Small Caps Live Weekly Summary

LUCE CAPD APP G4M TUNE SMRT MPAC KMR CCT MAI NWOR QUIZ RBG TGP

There was no shortage of small cap news to discuss this week, so we’ll dive straight in.

Small Caps

Luceco (LUCE.L) - 2022 FY trading update & CFO change

Luceco announces results at the upper end of the guidance range. However, this was cut significantly during the year:

The market has really liked this update, however, since the shares rallied by 25% on the morning of the announcement, and we can see why. The big fear was they had allowed themselves to become overly indebted in a weakening market. However, Q4 cash flow has been great:

The Group generated exceptionally strong free cash flow of c.£21m in Q4, adding to the £11m generated in Q3, driven by inventory optimisation and disciplined cash collection.

And net debt looks low enough that they could do more acquisitions if they want to:

We expect to report pre-IFRS 16 net debt at 31 December 2022 of £24m (30 June 2022: £53.9m), equal to 0.8x Adjusted EBITDA (30 June 2022: 1.4x). This significant deleveraging was driven by record full year free cash flow of c.£30m.

Plus, maintain the dividend.

Looking forward, they say that customer destocking is close to being over, there is no disruption to their China manufacturing, their margins are rebuilt with cost pass-through, and freight costs are falling. If anything, it looks like 2023 should be an upgrade.

Broker Liberum are taking the wait-and-see approach, though, saying:

We leave our 2023E estimate unchanged awaiting the health of the spring selling season to understand the strength of the residential RMI market this year. Given the comments on gross margins and that cost inflation is expected to moderate, and that activity appears to be stabilising, we consider the risks to be to the upside.

As well as this trading update, there is an interesting CFO change:

Matt Webb has informed the Board of his decision to step down as Chief Financial Officer after five years in the role in order to pursue other opportunities.

He is thanked:

On behalf of the Board, I would like to thank Matt for his outstanding contribution to Luceco's progress over the last five years, a period in which the Group has evolved into a strategically focused, highly profitable and well capitalised business. As reported in today's trading update for 2022, he leaves the business in good shape and we wish him every success in his future career.

So clearly amicable and nothing to be worried about. The interesting part is that the replacement is a non-exec that steps back into an exec role:

…will be succeeded as Chief Financial Officer by Will Hoy, who currently serves as Audit Committee Chair and Non-Executive Director of the Company. Will Hoy will assume an Executive Director position from 1 March 2023 before becoming Chief Financial Officer on 1 April 2023, in order to effect an orderly handover.

These sorts of moves don’t always end well. The Chairman of Tekmar becoming CEO presaged a further collapse in the business. (Although to be fair, the seeds were sown and he was at least trying to step in and do something about it.) However, in Luceco’s case, he's a fairly big hitter:

Will held a number of senior finance roles in a career with GKN that spanned over 20 years, including three years as Chief Financial Officer of GKN Aerospace and nine years as Head of Corporate Finance in which he oversaw GKN plc's M&A activities. Prior to joining GKN, Will qualified as a Chartered Accountant at KPMG LLP and worked in its Corporate Finance department.

GKN Aerospace turned over £2.5b, according to Google, before being sold to Melrose. So he was the CFO of a much bigger business and has extensive M&A experience. It seems Luceco may have some big ambitions.

Capital Limited (CAPD.L) - FY 2022 Trading Update

This starts off well:

