Small Caps Live Weekly Summary

Energy Damand MCRO JOUL ALU GDP ODX MRK

A quick reminder to sign up for the scl meet up on the 23rd March. This is shaping up nicely, with some quality content. As always, this is free to attend but you do need to register.

Large Caps Live

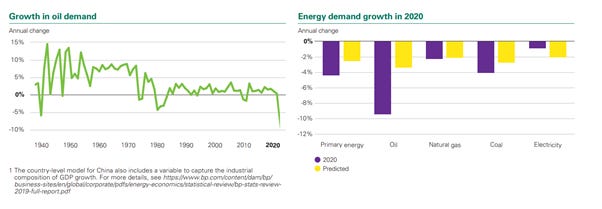

Let’s start with a number – an important number: -9.3%

That number is from the BP Statistical Review of World Energy 2021 (referring to 2020). With context:

Just look at those charts!

- We have massive increases in wind and solar capacity – but really driven by China.

- Let me put this another way:

o Modern economies require energy

o Renewables such as solar and wind – post the initial capex do not have ongoing costs that are linked to the oil / gas price or commodity prices

o To put it another way the above charts suggest that China is decoupling its economy from expensive fossil fuels pretty damn fast and this may become an economic advantage

Now I know what you will all say – China is starting from a lower base and probably needs to grow its energy production to catch up with the rest of the world. Have a look at this table though:

So basically North America (including the US, Canada and Mexico) used 88 Exajoules in 2020. And 77 Exajoules in Europe:

China - 145 Exajoules, India 32 Exajoules. Basically, India is at about half the consumption of Europe. And China – about double of Europe. Or India plus China is about the same as the whole of Europe and the whole of North America.

Another issue of course is consumption per head of population. Indeed, I would suggest to you that power consumption per head of population is a good proxy for wealth. I accept that some countries are more inefficient than others - so there need to be some mental adjustments eg the US and Saudi are going to have higher power consumption per head than a country with no O&G resources. But the BP review has some interesting numbers:

(Obviously, also climate plays a part - Canada is kinda colder.)

So in Europe, we can see that the UK has 101.6 Gigajoules per person. And given that we are all familiar with the UK we can see that roughly the US is 2.5x more power consumption per head than the UK. The closest to the US is Sweden at 218 GJ/capita (again the climate no doubt plays a part). And India / China:

I guess we all expected India (23.2GJ/capita) to be low. BUT did you expect China to be about par with the UK at 101 GJ/capita? Now I know that GDP/head does not match the UK vs China. But there are always issues of purchase power parity (PPP) – so looking at energy consumption is interesting. Basically, I fell off my chair when I realised that energy consumption per head in China is now on par with the UK. And I know we will have a discussion about energy efficiency etc but it is still stunning where China is vs the UK. And also clear that there is going to be massive growth in demand in India over the next few years.

Large Caps

Microfocus (MCRO.L) - Final Results

This has always been a bit of a special situation in the last few years. As a heavily indebted tech stock with declining revenues, it always trades much more like a value stock than the NASDAQ. The revenue isn't declining as fast as last year:

Revenue of $2.9bn (FY20: $3.0bn), improving the rate of year-on-year decline from -10% in FY20 to -5% in FY21 on a constant currency basis ("CCY")

But it is still declining. EBITDA & Profits are not really what matters here, at least in the short term. It is all about FCF & debt:

Adjusted free cash flow of $292.4m (FY20: $660.1m), with current year impacted by significant cash outflows in respect of working capital and one-off tax payments.

Net debt of $4,195.9m (FY20: $4,153.5m), representing a net leverage ratio of 4.0x. This reduces to 3.8x on a pro-forma basis, assuming the disposal of Digital Safe.

And you can see why these results are potentially disappointing. Net debt is actually up until the sale of Digital Safe that closed on 31st Jan. The debt isn't an immediate concern since they say:

Successful refinancing of term loans totalling $1.6bn in January 2022, extending the average maturity of the Group's debt from 2.7 years to 3.6 years.

