Small Caps Live Weekly Summary

FCAP NTBR MWE CAPD PDG SOM LUCE BSE EVE FUL TON

There was no Large Caps Live this week.

Mark has started writing an article series for Stockopedia called Screening for Value. In it, he explains how he thinks now is a good time to look for value investments and how to use the Stockopedia tools to find potential investment candidates. All three of us are Stockopedia subscribers and value the Stockopedia StockReport as a way to quickly check out key company financials. You can get a 2-week free trial and 10% lifetime discount if you want to check it out.

Small Caps

finnCap (FCAP.L) - Final Results

These results were actually last week but were missed from the summary. We were also hoping for a management presentation to add detail, but they seem to be missing in action on this one which is disappointing.

· Revenue up 13% to £52.5m (FY21: £46.6m)

· finnCap Cavendish revenue up 101% to £24.3m (FY21: £12.1m)

· finnCap Capital Markets revenue down 18% to £28.3m (FY21: £34.5m)

· Adjusted PBT(1) of £9.3m (FY21: £9.6m); PBT of £8.1m (FY21: £8.4m)

· Adjusted EPS:(1) 4.51p (FY21: 4.80p); Basic EPS: 3.95p (FY21: 4.41p)

So adjusted EPS comes in slightly above forecasts. The adjustments are the normal sort of ones, although given that they have excluded Share-Based Payments, we think investors should be looking at fully diluted EPS here. This would be around 4.1p on an adjusted basis.

Of course, this is now looking back, and current trading is not as good:

With weak and volatile equity markets, the start to FY23 has been challenging in ECM across the market although we do continue to see good transaction levels in M&A, both plc and private, where our pipelines remain good. Inevitably these conditions will mean substantially lower results in FY23 but we remain confident that, through the teams we have developed and the client base and reputation we have established over many years, finnCap is well placed to resume growth once market conditions permit.

Cash is up to £24m, some £14m above where they say their minimum requirements are, and it is pleasing to see that they have increased the dividend. They now yield over 10%, and although they are not guaranteeing this will increase again this year, we think they’d like to at least maintain this level going forward.

Overall, these results are in line with Mark’s expectations. However, the weaker outlook was not greeted well by the market, which marked the shares down in response. This is very much a sell the rumour, sell the fact market!

In terms of outlook, they say:

Equity issuance through our Capital Markets division has been very low but we continue to execute plc M&A mandates. Sales and trading activity has remained broadly stable.

In contrast, the private M&A market and our team's M&A performance has been strong and we have closed several private M&A transactions post year end.

As we enter Q2, our public and private M&A pipeline remains good and we have seen some marginal signs of improvement in ECM activity.

There are some signs of life returning to the ECM markets this month with finnCap raising £10m for Frenkel Topping and acting as joint broker on the £25m raise for Solid State. Some strength in US tech markets this week may also help.

However, they are still highly dependent on M&A revenues, and the question remains whether the M&A strength will continue. Companies that have cash may be seeing bargains, but equally, this may simply lag the equity markets.

These headwinds mean that the share price has now dropped to the level where there is very little value being attributed to the ongoing business. This seems a little harsh given their long-term track record of growth.

Northern Bear (NTBR.L) - Preliminary Results

These read reasonably well:

· Revenue of £61.1m (2021: £49.2m)

· Adjusted operating profit* of £2.6m (2021: £1.4m)

· Adjusted basic earnings per share* of 9.8p (2021: 5.5p)

· Cash generated from operations of £2.2m (2021: £3.8m)

However, impairments and provisions have definitely taken the shine off:

· Impairment charge in relation to A1 Industrial Trucks goodwill of £2.6 million

· Legal claim against Springs Roofing settled in July 2022 for £0.6 million

These are adjusted out in the EPS figure above, but at least the impairment is non-cash, and the provision is one-off. So that seems fair, overall.