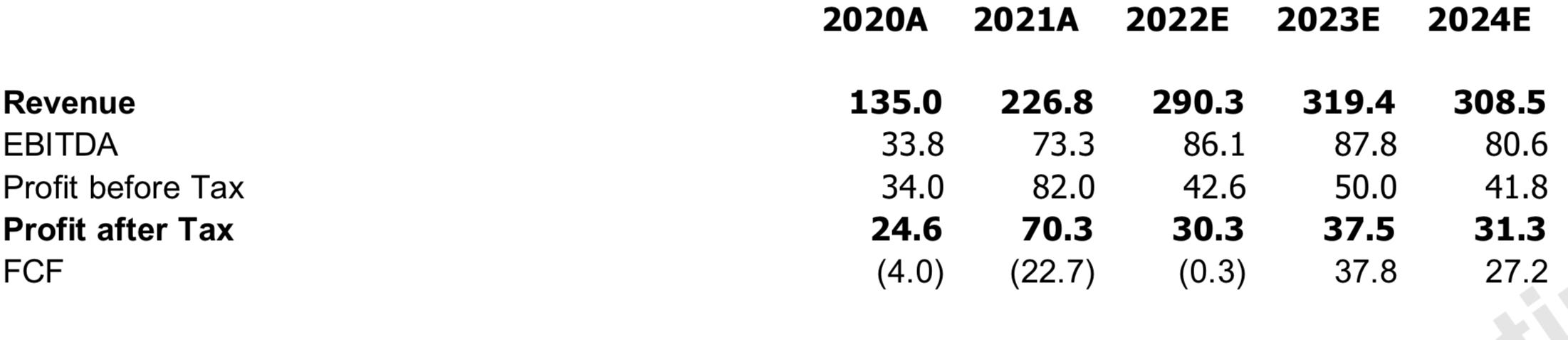

FY 2022 revenue of $290.3 million, up 28.0% on FY 2021 ($226.8 million), slightly ahead of the upper end of revised guidance of $280-290 million (up from $270-280 million guided at our FY21 results);

So a slight beat on Revenue. The utilisation is down a bit. However, this is due to adding two rigs in the quarter, and the rig moves to longer-term contracts carried over from Q3 into Q4:

This is the result of our active strategy to reposition the contract portfolio, as outlined at the H1 2022 results, reducing exposure to short-term exploration contracts, and focusing on large scale mine sites and Tier-1 projects with significant growth potential.

The only negative is the drop in the value of the listed portfolio, but we knew this already as equity markets for risk assets have been weak, even in an environment of rising gold prices:

The total value of investments (listed and unlisted) was US$38.7 million as of 31 December 2022, versus $47.3 million at 30 June 2022 and versus US$60.2 million at the end of 2021; The portfolio recorded investment losses (unrealised) of US$9.55 million in H2 2022;

They have still turned $12.5m into $38.7m so shareholders can’t have too many complaints.

When you have a cheap company, generating excellent results, the most important lines in an RNS are always the outlook, and here, this remains very strong:

· The Group continued to see strong demand across all its business units in Q4 2022 and gives the Group confidence to continue to invest in growth.

- The drilling business has a strong outlook entering 2023 with its highest rig count, robust utilisation and strong ARPOR;

- Tendering activity across all business units remains robust;

So no sign of the mining cycle showing any weakness. Perhaps the only disappointment is that they are still tendering in mining which we are not a big fan of from a capital allocation point of view. Still, their full-cycle ROCE is good, so the company has a history of very good capital allocation as a whole. And they won’t invest capital unless it’s going to 4-year+ inflation-proof contracts at this stage.

We also hear from the new CEO, Peter Stokes, for the first time:

It is clear Capital stands as a leader in its chosen fields, not only through the strength of its relationships and high-quality equipment but also through the focus on safety and push towards a highly nationalised workforce, something that really drew me to the company to begin with. Capital is certainly on an impressive growth trajectory and we are very optimistic about the year ahead.

