Small Caps Live Weekly Summary

Happy New Year! ARB HARL POLX

Happy New Year!

The period between Christmas and New Year tends to be a strange time for small cap markets, characterised by two types of events. The first is that tips from well-followed investors tend to cause spikes. Providing picks for the year is all part of the fun of the markets, and it can be good to see where others see the investment landscape in 2023. However, in terms of actual investing action, these spikes are usually best sold into rather than bought. Tip buyers tend to be ill-informed and short-term in outlook; hence, these price rises often quickly mean-revert.

The second type of event tends to be the profit warnings where companies hope investors are too satiated with mince pies to notice. So while we retain our festive cheer personally, we hope you’ll forgive that this week’s summary is, by nature, a little gloomy.

Small Caps

Argo Blockchain (ARB.L) - Transformational Strategic Transaction

Unusually for Argo, there's no hype in the headline. By any definition, this deal is both transformational and strategic in the context of the time-to-live for Argo. Ideally, they would have stated that they now won't "become cash flow negative in the near term and would need to curtail or cease operations.", but certainly, they have delayed judgement day.

Clearly, hosting facilities have the possibility of alternative use apart from crypto mining, thus the willingness for a third party to buy it. However, most alternative uses would require high capacity and low latency internet connectivity, which this may not have as this is not a requirement for mining. They also require low electricity costs.

As the owner of Helios, Galaxy intends to enter into a fixed-price power purchase agreement ("PPA") with a licensed retail electricity provider to procure electricity for the facility. The hosting agreement provides that Argo will have access to this electricity at the PPA rate.

This suggests they were previously buying electricity in the spot market and this is not considered by Galaxy a viable way to continue.

Argo will collaborate on designing a curtailment strategy in order to participate in certain demand response programs offered by the Electric Reliability Council of Texas, which manages the Texas power grid.

This suggests there is a shortage of electricity at times. While this is the hallmark of any well-run grid, given that many industries/consumers can easily cut consumption if so incentivised and it is a poor use of capital to provide excess capacity at all times, there is evidence Texas have taken things too far:

Time: U.S. Declares Texas Grid Emergency in Arctic Blast

Austin American-Statesman: 'Marginally better': Texas power grid still vulnerable to extreme weather

NRDC: A Tale of Two Grids: Texas and California

Some estimates put the deaths due to that event at 80 people. Unfortunately, mining is not a good candidate for load shedding beyond a few hours a year because of the extreme capital cost and depreciation of mining equipment. As with battery manufacture and other capital-intensive 24-7 operations, crypto mining is best powered by hydro which typically does have excess supply 100% of the time:

Argo plans to refocus its efforts on growing and optimizing operations at its two data centers in Quebec, which are powered fully by low-cost hydroelectricity.

In addition, Galaxy will provide Argo with a new asset-backed loan in an aggregate principal amount of $35 million (£29 million) with an initial term of 36 months. This financing will be secured by a collateral package that includes 23,619 Bitmain S19J Pro mining machines currently operating at Helios and certain machines located at Argo's Canadian data centers.

So how much would you lend and for how long on mining rigs? The S19J Pro consists of a number of submodels, so it is difficult to say (provided hash rates may help, but power consumption is also key), but apparently, Galaxy is valuing them at $1500 each. This is brave.

Unless Galaxy is stark raving mad, this loan security will be subject to frequent revaluations with a requirement on Argo to post cash collateral when the LTV exceeds a certain level.

Argo has agreed to ... provide certain additional collateral for, the financing.

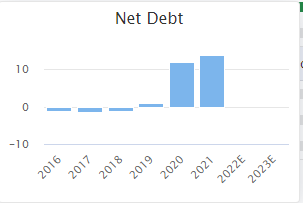

Effectively they have turned much of their non-cash depreciation charge into a cash outflow, the timing and magnitude of which are highly uncertain. So we think it is pretty clear how this will end, short of shareholders stumping up more cash.

Harland & Wolff (HARL.L) - Trading Update

This has been a big winner in the last three months:

Much of the rise is in response to being awarded preferred bidder status on a large MOD contract, and guaranteed revenue certainly should put them on a firmer footing. However, a quick look at the stockreport shows a company that has so far failed to capitalise on their opportunities and has been issuing shares and taking on debt:

The £70m forecast revenue seemed to suggest a turnaround was on the way. Although if the forecast in stockopedia is to be believed, they were also going to lose £21.9m on that revenue! They need to deliver a least 50% more than that to break even. So in that context, today's profits warning is not great:

The Group previously announced in its interim results on 30 September 2022 that it expected to achieve revenues of between £65m and £75m in FY 2022. As a result of the issues detailed above, which have led to material deferments in December 2022, the revenue out-turn for FY 2022 is expected to be materially below expectations at between £29m and £31m.

