Small Caps Live Weekly Summary

SHI UPGS CAM SNWS AML NUM SOM SMRT

A relatively quiet week this week with a UK Bank Holiday on Monday meaning there was no Large Caps Live this week plus just a small amount of small cap news so the email is going out early.

Mark is talking at Mello Monday next week on ‘When to Sell’ - plus it looks a good line-up, so make sure you get your tickets.

A small change in format this week. Lots of people are reading the email (thanks everyone!) but few people are using the direct links to Discord so I will get rid of these since discord has an excellent search function for those who want to find the full discussion. [A Discord server invite is here.]

Also, I will now use quotes for company statements instead of our discord discussion which should improve readability.

Small Caps Live Wednesday 5th May

SIG (SHI.L) - Trading Statement

The building supplies merchant, SIG Plc, became popular amongst private investors since, at one point last year, it had more cash than its market cap. Unfortunately, this was due to an extreme working capital position. The balance sheet was, in fact, much weaker than it first appeared, as was shown by the subsequent need for SIG to raise a large amount of equity. This was slightly controversial since they gave preferential treatment to a large new Private Equity company, allowing them to invest at 25p but offering at 30p to existing shareholders!

It didn't seem to dampen the love-in, though, with the share price rising on the news. However, the large losses at the half-year to 30th June subsequently took the shine off, and the share price even went below the PE placing price. Since then, however, the price has doubled as the recovery narrative has played out:

Today we get a trading statement confirming that recovery:

The Group has made an encouraging start to the year, with the Return to Growth strategy continuing to deliver good progress and with trading underpinned by continued strength in RMI demand. After a solid start in January and February sales volumes then picked up strongly, and March and April traded ahead of management's expectations.

However, you have to ask: how low were those expectations? Looking at the figures, group like-for-like sales are still down 4% on 2019:

Yes, there have been lockdowns in this period, but their stores will have remained open during this period. And construction in most markets is absolutely booming.

The outlook is all very positive:

The momentum we have seen through March and April, together with improving visibility on the near-term order book, means that we now expect the Group to deliver an underlying operating profit in the first half, returning the Group to profitability earlier than expected.

But this is an £800m EV company – and the profit will be minimal despite booming conditions. They note caution for H2 as well

Given the prevailing macro-economic uncertainties, we retain a cautious view of the second half at this stage. We do however continue to expect the second half to be both profitable and cash generative, and in light of the stronger than anticipated recent performance we now expect full year revenues to be slightly ahead of prior expectations, and profits also to be higher than previously expected.

Prior expectations were a £20m loss, according to Stockopedia. And I think they run the risk that building material inflation will catch them out. As widely reported, lumber prices in the US are hitting home construction costs.

@mojomogoz on Twitter has an interesting theory on SIG:

Isn't today's tu disappointing given the strong housing backdrop in UK? What's wrong with the biz? French biz is the cream. Did you notice that PE biz that took big stake in Sig dropped 2 frenchmen onto board? What's going on? The CEO is not a business builder, he's a financial re-engineering guy....I doubt he knows what growth is (his rhetoric on this has been fluff not substance). Looks to me like PE guys want to carve off the profitable and well run french biz leaving UK runt.

With the placing, the management has shown that they are willing to give preferential treatment to Private Equity, so although it seems a little bit of a conspiracy theory, it is certainly possible.

UP Global Sourcing (UPGS.L) - Results Presentation

There was lots of focus on EBITDA margin - mentioned in CFO run-through and again in questions. This is a bit mangled, but hopefully, you get the idea:

Q. How much more could sales grow with current overhead costs?

A. I think this is our revenue grows at some point, so opex inevitably has to grow. But we believe that we can grow our revenue line at a significantly faster rate than our opex and the key, the key metric, there are gases that EBITDA margin can we keep? Move, you know we moved there from 9% year last year. I could do that development of forecasting nine and a half. We've set ourselves a target of 10. And we're very confident we're going to get there. It's a question of when we feel, not if. I think beyond that, Hannah, I think it imposes certain questions about what would we do if if we were heading towards 11 or 12? You know, what would we? Would we recycle that into investments in price or areas such as marketing?