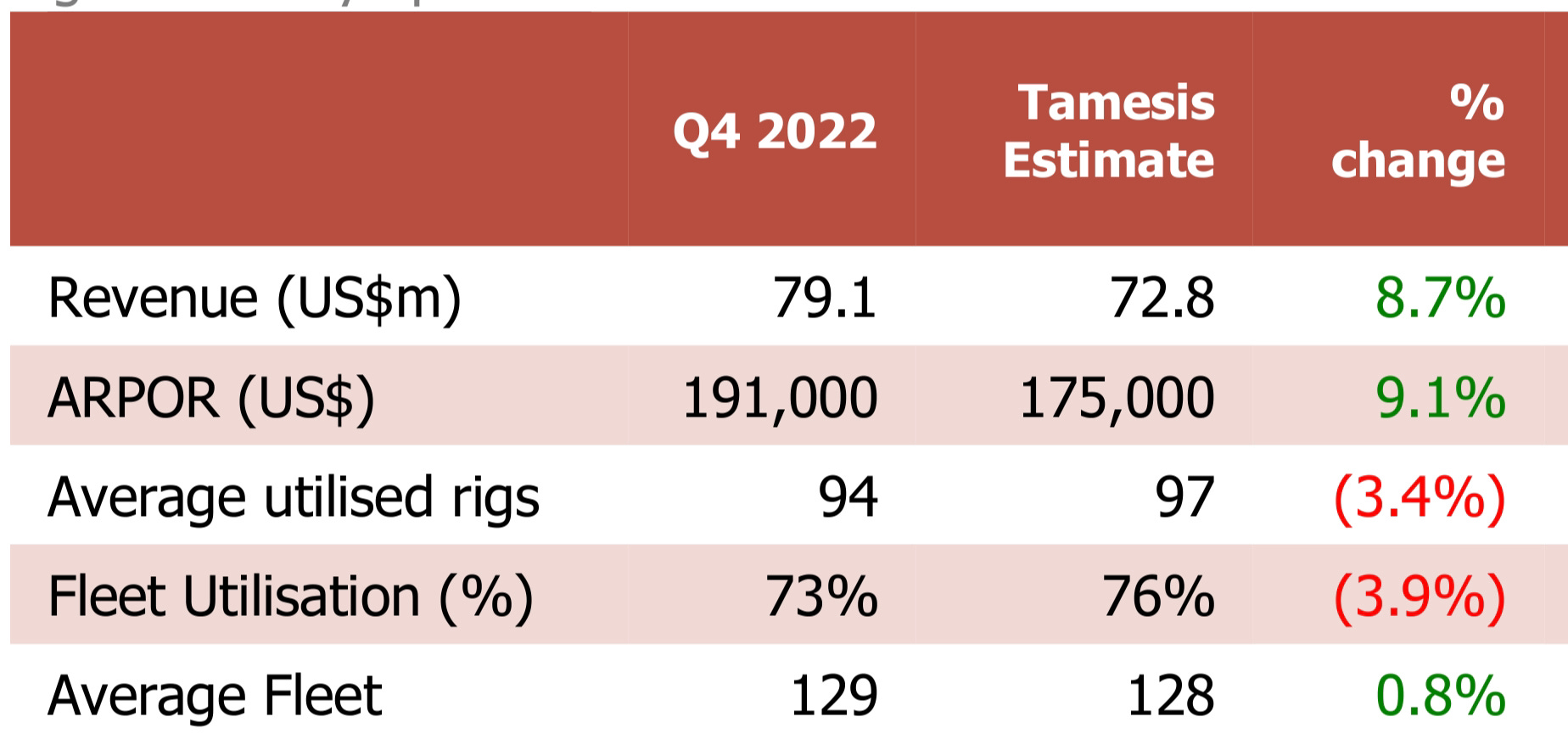

Broker, Tamesis has this as an 8.7% revenue beat for Q4:

Although Tamesis have always been a little behind the curve when it comes to revenue estimates. And these assumptions still look a bit light to Mark:

Their PAT includes portfolio gain/losses, which means it is largely meaningless for valuation purposes:

The company is starting to be more than a drilling company, with MSALABS showing continued growth:

• MSALABS now has four units commissioned across Africa and Canada, with three further units due to begin operations in Q1 2023, including Barrick's Kibali Gold Mine;

• Trials with major mining companies are continuing with PhotonAssay in high demand globally. The expanded relationship with Chrysos will see MSALABS deploy 21 units by 2025, giving the company a strong competitive position in the coming years;

The guidance for revenue for the year just gone from MSALABS is around $30m, which from four newly commissioned Chrysos units and their existing fire assay business makes their 2025 estimate of $80m revenue from 21 Chrysos units look very conservative. Of course, the first units will go where they get maximum utilisation. But still, it is easy to see a route to $100m+ revenue here. With 25-30% EBITDA margin, their 75% stake in this business could represent a significant part of the current market cap.

Anyway, in summary have yet another beat, pretty significant on a quarterly basis, confirmation of further imminent progress at MSLABS and an upbeat outlook statement.

Despite this, the initial share price increase in response to this positive statement was met with selling. Partly this reflects that the share price had been strong in the run up to this trading statement and investors were “buying the rumour and selling the fact.”

