Small Caps Live Weekly Summary

GSK MRW SOM K3C KINO CORA HUM MPAC NTQ Investor Favs

Large Caps Live Monday 5th July

One topic worth touching on is activism and takeovers. Recently:

Morrisons had what looked like an agreed bid from Fortress (controlled by SoftBank) over the weekend and now it looks like Apollo is counterbidding

Elliott wrote a letter to GSK

In both cases, the issue is really that of hidden value. In the case of Morrisons, it is clear what are the properties worth. But I also think that there is a realisation that the mainstream UK supermarkets are able to hold their own vs the Germans. But have a look at this graph from Kantar:

You can see that over the last 8 years or so Aldi and Lidl have gained share - mainly at the expense of the UK big four. But if we look at the impact of Covid so compare to Jan 2020 for instance the changes have not been that dramatic:

The key point for private equity is that even if a supermarket loses 1- 2% market share per year, price inflation probably keeps the top line stable. Then add in sale and leaseback and you probably are buying the supermarket for almost free; so you end up with a free option for the future and you pressurise management to generate cash even if it means reduced maintenance CAPEX.

The interesting aspect of this goes back to the discussion earlier on lifetime values. Tesco, and to some extent Sainsbury’s have used the footfall they have to expand their product offering to eg financial services or department stores (eg clothes, BBQs etc) and now, with Sainsbury’s to Argos and Habitat. In the past, Tesco tried to expand to restaurants with Giraffe.

I think that there is a significant opportunity still for all four big boys in this area - eg Asda and Morrisons have hardly touched financial services or other areas. My expectation is that the non-food side of Asda (eg George) might be subleased or sold to a third party - or at least the amount of floor space dedicated to the non-food will be sweated/questioned.

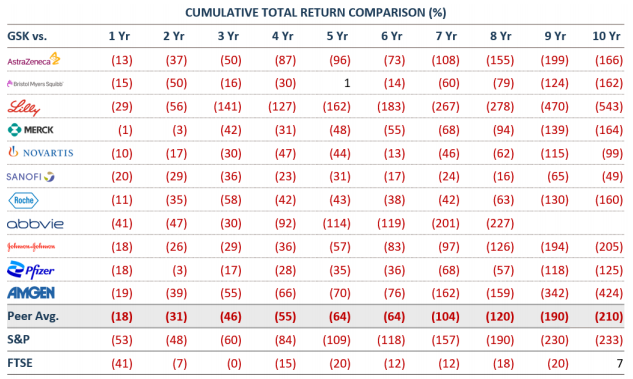

In terms of GSK, I think that the Elliott letter is very good at highlighting some of the issues re growth, respect for management and over the distribution of a dividend.

I think that the following table is really telling:

I think the way to interpret it is that AstraZeneca has outperformed GSK by 166% over 10 years (rather than GSK has underperformed by 166%). The curse that GSK has in vaccines is that they work but it is deadly boring and watching paint dry business - or it was until Covid. And then the failure of GSK to come up with a vaccine blew the management credibility.

I think that a number of UK companies could be described the same way - an obsession with maintaining a dividend at all costs meant that boards cut on CAPEX or R&D and destroyed long term value (which kinda gets us back to P.E ownership of supermarkets). I thought the above table was brilliant as it basically said to GSK board that it is not just us, but the entire investment community, that thinks your management team is crap.

As an aside, not many people know that the cash flow from the Beatles allowed EMI to fund its Central Research Labs which invented the CT and the MRI scanner. However, the board/chairman did not really understand the potential, and at the first issue, they basically jumped ship giving the entire market to the USA (GE), Holland (Phillips), Germany (Siemens) and Japan (Toshiba).

Just think about it a UK company invented the CT and the MRI scanner using profits from the Beatles but then did not see it through. I am sure that at the time they were facing shareholder pressure to 'optimise the balance sheet', 'maintain the dividend' and not invest in loss-making projects. In fact, there is more to the story - CRL was taken private in a buyout; refloated as Scipher in 2000 and promptly went bust in 2002 or so. Again financial engineering and asset stripping.

That I think is quite a salutatory lesson when considering GSK or indeed Morrisons. So as a short term investor I think I will make money on Morrisons but longer term I am wondering if I will get better value out of Siansbury’s or Tesco.

And for GSK - it is going through a split into two companies. Combined with an activist who does not take prisoners and is clearly trying to impose a new board and management; plus a decade of underperformance and I think that GSK becomes interesting.

