Small Caps Live Weekly Summary

CAPD GMS CNC FA. PRES XPF K3C MGP IMMO THRU RAI

It’s been a turbulent week in the markets, starting with a “mini-budget” that was not well received by the international investors that will be funding this largesse. However, the real sell-off for equities was driven by a hitherto unknown bit of pension fund operations known as LDI. Discord contributor SaintJim gave one of the best explanations we’ve seen of what went on:

Pensions buy long-dated gilts….they have to. The regulator makes them, and that suits the government because there is a patsy to finance long-term borrowing. Pension liabilities are PV’d against the gilt yield so to manage and match their liabilities pension companies are also happy to buy gilts. Trouble is gilts have been a terribly low yielding investment for years.

Step forward LDI. I’m going to use the gilt UKT 0.5% 2061 as my example because it’s a fun bond. It was issued last year by the Government at par (a price of 100), implying you would receive 0.5% per year for the next 40 years. Not great, but as a pension co. you have to buy it.

Next, you decide to enter a 40 year swap against it. You pay the fixed coupon and receive floating. This looks a smart move….you have your gilt (regulator happy) but you have swapped the lousy 0.5% coupon for a floating coupon. As yields rise, the gilt will lose money, but the swap will compensate (and vice versa). The swap needs a bit of collateral for initial and variation margin as the market moves.

Next, you decide to repo out the gilt. There’s no point doing it short term (most repos are overnight) so you ask the repo desk to price where they would do the repo for 2, 3 even 5 years. You then lend the gilt to them at par and take the cash. The repo also will have initial and variation margin. Whoopee… you bought a gilt, hedged it and got cash back in the bank to go and buy Tesla with!! Everyone is happy.

Fast forward to 2022, and the UKT 0.5%2061 bond has a yield of 5%. In price terms, that means it has dropped from 100 to 25. Yup 75% value destruction in a year. As the pension co. the pressure point is not the gilt or swap (they hedge each other), and the Present Value of your liabilities has dropped. (The payouts that pension company have in the future are discounted back using a gilt yield.) No, the pressure point is the repo. All that cash you borrowed was secured against an asset that trades at just 25p in the £.

Cue margin call. You sell the Tesla shares, you raise cash wherever until at some point you think ‘Sh@%, the only think left is selling gilts’. Better phone the regulator….

This explains the big sell-off in equities this week, as pension funds have been selling down their most liquid risk assets. This is not unlike the issues we saw with risk-parity funds blowing up in March 2020 in response to the COVID emergency. Forced selling does create bargains, and the risk-parity blow-up did mark the bottom in 2020, but it takes a brave investor to buy UK-exposed businesses when the outlook for the UK looks so grim.

Large Caps Live

What’s going on in the economy this week:

(1) Falling confidence in the UK due to the energy price cap, which will cost circa 6% of GDP and a cut in tax rates - which will cost circa 1% of GDP.

(2) Burning up of cash from pandemic means that UK bank deposits become less plentiful

(3) UK Banks will be in price competition for deposits

(4) UK Banks have benefitted from a 'widening of the jaws' - i.e. increasing net interest margin (the difference between deposits and loans) - that is being projected ahead by analysts - I think it will continue to widen for a quarter or two but as deposits fall the jaws will narrow and so bank margins will fall

(5) A combination of falling deposits (UK Banks have a lot of deposits at the BoE and UK gilts etc) and the wider market environment means that (a) UK banks will have to raise the spread above BoE rates for mortgages (b) pressurise the long term yield curve in the UK

(6) About 45% of UK mortgages are currently variable rate - that goes up over time unless people remortgage. (It goes up as the 2 - 5 year fixes expire)

(7) A combination of tax (on landlords), regulation (increased EPC requirements), energy and mortgage rates will drive UK house prices negatively

WHAT THE MARKET IS MISSING:

I like that there is a high risk that people are not thinking about (a) UK Govt receipts - they will be down as energy and interest rates rise (b) and rising rates mean less UK govt spending

So my 'variant perception' is that the market still needs to work through the impact of a recession with rising rates on UK govt - and thus, the borrowing could be higher than the market expects. And remember - that the UK govt will have to raise wages, and pay energy bills for its buildings - and the real squeeze will be local councils / schools / hospitals etc.

