Small Caps Live Weekly Summary

Cryptocurrencies, WEY, PGM Miners, Gold Miners, MAST, SDI, DLAR, NMCN, GMAA, RGD, PEG, RBG, CEY, HUM

[A Discord server invite, to see all this week’s discussions, is here.]

Large Caps Live Monday 24th May

This chart is frankly stunning - it looks to me that roughly 1 Bitcoin transaction consumes as much as 1M visa transactions

So, let’s look at a study from the Cambridge Centre for Alternative Finance – the ‘Global Cryptoasset Benchmarking Study’. So how is that power generated:

Note that in Asia Pacific – which frankly mainly means China – a lot of hashers use coal-based power. A recent CNBC report (based on a paper from Nature Communications) estimated that 75% of the world’s bitcoin mining is done in China.

To be specific the idea of bitcoin / blockchain is that there is a public ledger which is cryptographically verified - the issue with that is that a distributed ledger (or database) is always going to be more power consumptive than a single instance. Also - as I keep on reminding people - the cost in transactions is not the payment - it is the fraud detection, AML, KYC, repudiation, verification, validation etc. The simple way to think about this is that (however bad the service is) if something goes wrong with a payment you can ring your bank and eventually speak to a human. With Bitcoin - who are you going to speak to?

If you look at the IEA website it appears that China consumes 6833 TWh in 2018 which is the last data it has. The Nature Communications paper estimates that in 2024 China-based Bitcoin blockchain mining would consume296.59 TWh. Now I know that I am mixing up years but that would suggest Bitcoin would be consuming about 4.34% of Chinese electricity.

Now - going back to the Cambridge paper re 39% of bitcoin is renewables - I think that is based on the 'mix' of grid electricity in various countries. But in eg China, some miners have been setting up next to abandoned or low margin coal mines/power plants and indeed getting subsidies - either directly or indirectly (ie cheap/subsidised electricity) to place their Bitcoin farms there.

So I think the 'carbon footprint' of bitcoin is much higher than the Cambridge paper asserts. In addition, I am using 'Bitcoin' generically here to mean all cryptomining - I am not clear what definition others use.

So anyway - I would suggest that it would not surprise me if 6 - 7% of all Chinese COAL based electricity is being used for crypto/bitcoin / blockchain mining - and because often it will be near older / remote coal mines/power plants it is probably the dirtiest version of coal-based electricity.

I think that a number of funds that raced into Bitcoin will now be looking at the carbon footprint.

Small Caps Live Wednesday 26th May

Wey Education - Scheme Effective

Like all the best investments, in retrospect, this was a no-brainer. The largest division InterHigh was earning 60% gross margins and had been consistently growing at around 30% a year for 15 years. It was nowhere near market saturation yet and at the low point, the market capitalisation was dominated by cash.

Throughout, this was a story of people - the popular executive chairman who lucked upon a business but never understood what he had, the visionary founder who never wanted to be a plc CEO, the aloof chairman in it for a quick buck. In the middle of it all, there were plenty of opportunities for investors to make money, but there will always be a nagging feeling that a much bigger opportunity was lost.

PGM Miners

Rhodium has been one of the best-performing metals in the last year, rising 5 -fold in response to demand for tighter vehicle emissions and COVID-19 causing supply constraints:

Although Rhodium is usually only a small amount of the production of PGM miners, its relative value makes it a big proportion of profits. This has led to exceptionally strong results from companies such as Sylvania Platinum. Which has been reflected in their share price:

However, in the last few days this has faced a brutal sell-off:

This is a relatively thinly traded metal so we have to be careful reading too much into the graphs. Indeed Kitco and the Rhodium ETC show these severe falls, however, Johnson Matthey shows a much less severe decline. It is also not entirely clear what has led to the sell-off. A clampdown on speculation in China appears to be the most believable narrative but is pretty vague.

Whatever the cause, if this drop is real and sustained it will have a big effect on the profitability of the miners. Again, taking Sylvania where I have a detailed financial model, Rhodium at $25k/oz would mean they generated around $170m EBITDA for 2022. Whereas Rhodium at $15k/oz would give them $107m EBITDA. $5k/oz would be just $45m EBITDA.

