Small Caps Live Weekly Summary

Airlines PMP KMR BSE SHI SYS1 CAPD

This is going out early this week, we are not expecting any great news on Friday, Leo is on holiday and Mark is preparing for his wedding, so may need the time on Friday! On Thursday, we did a Capital Ltd. scl special, so check that out at the end if you follow the company.

Large Caps Live Monday 12th July

I know we have touched on airlines before and clearly, they are still in my sights. However, it seems to me that there is some risk/realisation that if we have to ‘live with Covid’ ie we never get it completely under control then it will put people off travelling ……. Which goes back to what happens in the next few months.

I was looking at a comparison today and I noticed the following:

I can’t remember ever screening and finding 3 – 4 companies, all in the same sector, with Piotroski F-Scores of 1 – 2. Details of Piotroski score are here. Of course scores such as Piotroski are backward facing e.g.

I must admit when I look at the above list of factors that make up the Piotroski score I am actually stunned that some airlines managed to score 2 and not zero. But the above brings up an interesting point – how do quant funds adjust? If you are a quant fund manager you have two choices – either stick to your algos or make adjustments based on your insights / intuition / gut feel (also known as dabbling). Usually investors pay quant funds NOT to interfere with their algos. So I am willing to bet that airlines (and other similar companies eg cruise liners / hotels) have been underrepresented (or maybe even shorted) by quant funds and a lot of other investors that have scorecards or other screening mechanisms.

Indeed I have known investors who will not invest in (go long) stocks with a low Piotroski score or a low Altman Z-Score. Without knowing anything about the future path of Covid it seems to me entirely rational that Piotroski scores (and other fundamental tests / factors) will improve rapidly over the next year. This of course is always with the proviso that we do not find a Covid variant which is resistant to vaccines. The second point with the above is that I think regional travel ie within the EU or within the US will open up prior to international / interregional travel ie LON – NYC or Madrid to Latin America. This clearly means, if I am right, that IAG is the slowest to recover. Furthermore on the above table IAG looks the weakest on both Altman Z-score and Piotroski.

It is however also worth remembering that in a ramp up in business airlines benefit in getting money from customers prior to the costs ie the flight. Obviously this hurts when revenues fall due to Covid. But if / as we ramp back to normality there is a chance that airline balance sheets recover much faster – and I would suggest that long haul flight airlines who have tourists (in particular) book further in advance probably recover faster.

Of course your biggest single expense is leases - and though people go on about load factors it seems to me that the key is load factor X price. In the peak season you might charge 2 -5x what you charge at the nadir of an annual cycle. So you pay your money and take your bets.

I think it is worth going beyone our shores and looking at Lufthansa:

So we can see from the above that even by the end of 2022 there is no expectations that it will return to 2019 revenues. Lets compare that to eg IAG:

So for LHA the market is expecting that 2022 will be 73.9% of 2019 revenues. For IAG it is expecting 75%, And for Air France – KLM – 74.8%:

So for the major international carriers the expectation is that 2022 will be about 75% of 2019 revenues. Similarly for Easyjet 2022 revenue is 82.4% of 2019 revenue. In the ones I have looked at so far there is one stock that stands out – Ryanair:

Partially this is due to a year end effect (March instead of Dec) – so I have used 2023 numbers but they are 4% above 2020 numbers (again trying to adjust for the March year end). i.ee 2 years hence, the market expects Ryanair to do 104% of the revenue it did in the year BEFORE Covid. I accept the year end; and moves of GBP vs the EUR might be impacting Ryanair. But I am still left scratching my head whether there is something Ryanair specific or whether expectations for the company’s recovery are greater than for its peers? I also accept that Ryanair is intraregional and not interregional. But will Ryanair substanially outperform Easyjet? Seems unlikely.

Small Caps Live Wednesday 14th July

Portmerion (PMP.L) – Trading Update

Before we go into today's trading update, some background: Leo used to hold, but sold out in 2019 citing the negative earnings forecast trend, high valuation, low structural growth, cyclicality, risk of low-cost competition outside key products and lack of book value cover.