The balance sheet is looking much better than it has in the past, with £2.2m net cash at the balance sheet date and a current ratio now at 1.16. This isn't exactly bomb-proof, but given this has often traded below 1, this is an improvement. The market perhaps hasn't liked the company not declaring a final dividend, though. They seem to want to use the cash for acquisitions:

Following Board changes in late 2021, including my appointment as Non-Executive Chairman, I commenced a process of engaging with the Board and management to discuss and review the Group's strategy and approach to capital allocation. This review remains ongoing and, in recent months, we have assessed two potentially accretive acquisitions of a more substantial size than those we have made previously. Ultimately, these did not come to fruition. We continue to explore avenues for increasing shareholder value.

Not sure how much firepower they actually have for this, given that they face large working capital movements during the year. A+ for disclosure on this, tho:

As we have emphasised in previous years' results, our net cash/bank debt position represents a snapshot at a particular point in time and can move by up to £1.5 million in a matter of days, given the nature, size and variety of contracts that we work on and the related working capital balances.

The lowest position during the year was £1.6 million net bank debt, the highest was £2.5 million net cash, and the average was £0.1 million net bank debt.

We’d like to see all companies report similarly.

The outlook is a little mixed:

It has been widely publicised that industry-wide challenges continue with respect to both the availability and price inflation for construction materials. Our companies have strong and well-established customer and supplier relationships and have been able, on the whole, to work with both groups to ensure continuity of supply for contracts and to pass on cost increases where possible.

The following suggests that they will perhaps report lower EPS this year:

However, we have seen some impact on our results and expect this situation could provide a short-term headwind to operations until industry supply and demand revert to more typical levels.

Once cost inflation works through the system, they should be in a better place:

Our forward order book remains strong and should support our trading performance in the coming months, subject to potential supply chain challenges and the business-specific considerations noted in the trading statement above.

There are no forecasts in the market, and even the company say they find it hard to predict the FY result. However, if you look through any short-term headwinds to typical long-term profitability, this looks pretty cheap...assuming you trust management will add rather than destroy shareholder value with their new acquisition strategy.

MTI Wireless (MWE.L) - Significant Contract Win

The company announced what they term a “significant” contract win today:

…its Distribution & Professional Consulting Services division has won a three year contract (with an option to extend for a further four years) with the Israeli Ministry of Defence ("MOD"), which is expected to be worth US$1.4 million per annum or US$10 million over seven years.

However, they only own 51% of the subsidiary that won the order:

This contract was won by P.S.K. WIND Technologies Ltd ("PSK"). The MOD is a returning customer for PSK, a company that the Group acquired 51% of in January 2022.

And it seems like it may not actually be new business:

...with this contract being a continuation of the same services.

Even if it was new, 51% of $1.4m only represents 1.5% of forecast revenue - so I think their definition of "significant" differs from ours. The bigger problem was that this company has looked expensive for a while on fairly mediocre growth forecasts. Historically, this has traded at a discount to the market, reflecting its high-risk areas of operation. The valuation anomaly has become even worse recently since the general market for small caps has fallen significantly, as MWE hasn't really sold off.