I do think the BoE OUGHT to have had an EMERGENCY meeting to raise rates, but they appear to have bottled it.

I was reading somewhere that when inflation goes above 5% it typically takes countries about 10 years to get it below 2% again. _ I don't think that is priced in. And I think that is why Jerome Powell is trying to hit inflation hard and fast - and why the BoE is losing credibility.

The 'real' growth in UK retail physical sales is awful - over 3 or so years. Also the WFH move undermines office valuations - before we even look at rates. And Druckenmiller had previously noted that when inflation goes above 5%, it has never comes back down until real interest rates are positive

On top of that (a) the UK has historically been subject to spreading wage inflation following a commodity jump; (b) the UK govt is effectively short energy and short USD; (c) the public sector has faced a decade of 'austerity'; and (d) a lot of focus is on UK Gvt expenditure but there is a big hole in a lot of council budgets.

Oil maybe destined to go higher too. The US needs to refill the SPR. Perhaps they would be they would be happy to refill between $70 and 80 (having sold from over $100). It puts a floor in and then there is the whole China economy picking up after Covid and the lack of investment arguments. The question is how far the price falls in a recession but then I think the SPR might put a floor in

Small Caps

Capital Limited (CAPD.L)

We don’t normally comment on stocks without specific major news. However, with Capital there has been a number of small changes that have potentially added up to a big change in valuation. These are a new contract with B2Gold, a placing at Firefinch, but perhaps most importantly, a weakness in the pound. This still provides a tail wind even though the current spot rate has bounced strongly back to 1.12 on Friday.

On discord, Mark has tried to make sense of this with an updated valuation model. As usual, he calculates a mid-case valuation but also presents a low and high case for those who are particularly pessimistic or optimistic on how Capital should be valued versus its listed peers:

First up is the investment portfolio. Lots of moving parts, but I have updated holdings where we know about them and also marked Firefinch to the AUD6c placing price vs 20c suspension price. I reckon listed and unlisted are worth about $44m at the moment, and I take a 10% discount to reflect illiquidity, giving a $40m valuation.

MSALABS I value on a revenue multiple. The growth rate will be slowing from the 100% pa historical rate, plus market valuations have come in for growth stocks. So I reduce my revenue multiple to 4x. However, the TTM revenue is now around $21m making a $64m valuation for CAPD's c77% stake.

For Capital Mining & Capital Drilling, I used EBITDA multiples of 3.7 & 4.1, respectively, which is the competitor mean from the 22H1 results presentation. Splitting the admin costs pro-rata between the businesses and ignoring MSALABS (which is conservative since at least some of the admin costs will be due to this growing business), I get around $16m EBITDA for mining & $70m for drilling based on my estimates.

This gives a $59m valuation for mining and $288m for drilling.

Year-end debt will be higher due to purchasing the 10 rigs from Perenti. I am estimating this at $42m net debt since the guidance was for this to come down a bit from the $36m at H1, prior to this deal.

All of these are in USD, and with the current GBP weakness, this mid-case valuation works out to be about £1.93/share for a 128% upside to fair value.

My downside valuation, implying that the various parts should trade at a discount to industry averages, gives a fair value of £1.24/share for a 46% upside.

If you believe that the business should trade at a premium to peers, (an argument that I have some sympathy for, given their pursuit of long-term contracts rather than high spot rates), then I get an upside valuation of £2.76/share for a 226% upside.

I've always thought that Capital was a good place to be invested because of the quality of management and where we are in the cycle, but that the returns would be good but not stellar. They would just be a lot more certain than other places to put your money, and this justified a reasonable holding. Of course, returns in a spreadsheet are not the same as an actual share price, and the areas of operation make the company higher on the risk spectrum than average. However, I am increasingly seeing that this could be a multi-bagger with a fair wind, not just a solid but unexceptional return.

