Small Caps Live Weekly Summary

AO. SUP CML MPAC AGFX NCYT D4T4 SMRT

One of the critiques we often receive is that we are unduly negative in our summaries here. In considering this, it is worth bearing in mind that what is in this email is often a summary of a more thorough discussion on our discord server where a bigger range of views is likely to be expressed. However, there is good reason for our usual caution. The companies we choose to analyse are quite eclectic. Sometimes they will be companies we own shares in. But often they represent companies that look interesting, or are popular or talked about in other places.

Investing in popular stocks is usually a bad idea. Ed Page Croft from Stockopedia tracked the returns of the 100 most discussed stocks from popular UK investment discussion websites between 2014 and 2016 and found that these underperformed the UK All-share Index by over 18% during this two-year period. Ed says that the problem with investment forums is that instead of producing a diversity of opinions, ‘the best storyteller with the best story wins.’ We don’t want to be a similar echo chamber, so if you disagree, join us on discord and have your say.

That said, we tend to focus on the things that most investment commentators don’t understand or choose to gloss over in their pursuit of a good story. We look at balance sheet strength and cash burn for growth stocks - even more so in the current bear market for small caps. We look at the triennial pension deficits and the agreed recovery payments rather than simply taking the IAS19 number from the accounts as gospel. We adjust our earnings yields for debt, pensions or negative working capital. We look for anomalies that suggest the income statement may not reflect economic reality.

Concentrated investing based on valuation criteria should have a high bar for investing in any given stock. This means we reject the majority of companies we analyse. We often find good companies that are priced much too highly and hence these go onto our watchlist. Or we find stocks that have a superficial attraction but have factors that makes them uninvestable for us. Sometimes a company looks good but a similar company is available to purchase at an even better price. We don’t always get it right. In fact, Mark, Leo & WayneJ regularly disagree completely over what companies are the most attractive at any given time. However, over the long term, we get enough right. Our aim is not to “tip” stocks, but to show how a conservative experienced investor might go about assessing an opportunity and to generate debate.

Again, there was no large caps live this week, but plenty of small cap news.

Small Caps

AO World (AO.L) - Response to Recent Press Reports & Placing

Yes, this is a small cap now! This week they issue a response to the following article in The Times which said:

Online retailer AO is facing a cash crunch after a leading credit insurer cut cover for suppliers following a deterioration in the company’s finances.

Market sources say Atradius has slashed cover for suppliers to AO, which sells everything from washing machines to TVs and fridge-freezers.

Removal of suppliers’ credit insurance often spells the end for businesses, so we read this response with interest:

AO World plc ("AO" or the "Company"), a leading online electricals retailer, notes today's share price movement following press reports over the weekend. The Company's current financial performance and financial position remain in line with the Board's expectations and the guidance set out in its trading update on 29 April 2022.

The guidance didn't look good but this isn't about whether they are in line with guidance, but about balance sheet strength and confidence.

AO confirms that it is aware that one of the third-party credit insurers who provide credit insurance to some of its suppliers rebased their cover in May 2022 with respect to AO, reflecting post-Covid sales levels.

OK, so did the credit insurance company decide AO didn't need the coverage anymore because the sales were lower? Or did they decide they didn’t want to cover them because their finances were further threatened by sales being lower? We’re assuming "coverage" is a pound amount rather than a percentage. Do credit insurers really set pound coverage based on what they think the customer needs rather than what their balance sheet can support? Seems unlikely.

This was a reduction from the heightened levels that had been in place and required through the period of the pandemic. To date this rebased cover has had no effect on AO's liquidity position which remains in-line with the Board's expectations for FY23.

It does at least seem to be the case that they weren't using the removed cover since this happened back in May.

On 9 June 2022, AO announced the decision to close its German operations. Progress to date has been encouraging with total cash costs of closure now expected to be towards the lower end of the Company's original estimates of nil to £15m. The higher end of that range assumes the Company would be unable to exit certain asset leases, of which c. £10m of cash outflow would be due in future years.

Either they have somebody signed up for the leases or they don't. The above suggests they don't.

AO continues to have full access to its £80m revolving credit facility, the term of which runs until April 2024. In addition, the Company continues to consider and implement a number of ongoing initiatives and further actions to strengthen its balance sheet while optimising its focus on profit and cash generation against the uncertain macroeconomic conditions in the UK and the continuing global supply chain challenges.

