with overall sales levels, and currently represent approximately 16% of total sales by value (H1 2020: 16%).

Retail sales for the period overall were up 26.5% to £12.4m (H1 2020: £9.8m), generating gross profits of £6.7m (H1 2020: £2.8m). Strong demand in particular for high quality watches enabled us to release provisions held in accordance with our normal accounting policy, against previously slow-moving stock items. Headline gross margin of 54% (H1 2020: 28%) reflects this dynamic. Underlying gross margin excluding provision movements was 46% (H1 2020: 41%), reflecting both business mix and strong demand for high quality pre-owned watches and jewellery.

The implication is, yes. The other side is Gold sales/purchases. Both do better when the gold price is higher - if it has gone up then stuff people were selling anyway (including jewellery) is worth more, and people want to buy into a rising trend.

Gold purchasing profits reduced 53.6% to £1.3m (H1 2020: £2.8m) on sales of £8.0m (H1 2020: £9.6m), a reduction of 16.7% and primarily reflecting reduced transaction volumes from January to April 2021. At 16%, the margin on purchased gold has moderated back closer to historic norms after the positive impact in 2020 of a higher gold price (H1 2020: 29%, H1 2019: 17%).

So I do see a future for the business, with jewellery sales making up for lost FX. But for H&T liabilities from historical issues would worry me. And remember this is exactly the sort of thing that the likes of Stockopedia won't account for in their ratings...and so in today's market, they may not be factored into the valuation.

Northbridge Industrial (NBI) – Pre-close trading Statement

We’ve looked at Northbridge in the past. Firstly in #scl-2020-10-02 where we liked the load bank part of the business but thought the oil tool rental business in Australasia was struggling and a little out of place. Then in #scl-2021-04-14 when they announced their intention to sell Tasman Oil Tools and we said:

the unknowns are a) how much they will get for it, b) if they will cut central costs by the same amount.

Otherwise, they may end up with a better overall business but similarly unprofitable. Maybe one to retain on the watchlist until more details are known.

Well, it seems they are now firmly profitable and the trading statement is a positive one:

Trading Ahead of Expectations

Again, Crestchic is bearing the load (pun intended):

The Crestchic factory remains at full capacity and the order intake continues to be strong. Sales and service revenue for the period was £7.1m which is up by 19% on 2020 (£6.0m). Sales to the US and data centres worldwide remain strong.

Being at full capacity is a nice problem to have and they have received planning permission to increase their factory space in Burton upon Trent for H1 2022. The only headwind has been commodity pricing, affecting margins slightly:

Although Crestchic is managing to pass on most of the cost increases seen from the rise in commodity and shipping prices, the supply chain disruption experienced in 2020 is continuing to slightly affect margins as a consequence of extended assembly times.

Tasman has not shown similar strength though:

Revenue for H1 2021 was £3.8m which is 25% lower than H1 2020 (£5.0m).

They have managed to get it to close to break-even though:

Despite rental revenue not recovering as quickly as anticipated earlier in the year, the business has been resilient, and prudent management of the division's operating and capital expenditure has restricted the loss before tax to £0.2m and has seen it generate a positive free cash flow.

It really is the right thing to separate the businesses. There is little synergy. Of course, the risk is that they are selling Tasman at the worst possible time - when it is trading badly and the ESG focus means that oil majors are not investing in new fields at anywhere near previous levels. That it has taken this long to sell the division, doesn’t give me much confidence that they will get much for it, however:

We are taking steps to restructure the Tasman Oil Tool Division to return it to profitability and, in parallel, are actively negotiating with potential buyers for the Division.

This to me has the smell of a subsidiary that will be sold to the existing management of the business for a fairly nominal fee, that will be largely deferred.

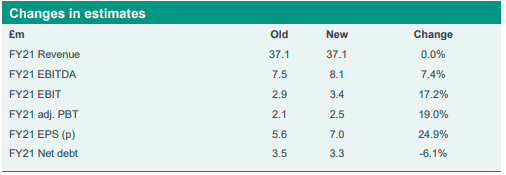

For those expectations we turn to Equity Development:

The outlook remains similarly impressive, particularly within Crestchic, and as a result we have increased our estimates, with adj. PBT rising to £2.5m (from £2.1m previously).