Small Caps Live Wednesday 7th July

Somero (SOM.L) - Trading Update

When we last looked at Somero following an unscheduled trading statement on 6th May, we commented on the accelerating pipeline of new products and that it didn't seem a good time to take profits here.

Given that trading statement, Somero didn't give a formal AGM Trading Update on the 15th of June, but those of us who joined the AGM Q&A knew that they were still trading well.

Somero's H1 update doesn't normally come out for another week. On Monday the company was happily using their buyback authority to purchase shares at 460p, whereas yesterday they were absent from the market. So presumably, something changed when they completed month-end-close for June, or maybe updated their internal sales forecast, which led to today's trading statement:

The Board is pleased to report that due to stronger than anticipated trading in the US to end H1 2021 and with this momentum carrying over to begin H2 2021, it now expects to exceed previous guidance for FY 2021 established in the 6 May 2021 trading update.

Go Somero!

The company's previous FY 2021 guidance indicated revenues were expected to approximate US$ 100.0m, adjusted EBITDA would approximate US$ 31.0m and net cash would improve consequentially from the original US$ 27.4m target established in our 10 March 2021 final FY 2020 results statement. The Board now expects FY 2021 annual revenues will approximate US$ 110.0m, adjusted EBITDA will approximate US$ 35.0m, and year end net cash is expected to exceed US$ 33.0m.

As usual, it is the US that has outperformed, with Europe and Australia in line, and China presumably not material enough to mention. They admit some catch-up, but the medium-term outlook still remains strong:

Higher than anticipated momentum is carrying over to begin H2 2021, with customer workloads at high levels and project backlogs extending into 2022....particularly good performance in the boomed screed category, driven by the demand for new warehousing required to keep pace with growth in e-commerce operations.

Our view continues to be that, in order to scale quickly, competent online operations would have taken on a number of sub-optimal warehouses and will now be moving to cut costs by switching to a smaller number of larger, modern, more efficient ones. The company currently seems to be in the sweet spot of a long-term megatrend towards larger, super-flat floored e-commerce warehouses, accelerated by covid and pumped up further by catch-up work. They have also accelerated the rate of new product development (or at least, the rate at which they talk about it), adding another dimension to growth.

They command a price premium through superior support and service, vital for small-medium contractors, where a problem while concrete is setting would be a disaster. This is a particular advantage in the US due to the structure of the market and the overwhelming scale they have there.

The normal demand cycle may have been exaggerated by covid, but the warehouse megatrend seems set to continue, and concrete laying remains labour intensive, which should provide lots of opportunity for further product development, especially if recent wage trends continue. There is also potential for increased demand in residential and infrastructure, both of which appear to have a backlog of renewals in the US.

The risk has to be from competitors, and we can see two ways they could enter the core US market:

a) Increased use of larger concrete-laying contractors would mean a greater focus on the cost of machinery (rather than the red-neck "Get it done. Get a Somero" mentality), giving an ability to provide support and spares in-house, dissolving their main competitive advantage.

b) Leap-frogging of technology by competitors. For example, a survey of Somero's contractor customers is likely to indicate about as much demand for self-driving fully-automated machines as there was for the iPhone when development started in 2004/5.

Back to the present, the most impressive thing in Somero's update is once again their cash flow, and while the upgrades keep coming, today's price looks positively cheap. New forecasts from finnCap have adjusted EPS of 45.4c for FY 2021 and 48.7c for FY 2022 and dividends of 29.8c and 32.4c, respectively. Digging into it a little bit further, finnCap say:

This results in an upgrade of forecasts, bringing our adjusted PBT up from $29.6m to $33.6m, and EPS up from 39.9ȼ, to 45.4ȼ, a rise of 13.6%. Our year-end net cash increases by $2.1m to $33.0m. On the back of the higher cash position, our total dividend forecast increases from 27.9ȼ to 29.8ȼ.

In light of this, the current 10% rise in price that google finance shows looks a little miserly, given that it comes off a weak day for the shares yesterday. Perhaps a few investors expected a further upgrade though and some of this was already in the price. On valuation finnCap say:

The shares have been strong performers over the past year, but remain attractive at these levels, continuing to trade at a discount to their peer group averages. On the back of the upgrade to forecasts, we similarly raise our price target from 520p to 590p, continuing to value the group on a FY22 P/E of 16.8x and EV/EBITDA of 11.5x. With today’s positive trading update, we see renewed opportunity for the share price to appreciate, highlighting also its continuing cash flow and dividend yield attractions.