It goes to show that the company’s shares are still pretty illiquid. It seems a few smaller investors may have been overweight and would be sellers at any price on the day. If this is the case, then it is easy to see why the share would be volatile. However, those sellers may come to regret it, since this remains one of the cheapest shares on the market with excellent short and medium-term business momentum.

Appreciate (APP.L) - FCA Approval & Timetable

We highlighted this as a takeover arb opportunity recently, with the shares trading below 40p and an offer worth about an 8% premium. We expected the deal to complete, and shareholders to get paid much sooner than the June date previously guided.

This week one of the final hurdles is passed as the deal gets FCA approval, and now the timetable is given as:

It is expected that the Acquisition will become Effective on or before 31 March 2023

There is still the shareholder vote and court approval. But given the presence of a large arb position from Samson Rock, we expect this to be a formality.

Gear4music(G4M.L) - Trading Update

In-line from this music equipment retailer:

FY23 EBITDA and net debt reduction in-line with consensus market expectations

However, this was not well received. Investors were presumably hoping for a beat.

Progressive covers this one and says:

We leave our forecasts unchanged, with our key revenue, EBITDA and PBT figures for FY23E in line with consensus market expectations. The shape of delivering these profit figures will likely differ slightly from our full model, with a lower gross margin percentage delivering a lower gross profit figure, offset by lower operating costs.

Although they would have perhaps done better since they met expectations despite a headwind. When the headwind is removed, things should improve.

UK revenues during December were impacted by Royal Mail strikes and the knock-on disruption of other couriers, which led to longer delivery times and an earlier pre-Christmas cut-off date than we would expect under normal trading conditions.

This seems like an amazing fall from grace, considering it was over 1000p a year and a bit ago. We doubt they really have much of a moat as a business, so they were simply lucky rather than good. Debt and payables now seem significant relative to market cap as they have had to hold more inventory, making them risky too.

Given that debt, they still look very expensive, with a debt-adjusted P/E of around 60, dropping to 20 if they hit the next year’s forecasts in a highly uncertain environment. In this context, in line isn’t good enough. Too high for a weak-moat business. Focusrite remains cheaper and a much better quality company with the same market exposure if investors like the sector.

There are signs that the sector may be facing headwinds, as Focusrite CEO, Tim Carroll sells over £100k worth of shares in the market for “financial planning”. It makes sense not to be overly exposed to his employer, but it still looks like he’s calling the peak of the share price in the short to medium term.

Smartspace Software (SMRT.L) - Change of Auditor and Trading Update

The trading update simply says in-line. However, it is always worrying when a company change their auditors to someone you’ve never heard of, a fortnight before the financial year-end. This is a strange time to change auditors, and shareholders voted to reappoint RSM in July.

Realistically, this is likely to be a cost-cutting move, as they try to get to a profitable business without having to raise more cash from the market. However, this might backfire; at the moment, a cheap auditor appears to be a recipe for getting suspended for failing to produce accounts on time!

Mpac (MPAC.L) - Full Year Trading Update

The trading update says that they are in line with expectations. Although, these were cut very significantly for 2022 & 2023 in the middle of last year:

They say:

Order intake in H2 22 was significantly above H1 22

And that they are:

well placed and with an encouraging outlook as we enter FY 23.

However, the order book itself is lower:

The Group ended 2022 with a closing order book of circa £69.0m (December 2021: £78.4m)

Which they fail to explain. Perhaps more worryingly, they now talk about net debt at the year-end, whereas at the half-year, they said:

Net cash at 30 June 2022 was £9.5m

That’s quite some cash burn in six months. On this, they say:

The Group's balance sheet continues to be strong, and these increased levels of working capital are anticipated to largely unwind during H1 23.

Broker, Equity Development have materially upgraded EBITDA for the current year and the year just completed. However, in another hard-to-explain move, the forecast cash swing is from £11.6m cash to £4.2m debt, i.e. £15.8m. It beggars belief that £15.8m could have gone into inventories which were already elevated at £6.3 at the end of H1. That would be £15.8m negative cashflow on £44.6m of revenue (since they did £50.6m revenue in H1 and have said they are in line with the £95.2m forecast.)