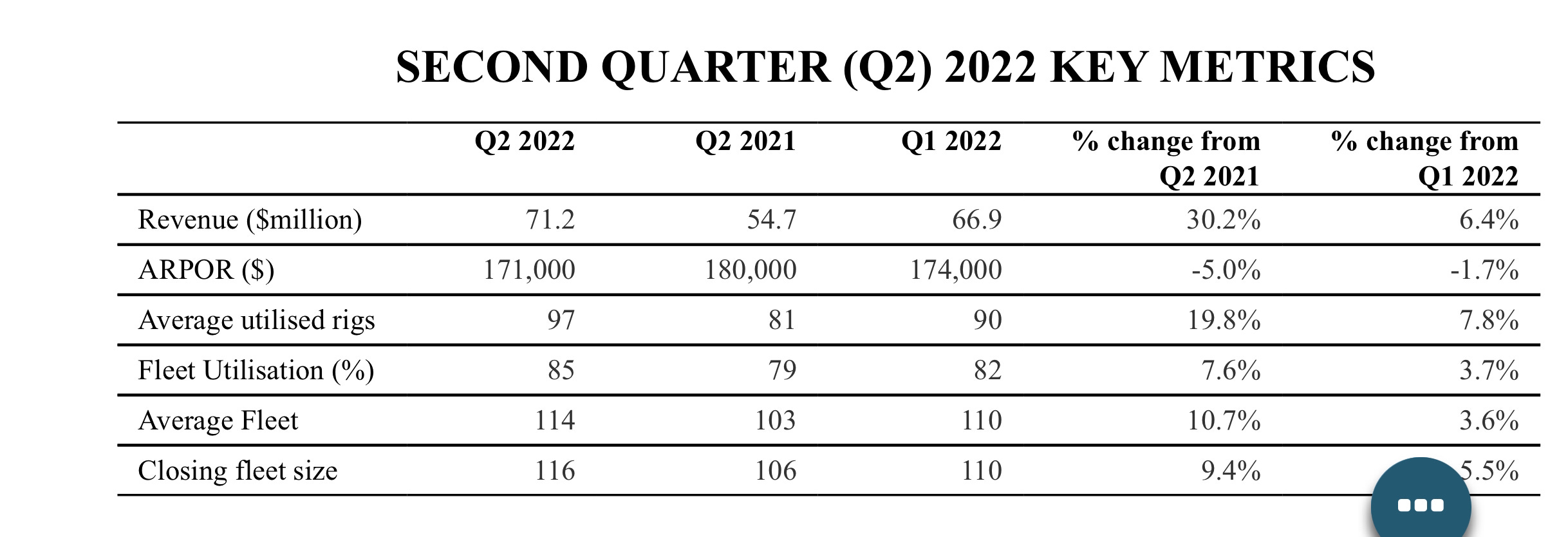

Capital Limited (CAPD.L) - Q2 2022 Trading Update

Here are the Q2 headlines:

The number of rigs utilised is quite a bit higher than Mark expected at 97 vs 92. 85% utilisation is about the maximum they can achieve while still moving rigs between contracts and maintaining the fleet.

The average revenue per operating rig is a little bit lower again in Q2. The drop here in Q1 led some to question why, so seeing it drop further may worry some, particularly when we know the market is tight. However, there are some reasons why ARPOR is lower:

A higher proportion of underground rigs. About 20% of the fleet is now underground rigs, which command lower rates. However, the EBITDA margins are similar. Given that underground rigs are cheaper to purchase, the return on capital on the underground fleet may actually be higher.

Rates are not the biggest driver of ARPOR. Factors such as how long a contract has been operated (and therefore operations have been optimised) and whether they can operate double vs single shifts matter more. Rates themselves are being priced at around 15% higher than the same time last year.

The other bad news was the value of the listed investments has suffered due to the weak equity markets:

The portfolio recorded investment losses (unrealised) of US$10.3 million. The total value of investments (listed and unlisted) was US$47.3 million as of 30 June 2021, versus US$60.2 million at the end of 2021;

However, this loss is lower than a simple mark-to-market would suggest, showing some outperformance from trading these. And they’ve taken cash out, which is good to see:

…the portfolio generating net sales after investments of US2.6million, with the proceeds directed toward group capital expenditures.

They also highlight some of the previously announced recent positive news that has been separately announced:

First contract with B2Gold Corporation at the Fekola Gold mine in Mali, one of largest gold mines in Africa: Capital has been awarded a reverse circulation drilling services contract.

They now have a toehold into the first and second largest gold mines in Africa and will be seeking to expand their presence in these.

MSALABS recently announced an expansion of its global partnership with Chrysos, now guiding to deploying 21 Chrysos PhotonAssay units by 2025;

The growth here is phenomenal, as are the potential margins and low-capex required to expand. Interestingly, they say MSALABS starting to drive work to the drilling side, not just the other way round. It shows that it is starting to be a strong business in its own right.