Clearly, continuing growth margins combined with growing revenue would have a big impact on profitability. It was also made clear once again that the 6% revenue growth used in ED forecasts is merely a placeholder based on the long-term sector growth and ignoring special factors sector-wide this year. I know I keep banging on about this, but it is really important. In principle, it could be more or less than 6%, but I thought it was very very clear it would be more. That means the ED forecasts are too low.

Traditionally, Action and B&M have been their two major customers, accounting for 46% of revenue at IPO. This very badly bit them in the bum in FY 2018 causing a share price collapse. Customer concentration then fell to a low of 26% in FY 2020. BUT, in H1 it was up to 31.3%. So I asked the question about customer concentration. Several interesting things here:

1) Hannah didn't read my question out fully, skipping the point about it going up in H1, but focusing on it falling previously. Is this a sore subject?

2) Andrew looked slightly uncomfortable when answering.

3) Despite much talking around it, it became evident that they expect Amazon to be in the top 2 at the full-year. And of course, Amazon in the top 2 is not because B&M or Action have fallen back significantly - both are doing well overall.

So we now have implied 40%+ revenue coming from the top 3 customers. This is not good. Still, this is in the category of things that will be fine until they're not.FY 2021 and FY 2022 look to be fantastic and any "accident" won't come until later.

Supermarkets will have done very well over the period compared to Action which has suffered various full or partial closures, some ongoing, but this is temporary. I think it will be the likes of Aldi and Lidl which really result in diversification. Relationship there is still at an early stage.

In summary: The only immediate issue I have with UPGS is valuation. Here you need to do your own model and come up with your own numbers (but not 6% revenue growth!). It is quite possible to justify 200p, but there is no getting away from the fact they are far more expensive than they were in March 2020. And of course, it is also a matter of weighting. 15x say 15p EPS = 225p, which is above the current price but isn't the sort of upside that makes me go all-in.

Camelia (CAM.L) - Final Results

Camelia is a weird beast. It is a hybrid agricultural, engineering, food services & investment company. They used to also be a bank, although I think that was divested. Results are largely flat, which could be considered reasonable results in the circumstances:

The outlook is pretty cautious, though:

At this stage, whilst there are signs of the world returning closer to normality with the roll out of vaccines, we do not believe that normal trading conditions will emerge until 2022, and certain businesses will continue to feel the effect of the pandemic for some time thereafter.

We remain financially strong, with significant net cash, and have the resources to withstand a further period of disruption. The demand for our agricultural produce will remain and we are managing the business in a manner which we believe will ensure our future prosperity, whilst taking the necessary steps to manage our costs in the short term.

So not recovery in their markets until 2022 and still actively managing costs down.

So much is going on in the different businesses with different commodity prices, weather patterns etc. that it is almost impossible to analyse. However, one thing does stand out – at 7000p (a share price that itself tells of a management that doesn’t follow market norms) this is on a P/TBV of 0.49. Unusual, in the current market, for a company that is both profitable and dividend-paying.

This isn’t immediately a value-trap, in that the Tangible Book Value isn’t in free-fall, unlike something like Simigon that we looked at the other day. There may be hidden value too:

Investment Portfolio. The Group has a portfolio, principally of listed investments, the strategy for which remains to invest in high quality companies where we believe that there is long-term value. This portfolio also enables us to balance our geographic risk exposure.

Investment Property. The strategy is to continue to invest in quality assets where an appropriate yield may be realised. The process of developing some of our existing properties to enhance yield will continue.

Collections. The Group has collections of art, philately and manuscripts which are regularly reviewed and are added to or sold as appropriate.