The company is unusual in that it does not have a "cost of sales" line in its financial statements and therefore no gross profit line or easily calculatable gross margin. This makes it difficult to predict the gearing effect changes to turnover might have on profits. However, what they do report is the numbers of staff in various categories and the cost of inventories. From this, you can see that many of the people who actually work in the factory are either low paid and/or part-time. This is consistent with their job description as "operatives".

With the caveat that hours may be increased to meet demand without employing more people, it is then possible to estimate the gross margin of the business and therefore use this to extrapolate forward. Given that in most companies some of the admin costs are actually not fixed at all and are variable with revenue, we suspect the figure Leo has for gross margin is at least as accurate as with other companies we analyse. The calculated gross margin is acceptable, but falling, trending down from 38% in 2016 to 35% in 2019. 2020 was an exceptional year, but assuming for modelling purposes that government support provided appropriate compensation, gross margin remained broadly steady.

However, N+1 Singer's current forecasts on £90m of turnover imply a further fall in gross margin to 32%. Given distortion from recent acquisitions and coronavirus, plus a continuing trend for strong pay increases at the bottom quartile of workers, this is quite possible but does seem on the pessimistic side. It also implies an adjusted operating margin of 8.1%, versus 8.4% in 2019 and 11.1% in 2018.

So, on to today's update:

Sales for the first half of the year will be approximately £43.0 million (2020: £32.0 million), representing an increase of 34% compared to the prior period. We were pleased to see sales growth across our three biggest geographical markets of the UK, USA and South Korea compared to H1 2020. We have also continued to see strong sales growth in online channels in our major markets.

FY 2020 was of course affected by coronavirus AND didn't have the full benefit of recent acquisitions, so this 34% figure is specious and should be ignored. Fortunately, they give is a more useful figure:

Against pre-Covid-19 performance in H1 2019, our like-for-like sales at a constant currency are up by 6% (excluding the benefit of Nambé acquired in July 2019 and the remaining 50% of the issued share capital of Portmeirion Canada acquired in August 2020).

This is a useful increase given the low structural growth we mentioned earlier, but of course, could benefit from some catch-up sales. They comment:

We have continued to trade strongly in May and June and it is particularly pleasing to see that we are achieving like-for-like sales growth over pre-Covid-19 trading levels, despite continuing disruption in our markets due to the UK's lockdown in Q1 2021 and ongoing Covid-19 related global shipping and supply chain delays.

We have a strong global order book going into our important second-half trading period. Whilst we remain cognisant of the ongoing supply chain-related challenges, we remain confident of the trading outlook for the rest of FY21.

In their opinion:

This performance demonstrates the strategic progress we are making as a business, including our online and digital transformation and rest of world sales growth.

But the key fact here is the £43.0m revenue for H1. Traditionally the business has been heavily H2 weighted, presumably related to Christmas. From 2016 the H1 weighting has been 37%, 39%, 41%, 38% and 36% respectively. 2019 H2 was helped by the Nambe acquisition and 2020 Q2 may have been more affected by coronavirus than Q3.2020 H2 was helped by the buyout of the Canadian joint venture.

Still, there is every reason to thing that the fundamental H2 bias will remain, and no reason to think that candles or Canada has any less of an H2 bias. So the 48-52% H1/H2 split implied by current market forecasts seems far too pessimistic. Using a 42% H1 weighting - higher than any year yet recorded - gives sales of £103m versus £90.1m market forecasts. Assuming no improvement in operating margin, it implies EPS of 44p versus 36.4p N+1 Singer.

On the lower, more conservative, margin, we get 42p EPS. But on a more realistic 40% H1 weighting we get back to the 44p EPS. The share price jumped initially today and then fell back. Perhaps the market already knew the N+1 Singer forecasts were too low? Or maybe they haven't realised it yet. So, like MPAC, this looks like another one due an upgrade with the H1 results, but where it is easy to argue that it is already fully valued.

The big question is whether they have really "fixed" the issue with the business, or as they put it:

This performance demonstrates the strategic progress we are making as a business, including our online and digital transformation and rest of world sales growth.

...or whether margins will continue to decline once the noise of acquisitions and coronavirus is out of the way. All we can say for sure is that it weathered the last year pretty well and it looks better value than when Leo sold in 2019.