The year-end is March 31st, so that means a 12-month going concern statement for FY 2023 would still factor in the revolving credit facility. So this is a while away yet. But they did seem to be raising the possibility of issuing more equity. Cost-cutting or new debt facilities wouldn't qualify as "strengthening the balance sheet", and I don't think they have anything to sell. "Optimising focus on profit" could, inter alia, include reducing google adwords spend which would directly save smaller competitors, such as Marks Electrical that we have covered in the past, money and shift their economic sweet spot towards more advertising and faster growth.

It didn’t take long since later in the week, AO announced the placing:

The new Ordinary Shares issued pursuant to the Placing and the Primary Bid Offer (together, the "Capital Raise") are intended to raise gross proceeds of approximately £40 million. The net proceeds of the Capital Raise will strengthen the balance sheet and increase liquidity back to historic levels (relative to revenue base), and provide the flexibility to capitalise on market opportunities.

But is this enough to avoid further cutbacks?

In 2021 they claimed PBT of £20m and cash generation of £60m, but 2021 was a strong year. Their measure of EBITDA excluded £14.2m depreciation on right of use assets (£8.7m leases) and £4.0m interest on lease liabilities. On the balance sheet, current liabilities were well ahead of current assets. Of that £60m cash flow, £58.5m was net working capital movements, with payables increasing in pound terms well ahead of inventories and receivables. They did repay £22m of debt, but we would expect the forecast negative net profit swing of £38m to mean they will consume cash in 2022 before working capital movements. And while inventory may unwind, we've read the evidence that payables are unsustainably high. On any reasonable assumptions, the current ratio will still be less than one at the end of the year even after a £40m raise.

So we think they are still going to have to cut costs. Advertising and marketing was 3% of revenue last year. Reducing this to 2% would save them £15m assuming some resultant hit on revenue. Warehousing is quoted as 4% of revenue, but they have expanded space in the face of falling sales so this is likely to unavoidably rise.

Whether they have raised enough for the next year likely comes down to whether they listened to the credit insurers properly and whether these are now likely to change their minds.

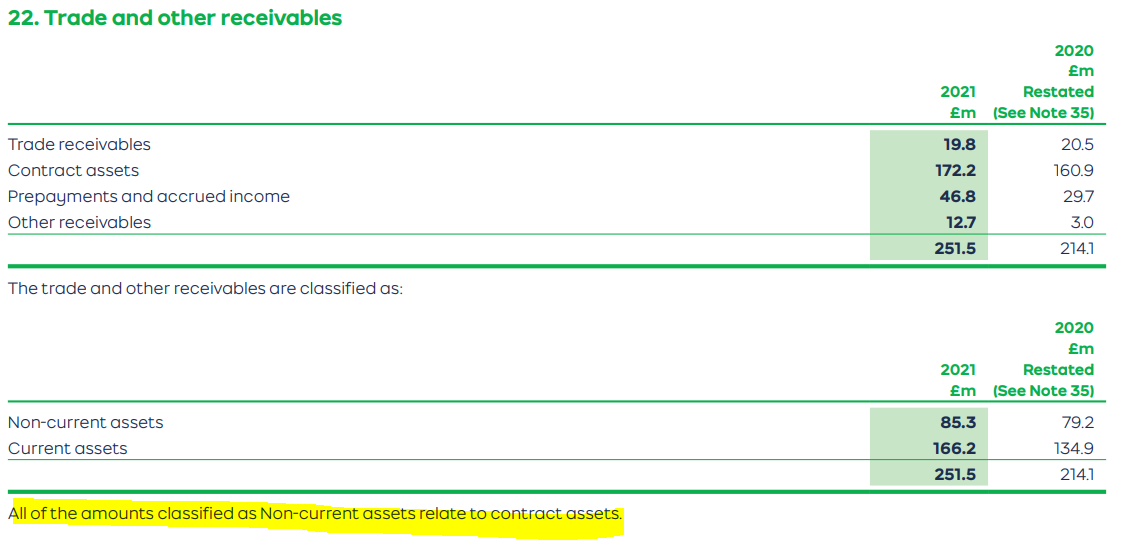

Ideally, their current ratio should be over one. Their non-current "Trade and other receivables" also look far from ideal. This is what the notes to the accounts say:

These can be reversed, as indeed happened last year:

Included in the total contract asset balance at 31 March 2020 was an amount of £3.6m in respect of variable consideration recognised as revenue up to that date that has been reversed in the year ended 31 March 2021.