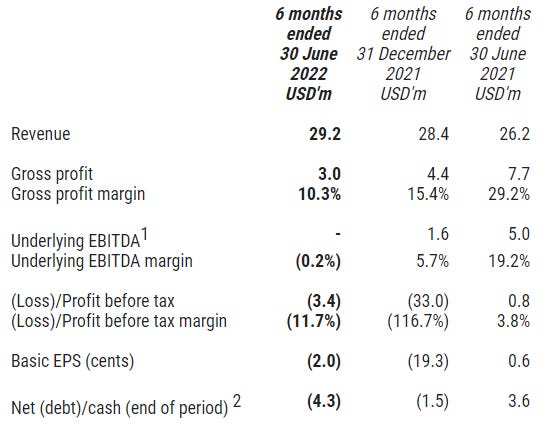

Gulf Marine Services (GMS.L) - Interim Results

This has been a bit of a surprise investor favourite since it was presented at the Mello BASH in the spring. This week we get interim results:

Revenue for the period increased to US$ 66.4 million (H1 2021: US$ 51.4 million), mainly driven by an increase in day rates to US$ 27.2k (H1 2021: US$ 25.5k) and by an increase in utilisation to 89% (H1 2021: 77%).

Some decent increases there. However, revenue seems to be down on H2 last year, and with utilisation at 89%, there isn't much scope to increase this. Costs were also higher, but overall, this drove increased EBITDA:

H1 2022 EBITDA stood at US$ 37.3 million (H1 2021: US$ 26.5 million), which was driven by an increase in utilisation, improved day rates and continuous focus on cost savings.

A lot of investors have simplistically focussed on the low P/E here, forgetting that the vast majority of the capital structure is debt, not equity. The real bull case is that increased day rates will make the earnings look cheap. However, they are still some way away from this:

GMS reported a profit after tax during H1 2022 of US$ 13.1 million (H1 2021: US$ 2.0 million). This is mainly a result of the increased EBIDTA coupled with reduced finance expenses.

Taking double H1 as the estimate for the full year, 2x $13.1m = $26.2m, gives a return of just 4.3% on their $607m of tangible assets. Although, there is some sign that things may be improving here:

During H1 2022, two new contract awards were announced by to the Group for K-Class vessels, where average day rates were 32% higher than their previous contracts.

But this is a long way from making these assets acceptably productive again. Indeed, the company now say:

As demand in the market continues to grow, the Group anticipates improvements in day rates and utilisation, albeit at a slower pace than originally envisaged.

Debt-adjusting that forward P/E gives a multiple more like 17x, and even that now looks at risk. So we really need a pathway for day rates to triple from here to make this look obviously good value. This may be possible. After all, the company will not have built these ships expecting a 4% ROA, but this is a long way from where they are today. And why would an investor pay up today in the hope of a massive increase in a few years’ time?

The other issue is that they remain heavily indebted. Some of that debt has become current, meaning the current ratio is now 0.9. They should have the cash flow to pay this:

We are pleased to be able to reconfirm our 2022 EBITDA guidance of US$ 70-80 million.

But the best case is that all their cash flows will be going to pay down this debt for the foreseeable future. There are unlikely to be any dividends for many years, given that the overall net debt is $341m.

The other factor to consider is that the deprecation is real here. These are physical assets that are operating in harsh environments. If the company doesn't make any capital investments over the years, then the assets will decline to nothing together with their earnings. With such large debt, increases in interest rates will also negatively impact them more than the average company. So this remains a company that is both expensive and high risk in the current market environment.

Concurrent Technologies (CNC.L) - Interim Results

This looks like more over-promise and under-deliver from the management here:

Component supply issues have delayed shipping of some of the Company's products, such that a proportion of expected H1 2022 revenues will be recognised in a later period.

Although they point out that this is largely out of their control:

However, this is a short-term issue and in no way relates to the quality of the underlying business. Demand for the Company's products is higher than ever with a strong H1 order book (£14.2M) and record backlog (£20.3M).

It is impacting multiple dimensions of their business, however:

Gross margin of 50.4% (H1 2021: 54.3%) - reduced as the result of price increases of some components due to high demand and limited supply (-£0.3M against H1 revenue)

Pricing power appears weak, at least in the short term. Overall, they only break even, but tax credits give them a positive EPS. The cash balance remains decent, but the cash burn is £2.5m for the half year:

Cash Balance (including cash deposits) as at 30 June 2022 of £9.3M (31st Dec 2021: £11.8M)

So you can see why they have cancelled any interim dividend payment. Their broker, Cenkos, seems unconvinced that this is all to do with the timing of delivery:

They have cut 2022 estimates to break even, suggesting that the company isn't going to catch up with those orders in H2. Even more worryingly, they have halved 2023 estimates for earnings and dividends, suggesting that this is the new normal here.