So EPS has gone from 5.6p to 7p. Since the share price this morning is c113p which is 16x earnings. This falls to about 15x if you exclude the £0.2m loss from Tasman from the earnings, assuming someone can take this off their hands.

ED have no forecasts beyond 2021, but with their factory capacity-constrained, then growth will be positive but perhaps not spectacular in 2022, and this has proven to be a cyclical business to some extent.

So 15x forward earnings looks about right to me even with positive trends at Crestchic.

Equity Development have a peer valuation someway above the current price:

Making a conservative assessment at this time that ignores the huge EV/Sales disparity and simply eradicates the 33% average discount on other metrics, would suggest a fair value of 152p / share.

Which sounds good, until you release their chosen peers:

Aggreko, Ashtead, Caterpillar, Herc Holdings, HSS Hire, Speedy Hire, United Rentals and VP Group.

I suspect that the management of each of these companies would be quite insulted if you said to them “I’m invested in your peer, Northbridge”!

Apart from HSS Hire – which has been an indebted high-risk stock for years, I would rather own all of those large, diversified, equipment rental companies than Northbridge at the same valuation.

Crestchic does have manufacturing as well as hire revenue though so this perhaps should give them some rating advantage against pure hire companies. But again having a $100b+ market cap Caterpillar in there as a comparator just looks daft.

Small Caps Live Friday 13th August

Best of The Best (BOTB) - Trading Statement

I'm going to take this line by line, and touch on the background as relevant.

Best of the Best PLC (LSE: BOTB), the online organiser of weekly competitions to win cars and other lifestyle prizes, provides the following trading update for the 15 weeks ended 8 August 2021.

So that's since their 30th April year end.

At the time of the Company's Preliminary Results announcement on 16 June 2021, we indicated that trading had softened since the COVID lockdown ended on 12 April 2021.

At the time they said:

We are excited about the opportunities that the year ahead holds for BOTB, with a recovering economy and hopefully a return to normality. However, in contrast to the summer 2020 period, we have experienced somewhat of a reduction in customer engagement since the latest easing of lockdown restrictions on April 12, 2021, specifically relating to the understandably long-awaited re-opening of hospitality and non-essential retail. We are closely monitoring this, but with our flexible model, growth strategy and plans for the year ahead, we expect customer engagement to return to normal levels before too long. I look forward to updating shareholders in due course.

That's my emphasis. Of course, the word "normal" is key. If they return to "normal", pre-covid levels then they still look very expensive. Presumably, they were hoping to return to some kind of "new normal", "permanent plateau" etc.

Today they go on to give lots of detail:

Below we outline what has happened to the three customer cohorts since that update:

1. Existing customers, signed up prior to May 2020 remain loyal and engaged but with their newfound freedoms, the distractions of major sporting events and ability to travel, they are generating revenues c.6% lower than during the final 15 weeks of the financial year ended 30 April 2021. Despite this, revenues generated by these existing customers remain higher than in the 12 months pre-pandemic, and now form c.50% of the total.

So of course, the question is whether those final 15 weeks of FY 2021 were representative of the year as a whole, or represented the high point.

2. Customers signed up between May 2020 and Apr 2021 (during the Pandemic), representing c.40% of total revenue have performed well and in line with our normal models and expected behaviour.

My recollection is that the pandemic started before that, but of course, they have aligned to their financial years. By "expected behaviour", what they are presumably talking about is higher attrition of relatively new customers. I've looked and I can't really tell. That's two of the last 15 weeks of FY 2020. Clearly, the higher the levels of attrition, the harder it is to stand still, and the more they need to spend on advertising.

It is the third group where they are really having difficulties:

3. In line with many other businesses, the cost of acquiring new customers has significantly increased in recent months with the cost per thousand impressions (CPM) on social media platforms - which account for two-thirds of BOTB's marketing spend, increasing by up to 60% compared to previous levels. Combined with the aforementioned reduced levels of engagement post-lockdown, our variable marketing investment has therefore not yet increased in line with our budgeted forecasts but has cautiously remained in-line with the prior period. As a result, new customer revenues (registered within the last 15 weeks) are c.40% lower (accounting for a 9% fall in total revenue) than during the final 15 weeks of the prior financial year. Importantly, new customers acquired in recent months have performed in-line with previous customers, but we have simply registered fewer of them for the same levels of marketing investment. We are monitoring our marketing costs and returns very closely and remain ready to increase investment as soon as market conditions improve.