Clearly, consumer behaviour with these generally poor value products is liable to change during a cost of living crisis. A campaign by MoneySavingExpert etc. could also have a considerable impact and regulatory intervention is not impossible.

So, in summary, £40m doesn’t appear to be enough. Forced de-stocking, a halt on advertising or even, in extremis, failure during the next 12 months cannot be ruled out. Risks from consumer and credit insurer behaviour are clear but difficult to quantify.

Supreme (SUP.L) - Final Results

Following the year-end trading update we said:

simplistically, they did £10.1m Adjusted EBITDA in H1 which was 5.9p Adj EPS so £21m FY EBITDA would be 12.3p pro rata.

Stockopedia shows a 12.6p forecast. This is how they actually did at the EPS level:

So that looks like inline / a tiny beat on fairly standard adjustments:

Adjusted EPS means Earning per share, where Earnings are defined as profit after tax but before amortisation of acquired intangibles and Adjusted items (as defined in Note 7 of the financial statements). Adjusted items include share based payments, fair value movements on non-hedge accounted derivatives and other non-recurring items (including all IPO-related costs).

Some positive relative trends from an ESG perspective:

- Vaping revenue growth of £4.1 million (10%)

- Sports Nutrition & Wellness revenue growth of £9.0 million (132%).

And no mention of supply chain issues or any other obvious challenges in the operational review. The headline outlook statement says:

The Group expects to deliver another solid, profitable year in FY23 but revenue and EBITDA are both expected to be below FY22 levels and below previous market expectations, driven by a recent marked decline in the Lighting category following a slow-down in sales compounded by customer overstocking in FY22.

That's got to hurt. And indeed it did with the share price down over 30% on the day.

They said lighting was brought forward and also predictable, yet they apparently didn't predict the knock-on effects!

Whilst it is still early in the new financial year, the nature of lighting sales where a significant portion are sold "FOB" on long lead times means that the Board has relatively strong visibility into the latter part of the year and the expected weakness in trading.

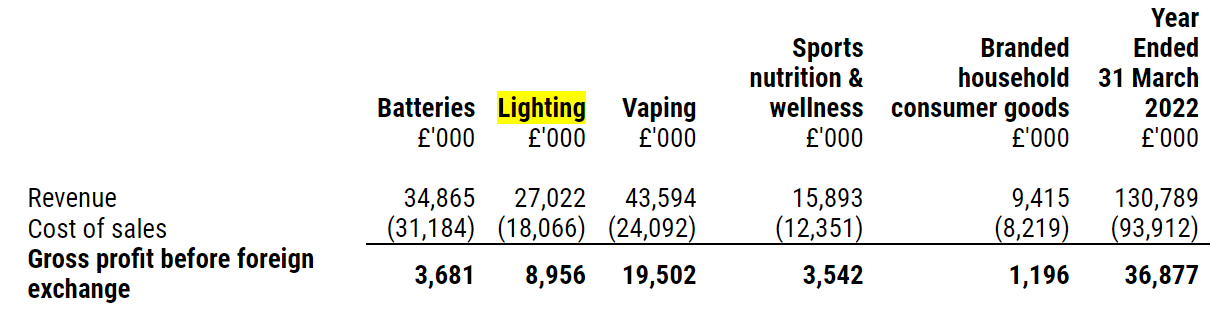

So the claim appears to be that they have long visibility and as a result, they can see problems on the horizon. However given their March year-end, this is falling in this financial year. Here's the segmental analysis:

Lighting is 21% of sales, and 24% of profits. Broker, Equity Development, say:

High margin (33.1%) Lighting products contributed 24.3% of FY22 gross profits, making the impact of inventory correction noteworthy.

Accordingly we reduce our Group FY23 revenue outlook from £143.5m to £129.5m, and EBITDA from £22.8m to £17.5m.

ED has cut sales forecasts by £13.5m. So revenue in the lighting segment is halved. But EBITDA was cut by £5.3m. Which does not add up because the gross margin on lighting as per the above table is 33% and 33% of £13.5m is £4.5m. So there must have been a cut elsewhere too.

With a 25% cut in 2023 EBITDA, the 30% fall in share price looks much too high if this is a one-off destocking effect. The company say:

There are no customer or retail listings losses to report and therefore profit progression for this category is expected to return in FY24 once the supply chain has rebalanced.

