Small Caps Live Weekly Summary

CAPD CARD FDEV G4M JSE TUNE NWOR NXQ PMP WRKS WOSG ZTF

The sheer volume of trading statements and results announcements this week was hard to keep up with, so many of these are an executive summary. Still, it feels better to be getting news flow rather than share prices moving randomly on tips or share overhangs.

Capital Limited (CAPD.L) - Q4 Trading Update

Q4 trading has recovered somewhat from a weak Q3:

However, it isn’t enough to meet revenue expectations:

FY 2023 revenue of $318.4 million, up 9.7% on FY 2022 ($290.3 million), marginally below guidance of $320-340 million

The reasons given for the drilling weakness are Persus not restarting yet in Sudan, which always looked optimistic to us, and “subdued activity in Mali”, which we would have liked a bit more detail on.

Regular contributor Jeff had pointed out that the MSALABS rollout of Chrysos looked a little behind schedule, so kudos to him for spotting the third factor for the weaker revenue than expected. We have some sympathy with Chrysos being a pretty lumpy rollout, though and that this remains a rapid growth area for the company.

There is good news on the drilling side with Sukari renewed for a further five years, more rigs in Ivindo, an extra contract with Perseus, and the Nevada deal that has already been announced.

Broker Tamesis don't seem to have updated their block model, but they do say:

The shares are trading on 2024 PE and EV/EBITDA multiples of 6.8x and 2.6x respectively with a dividend yield of 3.4%. Not sure there are that many companies, certainly in the industry, generating 33% CAGR in revenue and paying a decent dividend.

And their note also contains this interesting snippet:

Meanwhile the sector consolidates (it was a hard year generally for drilling contractors) thereby improving potential industry returns and the economic rent of those operating within it. After DDH1 was taken over by Perenti the no.1 drilling company in the sector, Boart Longyear, is to be taken private by a consortium of Private Equity investors.

So, it is hard to be too pessimistic despite the slight miss in revenue for 2023.

Card Factory (CARD.L) - Trading Update

Stores doing well, but online struggling:

Store revenue grew +8.2% on a Like-For-Like1 (LFL) basis…

Online LFL sales of -12.8% for the 11 months to 31 December, an improvement from the half year driven by positive performance in cardfactory.co.uk (YTD +0.2%), reflecting the ongoing investment in online capability, platform performance and customer experience.

But overall, leading to:

Given the strength of performance in the year to date, the Board expects to deliver full year adjusted profit before tax (excluding one off items) at the top of the range of market expectations…

That range is given as:

current range of market expectations for FY24 adjusted profit before tax is £58.4 million to £62.0 million

So, top end, say £61m? That would be £45.8m PAT with a standard tax charge, slightly lower than Stockopedia consensus. But there must be assumptions of a lower tax rate in there, as the consensus went up slightly after this trading update. There’s no mention of net debt or working capital, which really matters to the valuation here. But this is a Christmas trading update not end of year, which is obviously chosen to be a seasonal low point for working capital.

The fact that the share price fell on this statement probably reflects that this is one of the most promoted stocks rather than any fundamental issues with this trading update. A debt-adjusted P/E of 9 is undemanding. However, As a new investor to the stock you’d really want to see that balance sheet before making an investment.

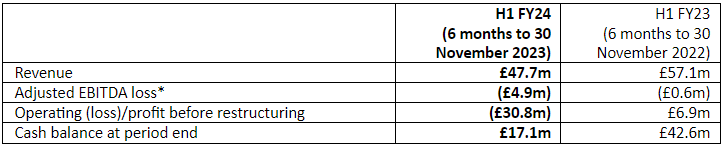

Frontier Development (FDEV.L) - Interim Results

We knew earnings would be terrible, and they are:

So terrible that it is all eyes on that balance sheet. Recent cash is not provided in the outlook statement but in a separate section:

Cash balance of £17.1 million at 30 November 2023 (31 May 2023: £28.3 million). Microsoft Game Pass subscription fees for F1® Manager 2023 and Jurassic World Evolution 2 were received in December 2023, with cash at 31 December 2023 growing to £19.9 million. Cash from the sales recorded in December will be received from platform and channel partners in January and February.

But are they still "well capitalised"? Well, they do (did) have £5.4m of PP&E in addition to that cash. From the annual report:

Property, plant and equipment relate mainly to IT equipment and the fit-out of the leased studio facility, which the Group has occupied from April 2018

In our view, the leasehold improvements have no realisable or security value, and the computer equipment is more of a liability due to the costs of keeping it refreshed. Maybe they could defer maintenance capex for 6 months or so, but this would be a great way of annoying employees. They also have £19m of lease liabilities. Although these are covenant-free, this financial liability is not dissimilar to debt.

Receivables are ahead of payables and have been covered in the cash commentary, but there are £4m of provisions and deferred income. It is hard to see anybody lending them unsecured debt while they are loss-making and with the obvious levers leading to cash outflow ahead of accounting profits. If they run out of cash, then they may need to issue equity.

