Small Caps Live Weekly Summary

Mello TIS CSC GDP JSE NXQ PMP SNX

Just our usual promo to join many of us at Mello Chiswick on Tuesday 2nd and Wednesday 3rd June, which is shaping up to be a well-attended event by both companies and SCLers. 25% discount code: SIMPSON25

Also, an early promo for The Investors’ Summit on Friday, 18th September. The set of speakers is yet to be confirmed, and it has a different flavour to Mello, more inspirational keynote speakers rather than meeting company managements and idea generation. Given that the ticket includes catering and is in a great location, many SCLers also enjoyed this event last year.

Here’s a selection of what we discussed this week. (Remember this is a summary of many opinions, and isn’t the view of any one commentator; check out the actual discussion on Discord if you want the nuance of the different opinions.) To avoid spam, the only way for new members to join the Discord server is via the Small Caps Live website. This will be instead of direct invites via Discord. All genuine investors are still very welcome to join in the discussions.

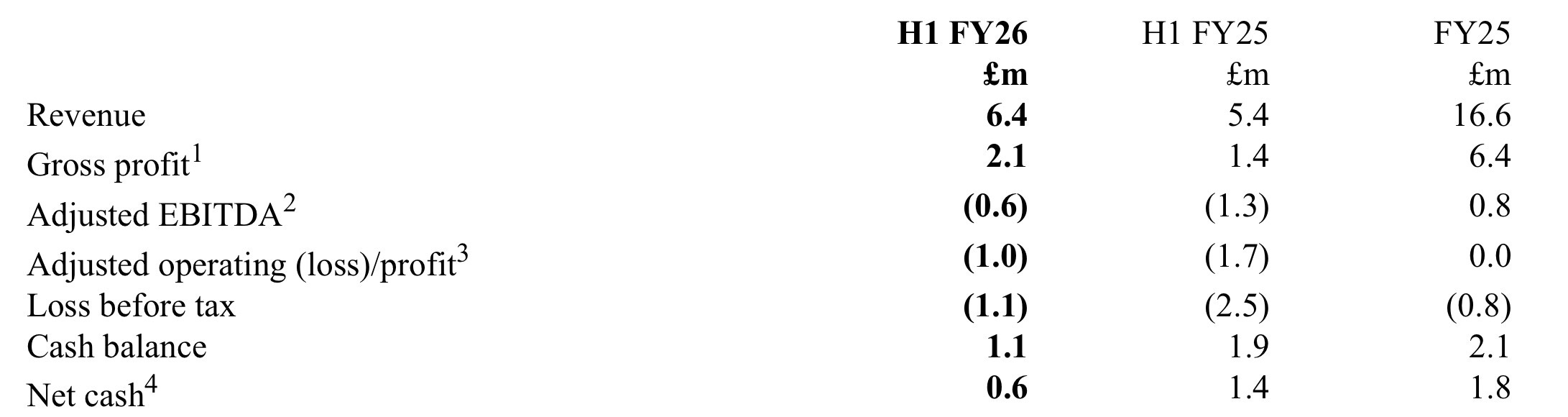

Chesterfield Special Cylinders (CSC.L) - Interim Results

On the back of the recent profits warning, we get their interim results:

The adjusted EBITDA loss and declining net cash make it look like another raise may be on the way. They claim:

Cautious cost management measures are in place to help mitigate the impact of delays, and further cost management steps are available if delays continue

But surely this is firing people, and that has an upfront cost? It’s not entirely clear that they can afford to do this, nor that they won’t bear re-hiring costs if orders do eventually arrive. Not a great place to find themselves…and this time they have little left to sell to avoid further dilution.

Goldplat (GDP.L) - Q3 Ops Update

As expected by many SCLers, but perhaps not by the market, this was a huge quarter:

The two recovery operations achieved a strong combined operating profit for the quarter of £3,855,000 (FY Q3 2025 - £694,000) (excluding listing and head office costs, finance cost and foreign exchange gains/losses).

Although the split is a little different to what we were expecting:

The Ghanaian operation achieved a profit before tax for Q3 of £806,000 (FY Q3 2025 - £784,000) which was supported by the operations team delivering to plan and higher, albeit fluctuating, gold price.

The South African operation achieved a profit before tax for Q3 of £2,624,000 (FY Q3 2025 - £(15,000)) and was supported by the operations team delivering to plan, securing once-off batches and higher albeit fluctuating gold price.

At this point, we were expecting Ghana to be recovering more strongly than it has. It seems like there is more work to do to get that back up to the c£1.5m per quarter op profit, which is probably steady-state operations:

· As communicated in Q2 announcement, GRG is in process of investing £700,000, of which £374,000 have already been incurred to improve our processes to increase recoveries and environmental management.

· The local Ghana beneficiation requirement has impacted all aspects of our business, and we continue to review, update and align our process and procedures to manage risks and maximize margins.

Slow progress on the TSF which is a bit disappointing. However, at least they are exploring other options, so they are not beholden to DRD:

We believe information gathered from this, should be sufficient to enable us enter commercial discussions with DRD Gold on utilisation of their servitudes, plant and deposition capacity. We also continue to evaluate methods through which we can process the TSF, as a start, through facilities on our premises.

Cash building nicely:

Our cash balances in the group remained strong at £5,077,000 at the end of Q3, with cash being held up in debtors in South Africa due to higher levels of supply. Cash has increased since, to £9,160,000.

£9.2m cash is over 30% of the current market cap.