However, ED has cut 2024 EPS forecasts by 24% too which again doesn't make sense if the only factor here is one-off destocking in lighting in 2023. In light of this, the fall looks much more reasonable. However:

Vaping, the Group's largest and most profitable category, continues to perform very strongly and is expected to deliver revenue growth of around 30% in FY23 - half of which driven by new product development, continued market growth and further distribution expansion and the other half from the Liberty Flights acquisition.

Vaping is already 1/3rd of the business. On these figures, it will be 40% for FY 2023. We don't think anybody can believe the earnings quality of vaping is as good as batteries, though growth prospects may offset that for some. It is also why they are cutting the dividend:

Management remains committed to investing in organic growth opportunities alongside pursuing an active acquisition pipeline, particularly in the vaping division.

Looks like they are going pretty-much all-in on the vaping side with more acquisitions planned.

With this in mind, the Board has reviewed its capital allocation policy and believes that M&A can drive better rates of shareholder return compared to servicing its existing dividend commitments. Accordingly, the Board proposes to revise its dividend policy from a pay-out ratio of 50% of net profits to a minimum of 25% in respect of FY23 onwards.

As much as the company say, “With increasing levels of government support for vaping, we expect the revenue growth to continue”, we really don’t like the regulatory risk on the vaping side. The ethical side is a bit more nuanced. The availability of vaping likely means that fewer people will die of smoking. However, this assumes it is just a smoking replacement whereas clearly it also has the power to addict new users who wouldn’t smoke. It is worth noting that all of their products appear to be flavoured in some way. Hence we see banning as highly unlikely but some regulations on advertising etc. very possible. At the end of the day, investors will need to make up their own minds on this.

The 2024 forward PE is now 7.5x with EPS below 2021 and 2022 levels following this trading update didn’t look especially cheap in the current markets given the risks. However, this has continued to fall during the week and is approaching a level where the adventurous investor may be willing to take the risk.

CML Microsystems (CML.L) - Full Year Results

Nice for them to start with an apology. Too many companies have had delays and tried to brush this under the carpet:

I must apologise for the delay in publishing this year's results, but this was due to the Group's auditor, BDO LLP (BDO), requesting additional time to finalise their audit process and internal review procedures.

The first thing to note about CML is that the balance sheet is rock solid - with a current ratio of 10.29. They have around £25m of cash and it appears to be largely surplus to requirements. This is after paying a £9m special dividend. Post year-end, they have spent £3m on a share buyback and also have a surplus property that they are looking to sell this year. In the current high inflation but low-interest-rate environment, cash sitting on the balance sheet doing nothing is not particularly useful. They seem to be keen to take advantage of the cash pile to scale up via acquisition, though:

Potential opportunities fitting these criteria are constantly under consideration and the ability to move quicky if opportunities materialise is essential. To aid this, the substantial number of shares in treasury, coupled with our relatively strong cash balance, provides the flexibility needed to meet these goals.

[A moving “quicky” has certain connotations, so we can only assume this is a typo and should read “quickly”!]

Perhaps in the current environment, they will actually get something over the line at a reasonable price?

The current results sound good, with growth in revenue & profits:

Revenues were £16.96m up 29% (2021: £13.10m), reflecting the recovery in our existing end markets. The revenue increase, coupled with tight cost control, yielded a considerable improvement in profit from operations. Profit before tax grew to £1.74m (2021: £0.01m) and a resulting tax charge of £0.50m delivered profit after tax of £1.24m (2021: £0.80m).

However, EPS came in at 7.45p vs a Stockopedia consensus of 10.6p. This may well be the result of stale forecasts due to them selling off a subsidiary last year. So even if this isn't a miss, how can we trust the consensus of 13p EPS next year? Even adjusting for the large cash pile & taking the 13p EPS at face value this is an adjusted forward earnings yield of around 6%. This is expensive in the current market.

Particularly since the cash flow statement shows that this growth/recovery appears to require high CapEx spend and the stockopedia stock report shows this with a ROCE of sub-10% even in normal times. The company recently bought back shares above £4 and has a consistently low ROCE. This appears to show that the management has quite poor capital allocation skills. So betting that they will suddenly change this and find great acquisitions seems foolhardy.

This is a very conservatively run business and with that balance sheet, this isn't going to go bust, which may appeal to some in the current market. But given the apparent level of overvaluation and potentially poor capital allocation, shareholders could easily lose money here if this derates to a more normal multiple, even if the company grows in line with forecasts or completes an acquisition.

