Small Caps Live Weekly Summary

SP500 EURUSD BKS STAF WYN ZTF

Thanks to everyone who made it out to the SCL Investor Meet this week. A particular thanks to Mark Smithson and Josh Egan from Marks Electrical, and Conor Rowley from Capital Ltd who came to present. We learnt a great deal about both high-quality businesses.

Given the effort required to organise such an event, we hope you will forgive the slightly fewer companies covered this week.

Large Caps Live

So let’s start with some macro charts - S&P 500 continuous front month future (ES1!) – in essence, this is the S&P:

Basically, it is clear that we doubled from the bottom in March 2020. Perhaps more interesting is what has happened in the last 3 or so months – we have been in a down channel.

(The channel lines are drawn at 2 standard deviations – clearly, I could have drawn at say 2.7x or something and got the extremes in - The 20d and 200d SMA are also on the chart.)

It is easy to think that the S&P will continue to bounce from here. I am not entirely convinced. I think that the key questions are:

1. What happens in Ukraine

2. What happens with inflation

3. How much does the Fed tighten. I think that interest rates will take time to take effect - probably an 18 month lead time. And more importantly, is quantitative tightening or how quickly the Fed reduces its balance sheet.

4. I have said many times before that the Fed takes its pricing (= input) signals from the US economy but its outputs (ie rates/dollar liquidity) influence the whole world. We can judge liquidity in other countries by soft signs eg in China in Dec the PBOC cut the RRR to 8.4% with a level of 5% for smaller banks. And of course, we have had various Chinese property companies go bust. All of this suggests to me that Chinese financial liquidity (which is influenced by the Fed if you tie your currency to the USD) is stressed.

Now let’s turn to currencies, with EURUSD:

This clearly shows that since the invasion money has gone into dollars and away from the Euro. I think this is a ‘safety’ trade. I think that there are additional things that are happening:

(1) In a crisis the dollar is considered the place of safety

(2) In addition the war is on the Eastern side of Europe – so why would you risk your money within the range of a warzone.

(3) Increased volatility means that people de-lever. And often that means moving your surplus cash back to your base currency which for a lot of fast money is USD

(4) Industrials etc buy commodities in dollars and so increase their USD liquidity at the time of a crisis.

(5) The general need for dollars for fuel etc.

(6) I think there is another issue that people have not really considered. The Russian central bank had circa $300Bn of reserves ceased – a lot of them were in dollars. Lots of Russian related businesses are facing sanctions. Who knows where the chains of customers and suppliers end up – and what contracts have needed to be cancelled. I think in that situation it is unsurprising that a lot of corporate treasuries and banks would hoard liquidity – in dollars – whilst they work through everything.

IF Russia continues in Ukraine, we have about 3.5M people already as refugees - let’s say that hits 4.5M. That is a massive population impetus to Europe as a whole. And those are energetic and hungry people and a lot of them are kids. So over 20 - 30 years I think that is a massive boost to European GDP. And if Russia leaves Ukraine - there will be a massive rebuild and then more European integration. So I am thinking that over a 30 year period I think that either way European GDP should pick up. This should be positive for the Euro, in the long term.

Small Caps

Beeks Financial (BKS.L) - Interim Results

The revenue increase here is impressive:

Revenues increased by 46% to £7.72m (H1 2021: £5.29m), of which 89% is recurring

However, this company seems to have the opposite of operational gearing:

· Underlying gross profit up 21% to £3.14m (H1 2021: £2.59m)

· Underlying EBITDA* increased by 41% to £2.43m (H1 2021: £1.72m)

· Underlying profit before tax** down 18% to £0.45m (H1 2021: £0.55m) following increased investment into the business as previously announced

And these are the adjusted figures. The unadjusted ones look terrible:

· Loss before tax of £0.27m (H1 2021: profit of £0.50m)

· Basic earnings per share of a loss of 0.42p (H1 2021: profit of 0.85p)

· Statutory gross profit of £2.97m (H1 2021: £2.36m)

You really need to take a view on how realistic it is to exclude things like share-based payments. All of these may be exceptional, but they don't appear to be non-recurring.

Even "Other non-recurring costs" occur regularly.

But the (first) elephant in the room isn't the adjustments, but how capital intensive this business is:

They have capitalised £7.3m of investment to increase revenue by £2.43m in the six months. Their gross margin of 37% doesn't suggest any great competitive advantage so this capital intensive growth is likely to remain the norm, too.

In 21H2 they raised £5.2m from shareholders. Despite this, we have a second elephant in the room: the balance sheet has one of the worst current ratios we have seen at just 0.51.

This is because they have £3.5m of current debt and £3.3m of payables. We doubt the bank is too worried since the debt is presumably secured on the £2.3m freehold property and £9.4m of computer equipment and will simply go in and re-possess all of that if they default.

