Small Caps Live Weekly Summary

Investor Meet Up, Black Friday, FDEV UNG CLX INCE DX. APP SCS

SCL Investor Meet Up

A reminder to get your registration in for our SCL investor meet up on the afternoon of the 1st December. It has been a while since investors have been able to get together physically, swap ideas and make new connections. The event will be designed to facilitate this plus there will be a few brief talks providing investment ideas or educational content. The event will be held in the centre of England, in Coventry, which has great transport links and is less than an hour from London by train.

The event is free, but places are limited so do sign up as soon as possible here.

Black Friday

This week has also been characterised by Black Friday sales with the FTSE opening down 3% on Friday and oil down 5%. Only gold has been a bright spot up about 1%. The worry, of course, is that the newly discovered coronavirus variant will lead to a new round of lockdowns.

While the response to the increased risks is logical, the moves in small caps are often far from logical. At this end of the market, moves are largely liquidity-driven, so even companies that may benefit from the changing economic conditions can sell off brutally. These are rarely times to panic sell, not least because in response to the lack of liquidity the market spread often widens significantly. However, big moves do have the ability to cause investors to act irrationally, either panicking and selling unnecessarily or acting like a rabbit in the headlights and holding when the outlook for a company really has changed for the worst. Although we don’t know the short-term trajectory of the stock market better than anyone else, this is a time to double-check your actions and make sure they are driven by a rational assessment of the situation, not a knee-jerk reaction to seeing losses appear in your portfolio.

Large Caps Live Monday 23rd November

Frontier Development (FDEV.L) - Trading Update

This has fallen about 1/3 today following a cut in revenue guidance and hence profits. The top-line guidance has been cut from £140M to £115M ie about £25M. This is a high gross margin business, c.60%, and with high operational leverage so a fall of £25M in revenue means a fall of £15M or so in operating profit which therefore cuts the fiscal year 2022 (to March 2022) operating profit from around £30M to £15M.

That is clearly painful but as always one has to dig in to work out what is going on.

(1) Jurassic World Evolution 2 was launched recently. They have gone for a higher price point (£49.99 on Steam) vs the original JWE (which was around £39.99 or £29.99 IIRC). (For convenience I will refer to the original game as JWE and the new one as JWE2)

JWE sold about 1M units in five weeks. It was launched on 12 June 2018. (The film Jurassic World: Fallen Kingdom was released on 21 May 2018 with full US release on 22 June 2018). JWE2 was launched on 9 Nov 2021 and has so far sold 0.5M units (noting the higher price point). About half the guidance cut is due to the company cutting its estimates for JWE2 as a result. They did mention that JWE 2.0 is in about 400k wish lists on Steam according to data they have seen. The next Jurassic World film, Jurassic World: Dominion was rescheduled due to Covid and is due to release on 10 June 2022.

I think there are a couple of things that people are missing here in baby throwing with bathwater:

(a) We are only 2 weeks into JWE2

(b) Black Friday / CyberMonday is next week.

(c) Ahead of a major film launch there is usually a big Christmas film splash so I expect Jurassic films on Christmas TV schedules.

(d) The company will have a lot of Jurassic uplift in fiscal 2023.

(2) The other half of the 'miss' was due to weakness in Elite Dangerous: Odyssey (ED:O) and Foundry. We knew it had a poor launch - a lot was due to hardware incompatibility issues and frankly, it felt a bit rushed to get it to launch during Covid. The main point to make about ED:O is that the reviews are improving and that sales are / will be picking up.

(3) Re Foundry - they had pencilled in 3 games at £5M revenue each. Lemnis Gate is probably going to be low single-digit millions. To be fair to the company this is a game that was always experimental and they had said that. Am not entirely sure that their guidance reflected that though. I get the impression that they are more positive on the next 2 foundry games.

So putting all that together my conclusions are:

(a) I am not entirely sure we are at the bottom but it certainly feels a lot like they have cut everything and it was clear that they hope / expect upside to the revised guidance.