Mpac (MPAC.L)

No news on this one but worth noting that Leo produced his second blog article on MPAC, focussing on the Freyr battery contract. The possibility of this contract makes the current MPAC price a low-cost option on the future of Freyr.

Argentex (AGFX.L) - Full Year Results

Decent revenue & profit growth here:

Group revenue increased by 23% to £34.5m (2021: £28.1m), including £8.0m from new clients

Adjusted operating profit(1) up 26% to £11.0m (2021: £8.7m)

Earnings per share (EPS) 6.6p (basic) and 7.0p (adjusted) (2021: 5.2p basic and 5.9p adjusted)

Although it looks like a slight miss on EPS: 7.0p vs 7.4p forecast in Stockopedia. However, the outlook looks strong:

Current trading has been positive with first quarter revenue increasing by 22% to £10.1m (Q122: £8.3m)

They continue to add more corporate clients and given that no one goes through KYC paperwork for fun, these are likely to be reflected in higher sales over time.

However, this doesn’t line up with the future their new NOMAD and broker, Singer, is seeing with a forecast of £39m revenue & 4.9p EPS for FY22. Previous NOMAD, Numis, had forecasts of £42.8m and 9.3p EPS. So this almost halving of EPS forecasts in response to today's results looks like a closet profit warning. The market has taken it as such, with initial enthusiasm with the results being sold into by those who then read the new broker’s note.

On the investor call, the management said these are a “conservative view” and didn’t want a repeat of the market selling off on great results that happened to slightly miss optimistic broker estimates. Clearly, they are setting these up to be beaten during the year. However, this leaves shareholders in a quandary - the shares appear overvalued on near-term forecasts. However, we are pretty sure those forecasts are wrong. But we have no way of estimating how wrong they are - perhaps they expect to get close to what Numis originally had in, or perhaps they see short-term investment meaning revenue growth will not be reflected in EPS this year and are aiming to beat only slightly.

Mark’s instinct says that this is still a good GARP stock, at least on a medium-term view. But management repeatedly shoots themselves in the foot on the IR front, and until they sort this out, they are unlikely to see a significant re-rating.

Novacyt (NCYT.L) - Trading Update

Group revenue in H1 2022 was £16.5m (£13.0m COVID-19 related) compared to £52.2m (£47.6m COVID-19 related) in H1 2021 [continuing operations]

It is very good of them to split out covid and non-covid, although some judgement will have been exercised in this. Excluding covid, that revenue fell to £3.5m versus £4.6m the previous year, so not a good sign.

This shows a 73% decline in COVID-19-related revenues for H1 2022 compared to H1 2021, which is faster than previously anticipated by the Board.

However, investors should have been valuing this on zero covid sales with anything received as a one-off cash bonus. The impact in the short term is given as:

the Board expects full year revenues of circa £25.0m (previously expected full year revenues of circa £35.0m to £45.0m)...

And the response is to accelerate cost-cutting:

Following a further review based on the faster than expected decline in COVID-19 revenue, the Company is taking steps to further rationalise its cost base, targeting an additional reduction in operating costs of £2.4m this year and a one-off cash restructuring charge of circa £0.8m.

This is actually quite positive - Leo has complained in the past that the company is run by academics and the strategy is more about doing stuff academics find fun rather than making money. The cost-cutting suggests otherwise. But it may also indicate an expected adverse outcome from the DHSC litigation and a desire to keep doing fun stuff for longer.

The ongoing operating cost run-rate of circa £17.0m doesn’t compare favourably to a revenue run rate of £3.5 x 2 = £7m.

The Company's cash position at 30 June 2022 was £99.6m, compared to £101.7m at 31 December 2021.

The bull case here is that those not-covid instrument sales that happened during covid give them an installed base of equipment customers can run their other tests on. The bear case is that DHSC has taken a sledgehammer to them all! For example, they say:

Novacyt has advanced the product design of two new polymerase chain reaction (PCR) assays for near-patient testing in infectious diseases. These new assays are focused on gastro-intestinal viruses and bacteria and will run on the Company's q32 instruments.

The trouble is with this and the rest of the developments detailed in this section is that they are reliant on public health systems to pick them up. Post-covid this puts them back into the business of very long sales cycles. It also means high customer concentration risk, including with the DHSC with they have a bad commercial relationship.