So the effect is:

New customer revenues (registered within the last 15 weeks) are c.40% lower (accounting for a 9% fall in total revenue) than during the final 15 weeks of the prior financial year.

Perhaps from this, the attrition could be calculated? There has been lots of talk of low barriers to entry here and more recently emerging competitors. It may be that the lower engagement that they have put down to the end of the lockdown is actually due to these competitors, and will only get worse. But what is certain is that these competitors are bidding up ad-words prices. To reiterate:

the cost of acquiring new customers has significantly increased in recent months with the cost per thousand impressions (CPM) on social media platforms - which account for two-thirds of BOTB's marketing spend, increasing by up to 60% compared to previous levels.

Recall that in the past they got "free advertising in two ways":

1) Presence at airports - now all closed

2) Publicity for winners in local newspapers.

In the results they commented:

Whilst the COVID-19 restrictions in place during most of the year significantly curtailed the ability of our presenting team to surprise winners at home or at work, we were pleased that the video calling alternatives available were well received by our players and continued to provide the engaging content for which BOTB has become so well regarded.

So, perhaps with the end of lockdown will come more opportunities for promotion from surprising winners. This is probably not local TV material, and perhaps the newspapers are getting wise to this, but it may make for some great viral tic-tock videos.But they have still given up their only physical presence, and although clearly airports are bad news at the moment, this puts them in the hands of search engine and social media monopolists.

In combination, these factors have resulted in a c.15% reduction in average weekly sales for the first 15 weeks of the new financial year, compared to the final 15 weeks of the prior financial year ended 30 April 2021. It is worth noting that the summer months are typically a low point and there is a seasonal lull in customer engagement and revenue generation, which we expect to improve over the coming months.

With our substantially fixed cost model, this will have a disproportionate impact on margins, profitability and earnings for the financial year ending 30 April 2022. Whilst still substantially higher than the pre-COVID comparative and the results delivered in FY 2020, these are now anticipated to be c.57% lower than what was reported for FY 2021. The new guidance the Board is providing today for the year ending 30 April 2022 is c.62% below current market forecasts with a commensurate impact on the following financial year. However, should revenue trends improve, it can be expected that the reverse would occur and margins and profitability would increase materially due to the nature of the business model and the operational gearing.

So that's the flip side of operational gearing. Other companies that have done well have higher variable costs including performance-related pay. They said before they expected things to "normalise".

Again, how conservative these guesses are all comes down to how strong the comparators were.15% down on an all-time peak last 15 weeks of FY 2021 is NOT conservative. And also about the basis for the forecast being that revenue trends continue (i.e. the down 15%).

We are hopeful that the cost of acquiring new players will normalise before too long and our flexible model means we are able to adjust to a higher cost of new player acquisition if necessary. Notwithstanding this, we remain focused on our growth strategy which together with new initiatives, the ongoing engagement of our large and loyal database, and a return to more normal patterns of customer behaviour should allow for profitability to increase and for margins to recover.

I don't like my management being "hopeful". And again, nobody knows what "normal" is / will be. I thought they were madly overpriced even at £20, and from then on things just went crazy...for a while. But it is important to note that they'd come off significantly in advance of today's statement, and not just because the formal sales process was ended.

How to value? Clearly, this is exceptionally difficult given the wide variance in possible outcomes. So let's look at a brokers note. This is what finnCap say:

So what would you say normalised EPS is there? 60p? Given the regulation risk, which I would say is even higher than the spreadbetters, perhaps a P/E of 10 is justified? So a valuation of 600p.

One more thing. Why would the management guide forecasts high, when:

Best of the Best PLC (LSE: BOTB), the provider of online competitions to win cars and other prizes, announces that it has been informed by the Selling Directors that, further to the announcement made at 6.00 p.m. on 31 March 2021 (the "ABB Announcement"), they have successfully sold a total of 2,469,352 Placing Shares at a price of £24.00 per Placing Share via an oversubscribed Placing. The Placing Shares in aggregate represent approximately 26.6 per cent. of the Company's issued share capital prior to the exercise of options.

The board are still in place and so perhaps they are now in it for the long term. In which case setting expectations low and consistently beating them would be the right approach. So, if you like the company and are not worried about regulation, 800p might be quite attractive.

Have a great weekend everyone!