The current move has therefore cut forward earnings for Sylvania by about 30% compared to where it would have been with pricing a couple of weeks ago, and about 40% when you include the recent weakness in other PGM and South African Rand strengthening against the Dollar.

It could be argued that the market was sceptical and never really priced in the large increases in Rhodium in the last year. Hence the lowly forward rating:

So having dropped around 10% yesterday, and around 15% off the all-time high, the temptation may be to Buy The Dip. However, Sylvania has always had a lowly rating due to a limited Life of Mine, at least at current production rates, plus political instability and what seems like a reluctance to return any significant amounts of their cash pile to investors.

The other reason to be cautious is that this has been much cheaper in the past, I originally bought Sylvania when it was on a forward EV/EBITDA of less than 1. Which makes today’s forward EV/EBITDA of c.3 look positively heady.

So at this point, buying the dip may be a little premature, and it may pay to wait and see if the recent drop in Rhodium price is an anomaly or the start of a return to more long-term average pricing.

Gold Miners

While Rhodium has taken a battering, Gold has popped its head above $1900 an ounce for the first time in a while. Renewed inflation worries plus the realisation that cryptocurrencies may not be as stable as some investors thought, potentially giving the barbarous relic a push.

However, as of yet, many gold producers have not returned to the levels they were when gold last hit these levels. For gold political instability has maybe helped with the price but not necessarily for individual miners. e.g. there appears to be another coup in Mali which is one of the major gold exploration areas.

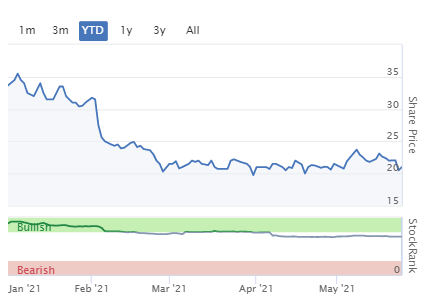

This sentiment has weighed heavily on the likes of Hummingbird Resources:

However, the last coup didn’t appear to impact gold mining operations in the country at all. And in general, I think the sector could be an interesting one over the next six months or so since it has largely not reacted to improved commodity pricing over the last month or so.

MAST Energy (MAST.L) - HY Report

Yes, Leo has looked at a company with “Energy” in the name, but he thought it would be interesting to look at something different!

This is one of a number of companies (listed and unlisted) working to balance the electricity grid where supply is becoming increasingly volatile due to an ever greater proportion of renewables. There are basically four ways this is being solved, placed in order of desirability and likely longevity:

Investment in the grid backbone, connecting geographically diverse generation;

Demand management through pricing, include at extremes paying people to consume or not to consume;

Storage, including battery, pumped and potentially hydrogen (etc);

Quick response energy generation from gas using relatively cheap and inefficient plant

MAST are in the fourth category. Today’s half-year results caught my eye. Why? Because they were issued late at 09:05!

MAST Energy Developments PLC acquired the entire issued share capital of Sloane Developments Limited (the 'Sloane SubGroup') with effect from 14 September 2020.

...

The acquisition has been recognised utilising the common control accounting principles under the predecessor valuation method, which requires the financial information of the acquired Sloane SubGroup to be disclosed for comparative purposes as MAST Energy Developments PLC has no historic trading activities.

Somehow they’ve managed to make it sound like the begrudge having to disclose previous figures!

Raised £5.54 million to support the Company's aggressive expansion plans following a successful IPO during concluded during April 2021.

As such Stockopedia doesn’t even know the number of shares yet, but we can see from their first RNS it is 188.6m, giving a current market cap of £24m, which happens to be in my personal sweet spot for investment.

They are listed on the main market and so the prospectus would be essential reading before any investment. I’m only going to review today’s statement, but the prospectus can be found here. Note however that, unlike an AIM Admissions Document, they may remove this at any time. The broker is “Clear Capital Markets”!? so not exactly mainstream.

The accounts show zero revenue and negative net assets of £0.4m as at March 31st. Adding in the funds raised might take this to £5.1m, although they are evasive about IPO fees and two months cash burn will certainly take it below £5m.

In the commentary, it is mentioned that their first site is currently over budget and that they are still negotiating debt finance. The second site is in testing, but only equates to £42k of revenue per month and the third one is still being evaluated.

Hopefully, by now, you have concluded that this is uninvestable. I would go further and say that this company is a complete joke and yet another example of why I usually ignore companies with “Energy” in their name.

