Small Caps Live Weekly Summary

Mello ARC CCT COM CTO ECEL FA. SDI VTU

Mello fever is well and truly us as Mark is busy preparing his talk, and Leo his famous company write-ups and “mini-guide.” It seems a limited number of tickets are now left, but SCL subscribers can still take advantage of our discount code Simpson50 which gives 50% off tickets.

https://melloevents.com/mello2023tickets/

Arcontech (ARC.L) - Appointment of Consultant

The strange thing about this announcement is that it appears to be a full RNS, not an RNS-Reach:

…announce the appointment of Stuart Roberts, owner of Sprada Pte Ltd, in a consulting capacity for Singapore with immediate effect.

We struggle to see this as material news, unless you consider that for a company with a PAT of £600k, the cost of hiring anyone means this is a profits warning!

Character (CCT.L) - Half Year Report

Despite the repeated warnings about the H1 numbers, they are still pretty shocking when compared to last year:

Sales are down over 30%. Given inflation, volumes must have halved for the period. So they barely break even in their typically strongest half. Leaving them to do all of the forecast 20p EPS in their weaker half. Yet somehow:

Overall, the Board is, accordingly, confident of the prospects for the second half and continues to expect that Character's profitability for FY2023 will be in line with current market expectations*.

The reason they give for their confidence is that:

Whilst the conditions remain challenging, the Board has a strong belief in the current product line up. The success of Heroes of Goo Jit Zu continues and is supported by other lines, including the influencer inspired Lanky Box and Aphmau products which are also featuring well in our sales numbers. In addition, the scheduled release of the new "Turtles" movie in August 2023 bodes well for the launch this summer of the Teenage Mutant Ninja Turtles line of products that we are distributing in the UK and Ireland."

Is Goo Jit Zu really still going? Is the 1980s revival still going? Will a film to be released in August really save the figures to August?

Current trading appears to still be poor:

Since the Group's trading updates issued in October 2022 and January 2023, trading conditions have continued to be challenging across all the Group's markets.

There’s a risk of them blaming the weather soon too. Colder and wetter weather doesn’t sell outdoor toys. While this is obviously out of their control, it isn’t going to help an already struggling business. To hit their full-year EPS, they must have slashed costs by now, but there’s no mention of this in the narrative. The one thing they never seem to cut is board pay!

In any case, the current valuation is not predicated on an H2 recovery giving FY EPS of 20p, but a recovery to the > 40p seen in most previous years. They seem miles away from that.

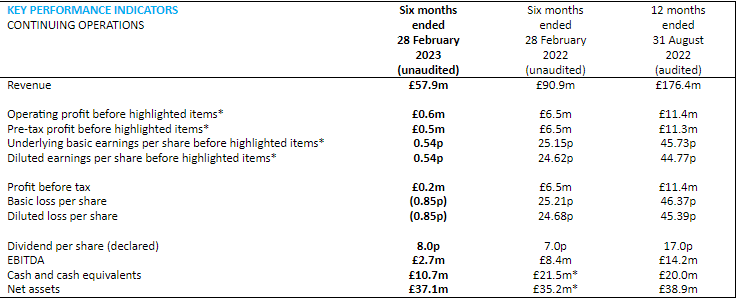

Comptoir Group (COM.L) - FY22 Results

Got to say we are a little underwhelmed by these results:

· Adjusted EBITDA* before highlighted items of £6.3m (2021: £6.4m).

· Cash and cash equivalents balance at the period end of £9.9m and a net cash position of £7.7m (2021: £7.1m).

· Basic EPS of 0.48 pence (2021: 1.34 pence).