They received a cash up-front payment for the FREYR QCP contract, with maybe 15-25% left to receive, which we don't think they would have expected by year-end anyway. So presumably, they recognised other large sales in December.

So, we have the risk of inappropriate recognition of work-in-progress on the FREYR QCP (or worse, on the main plant) and a massive inventory build, or we have maybe £16m of December sales gone into receivables plus a £2.8m inventory build. This would mean that Days Sales Receivables have gone from 130 days to 190 days. They are taking half a year on average to be paid, which is clearly a red flag for revenue recognition.

Broker Shore have some more details and say:

Given the organic development of the Group across all segments, we also note that contract assets (receivables) have extended to the year end. This has pulled in working capital and we now anticipate Mpac ending FY22F with a net debt position (ex-leases) of c.£4.0m (£10.1m net debt post leases compared to previously net cash of £5.3m). We expect a significant proportion of this capital to collected through the current H1 period and we note that debt levels remain minimal at Mpac.

So we think the implication is that they have multiple open contracts where they have recognised revenue into contract assets. But there have to be some serious questions over revenue recognition here, and we expect the auditors to take a very close look at this unless these contract assets have been invoiced and paid in cash before the audit date. Let’s face it, the management here has a habit of trying to ignore anything bad happening with their repeated use of highly-adjusted figures.

In addition to the working capital red flag, the debt situation and the FREYR delays, the following sentence in the Shore note made us think that there is also a risk of an equity raise:

We note that the clean energy segment will require further resourcing as orders build and we will consider the need here, as required, separately

The market seems to have missed these concerning development, with the shares actually rising on the day of this statement. Leo decided that the risk here has massively increased and took advantage of those who bid it up to sell out. He gives a full rationale on his blog here. Anyone investing here until we see audited accounts is taking a big gamble, in our opinion.

Kenmare Resources (KMR.L) - Q4 Prodution Report

Kenmare warned on production in November and production here is now in line with that revised forecast:

Ilmenite production decreased 3% in 2022 to 1,088,300 tonnes (2021: 1,119,400 tonnes)

This was due to power issues in Q4 and they seem to be cautious as their 2023 production guidance is in line with the reduced 2022, so perhaps they are anticipating continued power issues:

2023 ilmenite production guidance range of 1,050,000 to 1,150,000 tonnes

Cash flow has been excellent, though:

Kenmare has moved to a net cash position of $27.5 million at the end of 2022, which represents a $110.3 million improvement from the previous year, whilst also having paid record dividends. We continue to target a total dividend payment of 25% of profit after tax in respect of 2022.

They have been saved by high commodity prices:

Despite these factors impacting the market, Kenmare continued to see robust demand for its high-quality ilmenite products, achieving a ninth consecutive ilmenite price increase in Q4 2022 as customers continue to value supply security.

These are looking a little weaker for 23Q1, but still high by historical standards. And the company remains fundamentally cheap:

Perhaps the only argument against holding Kenmare is that competitor Base Resources looks cheaper. Base will equally benefit from the high near term Heavy Mineral Sand pricing, even more so given its short Life of Mine. From the three-month chart you would assume it was Base that missed production guidance rather than Kenmare, rather then the other way round:

Base should report their quarterly production figures, with prices achieved by the end of the month.

Character (CCT.L) - Trading update ahead of the AGM

When we discussed Character’s annual results to 31st August in December, we thought the outlook sounded like a profits warning, and were surprised that the shares didn’t sell off on the news and said:

Stockopedia consensus has the EPS halving to 22p this year, so this doesn't look cheap even after adjusting for a quarter of the market cap in cash. At least on this year’s earnings. There doesn’t seem to have been any further broker downgrade in response to this statement, though. However, this outlook statement does seem weak compared to the October note that forecasted the 22p.

This week the real profits warning arrived:

Despite the tough and challenging start to the current financial year, the Board remains optimistic that the anticipated rebound will come through strongly in the second half. Accordingly, the Company shall be profitable for the financial year as a whole, however, sales and profit before tax (before highlighted items) are expected to be marginally below current market expectations.