Perhaps the most damning aspect is that the company is now missing the old 2022 broker’s estimates by a country mile and only chose to tell shareholders about it 9 months into the year, at the end of September. It seems that either the financial controls here are weak (certainly possible, given that the last set of financial results were qualified due to their inability to find why there was a historical under-reporting of profit and assets), or the management has allowed a false market to persist since their last results statement.

Which is why when the management say:

After more than a full year now leading this business, I am even more confident in our ability to grow and develop a successful global enterprise.

…this should be taken with more than a pinch of salt.

The new forecasts put them on a P/E of over 20 for FY23 despite a 15% fall in the share price today. They looked at best fully priced on the old forecasts, but they look significantly overvalued on the new. These look like they have much further to slide to get anywhere close to a reasonable valuation.

FireAngel Safety Technology (FA.L) - Interim Results

FireAngel start by bigging themselves up:

The Company expects to deliver its best full year performance since 2017 when the Company's results were partially fuelled by demand driven by the impact of German legislation

Then introduce an adjusted measure that pretends none of the recent cost inflation has occurred:

Adjusted gross margin before the exceptionally high PPV costs for securing components

And then finally drop the bomb:

which will result in EBITDA for the full year being materially below market expectations and to be between break even and £1.5m

John Conoley, Executive Chairman remains “delighted” with this state of affairs.

Perhaps the only bright spot is:

International sales, up 55% to £8.4 million (H1 2021: £5.4 million), the highest for a first half year since 2017, benefitted from legislation in Benelux. In the period, Benelux achieved the highest sales in that region in its history

It was exceptional international sales that generated high sales and profits back in the day. However, back then, they had a competent and supportive partner for manufacturing and could deliver product into that high demand.

There's also some positive news on the sensors side. They always had this CO detection technology and manufacturing in the background that didn't do much nor cause many problems. Now:

Techem's selection of FireAngel's CO sensor, which will now be incorporated in the new generation smoke alarm, materially enhances the future value of this partnership

Buying the CO sensor manufacturer in Canada and then leaving them completely alone was one of the best strategic moves the company has ever made. However, the total revenues are a small part of the whole.

Following equity raises, the balance sheet is now looking better than it has for a few years. However, their reliance on invoice discounting and a days sales payables of 102 days suggest this is far from strong.

They say the Company will be cash generative in H2 2022, and they make it sound like a jolly road trip:

The Company's journey towards positive cash generation has continued.

We’re not sure investors have enjoyed it quite so much. As the company veered repeatedly towards a financial cliff edge before Downing grabbed the wheel and prevented them from plummeting to the rocks below.

Their broker shore say:

Conveniently, that is outside the forecast period. First profitability is now forecast for 2024 at 1.4p a share. Shore forecast year-end net cash bottoming out at -£4.1m in 2022 before improving to £-3.1m in 2023. So they appear to have sufficient liquidity to survive on current forecasts, although there is some evidence of problems utilising the invoice discounting facility, leaving them potentially reliant on a letter of credit that expires in under a year.

Given past performance, we see no value here at the moment until there is real tangible evidence of a turnaround in fortunes.

Pressure Technologies (PRES.L) - Trading Update

When we last looked at Pressure Technologies following their interim results we said:

…anyone buying at 70 p this week is betting on that possible trend improving further into FY24. But given they have very little forward order book coverage into 2023, betting on a strong FY24 result today seems brave, bordering on the foolhardy.

And foolhardy that bet proved to be, as this week they say:

However, whilst the second half of the year is expected to show an adjusted operating profit, the recovery has been significantly below that anticipated at the half year and the Group is now expecting to report an adjusted operating loss for the full year.

Losing money in the energy & defence sector at the moment requires a special kind of skill only this company seems to possess. Of course, the balance sheet isn’t robust enough to bear these ongoing losses, so it is unsurprising that they say:

As a result of the expected adjusted operating loss for the full year, the Group now anticipates that it will not be able to meet the requirements of the two existing financial covenants contained within the current facility. These covenants relate to leverage and interest cover and a first test is currently required at the end of October based on full-year performance to 30 September 2022. The Group is currently in constructive dialogue with Lloyds Bank regarding these covenants and ongoing facility requirements.