Which buys them quite a lot of time to continue their turnaround strategy. The problem is that the turnaround looks like this:

On track to deliver goals of FY23 exit with a flat or better revenue trajectory, reducing cost base from $1.9bn to c.$1.5bn-$1.6bn (allowing for cost inflation) and a run rate Adjusted free cash flow of approximately $500m.

The debt is 8x FCF so when you add in the $1.8b market cap you get some 11-12xFCF. Not crazy but the balance sheet and declining revenue trends make this quite risky. The good news is that the equity being just a small part of the capital structure makes the share price pretty volatile and therefore a great trading share. Management clearly thinks they can keep the debt show on the road too, since they are paying an increased dividend:

Final dividend of 20.3 cents per share (FY20: 15.5 cents) recommended resulting in total FY21 dividend of 29.1 cents, consistent with 5x covered policy.

Dividend increases can often be an even stronger signal than management commentary. 29.1c works out to be about 5.4%, which isn't too shabby.

You can rarely bottom or top-tick these sort of things but buying somewhere around £3.50 and selling when it gets to around £4.50 has been a good strategy for some time now. Probably the best strategy going forward too.

Small Caps

Joules (JOUL.L) - Interim Results

If you just read the headlines then you'd wonder what all the fuss is about:

Clearly, the drop in gross margin vs 2019 is doing the damage, plus the issues we already know about from the trading statement re: distribution costs. The strange thing is that they use Clipper Logistics as a third-party logistics supplier. Which begs the question: if they can just pass those costs straight through to customers then it begs the question, why would anyone use them? And why should Joules be responsible for improving warehouse efficiency? Surely, that should be Clipper’s response to their bottom line being hit by increased costs. Smacks of poor contract construction from Joules.

The lack of delivery has started to cause poor Trustpilot reviews too. This is what you get when things didn't turn up for Christmas or European customers get hit with unexpected tax demands. The cost and hassle of dealing with Brexit appears to be why Joules are partly pulling out of this region, at least on the wholesale side.

Anyway, although the narrative is around it all being distribution costs doesn't really bear out:

Everything else has increased too. Partly this is because they bought Garden Trading, and partly because the previous year had lots of furlough payments etc. Inventories have increased significantly too. Again, some of that inventory increase will be due to the acquisition of Garden Trading, but as you say the movement to net debt is the most worrying part.

A lot of that cash outflow is post-covid normalisation:

The Group had agreed with its landlords and HMRC to defer certain payments, which is considered exceptional in nature, and these deferred sums have now been fully repaid. The change was further impacted by the rebuild of inventories which were unusually low at the start of the Period. This increased stock buy, together with the acquisition of Garden Trading in H2 FY21 (net cash outflow of £4.2m), contributes to the year on year increases in both inventory and payables. The recovery of the wholesale channel also impacts cash resulting in increased receivables in the Period, alongside a decrease in payables when compared to H1 FY21.

Of course, following the recent trading statement, the first thing sensible investors read this morning was the going concern statement:

As at 28th November 2021, the date of the interim financial statements, the Group had net debt of £5.4m and liquidity headroom of £28.1m.

As reported in the trading update on 1st February 2022, trading in the first two months of the second half was below expectations and liquidity headroom had reduced to £11.5m as at 31st January 2022. The reduction in liquidity headroom is consistent with normal seasonal working capital fluctuations, although the reduction was greater than anticipated due to the timing of sales over Black Friday and revenue shortfall in January.

Liquidity headroom has gone from £28.1m at the balance sheet date to £11.5m at the start of this month. So that means a further £16.6m cash outflow. ouch!

Net debt is now £22m. double-ouch!