(b) I am not entirely sure I care what happens in the rest of 2022 as what really matters is 2023.

(c) In some ways the key thing that struck me was a comment that the original Elite Dangerous was 8 years as a franchise before ED:O came along. As for JWE it looks like they have cycled it on 3 years due to the film tie ins (obviously Covid has screwed that up). But they were clear that they have a product roadmap all the way to coincide with the film launch.

So what I am thinking is (a) the franchise for Elite is not dead (b) on an 8+ year journey for ED:O is this an interesting place to buy (c) and similar arguments for JWE / JWE 2.0 etc.

Incidentally, on Jurassic World etc - the Dominion film will be the last in the current batch of 3 films but there have been strong suggestions that there will be further films in the franchise.

I think that the key thing to observe is that the Foundry business will grow slower than people initially thought but is reliable and will continue. I think it will surprise over time. I also think that one has to consider if it is a franchise - I think the criticism/reviews of users suggest that it has 2 - 3 strong franchises (RollerCoaster Tycoon anyone? ) And anyone acquiring the company would consider that they could cut 30 - 40% (say) of costs due to using a 3rd party engine and investing less in the games. So I think profits in someone else’s ownership would be significantly higher.

Small Caps

Universe Group (UNG.L) - Takeover offer

12 pence in cash…

· 163 per cent. to the volume weighted average price per Universe Share of 4.56 pence for the three - month period ending on 22 November 2021 (being the last Business Day prior to the Announcement Date ).

We always said that Universe Group looked out of place as a separately listed company and would be better off as part of a larger group. This week they got a takeover offer. And with a very good premium. It goes to show what can happen if a company has good products & contracts and a tight shareholder base.

With Harwood, Downing and Ennismore supporting it, this looks like a done deal:

IISL has therefore received irrevocable undertakings and a letter of intent in respect of a total of 138,658,662 Universe Shares representing, in aggregate, approximately 51.20 per cent. of Universe's issued ordinary share capital on 22 November 2021

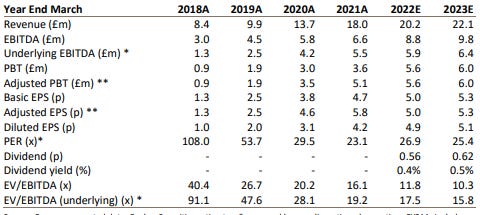

Calnex (CLX.L) - Half Year Results

These are a fairly new float so the figures are compared to pre-IPO. Revenue is up 19.8% However, underlying EBITDA is down 4.4% and Adjusted profit is flat at £2.308m. They say

The results for the first half of FY22 are materially ahead of the Board's expectations at the start of the year, as indicated in the Company's Trading Update issued in October 2021...

However, flat earnings isn't a great look for a supposed growth company. This was looking like another optimistic Cenkos float, similar to HeiQ, however, management appears to have steered this away from the rocks at the last minute.

Net cash was up significantly, but this was mainly IPO proceeds, not internal cash flows:

The Group generated £0.9m cash in H1 FY22 (H1 FY21: £0.9m)

On the outlook they say:

The Board is confident in meeting the upgraded** market forecasts for the year

So turning to the Cenkos note:

We see they have 5p of adjusted EPS in for FY22. So they will do c3p EPS in H2. This is the upgraded forecast!

They have 2023 estimates of 5.3p EPS. With only 6% earnings growth forecast, a normal valuation would be 10-12x P/E max. And only since it has high gross margins and a nice niche to operate in. Poorer quality companies would probably be rated more lowly.

So the fair valuation on these forecasts is probably around 60p, which coincidentally is where Cenkos floated this last year. The company do have a habit of beating forecasts, at least. However, you could argue that this beat is already in the price - those paying 125p/share, are paying a high price for a future that doesn't appear in either the results or forecasts, which is often unwise. Cenkos, of course, have to retain their Buy rating, but cunningly haven't provided a fair value estimate or price target, which potentially indicates how much faith you should put in that.