Marginally below doesn’t seem too bad. And again the share price reaction has been muted, down only 12% on this news. However, this doesn’t seem to reflect that they were on a 14x forward P/E even adjusting for the cash pile, on earnings estimates that have proven too optimistic and, even then, relies on a big rebound in consumer sentiment happening before 31st August.

They say profit warnings come in threes, so they appear to be saving up the third one for later in the year.

Maintel (MAI.L) - Trading Update

A trading update mid-afternoon is rarely good news, and indeed, it wasn’t for Maintel.

Group Revenue for the second half of FY22 is expected to be broadly in line with the first half of FY22, delivering approximately £91m of revenue for FY22.

Broadly, of course meaning slightly below. This is the main issue, however:

However, Adjusted EBITDA* has been negatively affected especially in the 4th Quarter, with Adjusted EBITDA for the year set to be above £4m, due to unexpected inflation costs on 3rd party vendor suppliers, professional services margin reduction due to project delays whilst having to maintain the associated cost base, increased office service costs and lower gross margin on technology sales.

The initial 30% drop in share price may have looked extreme until investors read on:

"In light of the disappointing second half EBITDA, the management team is in constructive conversations with its principal banking partner whilst implementing a program of revenue maximisation and process efficiency measures which not only recover Gross Margin performance after the economic headwinds of FY22, but also generate much improved EBITDA and cash generation which will recover to at least recent historical levels."

They say that debt has fallen:

The Company remained cash generative in the period and has reduced its net cash debt** position from £19.4m as at 31 December 2021 to £16.7m as at 31 December 2022, outperforming our expectations, despite Adjusted* EBITDA being below expected levels.

However, discussions with lenders suggest that they will breach covenants

Broker finnCap have had forecasts under review for some time, but in September said:

Interims to June 2022 delivered EBITDA of £3.6m (1H21: £4.3m) from revenue of £46.7m (£53.5m), with performance restrained by the continuing challenges of hardware availability, and with delayed contracts representing postponed revenue of £6m in the period.

So it seems that they have the same problem as Mpac, but in Maintel's case it is clear-cut that they don’t have the revenue recognition flexibility.

Looking at the H1 results statement, it looks like this is also network installation work that is delayed. If they have done cable installation work on site then at least the customer has control of it and it is a pity it can't be recognised for accounting purposes and if I were a bank I'd be tolerant of resulting covenant breaches if I was confident the contracts were secure. And at some point the business should turnaround and generate 20p EPS again.

This makes the fall tempting to buy, until you read the balance sheet:

On top of the long-term debt, Current liabilities significantly exceed Current assets. Companies can successfully trade with negative working capital for many years, until they have a downturn in sales. The combination of large payables and net debt means that the company isn’t well set up to weather any drops in revenue or delays in billing customers.

And when the fundamental problem for completing work and billing clients is component supply, delaying paying suppliers because you are not being paid by customers is not a great way to be prioritised for scarce components. The only way out of this hole may be an equity raise.

National World (NWOR.L) - Pre close trading update

This has been a busy period for National World, who tried to takeover much bigger listed competitor Reach. This may have been a lucky escape, as Reach subsequently warned on profits. No such issues here however:

§ FY22 be revenue expected to be not less than £84.0 million

§ FY22 Adjusted EBITDA* expected to be not less than £9.4 million

§ Strong balance sheet with a cash balance of £27.0 million held as at 31 December 2022

Adj. EBITDA is of course largely meaningless. However, generating £6.5m Free Cash Flow on a £20m Enetrprise Value is meaningful. Their intention to start paying a dividend is nice too. The share price has risen and given the effect of the large cash balance, the EV is now closer to £30m. So perhaps some of the easy gains have been had. Still this is a modestly-priced business that is trading well, and appears to be much better run than Reach.

Quiz (QUIZ.L) - Trading Update

Quiz had a decent Decmber for trading:

The Group is pleased with the gross margins generated during the Period which are consistent with those generated in the same period in 2019, prior to the impact of COVID-19.

2020 Gross Margins were 60% so pretty decent. So is cash balance:

As at 16 January 2023, the Group had total liquidity headroom of £12.7 million, being a cash balance of £9.2 million and £3.5 million of undrawn bank facilities (31 March 2022: £6.5 million, being cash net of borrowings of £4.4 million and £2.1 million of unutilised bank facilities).