Kenmare Resources (KMR.L) – Q2 Production Report

Kenmare Resources is a company we follow since we believe that the market dynamics in Heavy Mineral Sands (HMS) are highly favourable. Essentially, there has been no new capacity built into the sector in the last 5 years or so, and demand is generally correlated to global economic growth which is now bouncing back strongly.

Since this is largely a commodity product, the converse is also true. Large drops in global economic activity tend to cause large price falls. Mark sold out of Kenmare at the start of the COVID crisis due to concerns about their debt level, CAPEX commitments and a declining commodity environment that would put them under financial pressure.

Although this was clearly a good call in the short term, in the long term this was a mistake, as the following chart shows:

Kenmare executed their CAPEX projects well, and in reality, the supply constrictions caused by COVID actually helped keep prices for HMS high. Making today’s production report pleasant reading:

HMC production was 436,600 tonnes in Q2 2021, representing a 41% increase compared to Q2 2020 (310,300 tonnes). This was a result of a 43% increase in ore grades (to 4.7%) and a 6% increase in excavated ore volumes (to 10.9 million tonnes), setting a new quarterly record of HMC production.

The benefits of their capital investment are clearly paying dividends. Literally in this case:

On 19 May 2021, Kenmare paid its 2020 final dividend of USc7.69 per share. This was the balancing payment of a 2020 full year dividend of USc10.00 per share, up 22% from 2019. As previously stated, Kenmare is targeting a 25% Profit After Tax dividend payment for 2021.

Although net debt has increased in the period showing how much they were spending on CAPEX:

Accordingly, as at 30 June 2021, Kenmare had net debt of US$76.1 million, compared to US$64.0 million net debt at 31 December 2020, which is mainly due to the timing of capital expenditure payments and a reduction in the use of invoice factoring.

As expected, price trends are positive:

Positive market conditions prevailed for mineral sands in Q2 2021 with market prices for ilmenite, zircon and rutile all increasing.

Ilmenite prices continued to rise through the quarter, benefitting from strong demand. Pigment plants are operating at high production rates, whilst the titanium metal and welding sectors are also experiencing a strong recovery.

As in a lot of industries, increased freight costs may be taking more of the margin:

Positive market conditions for all Kenmare’s products are expected to continue in Q3 2021, despite an expected strong freight market having the potential to dampen received prices. We have a strong order book for our ilmenite products and we expect to a supportive market for rutile and zircon in H2 2021.

However, in a product that is hard to substitute, the increased costs will often be borne by consumers, not producers. Of particular note, is the strength of Zircon:

The recovery in demand for zircon accelerated in Q2 2021 and price increases were achieved for Kenmare’s zircon products. The zircon market is tight and further exacerbated by production disruptions from zircon suppliers. Demand for Kenmare’s zircon products is currently exceeding its ability to supply.

Which bodes very well for the other UK-listed pureplay HMS miner Base Resources, which has a higher proportion of Zircon per tonne of HMS produced.

Base Resources (BSE.L) – License Extension

Base has a much lower life of mine at its current active operations than Kenmare though. Hence the difference between the £550m Kenmare EV and the £130m Base EV, despite Base producing around half the volume of HMS with a higher average price point.

Base themselves announce an extension to the mining license in Kenya today. Which while good news, was largely expected. The future of Base depends on Madagascar allowing operations to begin on building the new Toliara mine.

Despite these good results, Base looks preferable to Kenmare at current prices. The current Base share price is largely covered by the NPV of the cash flows from Kenya alone, and the world-class development resource is Madagascar is in for free.

If this can be brought into production in the tight market pricing environment that is likely to persist for the next few years then the returns could be phenomenal.

Whereas with Kenmare you are likely to see the debt paid down and a continued dividend stream. The yield is forecast to be around 4% going forward, which while not bad, doesn't seem particularly exciting in the same way that Base does with their upside potential.

SIG (SHI.L) – Trading Update

Today we get a trading update from SIG Plc for the six months to June 30th. This is in the building supplies sector, so you would expect them to be going great guns at the moment like the rest of their industry.

And indeed they are….compared to 2020:

Revenues in H1 were strong, with like-for-like ("LFL")2 growth of 33% compared to the Covid-affected prior year and up 1% against 2019, a more meaningful comparator.