Given the nature of the business, the payables are perhaps accrued electricity costs, wages or computer equipment delivered but not yet paid for. Which means that if or when asset growth ceases this will need to be normalised. They say:

...we continue to evaluate Beeks' working capital and investment profile in support of our growth objectives and strong pipeline.

Which sounds like another raise is on the way. Canaccord have never had any issues getting these away in the past since it seems to be a story that shareholders readily buy. However, this is a "growth" company whose EPS for 2023 is forecast to be below 2021 and is on 32x 2023E earnings. And this is for a company which has a relatively low gross margin and is very capex intensive. Seems bonkers to us.

Beeks followed up these results with a contract win:

multi-year Private Cloud contract. The contract , worth £4.4 million over five years, is for a new European Tier 1 client, and was secured via a partner.

£4.4m over 5 years is £880k a year, so this is material to Beeks which did just £8m of revenue last year. At the current 37% gross margin this is another £320k to the bottom line, which is enough to push them into profit.

However, they don’t say if this contract requires further capex, which they patently can’t afford in the short term. Even if this contract win can be delivered from existing capital invested, they likely need more money soon and the announcement of a sizable contract win is exactly what you want before a large placing. The subsequent dilution will make the valuation look even dafter, however.

Staffline (STAF.L) - Full Year Results & Contract Win

Revenue, gross profits and underlying operating profit were already announced on 25th January. As previously commented, the end of January was about the time that previous management used to publish FY results for the year ending 31st December! Unfortunately, it turned out that results published within a month of the year-end were not terribly accurate and the new management sensibly decided to do them properly. Still, today's results are fully audited and still very quick.

They have also found a bonus of £0.3m extra operating profit since the provisional January numbers. But, as ever, the focus will be on the outlook:

The Group has an encouraging pipeline of opportunities emerging across traditionally strong sectors such as automotive and travel as the UK economy continues its recovery from the Covid-19 pandemic

· The Group has today announced a major contract win with BMW and a material extension with Vinci an existing customer, demonstrating Staffline's scale, reach and its capacity for increasing market share

· Whilst macroeconomic uncertainty has increased, the Group's strong market share in resilient sectors such as food distribution, logistics and on-line sectors provides good visibility of revenues

· Overall, the Board of Directors is confident that Staffline has the operational and financial foundations in place to deliver sustainable growth

· We have made a strong start to 2022 and are confident in meeting our expectations for the full year

The question that immediately strikes me is whether the "major" BMW contract is actually a "Mini" one. That statement is described as a "Customer win":

It is anticipated that the contract will commence in Q2 2022 and BMW Group will become one of Staffline's top 5 clients.

The question with contract wins is whether they are really extensions. But this seems to be a new contract with a new customer. It is also clearly major - more MINI Clubman than Morris Mini. They say:

Management also believes that this contract, combined with the notable increases in demand that are evident across Staffline's core automotive and automotive supply chain services, will see the Group's activity within this segment return to pre-pandemic levels from H2 2022 onwards.

This is quite an achievement - we’re not sure the UK automotive manufacturing sector as a whole will ever return to pre-pandemic levels.

Car manufacturers have recently employed a mixture of permanent and short-contract staff. What is not clear is whether this is part of a move to change the balance more towards shorter contracts, or whether they are moving management of existing contract staff to Staffline. We can't see anything in the general news about it so I assume the latter, but this is a reminder that Staffline's business can and has been controversial. The implication is that they may be handling some full-time recruitment also:

supply the flexible operational workforces and a number of specialist roles for its manufacturing sites in England.

The other contract win is clearly flagged as an extension, but nonetheless, five years is very significant. There is no indication of size, rather:

It also points to encouraging signs of recovery in the construction industry, historically a strong sector for [Staffline unit] Datum

There seems to be a lot of scepticism in the market about the company because a merely "inline" statement has resulted in a 6% rise on top of a share price that was very strong going into the results.

Broker Liberum comment:

After upgrades in January, we now leave EPS estimates unchanged, with possible upside from inflation

On the war they note:

The situation in Ukraine will not materially affect the work-force since there are only 25-30 Ukrainians on the pay-roll. However, it may affect customers’ supply chains and the wider economy, and Staffline is most exposed to GDP cyclicality through the high margin perm business which has been growing in the mix. It is worth noting that food production is Staffline’s largest market and this tends to have low GDP cyclicality.