Largely backing up our thoughts. What is also striking is that finnCap have only $1.5m of capex forecast for 2021. This means that the vast majority of their product development has been expensed, and continues to be so. This perhaps flatters ROCE in periods when they are not investing heavily in new products. However, this is a period where they are investing in growth and finnCap are forecast a pre-tax ROCE of over 50% for 2021. Which is, frankly, amazing.

Given the momentum here, and the ability for multiple new products to gain traction, there is scope for both further upgrades during the year, and positive multi-year trends. It was a bit of a mystery why this was available to buy in the 460s after this trading statement.

K3 Capital Group (K3C.L) – Acquisition and Placing

We mentioned K3 Capital last week as the sort of highly-rated business advisory group that is perhaps where finnCap are heading. Interestingly, finnCap are actually their Nomad and are acting as joint bookrunner on today’s announcement of a placing to fund an acquisition:

Acquisitions highlights

• KCFG is a specialist M&A advisory firm within the telecoms and technology sectors with consistent growth of revenue and EBITDA over recent years.

o For the financial year ended 31 March 2021, KCFG generated revenue of £1.71 million and normalised* EBITDA of £0.78 million, representing an EBITDA margin of c.45%.

· Consideration of up to £8.6 million, comprising

Although much of the consideration is deferred, this does show the value of having highly valued paper to do these sorts of deals. K3C are raising more than the acquisition value, and a fair amount is paid in shares. Presumably, because what you are buying with this sort of deal is customer relationships and networks, and these largely sit in the people not the firm.

In this case, I don’t have any great insight into whether this specific acquisition is a good deal or not for K3 Capital. I am more interested to note that finnCap, together with Cannacord, are getting this placing away at a very small premium to the closing mid-market price.

As we have said on scl before, although the market for bailing out badly run, heavily indebted companies with fresh equity has undoubtedly soured. But the market for small placings for strategic purposes is very much open, and this deal provides a nice start to Q2 for finnCap.

Kinovo (KINO.L) – Final Results

One could be forgiven for thinking that Kinovo is a listed German cinema chain. However, it turns out that it is just the renamed Bilby. Kinovo appears to be as random a name as Bilby in describing their activities which are now given as:

a specialist property services Group that delivers compliance and sustainability solutions

Their activities havn’’t changed with the name change though, so this really just means that they provide gas and electricity fitters.

I first started looking at Bilby in 2019. At this point, this was a buy and build that had gone seriously wrong. They ended up with a couple of loss-making contracts that were in dispute. They terminated the contracts and initiated formal resolution proceedings to try to recover the money they say they were owed.

The rest of the business seemed to be trading ok though, and in March 2019, they guided that they would still be generating £2-3m EBITDA, which compared to the then market cap of c.£12m seemed reasonably cheap, particularly if EBITDA & earnings were to recover.

The balance sheet put me off investing, though, as net debt increased and their current ratio dropped below 1. And it was a good thing it did, as they subsequently were forced to raise money at 11p, a roughly 50% discount to where they were trading at the time.

The 2020 results were a better year, but then along came COVID, and the price briefly touched as low as 8p in April 2020. Like many small caps, the price then recovered rapidly to over 40p as the market priced in a rapid recovery. This brings us to yesterday's results to 31st March 2021:

· Operating profit of £601,000 (2020: £2.3 million) on revenues of £60.2 million (2020: £65.4 million).

· Adjusted EBITDA of £3.0 million (2020: £4.7 million).

So, on the surface, they appear to be very much back to where they were in 2019, although now with a £21m market cap at 35p due to the dilution. Cash flow is much better, and now net debt seems under control:

· Strong adjusted operating cash flow of £4.7 million (2020: £4.6 million).

· Net debt3 reduced by £4.5 million to £2.7 million (2020: £7.2 million).

But this is largely driven by amortisation of customer relationships, and working capital movements. The former they like to exclude as non-underlying, and the latter is not really repeatable. The current ratio of 1.27, while not necessarily indicating distress as it did in 2019, doesn't give much room for further working capital improvements.

The outlook is positive, as you would expect for most companies at this stage of the cycle:

Despite the continued repercussions resulting from the pandemic, the business has had a positive start to the year. In the three months to 30 June 2021 our performance has been in line with management expectations. We remain cautiously optimistic in our outlook as the Covid-19 restrictions unwind and the new normality for society returns.

As a consequence of some of the delays and disruption referred to above, particularly with regard to planned or discretionary work, we anticipate pent-up demand for our services and a strong pipeline of work to follow.