They are not too bad in isolation and they had government support in the previous period, but these were the H1 results:

· Adjusted EBITDA* before highlighted items of £3.4m, up by 112.5% (Restated H1 2021: £1.6m)

· IFRS profit after tax pf £946k (H1 2021: £1.2m loss)

· Net cash and cash equivalents at the period end of £8.2m (H1 2021: £ 6.2m; 2 January 2022: £7.1m)

· The basic earnings per share for the period was 0.77 pence (H1 2021: basic loss per share 0.98 pence)

So an adjusted EPS loss for H2 which contains Christmas, a period you’d expect to be stronger for casual dining. Mark was expecting them to do similar EPS in H2, so 0.5p EPS vs 1.5p is quite a difference. On top of this, net cash is down, not least because of £1m exceptional costs related to board changes.

There is a large cash balance here compared to the market cap, but TBV per share is only 4.1p due to negative working capital and lease liabilities exceeding assets. Given this is a highly illiquid microcap, with a controlling founder, and casual dining facing severe short-term headwinds, this doesn’t seem that cheap at 7.5p to buy.

T Clarke (CTO.L) - Trading Statement

The Board is pleased to report that trading in the second half of the year has continued strongly and that the Group's financial performance for the full year is in line with market expectations…

The Group is expecting to achieve its target turnover of £500m in 2023.

This bodes well for future trading:

Our order book has now increased to £555m (2021: £534m).

And useful for them to provide average net cash, given that the balance sheet hasn't always looked the strongest here:

our average month end net cash during FY2022 was £2.6m

So a P/E of 6x. and a yield of 4.3%. Forecasts were for a tiny increase in EPS on an increase from £410m to £500m turnover, although some of this will be down to tax. Also, that jump is quite big compared to the increase in order book. However, they did beat on revenue, at £425m, and the order book is clearly multiyear so timing will vary.

Cenkos 2022 adjusted EPS forecast increased from 19.0p to 19.3p, but 2023 from 19.7p to 18.9p on a higher interest charge. We have seen brokers for a number of companies reduce forecasts due to a higher interest rate charge recently, but the process is far from complete. There are also quite a few companies that stand to benefit from higher rates. The dividend forecast for 2023 raised to 5.89p, so a 4.5% dividend at yesterday's close.

Overall a reassuring and positive update for those that had done their sums on interest rates. We just wish the board weren’t so generous with their pay since they could afford to pay a much higher dividend if they paid in line with similar-sized companies.

Eurocell (ECEL.L) - Trading Update

Group sales for the four months to 30 April 2023 were down 2% compared to a very strong equivalent period in 2022.

That doesn't sound too bad, given the macro conditions. This bit has perhaps done the damage, though:

We have continued to offset input cost inflation with selling price increases and surcharges. However, lower volumes and resin prices are driving increasingly competitive markets for our products, resulting in margin pressure.

And they now say:

Taking the above factors into account, we now expect adjusted profit before tax for 2023 to come in below current market expectations

Eurocell-calculated analyst consensus profit before tax forecast for 2023 of £22.0 million.

The already low rating appears to have assuaged the fall somewhat, with the shares only down 12% or so in response to this statement:

If we assume a 15% miss and a 25% tax rate, then we get around £14m PAT vs £18m forecast. So on a P/E of just 9 on a bad year. But without updated broker forecasts, then we are largely flying blind. And the market perhaps fears further profit warnings to come. TBV PS is around 94p, so could represent a good entry point for a company facing challenges but is still profitable.

Fireangel (FA.L) - Contract Win

The contract, which is valued at an estimated £1.5 million, will be delivered over the next six months, commencing this month. It includes the supply of over 60,000 Connected smoke and heat alarms, which will be installed in over 5,000 properties.

Given their track record of delivery, one could be forgiven for thinking they’ve missed a word out, and it should say “will attempt to be delivered”

The big problem is the location of the customer in the Middle East, where payment terms are often very extended. If this is covered by the UK government-backed export financing, then it could help keep the lights on until the fundraise.