INCE (INCE.L) - Cancelled listing?

You may recall that Arden Partners recently recommended an all-share offer from Ince, partly because Ince shares are much more liquid than Arden's.

Unfortunately, Ince shares were then suspended as Arden was their NOMAD and had to resign. That's about as illiquid is you can get. Ince investor relations blamed this on bad advice from the LSE, but said they knew they'd have to change NOMAD and signing up a replacement was already in progress. However, as of the time of writing, they still have no NOMAD.

With the clock ticking, there is further bad news this week:

The AIM Rules for Nominated Advisers require the Company, as the new controller of Arden, to satisfy the eligibility criteria for a Nominated Adviser in its own right as set out under those rules. Accordingly, there can be no guarantee that the application for such a change of control, when made, will succeed.

If the change of control application is not successful, the Company would be likely to seek the permission of the Takeover Panel to invoke the Condition.

Should the offer complete in circumstances where the change of control application is not successful, then Arden would cease to be a Nominated Adviser.

All of this raises big questions about the investabilty of either company at the moment.

DX. Group - Update on Publication of Annual Report

This rather tame RNS title caused a 40% drop in the share price on Thursday.

The Company is not in a position to publish its Annual Report ahead of the Annual General Meeting ("AGM"), which is taking place later today. The Company's Audit & Risk Committee has recently raised a corporate governance inquiry relating to an internal investigation commenced during the financial year ended 3 July 2021.

So not great, however, the knock-on impact is even worse:

The inquiry has yet to be concluded, and the process will delay the completion of the audit, but will be expedited as quickly as possible. However, it is not anticipated that the Audit & Risk Committee and the Company's Auditors will conclude their work before 2 January 2022, being the date that is six months from the end of the financial period ending 3 July 2021. If, as currently expected, the Annual Report is not published by 2 January 2022, trading in the Company's ordinary shares will be suspended in accordance with AIM Rule 19 on 4 January 2022, being the first business day following 2 January 2022. Suspension from trading will be lifted with the publication of the Annual Report.

So flagging that their shares will be suspended on 4th Jan. Normally a 40% share price fall that is not related to poor trading would be worth considering. Accounting issues aren't great, but the market often fears the worst and the reality isn't always as bad. The market hates uncertainty and illiquidity and you can often get paid well for bearing these risks.

However, accounting issues AND a weak balance sheet is a potential recipe for disaster. Since one exasperates the other and confidence is removed, something that is necessary to raise additional funds in the market. This is what happened to North Midland Construction recently, and while the same outcome here is unlikely, the current ratio of 0.76 doesn’t leave a lot of margin if things are worse than expected.

Appreciate (APP.L) - Half Year Results

Billings up 19.6% to 118.2m (H1 FY2021: 98.8m), broadly similar to H1 FY2020 (£120.2m), the last period of normal trading prior to the pandemic

Seems OK.

Revenue increased 49.6% to 41.0m (H1 FY2021: 27.4m) benefiting from redemptions, which had been deferred as a result of lockdowns, being realised as anticipated. Revenue was 23.5% higher than the pre-pandemic period (H1 FY2020: £33.2m)

Understanding this company is complicated by a difference between billings and revenue that isn’t clear on the first reading. Referring to the annual report, it looks like vouchers accepted by more than one retailer don't have pass-through revenue recognised as revenue, only the margin. Whereas vouchers for a single third-party retailer recognise pass-through revenue as revenue.

This doesn't help. We either want to know total revenue including all pass through, or revenue without the pass-through, not some strange mixture. So investors should side with them on this opinion:

Billings is an alternative performance measure, which the directors believe provides a more meaningful measure of the level of activity of the Group than revenue

But this is annoying. It is nice to have total billings because this is a guide to potential future real revenue. But what we want is the real revenue earned in the period, i.e. the sum of all the margins taken on the redemptions.