But there are a couple of additional headwinds:

Gross profit of £12.9 million (2020: £16.6 million) was achieved at a margin of 21.4% (2020: 25.4%).

There doesn't seem to be any explanation of why gross margin has dropped so much or if it can be expected to rebound. And…

Underlying administrative expenses of £10.1 million were down £2.2 million compared with the prior period (2020: £12.3 million) reflecting the restructuring of the business and Coronavirus Job Retention grants received.

So admin costs should go back up in 2021. It is hard to work out the potential effect of this, and there are no forecasts on Koyfin or Stockopedia, so investors are largely flying blind here. A dividend reinstatement shows some level of confidence in the future, but then they paid a dividend shortly before their emergency fund-raise in 2019, so perhaps we shouldn't read too much into this!

In summary, this is a relatively low-quality business, facing headwinds on costs and margins, whose buy and build strategy seems to have largely failed and was trading at c9x adjusted EV/EBITDA when it was at 40p+ vs a more normal range of 4-5x.

It is not surprising that the share price has been weak following these results as the market seems to have got well ahead of itself in pricing in the recovery here.

Cora Gold (CORA.L) – Drilling Results

In more news that I tend to follow for their business links rather than the company themselves, Cora Gold are up 43% today on the following drill results. The price rise no doubt helped by the title of the RNS:

World Class Intersection at Sanankoro with 19m @ 31.56 g/t Au from 65m at Zone A

And that this is a £20m (now c£30m) market cap company.

The company doing the majority of the drilling is, of course, Capital Ltd. and Cora are highly complementary about their efforts:

Once again I would like to thank our team and contractors who are delivering this programme on the ground over a very long field season. The quality and efficiency of their work has been extremely impressive, and I am very pleased that the results are matching their efforts!

Capital had a holding in Cora, although they went below the 3% threshold last year so may have sold out by now. However, these drill results are highly positive for both Capital, where I expect we will see win further drilling contracts with Cora over time, and Cora’s broker finnCap, who should find any subsequent equity raise much easier. So although I don’t hold Cora directly, I am pleased with the reaction to these drill results.

In terms of the drill results themselves, I am a little underwhelmed. 30g/t+ over 20m is good but it's not bonanza grades or anything. Cora gold is of course a spin-off from Hummingbird, who didn't have the resources to exploit the Sanankoro licenses at the time. Hummingbird still held 10% of Cora until a few weeks ago when they sold out. Bad timing on that one!

Hummingbird (HUM.L) - Drilling Results

However, Humminbird release their own drill results from Yanfolila today. Also likely to have been conducted by Capital Ltd.

These results included 9m at 26g/t at 100m depth. Clearly not as good as 19m at 33g/t, but this appears to have caused barely a ripple, with the price up just 6% for Hummingbird.

Of course, this shows what a difference scale makes with Hummingbird an £80m market cap. Plus perhaps the market's views on the quality of management. Hummingbird has a producing mine, however vs Cora's mere development opportunity.

The market often prefers to travel than arrive. But to my relatively untrained eye, I would be a seller of Cora and a buyer of Hummingbird given the disparity in their share price reactions this morning. And, of course, all of this activity bode well for the Capital Ltd trading statement due next week.

Small Caps Live Friday 9th July

MPAC (MPAC.L) – Trading Update

MPAC is a company that is highly reliant on capital sales, including for the very subdued non-covid healthcare sector, while progress in maintenance revenues was stopped dead by covid. In the event, trading also turned out to be highly resilient, e.g. in the January trading update:

The Board is pleased to announce that the Group expects to report underlying profit before tax for the full year 2020 above market expectations, primarily as a result of better than expected margins in Q4 driven by sector mix. Trading continues to be resilient, as Mpac serves essential healthcare, food, and beverage markets, deploying digital technology to mitigate travel restrictions despite the continued headwinds from the pandemic.

In September, they made a significant acquisition from their excess cash. While inevitably earnings-enhancing, we saw risks, but trading so far has exceeded expectations. Resilience has now turned outright strength with yesterday's update:

We are pleased to report that the strong momentum in the second half of 2020 has continued into the first half of 2021. Order intake in H1 2021 across all regions was significantly above the COVID-impacted H1 prior year, with the Americas region, underpinned by our previous investment in Switchback and an expanded commercial footprint, performing particularly well. Consequently, our order book going into the second half of 2021 is above the opening order book of £55.5m, providing enhanced coverage over H2 forecast revenue. The Board is therefore comfortable with current full year market expectations.