Leo has had a look at this, as it comes up a lot, and the potential hurdle is a requirement for 20% UK content. How this 20% is measured is wilfully undocumented - perhaps all that is required is to make a 20% margin or ascribe 20% to design or software for what is a 100% foreign-made product.

If not, then experience elsewhere shows it could take a long time to get paid, so at best, this will just be a non-cash transfer from inventories to receivables and, at worst, be the final straw.

SDI (SDI.L) - Trading Update

Subject to finalisation of the accounts and audit, we expect revenues to be approximately £69m (FY22: £49.7m). We are also pleased with the contributions from acquired businesses LTE Scientific (acquired July 2022), Fraser Anti-Static Techniques (acquired October 2022), and a full year's contribution from both Scientific Vacuum Systems (January 2022) and Safelab Systems (March 2022). Adjusted Profit Before Tax2 is expected to be in the region of £11.8m (FY22: £11.8m), in line with current market expectations1.

This looks like a beat in revenues and a tiny beat in PBT. However, our instincts told us that this sounded like a mild profit warning for FY24:

Whilst we have previously highlighted to the market that the Atik PCR OEM sales were of a one off nature, it is disappointing that there are not likely to be any more PCR camera or other product sales to this customer; we have adjusted the FY24 outlook

So it makes sense that brokers have downgraded:

That’s quite a downgrade from progressive. And finnCap’s EPS comes in even lower:

But it is all a bit of a mystery. In presentations, the company were saying that there were no further PCR orders for Atik, so why would brokers have anything in for FY24. This week we get a revenue upgrade for the other parts of the business, leading Progressive to upgrade revenue and finnCap to keep it the same despite the removal of PCR revenue. But the guidance of higher costs, including marketing and R&D leads to the earnings downgrade. So this appears to be more about cost inflation than PCR, in reality.

Also, the two brokers are telling two different stories. Progressive that margins will be lower in 2024 due to higher cost base / R&D, finnCap that margins will be lower because acquired business are lower margin than the Atik covid sales were. The former is suspicious because it is a positive spin, and the latter is suspicious because surely finnCap wasn't expecting covid sales to continue this long, let alone forever. Perhaps the truth is that margins from recent acquisitions were lower than expected?

And are they running out of good businesses to buy at modest valuations? We have been critical in the past of the multiple creeping upwards for acquisitions. Management claims it is because they have also acquired freehold property and adjusted that out, but don’t add back in the rent they save. They either don’t understand this nuance or are choosing to misrepresent it.

Given the big cut in expectations, the fall in share price here has been relatively light. This is a shareholder favourite that receives a lot of love, and that sentiment shifts slowly. Forecasts do not include future acquisitions, and they have a strong record pre-covid of beating them. And indeed, post-covid FY2023 is coming in far ahead of original forecasts, albeit likely because of unexpected further covid orders at Atik. The trouble is that the company may have to issue more shares to make further acquisitions which means they need a high rating to make the sums work. They issued more shares pre-covid, and the debt taken on this year leaves them pretty well geared, suggesting they will need to do so again or hold off acquisitions for a year.

And we agree that it is a decent company, just that any fair value multiple needs to be applied excluding the impact of the earnings of Atik cameras for PCR applications. This means basing it off the now 7.5p forward earnings consensus. If we assume 15x is fair value, then the shares should be trading at just over 110p, some 25% below the current price. Lower if you include net debt in the calculation.

One group who don’t seem bothered about paying the current 22x forward P/E (debt adjusted) is the directors, two of which bought £10k each this week. However, this is about 1% only of the almost £1m CEO Mike Creedon cashed in last year, selling his entire holding at 165p. Directors have been massive net sellers at these levels for years, and a couple of small buys aren’t going to change that.

Vertu Motors (VTU.L) - Final Results

Revenue came in 1.2% ahead of Stockopedia expectations. PBT was a 1% beat. However, the March & April trading update is less straightforward than last year. They say:

The Group delivered a trading profit above prior year levels in March and April 2023 ("the post year end period") despite the impact of significant cost headwinds driven by inflation, with Core Group gross profit generated up by £4m compared to prior year. The overall improvement in profitability was driven by the contribution from the Helston acquisition completed in December 2022.