Announcing these updates separately and the tone of the trading statement suggests that the management are getting increasingly frustrated at the lack of market reaction:

Capital Drilling: Strongest demand environment since the company's inception…

Capital Mining continues to perform strongly…

Q2 2022 has again seen extremely strong demand with the outlook remaining supportive;….

Tendering activity across all business units remains robust, with a number of opportunities progressing;…

We are currently seeing the strongest demand since the Company's inception, in contrast to the recent perception from global equity markets.

Our hope is they turn this weakness into an opportunity with a large buyback announcement to coincide with the results.

The guided revenue range is reiterated. However, the strength of trading in Q2 and the continued buoyancy of the end markets confirmed this week means that this looks even better value at 90p than it was a couple of weeks ago when it was trading in the mid-70s.

Pendragon (PDG.L) - Post-close Trading Update

We expect to report Group underlying profit before tax of c.£33m for the first-half of FY22 (H1 FY21: £35.1m).

2021 was a time of exceptional profits, and in January, nobody was expecting 2022 to be anywhere close. But here we are six months in, only 6% behind. And that's despite the withdrawal of government covid support. As we have seen elsewhere, both new and used margins remain very strong, compensating for lower than normal volumes. The company claim operational improvements, but all the franchise dealerships are in the same very strong situation.

Trading conditions 20 days ago (the end of the period they are updating for) were already well established, so what is most important here is the outlook:

We are pleased with the strong start to FY22 and remain confident we have the right strategy in place. We are mindful of the challenges to both new and used vehicle supply which are expected to continue for at least the remainder of the current financial year. Softening consumer sentiment also has the potential to impact on demand in the second half. However, we believe our market-leading proposition and mix of business models means we remain resilient in the face of these challenges and we continue to expect to deliver group underlying profit before tax in line with Board expectations.

Breaking that down, we have two things:

1) New and used car supply expected to continue - this is a positive

2) Softening consumer sentiment - this would be a negative, but they make it clear it is not happening yet, being only "potential".

Ultimately though, as elsewhere, there is no upgrade:

we continue to expect to deliver group underlying profit before tax in line with Board expectations

We continue to believe that the whole sector is performing ahead of current expectations and that the priority in setting guidance is not to miss should the overheating economy suffer a violent slowdown, rather than providing a central estimate of the most likely outcome. In our view, the risk to new car sales in 2022 is very limited because of the size of the order book and pent-up demand from customers not willing to commit themselves to a major purchase they won't even receive for several months.

focus has continued to be on ... strengthening the already robust order bank.

We think that means the order book rose further over the period. However, all the retailers are very coy over the exact levels, which we suspect is because customers can walk away from their deposits. Loss aversion means we suspect they'll only do so if forced to, e.g. by unemployment. High margin aftersales has a recurring element to it, making it relatively secure. In H1, it was up YoY, which is a good start, albeit aided by a lack of lockdowns. Used car sales and margins remain the most likely cause of motor retailers failing to beat expectations. If prices fell, this would severely dent margins pushing that part of the operation into a loss after fixed costs.

Somero (SOM.L) - Trading Update

Theoretically, an inline trading statement should be treated as a positive by the market given the 35% fall in the share price since January. However, Somero has never been highly rated by the market and, for them, was looking a little expensive in January. Arguably the rating has merely normalised. But we think this actually looks like a delayed "ahead" statement:

Driven by positive momentum from a highly active US non-residential construction market, healthy market conditions and elevated activity levels in the European and Australian markets, Group trading in H1 2022 ended higher than the comparable H1 2021 period.

Forecasts are for +4.5% YoY over the full year, so you'd expect that, but the commentary suggests it is more than 4.5% ahead. And there are some reasons to think H2 will be stronger:

While H1 2022 trading in Europe was down compared to H1 2021, due largely to logistics challenges that delayed machine shipments, based on the H1 2022 momentum and activity levels alongside anticipated catch-up on shipment delays to start H2 2022, second half 2022 trading is anticipated to accelerate, and Europe is anticipated to contribute to full-year 2022 growth.