But only 1% vs 2019 – so not exactly impressive.

They do report that:

…underlying operating profit now expected to be ahead of previous forecasts.

Sounds good, until you realise this is given as just £13.5m. And this is a company with an £800m Enterprise Value so has a long way needed to grow into that sort of valuation.

Again, the French business is the one delivering, and the risk remains that this gets hived off, leaving shareholders with the UK runt of the litter.

To pay this EV for the business, you are betting on a significant recovery somewhere out in 2023/24. This may happen, but when they are struggling to grow revenue vs 2019 in one of the most positive 6 months for their industry ever, it would be a brave bet.

System 1 (SYS1.L) – Final Results

System 1 announced their full-year results to 31st March 2021 today, which aren’t bad when you consider the period being reported:

Here is what the numbers look like split out by half:

These show a good recovery. As usual, however, you can drive a bus between the adjusted and statutory figures:

Adjusted Operating Costs exclude impairment, interest, share based payments, bonuses, severance costs and government support related to the Covid pandemic.

They are a marketing business after all! Here’s how these break down:

You have to question how one-off these costs are if they keep reoccurring. They are cash generative though:

The impairment comes because their AdRatings idea seems to have failed, and all capitalised development costs written-off:

The carrying value of the AdRatings product was tested for impairment at as 31 March 2020. The carrying value of the asset was allocated to the AdRatings cash generating unit ('CGU') for the purposes of assessing future cashflows. The principal assumptions used in the forecast were the timing and amount of future revenues and profit margins, which were derived from the latest forecasts approved by the Board. As a result of this review, and considering the continuing modest AdRatings revenues of £0.05m in the year, the carrying value of the asset was fully impaired; the amortisation charge included impairment charges of £0.9m.

This is several million pounds of shareholders money that has largely been wasted but at least they are no longer throwing good money after bad.

Not sure the layman would know the difference between the failed AdRatings and Test Your Ad, which they say is doing very well:

· Transition to scalable automated data products is underway. Data products represented 15% of Revenue in the final quarter helped by the success of Test Your Ad which also led to an 18% year-on-year increase in Comms Revenue

· We continued to invest in our growth strategy, spending over £2m on product development and restoring headcount to pre-pandemic levels to service demand in H2

They are very bullish on their hopes for the future:

We believe that System1 could be worth £1 billion eventually. Management owns 30% of the business, excluding shares under option. We take every decision with our medium term £100m+ Revenue milestone in mind. Aside from the automated product strategy, our choices on the calibre of our talent, the workflows in the company, our supply chain, the IT systems, and much more support achieving this goal.

That quote reads like it was written by a bombastic analyst touting for business rather than the company management. It shows good ambition, but also makes me slightly wary.

At least going forward they are expensing their development not capitalising it, so we are likely to get relatively clean figures. Many of the adjustments won't re-occur and given the strength of the H2, perhaps we could see them doing at least £3m real, unadjusted PAT if not in 2022, then in 2023.

Brokers appeared to cut forecasts for 2022 in response to this outlook from the trading statement in April:

System1 is focused on achieving Revenue growth over the short and medium term. In pursuit of this goal the Company will increase discretionary investment in product development, IT, marketing, and relationships with advertising agencies and advertising platform partners. We will also continue to recruit new talent, after a sizeable increase in headcount during the latter months of 2020/21 which took year-end headcount to 147 from 128 at the half year. The drive for further efficiency improvements in "run" costs will continue. We plan to remain profitable and to continue to generate cash in the 2021/22 financial year, notwithstanding that we are targeting revenue growth to be at least matched by the rate of cost growth as we prioritise scaling our automated predictive products.

Mark wasn’t convinced at the time since the stock was trading at 13x a highly adjusted set of figures, but with the adjustments likely to be less in the future and the price some 20% lower than when he commented, then this is starting to look interesting. It is not clear that the drop in broker forecast makes sense anymore, or if it does it will be only for the 2022 year while they invest. £3m real unadjusted PAT seems a reasonable target going forward and if we apply a 12x multiple (it is a people business so should never be much higher) and add in the £5m or so of cash we get a £41m valuation vs a £27m market cap today.