It can’t help that Lloyds appears to want out:

Ernst & Young LLP continues to support the Group with the review of funding options to replace the Lloyds Bank facility with new arrangements that provide increased liquidity, greater flexibility and the required working capital to support the Group's strategic investment in CSC, in particular for growth opportunities in hydrogen energy.

The outlook is all about opportunities, but then I guess management needs to be positive in the circumstances. The alternative simply accelerates the downfall. The most likely positive outcome here is a deeply discounted rights issue. A share price down 46% on the day says the market now agrees with us.

XP Factory (XPF.L) - Interim Results

These start well:

Recent performance across the estate has been encouraging with no discernible impact from consumer weakness.

We don't know about the recent acquisition Boom, but the Escape Hunt side is really quite expensive. Could it be the demographic - young people living at home or living off student loans? Although Escape Hunt also attracts families. Perhaps there is a read across to Brighton Pier’s golf business and also Hostmore, where this is often a group activity and similarly expensive.

With each successive week, Boom's trading performance reinforces our belief that it is a very attractive proposition, capable of delivering strong margins and an exceedingly attractive return on capital.

Sounds like it is possibly a better business than the Escape Hunt side then? They have apparently opened 10 new Booms in 7-8m and 1 new Escape Hunt (co-located with a Boom) in the 6m. With such an aggressive rate of new site openings relative to the Group's small size at the beginning of the year, it would be almost impossible to predict with total accuracy the specific week in which each new site would open. Indeed, in the past, they have had problems predicting the specific month or quarter, even getting it wrong after they had opened.

They talk about delays in the franchised sites, which must mean that almost all the franchise sites are late opening. This is more of a problem when they are due to open in time for a key trading period which they then miss. Of course, this is less material as they get larger, but suggests the execution still isn't quite as good as it could be.

Our full year outcome is skewed heavily towards performance in the second half of the year, notably the final quarter, and this is further amplified in the current year given the number of additional site opening that are still to come.

They do seem to be preparing the ground for a revenue miss, even if consumer spending remains healthy. And this looks particularly high risk:

we are now 7 weeks into the build at our site on Oxford Street, which is scheduled to open before Christmas.

The big hope here was once for a massive franchise rollout in the US of Escape Hunt. However, it appears to have gone nowhere:

Franchise recruitment activity all but ceased during Covid and has been slow to re-start. We expect to give greater attention to the US potential in 2023.

Apart from execution in building new sites and the risks of a consumer downturn, the other issue with this kind of business is a) underutilisation during weekdays, especially daytime b) Depreciation.

On depreciation, it is difficult to make the right accounting judgement, but using their figure of £1.1m, you can see that adjusted EBITDA gets wiped out. That's before any property lease costs, let alone their claimed pre-opening and exceptional costs. To put it another way, even if they owned all their buildings and never had to open or close another site, then they'd be just below breakeven.

So it is not proven they have a viable business here. Central EBITDA overheads are only £146k which is good, but means that opening more sites won't massively help. Net assets are £18.8m, of which £21.7m are intangibles.

Regarding liquidity, things are confused by the contingent consideration for Boom. The commentary appears to say this is economically misstated in the accounts:

£9.4m is the valuation of contingent consideration, inclusive of 13.7% p.a. notional interest rolled up from the date of acquisition, the payment of which depends on the achievement of certain turnover and site numbers from the Boom acquisition in the year to 31 December 2022. Details of the contingent consideration are outlined in the Company's Annual Report for the year to 31 December 2021. The contingent consideration is payable by the issue of up to 25m XP Factory plc shares, valued at the date of acquisition at 35.8p.

The current share price is 12.2p. Let's hope they haven't guaranteed the share price or something crazy like that.

Apart from the above, liquidity looks manageable for well over a year, provided they don't open any more sites. But they do plan to open more sites. The Going Concern statement says:

The Board has prepared detailed cashflow forecasts covering a thirty-month period from the reporting date. The forecasts take into account the Group's plans to continue to expand the network of both Boom Battle Bar and Escape Hunt sites through organic growth. The forecasts consider downside scenarios reflecting the potential impact of an economic slowdown, delays in the roll out of sites and inflationary pressures. Based on the assumptions contained in the scenarios considered and taking into account mitigating actions that could be taken in the event of adverse circumstances, the directors consider there are reasonable grounds to believe that the Group will be able to pay its debts as and when they become due and payable, as well as to fund the Group's future operating expenses.