We have previously reported that we believed that component supply chain issues meant that they were not able to make sufficient machines to meet strong demand and that they had prioritised shipments to the US over Europe in Q1. Competitors (yes, there are several!) were selling machines as quickly as they arrived in the UK. And unlike in the US, where Amazon's new tenders were starting to slow, the UK was still strong. So, we believe them when they say H2 should be strong in Europe.

While cognizant of the uncertain macro economic environment, the Board continues to anticipate healthy trading to continue in H2 2022, a view underpinned by direct feedback from customers in the US, Europe & Australian indicating high workloads and extended project backlogs. As such, the Board is pleased to confirm 2022 results are anticipated to fall in line with market expectations for revenues of approximately US$ 138.8m, EBITDA of approximately US$ 47.7m, and year-end cash of approximately US$ 39.9m.

The last direct guidance from the company was in the annual results:

with the investments for future growth being made, 2022 EBITDA is expected to be comparable to 2021

2021 adjusted EBITDA was $47.8m. Of course, $47.7m is worth much more in pounds than it was in January, and with significant sales to Europe will be harder to achieve. So you could argue that by not taking a currency hit on sales in the weak Euro and Sterling, this is already ahead. This update may also be a trigger for EPS forecasts to be reappraised in Sterling terms. by investors.

However, it is important to remember that visibility is not as good as it might appear. They are very dependent on boom screed sales in the US. And while they say “project backlogs that extend well into 2023”, capital purchasing decisions made by customers will be strongly influenced by the tendering market for late 2023-4. Any weakness would dent customers’ confidence and likely cause a delay in capital purchases at least until the extent of the downturn was clear. This could happen at any moment without notice.

Despite these factors, the 6% or so rise on the day seemed quite miserly. Things picked up on Wednesday following a Questor tip that caused a further double-digit rise. Normally we would be sellers into a tip-based rise since these tend to be the least-informed investors. However, it is hard to sell such a high-quality company on such a low rating, which it remains on even after this week’s rise.

Luceco (LUCE.L) - H1 Trading Statement

Starting with the word "broadly" is not going to endear them to anyone:

The Group has traded broadly as expected since our last update at the end of Q1. We expect to report revenue of c.£106m (H1 2021: £108.2m) and Adjusted Operating Profit of c.£11.5m (H1 2021: £19.2m) for H1 2022. This follows record results in 2021 and a particularly strong H1 2021 performance.

And indeed, the share price opened down 10% on the open. However, it is good of them to be able to put numbers to this, particularly operating profit so soon after quarter end.

On a like-for-like basis, we expect first half revenue to be 17% lower than H1 2021, but 13% ahead of the Group's H1 2019 pre-COVID performance.

We’re not expecting H2 to be any better on revenue. However, there are encouraging signs on the gross margin:

We expect to report H1 Adjusted Gross Margin of 34%. This is slightly lower than H2 2021's performance of 36% due to customer destocking causing a reduction in higher margin Wiring Accessories sales.

And interesting signs that cost inflation for them may be peaking:

Input cost inflation remains well controlled, with associated selling price increases fully implemented during Q2. The run rate for gross margin at the end of the first half was approximately 36.5%. We continue to expect second half margin to reach approximately 37% as we benefit from recent cost deflation, particularly in sea container rates.

The outlook is weak:

Consumer spending on home improvement continues to slow as disposable incomes reduce in the face of rising inflation.

A continued slowdown in consumer demand at rates similar to that experienced to date, combined with broadly stable professional demand, would leave 2022 Adjusted Operating Profit at the bottom end of current analyst expectations. The final outcome will largely depend upon how consumers and our distributor customers react to macroeconomic developments in the second half of the financial year.

But perhaps in a sign that the market is finally pricing these sort of things in and maybe even over-reacting, the share price subsequently bounced to finish roughly flat and gained further on Wednesday.