It sounds like management is now more comfortable with expectations than when they were first issued. Breaking this down:

We are pleased to report that the strong momentum in the second half of 2020 has continued into the first half of 2021.

Traditionally the split has been close to 50-50 H1 / H2. The mild H2 bias seen in 2017 and 2018 probably due to ongoing growth rather than anything else. H1 2019 proved to be exceptional, with £40m of underlying revenue (that is, excluding the Lambert acquisition) well above any period before or after - therefore the H1 bias that year was atypical. H1 2020 was, of course, heavily impacted by covid compared to H2 and so the H2 bias that year was again atypical. So, with H1 2021 now completed, we understand that underlying revenue was similar to H2 2020.

With the Switchback acquisition contributing less than three months and £3.8m of revenue in H2 and continuing to grow, the run rate throughout H1 is likely to have been ahead of the annualised £14.2m reported for 2019 at the time of the acquisition. Conservatively, assuming the same underlying revenue in 21H1 as 20H2, there could be £51.3m of revenue alone in H1. We will know for sure in early September.

our order book going into the second half of 2021 is above the opening order book of £55.5m

So, logically, H2 should be stronger than H1.

While travel restrictions, particularly in EMEA and APAC, continue to present challenges to new business development and to machine installations, the impact is largely mitigated through both the ingenuity of our employees and the use of digital technology to provide our customers with the highest standards of customer service. Despite the delta wave throughout the world, travel restrictions in H2 are likely to be significantly less than they were in H1, providing a further tailwind. While, of course, we don't have a sector breakdown for 21H1, Healthcare revenues were badly hit in both halves of 2020 and should have further to recover.

Add to this the underlying growth of the business and Shore's forecasts of £95m revenue for the full year seems very conservative. Added to this, they should have £9-10m of net cash which could be used for further earnings enhancing acquisitions (albeit with attendant risks).

Downsides?

Revenues are mostly capital sales and therefore very lumpy. As mentioned above, it would have been very wrong to extrapolate H1 2019's performance into H2 or beyond. But although there is a degree of catchup in H1's performance, and the forecast figures do not look exceptional on an ex-acquisitions basis.

Amortisation of acquired intangibles are excluded from adjusted figures, but the company is becoming a serial acquirer. If you are not confident that these intangibles are maintaining their value then you might want to add the amortisation back into your profit figure.

The elephant in the room is, however, the pension deficit, which is currently trying to hide behind the sofa.

The company engaged in an asset and liability swap that removed the IFRS19 liability from the balance sheet, and actually now shows this as a surplus. However, this change didn’t remove the scheme deficit (which was some £40m when they last included it in one of their presentations) or the requirement to make deficit recovery payments for at least the next 6 years of £3m a year. £0.3m of pension admin costs are also excluded from adjusted figures. These real cash outflows, which are not accruing to shareholders, of £3.3m pa. This is material to a company that did £6.3m adjusted profit after tax last year.

Here’s what those cash outflows do when we add them back in to create a “shareholders profit” figure from the Equity Development forecasts:

So if you trust the forecasts then adjusting for the deficit recovery payments, and adjusting for net cash, then Mpac is on around 27x adjusted PAT. Not exactly cheap given the rather lacklustre growth forecasts from Equity Development. Bear in mind there are acquisitions in these figures too and while they are driving increased forecast sales, increased operating expenses are keeping forecast profits largely flat for 2021.

On the other hand, if the company can start to beat their forecasts then the recovery payments will become less material. Plus most investors in the current market don’t read the cash flow statement so probably will focus on the headline EPS, and with the chance of an earnings upgrade within 2 months then this may not matter to short-term investor returns.

Howard Marks says that the key to long-term success as an investor is to be a second-level thinker. However, in the short term, and particularly in the current small-cap market, then being a first-level thinker is what is being largely rewarded. But then, maybe assuming that most Mpac investors are first-level thinkers who won’t read the cash flow statement is second-level thinking in itself?!

Investor Favourites

No place is the first-level thinking more evident than the short-term effect of tips on the market. Lots of investors want shortcuts and buying the latest newspaper tips or following a bullish commentator into their ‘top picks’ is one such shortcut. Unfortunately, few ask that if newspaper commentators are pushing something then is this really an unknown gem or that if that well-known fund manager was still buying why would they be letting private investors know on a podcast! The long term results of buying such stocks is patchy, to say the least.

It is in light of this, that I have noticed how many small-cap investor favourites are appearing in the biggest fallers list of the last 3 months:

So, perhaps we can look forward to second-level thinking making a return after all?

Have a great weekend all!