The ‘collections’ are ‘heritage assets’ of £9.8m, but that alone tells you how quirky this company is.:

Heritage assets comprise the Group's and Company's investment in fine art, philately, documents and manuscripts. The market value of these collections is expected to be in excess of book value.

The dividend of 144p represents a 2.1% yield so this is nothing to write home about.

In summary, I think there is value here, but unless you can analyse the trading to predict when earnings growth may come, or they intend to return much higher levels of cash to shareholders via dividends, the quirkiness means that this is low down my list of things to buy.

Smiths News (SNWS.L) - Interim Results

The background is this newspaper distributor bought a parcel company called Tuffnells to diversify away from its declining core business and rebranded as Connect. This subsequently lost them a lot of money so they sold it off and then rebranded back to Smiths News. A new management team are making a go of the original business, which was always something of a cash cow.

The Stockopedia StockReport has plenty of green:

Todays HY results show the same gradual decline:

With cashflow only down slightly, which is good:

Net debt reducing, on the surface, seems good, but it is merely a reduction in lease liabilities and this is purely from the sale of Tuffnels. The only major changes that could affect lease accounting are the assets and liabilities held for sale in the prior year. So realistically bank debt has not reduced in this period.

They run with negative working capital too, and negative equity, which adds to the risk here. This means that the balance sheet is still poor even excluding longer-term liabilities, which they refinanced recently:

A new three-year £120 million facility was agreed in November 2020, comprising a £45m amortising term loan (Facility A), a £35m bullet repayment term loan (Facility B) and a £40 million multicurrency revolving credit facility (RCF). The agreement is with a syndicate of banks comprising existing lenders HSBC, Barclays, Santander, AIB and Clydesdale and one new lender, Shawbrook Bank. The final maturity date of the new facility is 6 November 2023.

So financing runs out in 2023, but as they also have £15m due in 12-24 months. And Shawbrook Bank isn’t a mainstream lender but…

…offers loans to small and medium-sized businesses which are unable to obtain finance from the main commercial banks. (from Wikipedia, my emphasis.)

With £100m market cap and annualising the FCF then you have about 20xEV/FCF. Which doesn’t sound crazy, until you consider that cash flow here is likely to decline over the long term, and the balance sheet is very weak.

But perhaps more importantly this compares badly to Reach Plc that we calculated was on around 11x EV/FCF. Smiths News faces the same declines since it is in the same industry but without the potential for digital growth (not that we are that convinced Reach can be a major player here, or that its free cash flow doesn’t decline at a rate that makes the current share price overvalued.)

In the outlook Smiths say:

Trading for the year to date is in line with the Board's expectations and on track to meet the market's expectations for the full year. Subject to current performance being maintained, the Board expects to reintroduce the payment of dividends later in H2 FY2021.

Surely they would be daft to pay dividends with that balance sheet? Either they are very confident or very foolhardy. And given the history, I'm not willing to bet that it is the former!

Small Caps Live Friday 7th May

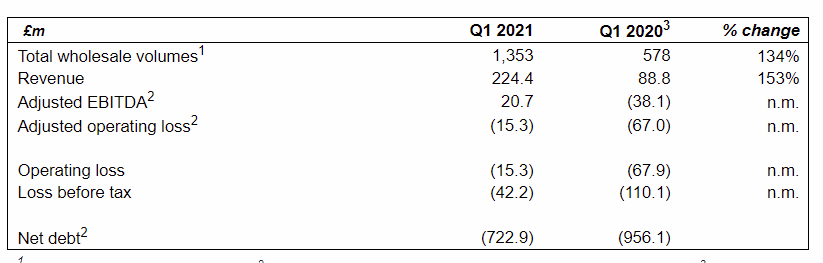

Aston Martin (AML.L) - Q1 Results

Aston Martin has been a financial disaster ever since 1913, going bankrupt or otherwise requiring financial rescue around 12 times (so far). Were it not for a loyal fan base, including Ian Flemming, the brand would surely have disappeared decades ago.