We don't know whether LFL profits are ahead or behind, but:

Like-for-Like revenue growth was delivered in the post year end period, predominantly due to continued strong growth in Motability new vehicle sales volumes.

Overall this is far stronger than we had previously hoped for:

The UK used vehicle market has remained resilient, whilst continued stability of used vehicle prices is exhibited. Like-for-like volumes of used cars sold by the Group declined 8.4% with gross profits per unit up.

Also, aftersales is strong:

Like-for-like the Group delivered improved gross profit from all aftersales channels in the post year end period compared to last year.

Given the annualisation of the acquisition, perhaps 2024 forecasts now look a little light?

The Board is very optimistic for the future, with confidence in the Group's ability to deliver on targeted acquisition synergies, a robust order bank, and encouraging trading results in the first two months of FY24.

However:

The Board anticipates that full year results for FY24 will be in line with current market expectations.

Despite the guidance, Zeus have slightly upgraded:

Trading in the first two months of FY24 has been strong, so we edge up underlying PBT estimates by £1.0m to £48.0m

They take a more independent view than Liberum (they have specialist sector coverage), and their forecasts have often been ahead.

The increased dividend shows some confidence in future cash generation, 2.15p vs the 1.86p stockopedia consensus:

The reported results reflect a strong profit and excellent cash performance, both ahead of expectations. As a result, we have chosen to propose a significantly increased final dividend, delivering a 26.5% higher dividend for the year as a whole. The business is in a healthy financial and operational position to further develop and gain from the benefits of scale as sector consolidation continues

The real story is indeed around cash here.

Free Cash Flow of £54.3m in the Year (FY22: £44.4m) reflecting excellent working capital management.

Active portfolio management strategy expected to deliver a further c.£9.5m of assets disposals in next 12 months, £3m above book value.

One of our fears was that their management of the pension scheme would come back to bite them. However, the accounting surplus is down but not as significantly as we have feared. For the first time, they have acknowledged that there is actually an actuarial deficit which is the first step to managing it properly.

On valuation, Zeus elaborate:

Last night’s closing price of 58.0p is below TNAV per share of 65.3p at 28 February 2023. We forecast this to grow to 73.6p per share by the end of FY24. In our view, TNAV per share should be seen a floor to the share price because it is effectively the value on a breakup basis. TNAV also only captures assets at net book value, but property price appreciation and value as a going concern means that the realisable value of these assets may be higher, as evidenced by the 30 April 2023 disposal of the Group’s standalone accident repair operation in Newburn, Newcastle upon Tyne at above net book value.

Excluding the “fake” pension surplus we calculate TBV (TNAV) as 64.6p as of the year end. We are pleasantly surprised that the TBV has remained this high after the Helston acquisition, no doubt helped by strong cash flow during the period. Zeus expecting this to rise by a further 8.3p in FY24 despite 2p+ dividends, and any buybacks means that free cash flow is expected to be well over 10p/share in the period.

These forecasts are conservative if current car market conditions continue.

That’s it for this week. Have a great weekend!

re VTU and pension, the statement says the following:

On the accounting valuation basis the scheme is in surplus. Different valuation assumptions apply to the accounting and actuarial valuations such as the use of corporate bond yields rather than gilt yields to discount liabilities. The impact of the Scheme's hedge being related to the actuarial position rather than accounting value generated a reduction in the accounting surplus of approximately £4m over the Year. A further reduction in surplus arose relating to movements in the applicable inflation assumptions. Overall, a net actuarial loss of £6.0m was recognised in the Statement of Comprehensive Income for the Year. The accounting surplus on the scheme decreased to £3.2m as at 28 February 2023 (2022: £9.1m).