The Group's £3.5m of bank facilities available will expire in June 2023. There are no financial covenants applicable to these facilities.

And least in line on the outlook is positive:

The Board is encouraged by the positive performance delivered during the Period which again highlights the strength and awareness of the QUIZ brand and growing customer demand for its trademark dressy and occasionwear offering. However, the Board recognises that current macroeconomic pressures may impact consumer demand across the sector. Notwithstanding this, the Board remains confident it will deliver profits for the full year to 31 March 2023 at least in line with its expectations and is well positioned to achieve further profitable revenue growth in the longer term.

In line is a P/E of 10:

Which seems low given that half the market cap is in cash (at a seasonal high, of course), and a lack of dividend suggests thatthey are not yet confident that they are consistently cash flow positive and have excess capital. This lack of any dividend and the history of clutching defeat from the jaws of victory perhaps weigh heavily on investors and the initial excitement appears to have been sold into, but perhaps reflects that it had already bounced strongly in January:

That chart says buy at 14p, average down if it reaches 12p to Mark, but then he is a terrible chartist (although that makes him no different to all other chartists!)

Revolution Bars (RBG.L) - H1 Trading Update

Another profits warning from this perma-under-performer:

our walk-in revenue was lower than in previous years, with a consequential impact on Group sales. Group LFLs for the Christmas Trading Period, when compared to the same period in 2019, the last Christmas period not affected by Covid 19, were (9.0)%.

The Board have now concluded that the IAS 17 EBITDA outturn for the year, including rental costs, is likely to be lower than previously guided and is estimated to be at the bottom end of the range of market expectations, of £6.7-10.5m.

Rail strikes of course don't help, but I think it is the nature of the venues which seem to work well for organised events such as Christmas parties, but not for walk-ins. This is underlined by the fact their acquisition did fine with walk-ins.

Pleasingly, over the Christmas Trading Period, our recently acquired, Peach Pubs business continued its strong performance delivering LFLs over the same period with revenues increasing 7.5% compared to 2021 and 10.1% compared to 2019 clearly demonstrating the additional resilience and diversity that Peach Pubs has brought to the Group since its acquisition in October 2022.

So to put it another way, their core business remains broken. in light of this, the share price reaction of down just 20% to 6p looks like an under-reaction, although it is an all time low.

Their broker finnCap say:

At end December, net bank debt was £18.5m, which includes the £17.5m acquisition of Peach Pubs. We expect net debt to rise to £23.1m for FY23E. Forecast FY23E net debt/EBITDA peaks at 3.5x and then declines to 2.7x for FY25E on new forecasts.

Not only does 3.5x EBITDA look very risky, the target price is not only massively cut and below the last fundraise price, but looks unsupportable by fundamentals:

Our new target price of 15p (was 36p) is based on c.10.0x EV/EBITDA and 6.1% FCF yield (Adj.) for FY24E.

So the target price is not only massively cut and below the last fundraise price, but is blatantly unsupportable. However, with an apparently unlimited supply of virtually free money from shareholders, banks and landlords, we find it difficult so see how they could go bust.

Tekmar Group PLC - Update on Formal Sale and Strategic Review Process

Tl;dr: nobody wants them.

Tekmar bounced strongly in January up to around 17p on various bits of contract news, revealing that at least a few people expect them to still be around in a few years time. Still these didn’t fix the fundamental issues with the business and they remained for sale. However, no offers appeared.

Instead, they keep extending exclusivity period with a “global institutional investor in the energy sector”. So this sounds like a fund not an industry player. Who will no doubt want 29.9% of the equity at a favourable price in return for the debt funding. This week we find out that this:

would represent new capital investment, at or around the share price at the time exclusivity was granted in November 2022

So this means about 8p/share. Investors missed this important bit early on and the shares were slow to sell off on this news, giving the savvy the opportunity to exit. The price remains significantly above this level now so perhaps it is still not too late for the tardy.

In reality, they probably would have been better off having a big rights issue months ago rather than engaging in a pointless Formal Sale Process.

That’s it for this week, have a great weekend!