They get to provide their accounts as a going concern, however, due to two scenarios:

· Base Case cash flow forecast to May 2023

· Downside cash flow forecast to May 2023

Base Case scenario:

For avoidance of doubt, the Base Case forecast reviewed by the Directors is consistent with the profit guidance for FY22 (i.e. not less than £5m PBT), which was given in the Trading update on 1st February 2022. The revenue assumptions in the Base Case forecast are consistent with recent trends in online traffic and store footfall; cost assumptions reflect changes in revenue as well as gradual improvements in warehouse efficiency.

Under this scenario, the Group will remain within its committed borrowing facilities and will meet relevant banking covenants.

So if they hit their current profit targets and they manage to sort out the warehouse they will be ok, at least in the short term. However, if they don't then they are into the downside scenario:

The Directors consider that the major risks in the Base Case forecast relate to UK e-commerce and UK wholesale. Therefore, a downside scenario has been constructed which assumes a 5% underperformance in these channels, a further fall in gross margin rate (c.1%pt) as well as a slower rate of improvement in warehouse efficiency.

The problem is these just don't look that severe in an environment where discretionary spending is being squeezed (although perhaps not for the average Joules customer!) And, in this case, they are into doing the following:

Under this scenario, and without mitigating actions, all banking covenants would still be met, but the Group would breach its current borrowing facilities for three months in FY23.

However, if this scenario were to develop, the Group has numerous mitigating actions available, including (but not limited to):

· reducing capital expenditure

· reducing discretionary revenue expenditure (not including performance marketing)

· rapid clearance of aged stock

The problem with these is that they transfer pain to the future, either directly or through loss of brand value. Given that the headlines of these results were not as bad as Mark expected, then he was tempted by a trading buy for the recovery in sentiment this morning. However, he had to remind himself that, despite the big fall here, this is NOT cheap. We are looking at 3p of EPS and an upper-teens forward P/E. For a company at a very real risk of breaching its borrowing facilities.

Even if they survive without an equity raise, the recovery must be now looking much further out into the future than before, and at a lower level due to the investment being cut. Although it will be painful in the short term, but at 55p they still have a market cap of £61m, and a placing and open offer of around £30m at say 35p should be enough to see them through. Long term it would be better than the slow destruction of the brand and a slide into oblivion.

Since the morning of the results, there has been a significant bounce in the share price (Mark should have had that trading buy, doh!) Presumably, this has been driven by a combination of investors who have anchored on previous high prices and some short-term momentum traders. Surely the management would be daft not to take advantage of this new exuberance to shore up their creaking balance sheet?

Alumasc (ALU.L) - Interim Results

The headlines from this week’s results are a bit underwhelming:

Revenue up slightly, but pretty much everything else down. 2020 had some exceptional characteristics, but construction is meant to be booming so these aren't great in the current environment. The issue, as with a lot of businesses is cost inflation:

The strength of our brand positioning and customer relationships allowed the successful pass-through of input cost inflation. As a result, gross margin was only slightly diluted at 34.6% (H1 FY21: 36.7%).

They say successful pass-through but gross margins down a couple of per cent show that they are not immune. And the overall level of Gross Margin shows that they have a weak moat, and is way below something like Somero has in the construction sector. Overall they say:

The business is on track to deliver against its full year expectations and looks forward to the future with confidence.

Which presumably are the finnCap forecasts:

So this is effectively for H2 to be slightly up on H1, but not by much. While the P/E looks good at sub 10, the EV/EBIT is less impressive, particularly when both figures are on an adjusted basis:

Net debt increases to £4.1m due to working capital outflow and the repayment of deferred VAT. finnCap is forecasting £13.3m EBITDA for the year, but further working outflows and other contributions mean that FCF for the year is likely to be negligible. And these figures ignore the pension contributions. They say:

The Group's pension deficit reduced further to £2.5m at December 2021 (June 2021: £4.6m, December 2020: £12.8m), as a result of the £1.3m of deficit repair payments, investment gains and the effect of higher bond yields, which offset an increase in the inflation rate assumption.