SDI (SDI.L) – Trading Update

There’s an old saying in the markets: Buy on the rumour, sell on the facts. It reflects the idea that everyone is trying to get in before everyone else and if you want to beat the market you have to be in and out before the crowd.

A few months ago, anything that produced results would pop up, since the recovery from COVID-19 was often leading companies to beat expectations. There are signs now that these beats are becoming expected. For example, SDI produced a good trading update today:

Subject to any audit adjustments, we now expect to report Revenue of approximately £35.3m and Adjusted* Profit Before Tax of approximately £7.4m, both of which are higher than those provided in our 10 February 2021 Trading Update.

But the share price is down slightly.

This reflects the fact that the price had risen over the last few days in anticipation of these results, and that having guided in line for FY22:

We have not changed our expectations for our current financial year ending 30 April 2022 compared with the update provided on 10 February 2021 (Sales > £42.0m, Adjusted PBT > £8.7m).

They are no longer cheap on a 2022 P/E of over 25. The forecast PBT growth rate is 18%, which isn't bad, but with the current rating, even more growth than that appears to be in the price. Holders are clearly betting that they beat again during the year, which they may do. I'm not personally confident enough of that to invest on that basis, however.

De La Rue (DLAR.L) - FY Results

These are Results to the end of March. Gross profit is flat, but adjusted EPS is up 32% to 14.7p reflecting their recent cost-cutting exercise. As many companies like to do, they calculate the EPS figure excluding the costs of making the cost savings but counting the cost savings! So these figures are perhaps a little flattered.

The outlook is positive but in-line:

Trading for the first two months of FY 2021/22 has been positive and in line with management expectations.

And they signal a return to dividends, but not until 2023:

Following an initial period of cash outflow to fund the Turnaround Plan, we continue to aim for the Group to be generating cash flow capable of supporting sustainable cash dividends to shareholders by the end of the Turnaround Plan in FY 2022/23.

Net debt is still £52m despite the recent equity raise, and they have always run with negative working capital. This perhaps makes the current rating of 13x 2022 forecast EPS look a little rich, given that there is little EPS growth forecast. This was an interesting turnaround story, but one that appears to be largely driven by cost-cutting, and is now priced in. Any upside from here will require growth to return, and for that, we appear to be looking much further into the future than I’d be willing to bet on.

Small Caps Live Friday 28th May

NMCN (NMCN.L) – Trading & Financing Update

NMCN is one of the biggest small-cap fallers this morning on the following announcement:

This has been a core focus of the Board in light of a number of contractual issues exacerbated by the COVID-19 pandemic which have resulted in the Group now expecting to report overall underlying losses before tax of £24m, approximately £6m of which are attributed to 2019.

The loss is not small compared to a market cap of about £24m. Some will be write-downs but this shows how badly things have gone awry. And this is a company that had contract and accounting issues.

They currently need to secure new banking facilities:

The Board has now received heads of terms and is working towards concluding an agreement during June. If the Group is unable to secure commitment for the requisite level of funding to satisfy its ongoing working capital requirements, then the Company will need to consider all appropriate options. The Company's overdraft facility with Lloyds Bank plc has been extended into June to accommodate the continuation of these discussions.

They seem likely to get them in the current market but with punitive interest rates, as we have seen from the likes of Hostelworld, who had to effectively pay 12% interest for their debt, or Smiths News who had to go outside of the mainstream lenders to borrow the amount they needed. If they don’t get the facilities, then it is either an emergency rights issues, or lights out.

The dire situation here didn’t stop investors hoping for a recovery buying the dip….twice, with the shares bouncing from £2 to around £3 in both November and March.

Nice work for a trader, but anyone holding the shares now faces a loss, maybe a total one if the banking facilities aren’t agreed.

Gama Aviation (GMAA.L) – Final Results

In other ‘what on earth were investors thinking’ news, Gama Aviation released their results to 31st December yesterday. You know things are going to be bad when the “highlights” don’t mention revenue or profits. Of course, revenue is down significantly and they report an EBIT loss.

This is another stock that has suffered from accounting issues, and has gone through multiple CFOs recently, which combined with high debts and ongoing losses makes it uninvestible for me. When a company has all these qualities why continuing analysing?