With forecasts and finances now stable, the Stockopedia Stockreport now has some value in assessing the company. They report it is a "Super Stock" on a forward P/E of 13.7x (before this week’s rise). However, they are missing both FY 2023 and newly introduced FY 2024 forecasts which are for 5.8 and 6.0p EPS respectively. Staffline's unique position in the market and scale advantages that technology drives ever higher means that there is plenty of scope for an outperformance vs. these forecasts. On that basis, they seem cheap at the current mid-60s share price. But, there is no getting away from the fact that they have risen 32% within a month on a worsening macroeconomic outlook. As such, this may be better as a trading stock than a long-term buy-and-hold.

Wynnstay (WYN.L) - AGM Statement

fertiliser operations at Glasson have continued to experience one-off gains from the exceptional current trading environment that has been sustained into the current financial year.

Leo often points out that in an inflationary environment FIFO accounting flatters distribution profits, although cash flow remains the same. We expect Wynnstay to be a beneficiary of these trends.

Market volatility across most commodities has persisted, with material price increases since the start of the calendar year. The recent outbreak of war in Ukraine has exacerbated this, and raised concerns over the supply of fertiliser and wheat, in particular. Energy and transport costs also remain a challenge.

Wynnstay has managed these difficult circumstances well, and once again the Group's broad spread of activities is proving a major strength. Farmgate prices have remained strong, enabling customers to absorb elements of this inflation, although higher prices are expected to curtail some demand.

Wysnstay is in a good place being able to pass on cost increases relatively easily.

On 18 March, the business completed the acquisition of Humphrey Feeds Ltd and its associated pullets business for an initial consideration of £9.5m. As previously reported, the acquisition is expected to be immediately earnings enhancing, and furthers the Group's feed activity in the growing free range egg sector, expands its manufacturing capacity, and opens up expansion opportunities in the South of England.

Not a good time to be getting into free-range eggs on the face of it, as they are banned on avian flu concerns. However, we suspect all the inputs/equipment are the same as Barn Hens, and if anything feed inputs would need to be higher. Outside equipment seems to be very limited on the pictures Leo has seen.

They conclude with the standard: "Wynnstay remains well-placed to achieve its goals for the current financial year.", but Leo think the real outlook is this:

I am pleased to report that trading in the first four months of the new financial year has been in line with management expectations across core activities, while fertiliser operations at Glasson have continued to experience one-off gains

So: Core inline, and one section outperforming => will exceed forecasts.

However, Shore read this as inline overall. But due to the acquisition:

we upgrade our FY22F and FY23F adj. PBT by c.3% to £11.0m and c.7% to £11.9m respectively.

The share price is flat on this update but has been strong over the last couple of weeks as investors realised that a Ukrainian war was more of an opportunity than a threat. This is another slightly expensive-looking SuperStock according to Stockopedia, but again, forecast beats are likely.

Zotefoams (ZTF.L) - Preliminary Results

These don’t look great:

While the revenue is up, that gross margin is really hurting them. Where they say:

• Profit margins impacted by:

- Significant and unpredictable cost inflation with a lag on sales price increases

- Unfavourable currency movements

They call themselves "a world leader in cellular material technology" however, those gross margins don't exactly scream competitive advantage, even before recent troubles.

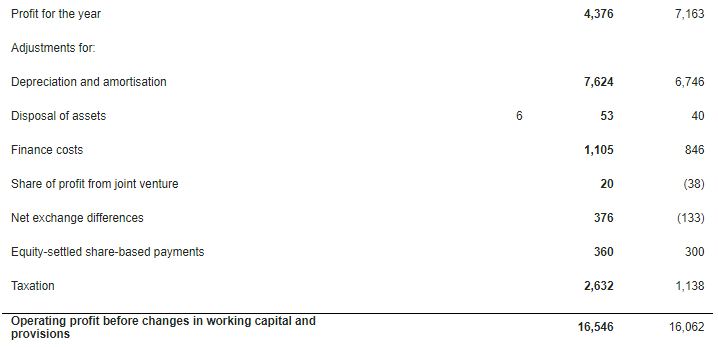

Cash generated by operations isn't as badly affected as EPS, but net debt hasn't reduced:

So we need to read the cash flow statement to find out what is going on:

Higher depreciation, finance costs and that FX effect means op cash flow before working capital is actually up slightly. The tax charge was also higher than the tax paid due to:

a non-recurring significant increase in the deferred tax charge mostly reflecting the planned increase in UK corporation tax

A slightly higher working capital build means that Operating Cash Flow is down slightly. Dividends + purchases of PPE & Intangibles eat up the rest of the cash meaning net debt remains similar. On the working capital, this is the current assets:

The receivables are about 3 months which makes sense for a largely automotive customer base, however 3 months’ worth of inventory doesn't look great. Current liabilities of £37m means that the current ratio looks good, however, £26.6m of that is debt, and there is little sign that they can turn the current assets into cash quickly.