So perhaps should see a 50% or so return in the next year or so if they can deliver on their short term aims. Longer term, maybe more, but their bombastic targets maybe should be taken with a pinch of salt, they are marketers after all!

Small Caps Live Thursday 15th July

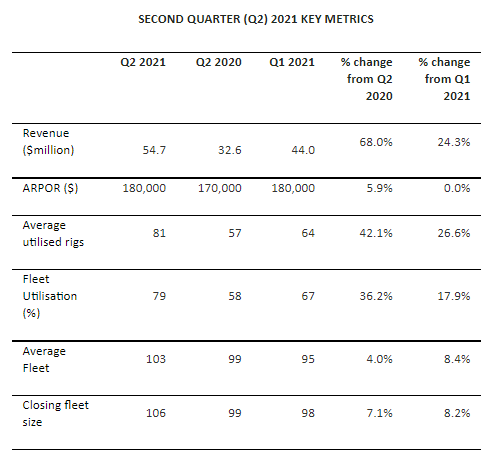

Capital Limited (CAPD.L) - H1 Trading Update

Here is what Capital are reporting for Q2:

The standout figure was the number of utilised rigs. At 81 it significantly exceeded the number from our contract analysis which was 74 and blew the Tamesis Partners estimate of 70 out of the water.

If you recall, Q1 was slightly disappointing on that front. we always believed that it was just timing. With the investors mantra being to trust, but verify, this has been resoundingly verified.

Q3 may well be seasonally weaker as West Africa, which is 38% of revenue, enters the rainy season, which will prevent access to more remote areas for exploration drilling. However, when asked about this on the call they said that Capital is more resilient than competitors since they have longer-term mine site contracts with graded roads for access. They have also seen increased activity in Tanzania where this is not an issue.

The ARPOR was in line with our estimates but higher than Tamesis assumption.

In light of these strong results, the company increased their revenue guidance:

Increasing 2021 Revenue Guidance: After a strong H1 2021 and better than anticipated drilling utilisation rates, the Group is increasing guidance on anticipated revenues for the current financial year to $200-210 million (up from $185-195 million originally guided at the FY20 results)

We’ve commented before that Tamesis forecasting the bottom of the previous range seemed to be nonsensical since taking their rig revenue assumptions away from this figure left a mining services revenue figure that wasn’t growing. In today’s management call the company confirmed that Q3 mining services revenue would be higher than Q2 and Q4 higher again. This is what they say in the Trading statement:

· Transformational Sukari Gold Mine (Egypt) waste mining and expanded drilling contracts continue to perform well:

- Blast hole fleet is fully utilised, with all seven new blast hole rigs now operational;

- Large excavator fleet (1 x CAT 6020 and 2 x CAT 6040) commissioned and operational;

- Workforce recruitment is approximately 94% complete.

The latest note from Tamesis doesn’t seem to have a precise forecast but simply quotes the company range, but they have updated their model saying:

On today’s guidance our first pass estimation of upgrade to EBITDA and Net Profit is 12% and 31% respectively for 2021.

It is not quite clear how they get to those figures. Perhaps the lower increase in EBITDA is them catching up with the mining services side which they had in as much too low but is lower margin.

Mark asked specifically about gross margins on the drilling side on the conference call. The company was understandably reticent to give specific numbers but the CFO indicated that these were more likely to rise in the short term than fall. One of the other analysts asked about cost inflation. The company said that they are not seeing this yet, but that it would be naïve to think that it wouldn’t arrive eventually given the market dynamics. Conservatively, we can assume that they will retain their c40% Gross Margins for 2021, which has been their historical norm.

They added 3 more rigs in Q2 and will add a further 6 rigs in H2 if we heard the conference call correctly. These should be going to specific long-term contracts, so add to utilised rigs. Overall, they should be doing around $165m rig revenue and with Mining Services growing, this may be towards the top end of their guidance. This would give around $55m EBITDA for 2021. Going forward, the signs are from contract renewals and longer-term contracts, plus the ramp-up at Sukari, that 2022 will be even better, maybe at around $65m EBITDA.