In 2018 they had been profitable for a whole 18 months (and three years on an adjusted EBITDA basis!) and other marginal manufacturers such as Jaguar Landrover were also making good profits, though premium saloons were rapidly falling out of fashion. Very wisely the owners decided to cash in much of their holding with an IPO and somehow got away with leaving it loaded with debt:

The thing that still strikes me in these figures is the level of debt given the levels of investment facing them over the next few years: They are beyond late to the gas-guzzling SUV party, yet the competition has already moved on to electric cars.

Their guidance is unchanged, though they note a heavy Q4 weighting. They don’t guide real profitability, only EBITDA, which for any car manufacturer in the current environment is ridiculous, let alone one so underinvested and indebted. They do however provide the figures to approximate cash flow and profitability and they seem to suggest they will be both profitable and cash-flow positive this year. Brokers estimates are however for losses in both FY 2021 and FY 2022.

It seems pretty clear cut to me that this company has no value.

Numis (NUM.L) - Half-Year Results

Clearly, these H1 figures are strong, e.g. revenue ahead 83%. We already knew their business was strong in the first quarter both due to high market activity and because they guided “growth of more than 75%” on the 30th March. It is good to see that profitability is ahead commensurately rather than most of the money going to staff as was apparently the case at Cenkos. But they imply they need to increase compensation going forward:

Attracting and developing talent will, as always, remain a priority for us as we continue to target long term strategic growth opportunities including the international expansion of our Capital Markets business.

It is the pipeline I’m most interested in after a very busy quarter. Unfortunately, this is all they have to say:

Whilst in the current environment there remains some short-term uncertainty, the business has great momentum, and the pipeline is strong. Execution of our Capital Markets pipeline will be influenced by equity market conditions but the outlook for the second half is encouraging.

The share price was strong first thing but has since fallen back, perhaps reflecting concerns that this strength of performance won’t be maintained indefinitely.

Somero (SOM.L) - Trading Statement

Somero brought out an unscheduled trading statement yesterday, which started:

The Board is pleased to report that as a result of stronger than anticipated trading momentum in the US in the first four months of the year alongside signs of improving activity levels in Europe and Australia, it now expects to exceed previous guidance for FY 2021 established in the 10 March 2021 final FY 2020 results statement.

The Company's previous guidance for FY 2021 indicated revenues were expected to grow in the single mid-digit percentage range from the US$ 88.6m reported for FY 2020, adjusted EBITDA would grow modestly from the US$ 26.1m reported for FY 2020 and ending net cash would approximate US$ 27.4m.

When we looked at the results in scl-2021-03-10, the price was weak on the day and we commented that:

Mid-single-digit revenue growth may not impress some people. particularly given that this would be weaker than 20H2. Say 7% revenue growth on $89m for 2020 = c$95m = $47.5m per half <$53m 20H2 revenue.

Saying that:

Modest EBITDA growth is understandable as they are now investing for growth - not sure I've heard them be this long-term positive before. So are they just being conservative on 2021 revenue?

This feeling was reinforced listening to their results call, which we blogged on the live-events channel, saying:

Some 20H2 was catchup but very positive outlook for 2021 - but too early in the year to say. My feeling is that we will see an upgrade here during the year.

Which turned out to be the case as the company now say:

The Board now expects FY 2021 annual revenues will approximate US$ 100.0m, adjusted EBITDA will approximate US$ 31.0m, and a consequential improvement in the anticipated year end net cash position.

This is still behind the 20H2 run rate for revenue and I think this is the earliest they have issued an ahead statement, so there could well be another upgrade.

I expect that it was not just us who were expecting the ahead statement since the share price response has been relatively muted, being up only around 10% yesterday. And the price had been falling the day before, presumably due to traders selling into perceived resistance at 450p.