This is a company that has managed to consistently grow revenue at around 10% a year, however, its book value has grown at a similar rate showing that this growth is capital intensive. The low gross margin means that there is no operational gearing and the EPS peaked in 2018 and is unlikely to return to these levels any time soon.

So how do we value such a business? Firstly, their commitment to paying a dividend is good. They have declared a 4.4p final dividend for the year, making 6.5p in total. This has been increasing around 3% over time, including this year. Stocks have typically returned around 10% nominal returns so a 7% yield is probably a reasonable level, assuming the 3% future growth. 6.5/0.07 = 93p fair value.

Secondly, we can also look at earnings. As a whole, this is a low-growth, capital intensive business with low margins and a weak outlook for the sector. As such a maximum of 4x EV/EBITDA is all you would really want to pay. EBITDA is £16.1m, so an EV of £64.4m seems fair, which is £31.2m market cap. With 49.3m diluted shares in issue, this is around 63p.

Zotefoams fares better on assets, with a Tangible Book Value of around 203p/share. However, given that these assets are relatively unproductive you wouldn’t want to pay a significant premium to this for the shares.

Finally, we come to a sum-of-parts valuation. Bulls of the stock will be keen to point out that Zotefoams has a mix of product lines. The growth of the successful product lines is being masked by the unsuccessful ones. We like to look for this sort of hidden value when it is being missed by brokers, as it is with the rapidly-growing Capital Ltd. subsidiary MSALABS. You have to be careful when applying this logic to product lines, however, since it isn’t always possible to produce just the profitable lines. For example, you would be daft to value Somero as a sum of parts on the incredible growth of Boomed Screeds alone, since their products are all produced in the same factory by, presumably, the same people and demand between product lines is somewhat cyclical.

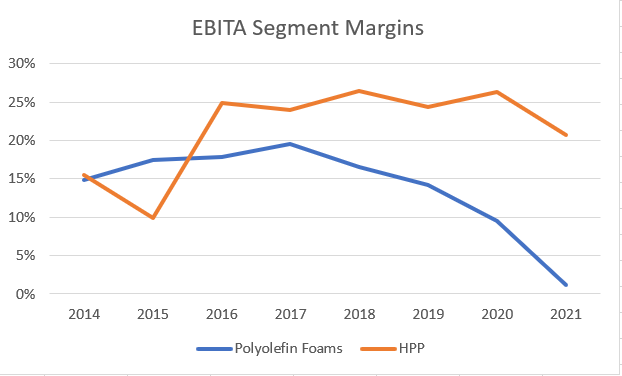

This caveat aside, clear segmental reporting allows us to break out how each product line is performing for Zotefoams:

HPP is clearly the star of the show with consistent revenue & profit growth. However, this appears to be growing linearly and doesn’t show signs of operational gearing:

Over the last few years, HPP has grown around 15% pa, so if we apply say a 15x multiple to the profits here, after pro-rata-ing the central costs and applying tax then we get a c.£95m valuation.

Despite MuCell being a highlight of 2021 according to the company, and them mentioning their development of ReZorce 31 times in the results, this business unit shows no sign of growth or profitability over the long term.

The core Polyolefin business looks in trouble, it will be now loss-making after allocating central costs, and the decline in profitability since 2017 despite maintaining sales, suggests a commodity business without any competitive advantage.

I think if we were feeling very generous, we could argue that Polyolefin should be valued at 1x sales which is £56m, which assumes that this can be successfully turned around. This may be quite optimistic since the CEO has been in place since May 2000, and so far has shown little tendency to address this failing part of the business in the last few years.

Again, generously, we could assume that the MuCell investments over the last few years are not wasted and it can finally start growing revenue long term, and value it at net segment assets of around £9m.

Overall then, our sum-of-parts valuation ends up at £95m + £56m +£9m - £34.3m net debt - £4.7m IAS19 Pension Deficit = £121m, or 245p per share.

So based on different ways of valuing the business we have a valuation ranging from 63p based on income, to 245p on a generous sum-of-parts valuation. Sadly this makes the current 325p share price look significantly overvalued on all metrics.

That’s it for this week, enjoy the sunny weekend.

@ Mark - Happy to join the discord server ; sounds useful but you would need to send me an invite I believe ?

BKS: I always appreciate a Company appraisal written with a negative slant - I'm very optimistic by nature and I really need a contrary viewpoint. BKS looks very capital intensive based on a snap-shot set of results - investment has gone into two new product propositions and a third on the way. Also, each contract win requires up-front capital investment - so funding expansion will clearly require additional capital.

The above analysis, by matching current revenues (that haven't yet benefited from this investment) against the investment spend and concluding that the business model is flawed - is too easy and isn't very helpful. The key question is whether there is a continual need for capital investment and if so does the pricing adequately reflect this?