Significant reduction in pre-tax loss to 2.0m (H1 FY2021: 6.2m loss) (H1 FY2020: £1.3m loss)

We prefer companies that make a consistent profit. But this is a highly seasonal business:

Appreciate Group's highly seasonal business typically sees a loss in the first half of the financial year.

Traditionally this was due to their Christmas Hamper business, and presumably, this continues because they only recognise much of their revenue when vouchers are spent and people send more at Christmas. But a £2m loss during a period of bounceback doesn't seem to compare well to £1.3m in the 6m to 30th Sept 2019.

Cash balances, including cash held in trust, at 30 September 2021, were 207.1m (H1 FY2021: 227.3m)

Again, that doesn't sound like a terribly useful metric, but being down isn't going to be good.

Free cash lower at £2.9m (H1 FY2021: 24.9m) - this is typically the low point in our cash cycle and also reflected growth in regulatory billings (which require customer monies to be held in trust until redemption)

That sounds terrible! Certainly, a valid reason for some people to sell. But note they don't say "a low point" or "near the low point". They have literally said "the low point". So as long as cash flow is positive over the next 12 months they'll be OK.

Given the uncertainties, you’d want to check the going concern statement!

The Group has prepared three forecast scenarios (low, medium and high billings volume) for the next year and applied five plausible downside scenarios to the 'low' forecast. The forecasts take account of the transfer to free cash of £11m which was previously held as ring fenced funds (see note 5). In all scenarios the Group maintains positive free cash and does not utilize the agreed RCF during the period to 31 March 2023.

See discord for a full analysis, but it looks like they are good for the next 12 months, and indeed in a far better position than they were in March. Recovered billings bodes well for the future, but there's no obvious growth there.

The outlook doesn’t contain any significant catchup though:

The Group has seen the usual seasonal increase in demand for its products in its key Q3 trading period to date, with a good pipeline of business; and the Love2shop marketing campaign, which is now underway, expected to support activity levels

However, these are currently below levels seen in FY2021 and FY2022 due largely to our decision not to supply low margin business to a direct competitor. Billings for Q3 so far would be 3.2% ahead for Q3 FY2021, and 2.0% below Q3 FY2020 on a like-for-like basis.

So actually underlying growth is negative. However, given their customer deposits, if interest rates rise by 1% the pre-tax profits will rise by £2m. That's pretty significant on a £42m market cap.

Liberum put out a note yesterday. Apparently "H1 was better than expected", but trading is volatile and much rests on December. EPS is forecast to grow strongly, from 3p for FY 22 to 4.6p for 2024. They have a 31st March year-end and so these dates are closer than they appear. The dividend was raised 50% at the interim and 2.29p/share is forecast for FY 2023.

This could be a good play on rising rates.

SCS (SCS.L) - Trading Update

The headline is:

Year to date performance ahead on two year like-for-likes

The trouble is that this is not a completely fair comparison because:

a) the start of the period was the tail end of post-lockdown catchup (last 7 weeks of the prior period as up 24% on normal and first 9 weeks of the current period was up 12%)

b) Christmas delivery sales were pulled forward due to shipping delays and manufacturing backing up.

Next, they say:

Total two-year like-for-like order growth of 0.9% for the 16 weeks ending 20 November 2021, with a one-year like-for-like order reduction of 10.6% following an unprecedented period of pent-up demand at the beginning of the prior year.

That's not super-easy to parse, but basically, they're saying to use the +0.9% figure and not the -10.6% figure. And they're right, subject to the caveats above.

As previously reported, the Group had a strong start to the year, resulting in two year like-for-like order intake growth for the first nine weeks. However, over the last seven weeks, the Group has seen a reduction in store footfall and conversion with consumers spending less on big ticket discretionary purchases. This appears to be driven by a change in behaviour with consumers shopping earlier for Christmas when compared with previous years.

This is as Leo had identified from the TrustPilot data, and from monitoring the availability of Christmas delivery on their website and comparing with (admittedly secondary) sources of data on previous years.

The extended product lead times currently being experienced across the furniture and wider retail industry are also having an impact on current purchasing trends.