The net debt is worth keeping an eye on, though. They say this is within their target range:

We expect to report net debt equal to 1.4x (31 December 2021: 0.7x) LTM Adjusted EBITDA at 30 June 2022 on a pre-IFRS 16 basis and pro-forma for acquisitions, in the middle of our target leverage range. We expect net debt to reduce in the second half as inventory levels adjust to normalising supply chain conditions and lower activity levels.

And assuming this does work its way lower during the year, this is nothing to worry about. However, we always prefer companies that have net cash, not debt.

Base Resources (BSE.L) - Q4 Operating Report

This is the best ever quarter for Base:

Record sales revenue of US$91.3 million supported a record revenue to cost of sales ratio of 3.5:1.

Driven by reasonable production and very strong pricing:

These would have been even better if they had had those unexpected flash floods. Although this is a quarterly ops update, they do give costs per tonne and selling prices which means we can estimate most of the financials:

As you can see, the operating cash flow is prodigious. Unfortunately, this isn't reflected in the cash balance:

As at 30 June 2022, the Company had net cash of US$55.4

At the end of March, they had $36.7m cash so this has only increased by $18.7m. They do say that working capital has increased since they had large shipments in June:

The Company achieved record sales revenue of US$91.3 million in the quarter, with US$51.8 million occurring in June, leading to an increase in receivables of US$26.2 million over the quarter.

This means $44.5m FCF before changes in Working Capital. So pretty impressive. Going forward, we get FY23 production guidance:

So down a bit on this year - mainly due to lower grade when they move to the North Dune later in the year.

In terms of pricing, Ilmenite is forecast to be flat going forward due to the uncertain global economic outlook. On rutile, they say:

Rutile prices increased again through the quarter with further price gains likely in the September quarter.

And Zircon is expected to

…ease slightly in the September quarter in response to market concerns from Chinese customers.

The bigger challenge is that their current resources run out in 18 months’ time, and the Toliara project is still stalled. Only Tanzania seems keen to allow them to find new resources:

The Company continued on-ground exploration in Tanzania. Following analysis of samples from the shallow auger drilling, test pits and rock chip sampling, a follow-up 3,000m air-core drilling program is planned to commence during the September quarter. Subject to the successful outcome of this program, a further 10,000m infill drill program is planned.

Although, surely Kenya must see the risk that its lack of permitting will cause. Base is the biggest employer in Kwale County and one of the biggest exporters in Kenya. Any gap in production at Kwale is not great news for Base but is likely to be much worse news for Kenya.

Eve Sleep (EVE.L) - Trading Update

This is not a good start:

Sales orders for the Group decreased by 19% year-on-year in H1, with Group revenue declining 17% year-on-year for the half.

Although recent trends are better:

There are some signs of recovery in recent months with June sales orders for the Group declining just 1% year-on-year, an improving trend that has continued into July.

It seems that, just as we said years ago, there are just too many competitors in this market to be profitable:

the recent increase in industry wide promotional activity has continued to negatively impact eve’s gross margin

How is their balance sheet:

As at the end of June, eve’s cash position stood at £1.5m

in addition the Company had drawn working capital facilities of £0.9m

That’s a strange phrasing. Net cash is £0.6m if we manage to interpret that correctly. In comparison, at the end of 2021, they had net cash of £4.5m.

Management will continue to focus on maximizing the business’ cash runway.

Brace brace brace! As we’ve commented before, they'd quite fancy raising some more cash and are a bit miffed nobody will give them any. So they put themselves up for sale instead:

leading to the Board receiving a number of indicative expressions of interest

But most of them were apparently chancers:

with a small number currently being facilitated in their due diligence and with further information requests

Surely they need to hurry up and get an offer in place soon or they risk running out of cash?

Fulham Shore (FUL.L) - Final Results

The financials here are relatively complex as there are lots of new openings and it is very hard to impossible to work out LFL profitability. Not even LFL revenue is given and even if it was maturation times and cannibalisation would make it of questionable value. EBITDA is a good measure of achievable short-term cashflow in an emergency, but excludes depreciation / maintenance capex necessary to sustain the business in the medium term. Operating profit is highly dependent on accounting assumptions.