£13.3m EBITDA - £2.6m annual pension payments = £10.7m and we have a true EV/EBITDA of around 8. Again, there are better quality companies growing faster than this that are on lower ratings. However, on the plus side:

The scheme's next triennial actuarial valuation is scheduled for 31 March 2022, and the Group expects to conclude ongoing funding discussions with the scheme trustees prior to publication of its full year results later this year.

So if they can agree to lower pension recovery payments this will look better. As of writing, their website isn't giving us their annual reports so we can't see the precise figures but in the 2019 results they said:

The valuation of Alumasc's defined benefit pension scheme deficit for accounting purposes at 30 June 2019 using IAS 19 valuation conventions was £13.0 million (30 June 2018: £15.1 million).

and:

Early indications are that the triennial value of the scheme's deficit has reduced from circa £33 million in 2016 to the low/mid £20 million range in 2019. This suggests, other things equal, the Group is on track to repay the deficit during the remaining eight years of the existing funding plan.

There are lots of moving parts here, but best guess is that the next triennial is still going to show a £10m+ deficit. Which with a now 5-year recovery period would be £2m a year and a similar level of payments to today. Although the end of the payments is perhaps getting closer, by then, we could be well into the down cycle for construction products. And in light of this, 8x EV/EBITDA is not exactly good value for this type of cyclical business.

Goldplat (GDP.L) - H1 Trading Update

As most readers are aware, GoldPlat is very much Mark’s style of company, and very much not Leo’s. The reason Mark likes it is mostly that everyone else hates it: it is based in a scary jurisdiction, is a microcap with almost no liquidity, is not an explorer with a big potential resource to get the rampers interested, yet is a resource stock so serious UK investors won't touch it, plus it has a rather chequered history of underperformance.

If you didn't hate it before, you hate it now, right? Well, here is their H1 update:

The two recovery operations achieved a strong combined operating profit for the quarter of £2,356,000 (Q2, 31 December 2020: £1,554,000), a 52% increase from the comparative period ended 31 December 2020. The Ghana operations continued to perform well with a steady supply of material and achieved an operating profit for Q2 of £1,012,000 (Q2, 31 December 2020: £569,000). The South African operations achieved an operating profit for Q2 of £1,344,000 (Q2, 31 December 2020: £985,000).

As often the case, a graph makes things easier to view the big picture:

So their Ghana recovery operation continues its march upwards in profitability and the South African operation is now making a very decent recovery. Things are now looking the best they have for a number of years. Although a stronger gold price has helped, a lot of this improvement is operational not just good fortune.

Perhaps the only weak point in the trading update was that the cash balance was only £1.5m but this was due to working capital flows which have since reversed:

Our cash balances remained strong at £1,452,000 at the end of Q2, with a significant balance invested in inventory and debtors at the end of the period. At the date of this announcement, the cash balance in the operating entities was £3,850,000.

This puts them back in a net cash position after they took on the c.£3m loan to buy out some of the minority interest in SA.

If we assume that both recovery ops can generate £1m per quarter of operating profit in H2, which seems very achievable based on the Q2 performance, then EPS should come out at about 2.8p. So a forward P/E of 2.5 and an EV/EBITDA of c1.5. Now there’s a rating you don’t see much in the current markets!

Of course, low ratings mean nothing if the cash never makes it back to shareholders pockets. However, in this case, management have committing to paying dividends again (pushed by a large private shareholder who is now a non-exec.) With their previous mining operation hived off into a separate company, and now returning cash as a smelter royalty on production, instead of requiring capex, Mark doesn’t see why they couldn’t pay a steady-state dividend of 1-2p in the medium term. It might require this cash to start reaching investors bank accounts before the hate finally starts subsiding, though.