This is more concerning. Prior to this, there was no evidence of people being put off ordering by the delays. Indeed, they were keen to get in the queue whether it be for sofas or cars. One factor here is whether competitors can get the goods sooner. In the case of Christmas delivery, this was clearly not the case for DFS, despite some level of vertical integration there. But "build to order" is just one model in sofa retail. It is a very attractive one for the retailer due to the negative working capital requirements, and also attractive to the customer as it offers lower prices and a greater choice. But it is not the only one.

At 20 November 2021, the Group's order book was £131.9m, £71.5m above the same point two years ago.

This sounds like great news for future revenues but is actually bad news. At the time of the full-year trading update (and presumably repeated later), they said:

At 31 July 2021, the Group's order book was £103.5m

So the order book has risen by £28.4m. This is revenue they have not booked during the period. OK, so you'd expect the order book to drift upwards at this time of year. I estimate that in the calendar year 2019 it rose from £42.9m to around £56m. But I don't think you can say there was a lump of delivery by Christmas orders this time and not last time around. I'd expect this to be in both figures.

Instead, it is likely that there are ongoing serious issues in getting sofas into people's houses.

Our online business, which is a key part of our ongoing strategy for growth, continues to perform well, with two-year like-for-like order growth for the first 16 weeks of the year of 38.5%.At the current rate they'll end up with a large order book at the end of the year too and will significantly miss revenue and profit forecasts.

This is good assuming these are sales of the standard range and not online specials at very low cost or ex-warehouse.

The Group is now preparing for the winter sales trading period, and whilst it remains difficult to predict shopping habits and consumer engagement, the business is planning to approach this key period in a manner consistent with that which has proven successful in previous years.

i.e. the Boxing Day sale will be critical. They go on to say:

We continue to work closely with our existing suppliers to mitigate current supply chain challenges. To broaden our customer proposition, we have recently partnered with new UK suppliers so that we can offer furniture on shorter lead times.

The question is whether they are ahead of or behind the curve on this. Quite possibly it is harder (at least politically / psychotically) for vertically integrated DFS to take on new suppliers.

The risk is that they are now going to miss revenue forecasts this year. Margins could be up, but given the lack of guidance, it is a fair assumption that they'll miss on profits also. So you can see why these sold off this morning in response to this trading statement. Although, in this case, much of the fall was due to market conditions, stop losses potentially being hit, and the price has now recovered from this morning’s lows.

As we have said in the past, there is a lot of uncertainty, particularly with margins, but the size of the backlog would lead to better performance for FY 2023. Broker Shore Capital say:

After a stellar period of trading through the various stages of Covid 19 restrictions, and easings, ScS has reported a step-back in trading momentum in recent weeks. We await to see if the slower trading is temporary, reflective of a change in Christmas shopping patterns, or of a more permanent basis.

We leave forecasts unchanged, looking for CPTP of £13.7m and EPS of 26.5p (both IFRS 16 compliant

That's based on revenues of £373m which looks high after today’s update and there is a high risk of a significant downgrade coming down the line. However, given that some of this would shift into the following year, it is unclear what effect this would have on the already bombed-out share price.

As such the stock trades on an undemanding EV/EBITDA multiple of 4x for FY22 and 3.4x for FY23, forecast to yield >5% in both years.

So it is very cheap and the dividend is safe since cash flow will likely be fantastic with all those deposits. The next thing to watch is:

a) The magnitude of the dip in review ratings around Christmas when deliveries are missed. This happens to a certain extent each year.

b) Volumes of sales reviews in the Boxing Day sales. But, again, marketing costs are significant. They should probably be considered by investors as a cost of sale (albeit a particularly variable one) and have already been incurred for that massive order book without benefitting the profit yet.

The risk is that a big cut in EPS forecasts is not in the share price, even if balanced by a rise next year.

That’s all for this week, have a great weekend, and don’t forget to sign up for the SCL Investor Meet Up happening next week!