Quite some miss there! There are three issues:

a contract value of £55m and contractual payments spread across FY 2022, FY 2023 and FY 2024. Whilst work on the contract commenced in August, the Company has not been able to undertake certain key workstreams during the fourth quarter of FY 2022 due primarily to a lack of material availability and specialist Original Equipment Manufacturers' parts, which have been impacted by global supply chain issues. As a result, management expects approximately £20m of revenues from the M55 contract to be deferred into H1 FY 2023.

...certain other clients within the cruise and ferry market to either defer their contracts into 2023 or reduce the scope of works. As a result, management estimates the loss of revenues on this account for the fourth quarter for FY 2022 to be between £8m and £10m.

The Company has also decided, in mutual agreement with Saipem, to terminate the contract for the fabrication of four wind turbine generator jackets for the offshore NNG Project.

1. and 2. are deferments (the management hopes), and 3. is subject to cost recovery discussions with the client (although if they haven't delivered, then it probably depends on how much the client wants the unfinished product.) Normally, we'd be pretty sanguine about revenue recognition missing an end-of-year deadline since these timelines are effectively arbitrary. You have to be careful of the type of postponement that sees the broker cut this year and next year, which clearly presaged bigger issues at Pressure Technologies recently. However, generally, a shareholder shouldn't care which accounting period the profitable business has revenue recognition in.

The problem here is that such revenue recognition does matter for going concern statements. And a company losing a lot of money, with net debt and negative working capital (which for companies that deliver large projects is a red flag) means that getting that going concern may be a little tricky.

To complete existing contracts and to deliver the potential contracts they are the preferred bidder for, they need extra debt facilities:

On 9 November 2022 the Company announced it had executed a term sheet with Astra Asset Management UK Limited (Astra) for a £70m facility whilst working together to increase this to £100m. Following the announcement of Team Resolute's Preferred Bidder status for the FSS and a review of the potential contracted order book for 2023 and 2024, the Company and Astra are jointly working to further increase the new facility to between £150m and £200m. As the Company executes larger contracts, it believes that it is crucial to maintain a significant quantum of liquidity with a larger committed facility that can be drawn down as and when needed.

Up to £200m is an unbelievable amount for a £29m market cap company that is delivering about £30m of revenue this year. In light of this, the share price being only down 21% today looks an under-reaction.

However, this debt level means that equity is just a slither of the future capital structure here. If the management can profitably deliver these contacts, agree these massive debt facilities without dilution and collect the cash, then the equity returns could be very good.

It remains massively risky, though. The failure to agree the debt facility increases would see equity holders wiped out, either by insolvency, an emergency rights issue or a debt for equity swap. So this is, at best, a punt. But it could be a good punt. However, the presence of a still enthusiastic Twitter trader base means better entry points will likely be had in the future. Perhaps when we see the state of the balance sheet to 31st December and the going concern statement?

The company clearly missed a trick by failing to raise equity when the share price spiked to 25p at the end of November. Perhaps they were advised that they couldn't raise then, given the risk to these contracts that have materialised. The recent appointment of Liberum, in addition to Cenkos as a broker, suggests that they are certainly considering raising equity going forward. And, if we were their banks, we'd be demanding that equity provides at least some of the required capital rather than the banks taking all the risk of an industry and management with a poor track record for almost none of the upside.

Polarean Imaging (POLX.L) - FDA Approves XENOVIEWT

Some good news from this beleaguered biotech:

Polarean Imaging plc (AIM: POLX), the medical imaging technology company, announces that the U.S. Food and Drug Administration ("FDA") has granted approval for its drug device combination product, XENOVIEW. XENOVIEW, prepared from the Xenon Xe 129 Gas Blend, is a hyperpolarized contrast agent indicated for use with magnetic resonance imaging ("MRI") for evaluation of lung ventilation in adults and pediatric patients aged 12 years and older. XENOVIEW has not been evaluated for use with lung perfusion imaging.

The failure to get FDA approval in 2021 in the year caused the share price to fall from over 100p to 40p:

The share price had settled around the 50p level. After an initial spike up to almost 80p on the announcement, the price is now back to only around 10% above where it was prior to approval. These are very different markets to 2021! So this could represent a good entry point for a de-risked stock.

However, a check of the StockReport shows that this remains a massively speculative investment:

At £123m market cap, it trades at 15x 2023E sales. In their last results, they say:

Net cash of US$22.7m as of 30 June 2022, which, based on strategic decisions, could finance the Company into 2024

We assume those strategic decisions involve making most of their staff redundant! Realistically, this does not yet have a path to cash flow positive with their current capital. Which means they will be back to the market sooner or later for extra equity capital. So despite this week’s news being a positive step, and some interesting technology, the market will be looking to the upcoming equity raise rather than actual trading, which will remain limited in the near term. As such, the lack of reaction here looks rational.

That’s it for 2022. Happy New Year, and see you all in 2023.