Apart from profits being well ahead, some other things to note:

The high level of cash generation and free cash. Dividends have always been generous and there is every reason to expect this to continue.

The Stockopedia figures don’t seem to reflect the latest news, so here we need to turn to the finnCap brokers note. Even so, the company gave us the key figure of $31m EBITDA. This means the company is on around 10-11x EV/EBITDA. Not that cheap but not expensive, particularly since there is plenty of time for a further upgrade during the year, and growth companies are at twice that rating in the current market.

The pipeline of new products. Somero have struggled to grow over the last few years with expansion in China coming to very little, but the introduction of innovative products in existing markets seems to going better. This is how finnCap summarise it:

New products launched in 2020, such as the SRS-4, the Broom+Cure and SkyScreed 36, are expected to provide a meaningful contribution to FY21 growth. In April 2021, the company introduced another new product, the SkyStrip, designed to automate the process of stripping plywood sheets from shoring, which commonly causes injuries and lost labour time. It also continues to work on a pipeline of new products targeted to expand its addressable market and anticipates a further product launch before the end of FY21.

So, like UP Global Sourcing we have a company that is cash generative, in a secular growth market and executing very well. Unsurprisingly, just like UPGS, it is trading at record valuations. Still, most companies seem expensive at the moment and it is surely better to be positioned in quality companies like these.

So we are not tempted to take profits yet.

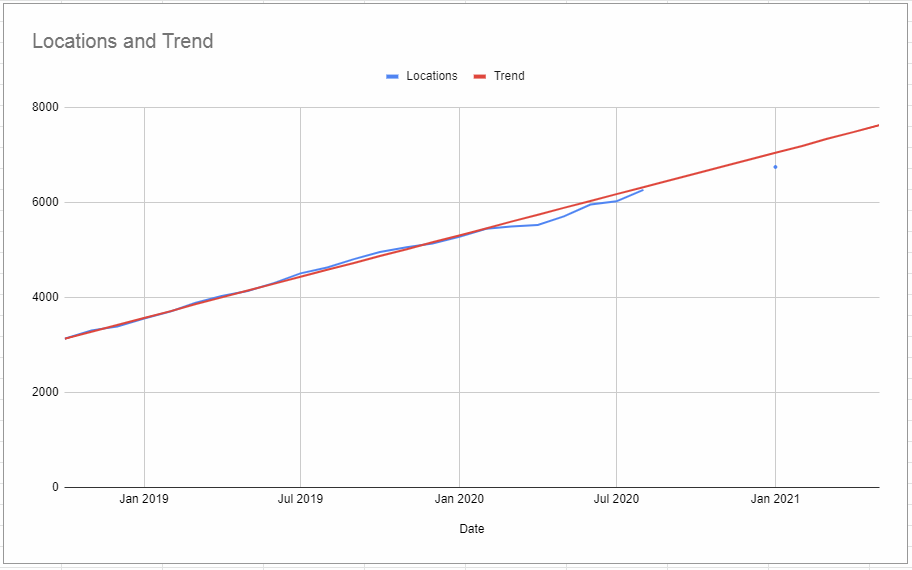

SmartSpace (SMRT.L) - Results Preview

Just a heads up that SmartSpace has results coming out on Monday and is doing some promotional activity, including at Mello Monday next week. Mark is on the bill for Monday too, talking about when to sell.

Potentially this could expose it to some new buyers, however, I don’t see the attraction here. Growth appears to be tailing off and they have a weak market position up against many stronger competitors, not to mention Google AdWords.

I found this graph I prepared when I looked at it before:

The astute amongst you will notice something about that graph: it is a linear scale. Which means they are only adding a fixed number of locations per unit time and the percentage growth is decreasing all the time.

There are no shortage of competitors in this space, and they are struggling to get in the first results on google. As I said earlier, they not only have direct competitors to content with, but google.

That’s it for this week, have a great weekend all!