Note the going concern is as of the reporting date, and no recent cash figure has been given. Given the post-period-end acquisitions and overruns/delays on various openings, things might not look so good now.

We think they'll return to the market to raise more money for expansion. Perhaps at that point, it will be clearer whether they have a viable business and have got on top of their long-running issues with getting sites opened on time. It might be a hard sell in the current markets, though, and a deep discount may well be required.

Accsys Technologies (AXS.L) - Trading Update

They start with:

Continuing strong demand and stable Accoya wood revenue for the first five months of the 2023 financial year

Stable Accoya wood is good. Stable Accoya wood revenue is not. This is a period where timber prices have been rising. So is demand really strong?

Volumes limited by production capacity with Accoya® sales volumes of approximately 18,803m3, down around 24% year on year due to the previously reported shutdown at the Arnhem plant in April/May 2022 around the extended completion and commissioning of R4.

Looks like there are problems with execution. This is one of many reasons why ideally, they should be licensing the technology to others. However, it looks like things are back on track and:

The R4 expansion increases the plant's current annual production capacity by 33% to 80,000m3

So, in annualised run-rate terms we have 59,400m3 in the 5 months last year, 45,100m3 this year and 80,000m3 potential. Unfortunately:

Accsys continues to expect to increase the R4 production levels to full capacity within two years.

They are also building a new plant in Hull, but has also been going badly, with a further cost overrun announced, problems with financing and questions over profitability at current energy prices. And they are building one in the US, which as we know, benefits from energy independence, but this is years away, even assuming no more screw-ups.

The product/technology is fairly unique and appears to be in strong demand, but production is proving more complicated than expected. In both cases, their inability to supply is slowing growth in the market and increasing the window for competitors to come in.

The trouble is that although both have patents, I suspect a considerable amount of the value is in "know how". This, combined with a limited established market, makes it difficult to license the technology in the short term.

March 2023 forecasts were almost cut in half off the back of the update, but the real value starts to be seen in 2024. Here the damage is less severe - a cut from 6.2p EPS to 4.8p. The trouble is that the Hull issues look serious. Edison goes into too much detail to quote in full, but there is basically a dispute amongst the partners with no route to resolving it, and Accsys don't have the money to throw at it even if they wanted to. A complete halt to work potentially for a year before the financial restructuring of the JV looks more than possible.

Edison's valuation assumes things will progress but increases the equity risk premium from just 5% to just 6%. They also seem to be behind the curve on the risk-free return. We suspect with sensible assumptions (Hull written off fully, WACC of 20%), their DCF would come in far below the current share price. So, uninvestable for now, but still worth watching.

K3 Capital (K3C.L) - Final Results

These look very good, at least on an adjusted basis:

· Group revenue increased by 50% to £70.7m (FY 2021: 47.2m) with strong organic growth of 24%**

· Group Adjusted EBITDA* growth of 30% to £20.4m (FY 2021: £15.7m*)

· Cash £13.7m (FY 2021: £14.3m), providing significant headroom to fund organic investment and acquisition opportunities

· Adjusted earnings per share*** 20.64p (FY 2021: 18.56p)

· Recommended final dividend of 8.1p per share, resulting in a total dividend for the year of 12.1p (FY21: 9.1p)

Organic growth is still good, as is cash conversion and Q1 trading:

FY23 Q1 has seen continued momentum across the Group, delivering turnover in excess of £20m and Adjusted EBITDA of c.£6.5m* in the three months to 31 August 2022

They are more diversified than before and claim to be partly counter-cyclical. This makes sense, but we will see what happens now we're approaching a recession. Their policy of cross-selling seems to be working and helps the rationale for acquisitions.

Perhaps the biggest problem is that they are a highly acquisitive company that wants shareholders to ignore all of the costs but count all of the benefits:

The conservative approach would be to take the 13p unadjusted EPS, not the 21p adjusted EPS in any valuation. This makes the current P/E around 18, which looks fair value in the current markets, even for a company with decent growth.

Medica (MGP.L) - Interim Results

This company was hit badly during covid as the NHS shut down for normal operations, and early hopes that lung scans would be used to quickly diagnose covid infection were dashed. Unlike elsewhere, this jump in sales is unlikely to be a one-off, with the NHS years away, at best, from recovering after covid.