They have basically delivered higher PBT in the first three quarters of the year than brokers expected them to do for the full year, an estimate that was materially upgraded just a few months ago. And there is no reason to expect Q4 to be any worse than Q3.

Mark has increased his FY estimate from 4.5p to 5.0p EPS. If one is happy to take the current £9.2m net cash, then this looks cheaper today than it did before the announcement, and it was already one of the cheapest stocks on the UK market.

The lack of share price reaction may be because the broker hasn’t updated their forecasts in response. Perhaps they feel they can’t make another material upgrade so soon after the previous one. Either way, they’ve been consistently behind the curve, and given the quarterly reporting, it’s very easy to make your own basic calculations.

Although it’s slow going on the TSF, there is reason to think the story here isn’t all about a rising gold price. Having had a presence in Brazil for a few years now, gathering mine waste and shipping it to Ghana or South Africa, they appear to be starting to do some basic processing on-site. This will be a slow ramp-up as they add plant and equipment, but it could become a material third leg of their operations over time. As we have seen with the likes of Serabi, the high gold price is likely to encourage higher gold production in Brazil, leading to a larger supply of byproducts.

Jadestone (JSE.L) - Full Year Results

High oil prices are generating very strong cash flow as expected:

Net debt at 30 April 2026 was approximately US$5 million, consisting of US$117.4 million in cash (incl. restricted cash) and US$122 million of outstanding debt on the RBL Facility. The Group’s US$30 million Working Capital Facility remains undrawn.

Stag is not coming back on stream until the end of the year to take advantage, but is fully insured for costs and lost production.

The only bad news is that CWLH may be delayed due to some sub-sea damage. Up to 8 weeks.

The hedging impact was already known and obviously annoying given what’s happened with oil prices, but the c$20m of FCF per month over the last 4 months without stag or CWLH shows the impact oil prices have on companies such as this.

Nexteq (NXQ.L) - Trading Update

A second profits warning in a row here:

As a result of the continuing uncertainty in the Quixant business, FY26 Group revenue is now expected to be approximately 15% below previous market expectations1 with a consequential impact on adjusted profit before tax.

Blamed on:

US tariffs, and directly by higher costs for critical memory and storage components (DDR4 and DDR5), which have increased our customers’ prices to end markets.

Normally, the maths would be simple: 15% of $85m forecast revenue x 33% Gross Margin = $4.2m reduction in PBT. This is actually one of the advantages of being a low-margin business. Everyone loves a high-moat business until revenue declines and profits get wiped out.

In this case, profits get wiped out anyway. With a previously $2m PBT forecast, this would be more like $2m loss without any further management actions. There is hope that they will be able to mitigate this somewhat:

More pleasingly, current gross margin % performance is expected to continue through FY26. The Board and Executive team remain strongly focussed on cost management to mitigate the impact on profitability as far as possible.

Being focused on and actually achieving are two separate things.

When the updated numbers from Cavendish finally appeared, they showed breaking even for FY 26 and a strong rebound forecast for FY27. Given recent trends, break-even this year looks a stretch, let alone a bounce back of that magnitude in FY27.

We are not sure why companies do this. The drip drip of further profits warnings caused by unrealistic assumptions is far worse than taking a one-off hit and rebuilding confidence slowly. I guess this is why they say profits warnings come in threes, and we are only two down so far.

It looks increasingly out of place to have splashed $15 million on an office in Taipei. There’s a reasonable discount to TBV now, and at least some of the remaining assets are liquid. Although perhaps a Taiwanese property fund should trade at a discount to TBV, given the geopolitical risks!

Portmeirion (PMP.L) - Statement re Government Support

As we argued previously, there would have to be some support for the sector.

The Board of Portmeirion Group PLC, the global homewares brand group, welcomes the announcement from UK Chancellor today that the UK Government will provide a £120 million fund to support the UK ceramics industry.

The obvious move to subsidise energy isn’t that important for Portmeirion, as they previously told us:

As part of our long term energy hedging process, in October 2025 we placed significant hedges for electricity at 100% of our requirements and gas at 80% at favourable rates through to 31 March 2027.

Greater certainty after March is useful, but so far, all we have from the Goveremt is hand-waving:

We look forward to finding out further details

The signalling is perhaps starting to make this look interesting. Even if the announced scheme doesn’t directly help them in the short term because of energy hedging, it would be embarrassing to announce it and have one of the most iconic companies go under.

A combined package of energy, labour, and government guarantees on loans would significantly move the risk-reward ratio here.

Synectics (SNX.L) - AGM Trading Update

This former PI favourite, now fallen on hard times, is still travelling hopefully:

first five months of the year ending 30 November 2026 (”FY 2026”) broadly in line with management expectations.

i.e., slightly below expectations.

Revenue and profitability for the full year will be weighted towards the second half of the year, consistent with the historical profile of the business1.

Subject to energy sector activity normalising through the second half, the Board currently expects trading for FY 2026 to be in line with market expectations2.

i.e., hoping an H2 recovery will save them.

The forecast numbers here were already massively cut in March.

This week’s update contains no specific order book number, which, given the only very short-term visibility over revenue, doesn’t give great confidence that they can hit even the reduced numbers. Many of us had already used this correlation to avoid the last warning:

The bounce back in the share price following the last warning looks premature, and it was no surprise to see the share price fall on this update. However, in what we can only surmise is a masochistic desire by some shareholders to be hurt again, the shares have since bounced back. Surely, at this point, it would just be cheaper to pay a dominatrix than buy Synectics shares.

That’s it for this week. Have a great sunny Bank Holiday weekend!