Omega Diagnostics (ODX.L) - Placing & Sale of Alva

A placing was flagged here at the end of January, but market conditions started to get in the way. At the time, they said:

As per the announcement of 19 January, the Company has significant cash resources . Accordingly, there is no immediate need to raise additional capital and the Company may choose not to proceed with a fundraising until such time as conditions are more favourable.

Not sure conditions could suddenly be considered more favourable. Still, their broker finnCap have done well to get this away, even if they had to do it at a 31% discount for 100k shares versus 182k existing. And this discount is off what is close to all-time lows!

The board are participating in what looks like a PR move. Perhaps this contributed to the reason for the recent resignations - not wanting to throw good money after bad? Additionally, there is an open offer. This is the cheapest most inclusive and most targeted way to allow existing shareholders to contribute. But the open offer part cannot be guaranteed. If the price falls below 5p it will probably not be taken up in full.

The net proceeds of the Fundraising, amounting to between £4.6 million and £6.6 million, depending on the take up of the Open Offer, will be used to drive growth in the profitable and growing Health and Nutrition Business, whilst also providing the necessary finance to relocate CD4 production to the Company's new, purpose-built manufacturing facility in Ely, Cambridgeshire, as well as supporting a transition to a sub-contract model for COVID-19 test manufacture.

This seems like a stretch. Perhaps a less generous commentary would say that it will be used to prevent emergency cost-cutting and likely collapse of the company. This is an emergency fundraising. Of course, the ongoing spending which now won't be cut (so much) was for investment.

Previous investments have been spectacularly unsuccessful, albeit not entirely predictably so or due to much fault of their own;

Without the DHSC contract for COVID-19 antigen LFTs, the Company intends to pursue opportunities in the commercial testing market, focusing on the travel and retail markets

I think general consensus is that the travel testing market will cease to exist in 3-6 months time and, of course, it is already well supplied.

The Company does not intend to purchase the Government-funded equipment for its own use, and is currently facilitating discussion with partners who may be willing to purchase the equipment.

To be clear, this won't result in any cash inflow, as the government are demanding their money back. Here's the potentially viable bit of the plan:

The Board will therefore focus Omega's efforts on its core business, primarily in pursuing sustainable growth opportunities in the Health and Nutrition sector, maintaining its leadership position and targeting significant organic growth through embracing digital technologies and related marketing activities.

Today's fundraising will mean the company will continue to exist for at least another 9 months in order to pursue this. But they face the usual problems UK companies have of breaking into US markets. If this requires regulatory approvals it is unlikely to work:

The Board believes the best route to market would be to replicate the Company's CNS Laboratory service direct to health care professionals and ultimately direct to consumer. Omega differentiates itself from established players by taking the Group's tried and tested market leading approach with education and support, coupled with its digital strategy, to engage and empower customers.

Later they admit that this really is an emergency rescue fundraising, not for growth:

"Working capital" means "keeping the lights on". "Exit Alva" and "Relocate CD4" is emergency cost-cutting to keep the lights on. Only £1.5m is for growth, and this is coming from the open offer. Nothing from the placing is for growth.

Also today:

Omega…announces that it has signed a conditional sale and purchase agreement with Accubio Limited, a wholly-owned subsidiary of Zhejiang Orient Gene Biotech Co. Ltd in relation to the sale of Omega's diagnostic test kit manufacturing business and facility in Alva, Scotland, for a cash consideration of £1m, payable at completion.

As many will be aware, Orient Gene are a major supplier for of LFT to the DHSC. It is the second generation of test available to pick up for free as part of the testing programme - the one with instructions to do the nose only and correspondingly short swabs, which, if you follow these instructions, may delay Omicron detection by 12-24 hours. Last time Leo checked it has not passed the UK testing regime either, but was excluded as already in use when it was brought in and the test sensitivity is similar to the now-abandoned ODX consumer-use test in independent testing.

This is the final insult - after having their business arbitrarily destroyed by the DHSC they have been forced to sell manufacturing to a competitor that side-stepped the rules. However, this and the new management draws a line under the affair and the company should be considered on its future prospects from now on.