They have also been winning new trust clients in the UK and customers in Ireland. The standout is of course:

UK Elective revenue increased 61% YoY from £6.2m to £9.9m, reflecting strong demand for services in response to the backlog of patients requiring scanning.

Further fast growth seems most unlikely, but nor does any fallback. One of the self-inflicted problems with the business is capital intensity. They say:

Successful launch of a new Picture Archive and Communication System (PACS) in February with continued investment in our FutureTech platform

This is reflected in the cashflow which is consistently terrible:

Capex in the period was £1.4m (2021: £1.2m) which included new IT equipment for employees and workstations for reporters, as well as costs relating to the ongoing FutureTech programme, including licences and capitalised internal costs.

However, only £1.8m of contingent consideration now remains, and so they should be cashflow positive in H2 as far as I can see. A major problem here is the dependence on effectively a single customer for over 70% of their revenue. The UK government could bankrupt them at a stroke of a pen and have done so with other suppliers without consideration of the consequences. However, dependence on the NHS is reducing and covid "recovery" obscures a greater underlying trend to do so.

You would think from the outlook statement everything is fine:

Following a strong first half performance, Medica continues to be well positioned. We continue to grow our strategically important NightHawk client base both in the UK and Ireland and are also seeing strong demand for new acute services. For our Elective service, the challenge has been both the availability of existing radiologist capacity, as well as initiating sufficient additional capacity to meet strong demand. This has limited our ability to generate the revenue growth we had expected in Elective over the period and into the summer, however, the current initiatives to increase capacity should support growth for the rest of this year and into 2023. Our US business continues to grow its revenues strongly, and we expect this to continue through the remainder of the year into next year as the pipeline of new opportunities convert to revenue.

But the profit warning is in the summary:

Overall, considering current year investments for growth in Ireland and RadMD, the impact of an increase in payroll costs across the group, and a reduction in our expectations for Elective revenues this year, we expect Group revenue for the full year to be line with market expectations with net operating margin for the year to be moderately below expectations.

Liberum cut revenue forecasts by 2% all the way out to 2025 and EBS by 7.2% in 2022, recovering to only reduced by 4% in 2025. On these new forecasts, the P/E doesn't fall below 10 until 2025. There are plenty of higher quality and faster-growing companies out there if you don't mind waiting for a traditional "value" PE until 2025. And anyway, history suggests these forecasts will not be met.

Immotion (IMMO.L) - Interim Results

This is another rapidly growing company with revenue up a very impressive 91%. And this one has managed to get close to profitability but not quite. An EBITDA of £500k becomes a loss of £300k at the bottom line, and they have changed their depreciation policy, too.

This might be enough to push them into break even for the year:

We anticipate EBITDA for continuing operations in Q3 to be circa £0.7m, taking the year to date to around £1.2m.

The problem is they have capex above depreciation and are shedding about £500k each half:

Meaning their £395k of cash is looking quite tight:

They now have deals in place for their non-core subsidiaries, although not yet completed. Uvisan is going for £100k, but we don’t know terms yet in terms of payment timeline, HBE is getting a £250k investment for 51%, but no actual cash out.

So while it’s good to clear these up, they don’t help the cash position that much and are largely immaterial vs a £11.6m market cap, so you can see why the SP is down 20% today.

Thruvision (THRU.L) - Year-end Results

This is a company that has cut it pretty fine in terms of releasing their results, assuming the 6-month suspension rule for results is back in place.

And they still haven't published the full audited accounts, saying:

The audited accounts for the year ended 31 March 2022 will be sent to shareholders later today and will be available on the Company's website later this morning.

Leo thinks that most would see this is as an upbeat set of results. There were a couple of things he was looking out for in particular.

The first one is that, if you were listening carefully at Mello, it seemed like they were saying they'd quite like more cash to push into the US where they were seeing loads of opportunities. But there is no mention of this today, in particular, no specific mention in the strategic update beyond:

We estimate there are in excess of 20,000 DCs across the UK, US and Europe, meaning Profit Protection represents our single biggest market opportunity.