There was a time where I thought Downing would backstop the equity in terrible companies no matter what went wrong, however, Redhall proved that not to be the case - and GMAA looks worse than that on some metrics - e.g. the debt is too big for Downing to underwrite!

Real Good Food (RGF.L) – Loan Note Waiver

Talking of Downing and 12%pa debt, there was an update from Real Good Food today. This is an interesting one. Interesting if you’re not a shareholder, anyway.

Downing have a big loan note investment in the company and a small equity one. They have said variously in the past that they don't care what happens to the equity and that it could come good, but clearly, the main interest is in the former. Traditionally debt ranks ahead of equity, with equity being wiped out first, but for expediency, this isn't always the case. In particular with lease renegotiations. However, when you see something like this:

Real Good Food plc, (AIM: RGD) the diversified food business announces that further to the disposal of Brighter Foods Limited, as announced on 22 April 2021 and completing on 11 May 2021 (the "Disposal"), each of NB. Ingredients Limited ("Napier Brown"), Omnicane International Investors Limited ("Omnicane"), and certain funds managed by Downing LLP ("Downing") (together the "Major Shareholders") have each agreed to contribute £180,000 towards the costs incurred by the Group in relation to the Disposal.

You've got to think the equity is worthless and they are only still listed in order to ease a debt for equity swap at a future point.Dilution is likely to be massive, otherwise surely debtholders would just take control entirely. Perhaps the debt holders have done this to allow the company to be a going concern in the next accounts, but if they thought the equity was worth anything surely they do a debt for equity swap on this little bit. I suspect it just isn't worth the hassle. The price is unchanged but was already near year lows, very unusual in today's market.

Petards (PEG.L) - Final Results

Petards do cameras and related systems for trains. This was previously driven by promises to replace/upgrade trains made by franchise operators in order to win bids. But these operators were effectively nationalised last year due to covid and it has recently been confirmed that the rail franchise system is being dismantled.

Results seem pretty good under the circumstances:

Total revenues £13.0 million (2019: £15.7 million)

Gross profit margin 36.4% (2019: 30.8%)

Adjusted EBITDA* £320,000 profit (2019: £281,000 loss)

Operating loss £1,145,000 (2019: £1,287,000 loss)

Loss after tax £583,000 (2019: £193,000 loss)

Strong cash generation from operating activities £2,398,000 (2019: £142,000)

Total net funds (cash less debt) £1,179,000 (31 Dec 2019: £525,000 net debt)

Basic and diluted EPS 1.01p loss (2019: basic and diluted 0.34p loss)

Post year end secured undrawn £2.5 million 3-year CBILS overdraft facility to May 2024

So they have improved margins, cut costs, improved working capital management and refinanced.All good. But:

To reflect uncertainty as to how Government's near term rail investment plans would affect the Group's order intake, the Board adopted a cautious approach to the revenue budget for this activity, basing it on already secured systems orders with a de minimis contribution from new business other than on-going orders for spares and repairs. While the outlook for 2021 order intake is now looking more promising, it remains too early to say whether such prospective orders might make a meaningful contribution to 2021 revenues.

That's pretty terrible, and shows how having multiple customers doesn’t always remove risk when they all face the same regulatory regime. Fortunately, they do have traffic and defence businesses also. My view is that Petards is subscale in each of its businesses and needs to be broken up….and that’s the bull argument!

Revolution Bars (RBG.L) - Placing

There has been much gnashing of teeth in small-cap land over the size of the discount on the Revolution Bars Group placing this week:

The Issue Price represents a discount of approximately 41.2 per cent. to the closing price of an Ordinary Share on 24 May 2021, being the latest practicable date prior to this announcement, and a discount of approximately 27.8 per cent. to the volume weighted average price of an Ordinary Share for the 90 day period to 24 May 2021.

This led to some rather unusual exchanges on Twitter, such as this one:

You’d have assumed someone claiming to be a debt fund manager understood the relationship between debt and equity. We have been warning that Revolution Bars needed fresh equity on scl for months.

In current market conditions, investors forget that this was a highly indebted business, that faced challenges even before COVID-19. Restrictions on trading have gone on longer than any of us would have imagined, and they previously raised money at 20p when things were looking better.