Marks Electrical (MRK.L) - First Look

Although there was no specific news this week, this company came to Leo’s attention recently. On the face of it this is a company that should not exist in a world of scaled-up and often loss-making competitors:

Marks Electrical is a fast growing, technology driven online electrical retailer which sells, delivers, installs and recycles a wide range of household electrical products.

First thing Leo noticed from the admission document is that the company only received £2.6m from the November IPO valuing it at £115m. So the IPO appears to be so that the founder can extract £25m. It is extremely impressive that the founder would have retained a 100% shareholding since the business started in 1987. The reason for an IPO rather than a trade sale appears to be so that he can maintain full control while extracting some cash.

FY 2021 to 31st March was a standout bumper year, with revenue up around 80%, profits up around 5x to £5.7m and operating cash flow more than doubling from recent levels to £2.8m with ongoing low investment spend. This assumption is of course that this performance was boosted by lockdowns and the IPO was timed to take advantage of this. On current trading, back in November, they said:

Whilst the strong start to the first half of FY22 is pleasing, the Group faces a tougher comparable in the second half of the financial year and hence the Directors expect the revenue growth rate, whilst remaining strong for the year as a whole to moderate somewhat from the 78 per cent. as experienced in the first six months to 30 September 2021.

Of course, there are IPO costs to consider, both one-off, and ongoing higher costs:

From a profitability perspective, the Group has made material investments in advertising and marketing in the first half of FY22, as well as professionalisation of the business as it prepares for life as a publicly traded company.

These investments have impacted margin but the Group is targeting an Adjusted EBITDA margin of greater than 9 per cent. in FY22 and thereafter, as it generates operating leverage over the investments made in overheads.

These costs were not yet fully included in the H1 results issued soon after IPO in November. A Q3 update was issued in January which showed revenue growth of only 27% in Q3 versus 78% in H1, as they warned:

Record trading period in Q3-22 with 27.4% revenue growth to £22.3m (Q3-21 £17.5m), including a strong performance during the seasonally important Black Friday and Christmas trading events

Because Q3 sales are significantly more than in Q1 and Q2, this slowdown has a disproportionate effect on the year to date, reducing YoY growth from 78% for the first 6 months to 55% for the first 9. Counterintuitively, Q4 is also a very strong quarter, or at least it was in the FY to March 2021, where revenue was almost as high as Q3.

So, although they have done very well to follow a (coincidentally) 78% rise for FY 2021 vs FY 2020 with a 55% rise for the first 9 months of FY 2022, I think Q4 will prove the hardest comparable yet. If they match last year's figures in Q4 then we're looking at +38% for the full year. Still pretty good. H2 EPS is also very difficult to judge because this would be the first time listed company costs will full accrue. As there is currently no PI-accessible broker coverage we have to rely on Stockopedia. It was Panmure Gordon that brought them to market and acts as NOMAD, so presumably, these forecasts come from them.

Stockopedia have £81.2m revenue for FY 2022 (remember, to 31st March). That implies the following progression:

(We don't have Q1 and Q2 figures so have used half of H1 for each).

So we have a 23% revenue growth rate for the latest period. What that will stabilise too is clearly a matter of opinion, but if you assume 20% then you can expect normalised EPS to rise faster than that with a bit of operational gearing. However, comparing FY 2022 EPS forecasts to FY 2021 you can see the effect of extra AIM costs and advertising spend), with EPS forecast to fall despite revenue up 45%. Going into FY 2023, Panmure has revenue rising a further 20% with operational gearing overcoming the costs of annualising AIM costs and EPS up 23%.