And in the Routes to Market section they say:

As previously reported, where we have a geographic presence (predominantly the US and UK), we continue to sell directly to end customers. However, as reported in the Profit Protection update above, we are starting to work more closely with large-scale security system integrators in this sector to increase our market penetration and speed-up sales cycles.

The average headcount has only increased from 40 to 43 staff during the year, so we see no evidence of their go-to-market strategy needing greater up-front investment in staff or systems. Inventory is a slightly different matter, however:

We forward-purchased [components] where necessary during late FY22 and early FY23 in order to protect production capacity and drew on our cash reserves accordingly.

Due to the timing, this effect is not seen in these results but we expect it to be in the H1 results. So it is well worth watching cash:

The Group's cash and cash equivalents at 31 March 2022 were £5.4 million (2021: £7.3 million).

With inventories at 3.8m, they could probably afford a 50% increase at current rates of cash burn. The £0.5million increase in trade receivables was due to the timing of material sales realised in the final month of the year, which we think was likely to be Tesco:

After an extended and ultimately very successful trial, Tesco became the second major UK grocer to purchase our technology and we completed the rollout of that significant order late in the period.

Mark was a little underwhelmed with the Ajusted Loss Before Tax since this came in as the same as the previous year at £2.3m, despite revenue growth. This is due to a rise in admin costs. Sales and Marketing was well under control, but for everything else appears to be impacted by inflation. This may push the it timeframe to sustainable profitability back somewhat.

In their last statement they seemed a bit cautious on the impact of retail weakness on their profit protection business. However, they seem a little more upbeat this week:

The first half of the new year has been challenging for the Profit Protection segment as retailers reacted to the changing economic climate. However, activity levels in this area are picking up as retailers identify the significant benefits of our solution to a number of the challenges they are facing. With revenue from both the Profit Protection and Customs markets expected to continue growing, the Board is confident that the Group is well positioned to deliver good growth this year and into the future.

Their research provider, Progressive say:

we are comfortable to maintain our FY23 estimates.

With a March year end, we'd have hoped for 2024 forecasts by now, and they don't even undertake to provide these after the next update. There is various extra colour provided in their report and so it is well worth reading.

The trend here is a positive one, but with a £23m market cap, investors are certainly betting on sustainable profits to come sooner rather than later.

RA International (RAI.L) - Interim Results

This is another company cutting it fine on reporting, this time the 3-month period for the release of unaudited interims. And this is another company where revenue is holding up ok, but profits have disappeared:

They still haven't really recovered from the events in Mozambique, and now look to be backing away from this even further:

As indicated previously, USD 1.2m of impairment was reversed in H1 22 resulting from the sale of Palma Project assets. In addition to this recovery of value, we have also significantly reduced the total storage costs moving forward. We are in discussions with parties interested in acquiring further parcels of assets which may lead to a further recovery of value and eliminate asset storage costs other than those being paid to safeguard machinery and heavy equipment in Northern Mozambique.

Having been burnt taking the risk on executing commercial contracts, then the move to more government work seems sensible.

Through RA Federal Services, LLC ("RA Federal") our US subsidiary, we now have the US credentials to deliver full scale capability to the relevant US Federal Government budget holders as a prime contractor. RA Federal is now operational and is delivering contracts on behalf of the US Government as a prime contractor. We will continue to invest in our US capability to spearhead further growth in this significant market.

And the MoD contract wins shows they are well able to win this sort of business:

On the UK side, we have today announced the award of a contract to provide operational support capability to the UK Ministry of Defence as lead contractor. This is a significant award for RA International and will lead to the Company working closely with British military operational headquarters, the Permanent Joint Headquarters (PJHQ), for the next five years, with an option to extend for a further two years. The win is testament to our capability to deliver operational support to the British military across the world; providing our expertise in project management, engineering, supply chain management, logistics and project delivery to support military planning, operations and training. The contract is structured as a global framework agreement, with a contract ceiling of GBP 35 million which will be drawn down as tasks are issued.

This comes with increased costs though:

The contract start date is effective from 1 December 2022 and we will be increasing the size of our UK operations to help facilitate and oversee the delivery of this contract.

Overall, it feels like it could well be the nadir for the business with the commercial ramping down and higher quality government work ramping up. It may be a while yet before this is see in the financial results and more importantly the cash flow. The market doesn't appear to be that forward-looking yet, with the share price down slightly.

That’s it for this week. Have a great weekend!