One of the downsides was the increase in net debt to $33.6m. Considering they had net cash and raised $40m of equity last year, you can see how much this expansion has cost. However, the good news is that when Mark asked about this on the call, the CFO indicated that they expect to be cash-flow positive in H2 and that this figure is expected to be around the high watermark for debt.

The current mark to market for the investment portfolio is around $35m so this completely offsets the net debt. Mark asked about the level 3 assets since we are aware of a number of unlisted options but these were unlikely to cover the full $10.9m valuation. So it was interesting to hear that Allied Gold makes up the bulk of that - we weren’t entirely sure from public docs if they still held that. Allied Gold could be marked up at the half-year, but that is the only part we can’t estimate from live equity pricing. They have taken profits in several places already, so this strategy of drill-for-equity has been a success on every level.

The other thing that the market may miss is the strength of MSALABS. This was described as trading in-line in the management call. However, in a previous call, this was described as planned to double revenue this year, from $8m to $16m, with high margins and low CAPEX. And that capital-lite nature was confirmed in today's call. Mark asked about the payback on the new PhotonAssay machines and it was said they pay a monthly rental. So payback is immediately when they are used. This is good since they don't take the technological risk and their cost of capital is relatively high at the moment (although will come down as they rebuild cash on the balance sheet.)

On these numbers, MSALABS could be worth as much as $40m on its own, of which, Capital own 75%. With the management of MSALABS holding the rest.

Putting all of this together with a 5xEV/EBITDA multiple on the drilling/mining side that is the sort of forward multiple the industry currently trades at, we get a valuation in excess of £250m or £1.35/share. This is potentially conservative on both gross margins and multiple, given that CAPD has better growth prospects than many competitors.

One other snippet:

Awarded an exploration contract with new client Shanta Gold at its West Kenya project, Kenya (commencing Q3);

A few years ago, Mark asked Eric Zurrin, Shanta CEO, what his views on Capital Drilling were. His answer was that they were good but expensive. In Tanzania, he had a couple of guys who did all his drilling and were cheaper. So it is a sign of strength that Shanta decided to pay up for quality in Kenya. There should be another 18 months - 2 years of drilling work at West Kenya.

In terms of share price reaction, you can't help thinking that the market has under-reacted to the news this morning. There may be a couple of reasons:

The first is that we've flagged on here that this TS was likely to be good, although we clearly underestimated quite how good it would be!

The second is that some people won't hold CAPD at any valuation. When Mark presented it at the Mello BASH the split was largely between Buy and Avoid - showing that Africa-focussed and gold mining was a step too far for a number of investors.

Summer; and

A lack of detailed broker upgrades, some of which seem to have phoned it in from the beach!

Results on the 19th of August may lead to more detailed research and some to re-assess, but again this is the peak Holiday season.

Risks are, as always:

The big revenue concentration at Sukari

Cyclicality may prove more fierce than anticipated

Wars, insurgencies etc.

Large tax demands

Undetected fraud

A share overhang if Brian Rudd retires and wants the cash quickly

Founder & Exec Chairman, Jamie Boyton, does seem to be a driving force. So if he became unwell it is unclear if the company would have the same drive.

Capital is a true multinational in that it has a Hong Kong back-office, a Mauritius head office, an Australian management, and largely Africa-based operations. They haven’t always handled this as well as they could, with a few mishaps on an RNS release and the like. Although it was interesting to see they had an IR representative on the call, and have been much better at putting the investment case to a wider group of investors recently.

These are not really any different to other entrepreneurial companies, though, and only Sukari stands out as an unusual corporate risk. The diverse geography of their operations helps mitigate a lot of specific country risks.

On the analysts, Berenberg and Peel Hunt research is generally good quality but a) we can't see it and b) they have been much more conservative than Tamesis on valuation/PT etc. and c) the research is going into an institutional base that may be limited in their ability to invest into the resource space. So perhaps don’t hold your breath for analysts support of the share price.

On scl, we prefer to do our own research and stay ahead of the market, with the hope that it catches up eventually somehow. At the end of the day, the cash will do the talking. If they start to generate significant FCF post the recent CAPEX and re-invest it into the right growth opportunities or pay it out as dividends, then this can't be ignored by the market in the end.

Thanks for reading this far, have a great end to the week.