So, based on this naïve analysis, albeit not as naïve as the Stockopedia summary, even with a forecast PE of 21x, they are on an adjusted PEG of below 1 and don't look bad value. However the big question is around the "covid effect", the nature of the benefit it has given them and whether it will unwind / competitors catch on in future. The good news for any shareholders is that I think we can rule out the possibility of covid driving a one-off benefit with revenue falling back to pre-covid levels. If this were going to happen then it would have already done so. Rather, the evidence shows there has been a structural shift in their favour. The question is whether this is something that will allow them to grow faster than usual, or just creates a new baseline, and also whether it will attract competitors.

CAGR of revenue in the approx. 18 years from 2002 to 2021 was 22.3%. But as you can see from the log graph below, growth has been less than consistent. There was a significant dip in 2007.

The competitive landscape is important in a mature sector. Comparing to the more well-known AO, Marks’ products are mostly priced the same, and in some cases cheaper, for nominally the same next-day service. More items seem to be in stock at Marks’ too. Their Trustpilot rating is truly exceptional at 4.8/5 vs 4.6/5 for AO.

Marks’ are going for a premium position with the products they sell:

in FY21 within the Cooking product category, the average price of products sold by the Group was 81 per cent. higher than that of the UK MDA market average for cooking products.

Substantial premiums were also achieved within Dishwashers (57 per cent.), Refrigeration (79 per cent.) and Washers & Dryers (45 per cent.)

Marks’ directly employ drivers which will be a massive, massive advantage in the current tight labour market. However, Marks still use third parties for installation, which is likely to lead to a less integrated service offering.

What about at the other end - sourcing stock? Marks’ joined the Combined Independents buying group of independent electrical specialists in the late 1990s to source products. Whereas AO uses direct purchasing. However, this doesn't appear to lead to better prices or availability for consumers of AO. Yet, how big can Marks get and still be part of an "independent" buying group? They currently have circa a 1% market share in the UK.

It sounds like part of their advantage is also their in-house IT team. Their website is notably exceptionally fast, compared to AO's which is only "fast". Interestingly they get 37% of revenues from telesales, saying:

website transactions typically see a lower average order value than telesales due to the more limited scope for upselling

As we have seen elsewhere:

The Directors believe that in FY22 to date the Company has seen increased competition in UK PPC [pay per click] and, as a result, increased digital customer acquisition costs.

The split of returning customers has been broadly stable at approximately 19-20 per cent. of overall orders. This has always been a concern with AO - selling stuff at a loss might make sense if you are acquiring customers, but how often do people buy white goods? Marks' greater focus on AV will help here.

Historically, marketing spend as a percentage of the Group’s revenue has been between 5-6 per cent., the majority of which is spent on Google advertising (PPC). In FY21, this was reduced to only 2.9 per cent. as a result of the COVID-19 pandemic.

This lower ad spend will have contributed to the large jump in EPS. However, apparently more recent growth is thanks to the resumption of adwords spend:

The Director’s believe that marketing spend is having a significant impact on website traffic; in the last six months website traffic increased 79 per cent. which is substantially above the rate of growth of key competitors over the same period.

Overall, compared to AO, Marks’ appears to basically be the better business. Better run, higher margins, lower costs and a larger runway. On the other hand, share liquidity is likely to be poor. Looking at recent trades it isn't terrible, but not good.

Comparing valuations is complicated by the fact that only one of them has a working business model. Theoretically, if AO could earn Marks’ margins on its sales then they would be much better value. But there's no reason to think they could.

On an absolute valuation, Marks’ current 17x EV/EBITDA could be justified if the forecasts were conservative. Albeit, without seeing the brokers note, we don't believe they are. Marks’ price is already falling back to the IPO price, so what's going to happen if they miss forecasts?

Summing up: if you were thinking of buying AO, then the very second thing you should do, after giving yourself a big slap, is to consider buying Marks’ instead. But, for us, the valuation means that Marks’ is just something to watch for a post-IPO stumble. Still, they've sold it to us as potential customers.

For those interested further, though, this is a really good interview:

Right, that’s all for this week. Enjoy your weekends!