Never the less. Leo likes a challenge:

Headline operating profit of £9.0m (2021: loss of £2.2m)

Profit is gooood.

Impairment charge on property, plant and equipment of £0.6m (2021: £1.0m)

Some sites will work better than others and which sites work may change over time. So I actually find it reassuring that they recognise this.

The Group incurred one off costs in the year of £0.6m (2021: £1.0m) from impairment charges for one restaurant (2021: 5) which was previously impacted by COVID-19 during the year and has not recovered at the same rate as other Group restaurants since the return to normal trading.

With our new openings, we have invested £0.7m (2021: £0.2m) in pre-opening costs.

Amortisation of the Franco Manca brand at £0.8m rounds off the major adjustments they made to get that headline £9.0m figure from an operating profit of £6.7m. Finance costs then reduce the PBT to £3.9m on which they had to pay tax, I assume for the first time.

Franco Manca is a strong brand and stronger for every restaurant opened. Therefore I think it is right to adjust out the brand amortisation. Pre-opening costs are more a matter of judgement. Impairment charges are likely in future, but probably at a lower rate than on average recently.

So Leo’s crudely adjusted-profit after tax would be £3.7m + £0.7m (pre-opening) + £0.8m (amortisation) + £0.1m (excess provisions over expected normal) = £5.3m or 0.8p EPS, a P/E of 15x. In normal market conditions I don't think that would be outrageous. Interestingly, Stockopedia as EPS of 0.2p forecast for this year whereas the accounting figure is 0.6p and their headline 0.9p. So this looks like a massive beat. Now more than ever the current trading and outlook is critical.

Current trading and outlook:

As at 20 July 2022, the Group operated 89 restaurants. We aim to have around 100 locations by the spring of 2023, including the 18 new sites we plan to open in the current financial year to March 2023.

In the three months since the beginning of our current financial year, we have continued to trade well at Headline EBITDA level, in line with management expectations.

Broker, Singer, have updated. Clearly from the above, the inaccuracy of the EPS forecasts and Singer's comments, EBITDA is what they focus on internally.

FY22 finals are 5% ahead at the adj. EBITDA level

Interestingly they get an adjusted FD EPS figure of 0.4p from today's results. They forecast accounting profits (which include pre-opening costs remember) to be flat in 2023 but EBITDA to rise significantly. There is no model.

As a self-funding rollout operating at the budget pricing but with a mid-market to premium product, and ongoing cheap lease opportunities offsetting costs elsewhere, these look interesting. It still looks a little expensive in today's market, but could attract investor's imaginations.

Titon Holdings (TON.L) - Trading Update

Profit warning from this ventilation supplier to the building industry:

As a result of these items our results for the FY21/22 financial year will be lower than our prior expectations.

These items are the usual - delays in passing on input cost increases. They do say that their 49% Korean subsidiary is performing ahead of expectations but this is still only just profitable. They also reinforce why we think that the scariest acronym for small cap investors is "ERP":

Our trading has also been affected by unforeseen operational impacts associated with the implementation of the new internal ERP system for the UK and European operations. This new ERP system represents a key business improvement needed as part of our growth strategy, but the initial implementation led to short-term production and despatch delays which resulted in lower than expected revenues for the last three months of trading.

Not good.

This is their third profit warning if I remember correctly, and I'm really surprised they hadn't fallen further in response to the previous ones - after initial falls the share price bounced back. They mention their balance sheet strength that may be providing some kind of floor:

The Group has consistently maintained a strong financial position with an on-going focus on working capital management and various cost efficiency initiatives. At 30 June 2022, the Group had cash balances of approximately £3.0m and no indebtedness.

However cash was £3.7m at 31st March and £4.2m at 31st January, so how long this can provide support looks quite limited.

That’s it for this week. Enjoy the sunny weekend.