Given that they are taking some inventory write-downs and show little sign of being willing to return their cash balance to shareholders, you can see why the market reacted negatively to this profit warning. In this case, the shares trading at a big discount to cash on the balance sheet seems well warranted.

D4T4 Solutions (D4T4.L) - Final Results

Revenues up 7.3% to £24.5 million (2021: £22.8 million)

ARR as percentage of total revenue increased to 57% (2021: 47%), delivering significant progress against medium term target of 65%

Gross profit margin of 51.9% (2021: 62.4%)

Adjusted profit before tax** of £3.3 million (2021: £4.4 million), and statutory profit before tax of £1.8 million (2021: £3.0 million)

Diluted Adjusted EPS of 7.1p (2021: 9.5p), and Diluted Basic EPS of 4.1p (2021: 6.75p)

Revenue is up, but adjusted PBT is down due to the drop in gross margin. This is mainly due to higher amounts of lower margin 3rd party sales this year. Both revenue and adjusted EPS are a small beat on forecasts though so these factors were expected. However, you can drive a bus through the adjustments. They are mainly share-based payments but they also have one-off restructuring costs that occur every year. The conservative investor will want to add back in the restructuring costs and take the fully-diluted share count when analysing this.

The growth in ARR is positive, however. Positive cash flow and a product that is relatively unique are what separates D4T4 from many SaaS businesses. Indeed, the special dividend announced with these results shows the level of cash generation and the willingness to return excess capital to shareholders.

House broker finnCap say:

D4t4 starts FY23 with a stronger pipeline and £14m of ARR. We lift our revenue growth expectations from 10% to 15%

Leo thinks these forecasts are conservative. However, they also say:

management intends increased investment to reinforce the success being achieved in new products, markets and direct sales, so we ease FY23 earnings expectations as D4t4 invests for long-term growth.

So we can perhaps expect the short-term earnings growth to be muted by this. Leo thinks that this investment will pay off and the effects of the SaaS transition distortions will be gone and lead to beaten forecasts in the short term and significantly higher earnings in the long term. Mark is more cautious. He looks at an EPS figure that is lower than 5 years ago, and doesn’t think distortions from the SaaS transition and increased investment should still be having so much of a negative effect after such a long period. Although this is clearly a good company with a good product, a forward P/E of 26 means that investors today are already paying up today for expected growth years into the future. The real test will be if that strong EPS growth appears or not.

SmartSpace (SMRT.L) - Trading Update

Trading in the current financial year has continued in line with management's expectations.

While this is good to hear, we don't know what management expectations are and the trends have been a bit meh recently. The most important information is missing from this update. Namely what the current cash balance is. This is Leo’s graph of cash level trend:

Management should be fully aware that there are concerns over cash levels. And we’d really want to see an update that showed they had positively deviated from that trend. Of course, things may be absolutely fine on this front but without this figure, we are in the dark.

SwipedOn has continued to trade well, with ARPU* and ARR** increasing

They do not say the number of customers has increased and ARPU changes recently have been due to price increases not a greater number of customers. To be fair, this has not been quite a fair metric: some small customers were picked up for covid-related functionality and then lost, as expected. Some ARR increase was pretty much guaranteed as previous price increases work their way through, plus SaaS contracts often include an annual inflation uplift for those that can't be bothered to negotiate. Sadly, management have chosen not to provide these numbers.

There is some positive newsflow on contract wins though:

We have also engaged with our first customers in South Korea.

They have invested significantly in localisation so it is good to see a return on that, however unquantified. And:

In the past week, SwipedOn signed its largest client for 'Desks', with the order coming from an Australian- headquartered consulting business with 200 offices and 10,000 employees worldwide.

However, it seems that the order is in several phases and who knows whether progress beyond the first phase is guaranteed. It is very common or even usual in the SaaS space to be sales-led rather than product-led and while SmartSpace may not be the worst of them, clients might not like what they see after the first phase of 200 desks.

The most positive news is buried in the middle:

A+K has had a strong start to the year, with revenues significantly higher than for the same period last year.

This more physical business had been a significant cash drag on the group and there was no guarantee it would recover post-covid. But again, no numbers are given. There is also some positive news for SpaceConnect.

A further trading update is planned for August where hopefully we will get some concrete figures and the latest cash balance. Until then, a very wide range of outcomes is possible here.

That’s it for this week, enjoy your sunny weekends.