So strange complaining about the discount. In reality, 20p looks a very good price in the circumstances. The bonkers part is investors bidding up the price of a business so clearly in trouble to such high levels.

Looking at the pro-forma balance sheet, the Current Ratio improves from 0.5x to 1.2x and net assets improve from -£39m to -£19m. (The net asset calculation is actually quite simple: £39m deficit of lease liabilities above right-of-use value, despite multiple CVA and similar events, £20m newly raised (after costs), everything else balances, Net Assets of £-19m.

So for RBG to now be worth zero, there must be £19m worth of unaccounted-for intangibles, e.g. brand recognition, know-how etc. Is that really credible? Surely you could do better with £20m by starting again from scratch?

finnCap update their note, and it is positive, as they have to in these circumstances. However, their price target of 40p is a PE of 44, two years out, on an adjusted basis, for a company with lease headwinds, a dismal track record, and operating in a market in long term decline! Perhaps, finnCap are just preparing themselves for the next time Revolution will need an equity raise.

Centamin (CEY.L) - Portfolio Update

Centamin fell yesterday on this update, which is perhaps strange when the RNS seems positive in tone:

The Doropo Project shows strong development potential with the completion of a positive preliminary economic assessment ("PEA"):

US$234 million post-tax net present value ("NPV5%") with a 21% internal rate of return ("IRR") at US$1,450/oz gold price

US$487 million NPV5% with a 33% IRR at consensus gold price per ounce of US$1,829/oz ("consensus")

Total development capital expenditure ("CAPEX") of US$275 million, including a 15% contingency….

Board has approved US$14 million spend to advance the project to PFS stage by mid-2022.

They can easily fund that level of expenditure from existing cash resources, so on the surface, this is an asset with an (unrisked) value of half a billion dollars. However, the eagle-eyed will spot that they have used a 5% discount rate in their NPV’s which seems totally inappropriate for the sector and location. They must think the project is worth progressing since they are getting to the PFS stage, so maybe better economics to come.

It does seem strange to sell off on the news though, I doubt much was in the price for explo given the c6% dividend yield paid from current production.

Adding to the woes, Liberum issued a sell note on CEY with an 82p target. Again, seems harsh given that CEY hasn’t risen much with the recent gold price strength. Last year when gold approached $2000/oz then CEY was above £2 per share. With gold at $1900/oz they are at £1.12.

Generally, we are not fans on scl of relative valuations but there does seem to be a bit of an anomaly here. Their cash flow with gold oat $1900 is much higher than at $1700, they may of course have been massively overvalued at £2.25. And since then they have had problems at Sukari. But there are problems and 'problems' - effectively they are removing some low-grade resources from the mine plan and paying Capital Limited $200m or so to do some waste stripping. I’m not sure that wipes $1b+ off the NPV. Gold at $1900/oz would seem to suggest the price probably should be higher than the current £1.10 or so.

Hummingbird Resources (HUM.L) – Final Results

Also struggling in the gold mining sector is Hummingbird Resources who produced FY results yesterday.

On the surface, HUM is cheap, you are getting 100koz of gold production for less than £100m market cap. Not only this but they have another 100koz project approved for development.

The cashflow here is impressive - with debt now completely paid off, post period end, and $66m of cash inflow from operations. The problem is that the bulk of that was in H1. And since then production is down and costs are up. The market has been long-term bears on the management here. We mentioned the coup in Mali on Wednesday's scl, which hasn't had a direct impact, however, has also presented challenges getting equipment across borders and similar impacts.

However, they now have a new mining contractor and a new ops director, plus a 100koz development opportunity approved at Kouroussa. On outlook they say:

During 2021 our primary focus will be to ensure that the operations at Yanfolila are stabilised and output is more predictable. Our guidance for the year is 100,000 to 110,000 oz of gold, with an All in Sustaining Cost of US$1,250 to 1,350 per oz of gold sold. We are at the high-cost part of the life of mine plan, and there are a number of initiatives in place that are being further developed in order to improve efficiencies and reduce cost across the operation.

So, much like Centamin, if Hummingbird can get a handle on their issues then they could be worth multiples of the current price, however, they are much riskier than Centamin and don't pay a dividend while you wait, so this is very much for the high-risk investor only.

There will be no Large Caps Live on Monday due to the UK Bank Holiday. Have a great long weekend everyone!