Frontier has confirmed three future CMS games with one releasing in each of the next three financial years - FY25, FY26 and FY27. This looks like a big gap! On the positive side, there are some console conversions coming through this year, and borrowing against the significant receivables should be possible. They may just squeeze through, but it will be by the skin of their teeth.

Gear4music (G4M.L) - Trading Update

We were expecting a miss here, which on a forward P/E of 35 with significant net debt would have been disastrous. However:

Revenues reflect previously announced FY24 prioritisation of gross margins ahead of sales growth…

FY24 EBITDA and net debt reduction in-line with consensus market expectations

They make it sound like this is a revenue miss. But profitability is what really matters, and the debt reduction implies they have not been left with excess stock. They appear to have really grasped the nettle of cost-cutting to hit expectations. Which is certainly good news short term. We guess we’ll see long term if they have cut away muscle as well as fat. It’s hard to justify the current price, let alone an economic return, without making some pretty heroic assumptions about years outside the normal forecast periods.

Focusrite (TUNE.L) - AGM Statement

The market hasn’t liked this update, and we can see why:

According to industry data our performance overall, whilst subdued, has been better than our competitors.

Being better than competitors is little salve when performance is lacklustre. They say:

As a result, our profit expectations for the full year remain unchanged, although with a significant weighting towards the second half, a period which is expected to include a number of new product launches. (emphasis added)

The risk of a miss must be high here, with a “significant” H2 weighting and relying on the uncertain impact of new product launches. But even if you share their confidence in the full year, why buy ahead of interims that we know will be terrible?

Jadestone Energy (JSE.L) - 2024 Guidance & Corporate Update

At first glance, everything is ahead of expectations, so it seemed a bit strange for the share price to fall 25% this week:

· 2023 production is estimated to have averaged c.13,800 boe/d, just above the top end of the implied annual 2023 guidance range of 12,600-13,700 boe/d, driven by strong performance from PM323 (Malaysia) and Montara into year-end…

· Net debt at 31 December 2023 estimated at c.US$5 million, based on estimated year-end cash balances of c.US$152 million and debt drawn of US$157 million. The end-2023 net debt position benefitted from timing of liftings and optimisation of working capital into the year-end.

· Akatara development project on track, with the gas processing plant c.92% complete and construction of the sales gas pipeline c.91% complete.

· The excellent results of the 2023 PM323 infill drilling campaign in Malaysia are expected to deliver strong production growth and reserve additions, with the four new wells currently producing at a combined gross rate of c.7,000 bbls/d.

But here is the sting in the tail:

Montara operating costs in 2024 are currently estimated at c.US$120 million and are included in the overall 2024 corporate operating cost guidance above. Going forward, operating costs at Montara are expected to average c.US$95 million per annum for several years with production now expected to cease in 2030.

Stag operating costs in 2024 are currently estimated at c.US$70 million. Going forward, longer-term operating costs at Stag are expected to be c.US$60 million per annum with no significant change to end of field life, which is now expected in 2035.

Montara causing problems again! However, it is worth noting that amongst all the doom and gloom, EPS consensus for 2024 appears to have actually risen by 50% on this update to 14c:

(Although a long way down from where they were expected to be 18 months ago.) It seems investors simply don’t believe the broker on this one.

National World (NWOR.L) - Trading Update

Like Nexteq, this is another company where the market was pricing in a miss, but the company managed to beat expectations instead:

FY23 Adjusted EBITDA* to exceed £9.0 million and will be above expectation

However, they presumably want us to ignore the substantial acquisition & restructuring costs that are really part of their business model:

Targeted annualised cost savings of £6.0 million were achieved. Non-recurring costs for the period were £5.5 million including £3.9 million restructuring costs and £1.6 million incurred on advisory costs for completed and potential acquisitions.

This seems like the most important bit of the update:

The Group maintains a strong financial position with a cash balance of £10.7 million at the year end, after paying £13.0 million consideration for the acquisitions completed in the period, (net of cash acquired) repayment of the final tranche of the £2.5 million deferred consideration payable as a result of acquiring JPIMedia Publishing Limited and its subsidiaries and repayment of £1.0 million of loan notes, making the Group debt free.

So that’s cash generated of £7.2m despite £5.5m of “exceptional” costs. If they stopped acquiring, they would throw off a lot of cash.

Forward guidance is:

For 2024, we expect to deliver revenues in excess of £100 million and improved EBITDA margin.

So, growth in both revenue & margins into 2024.

Understandably, the shares rose in response to this news, but the share price is still 25% down from a year ago, despite a broker trend looking like this:

With a growing business on 2024 P/E of less than 6 and significant net cash, this still looks like good value.

Nexteq (NXQ.L) - Trading Update

When reviewing the forecasts prior to this update, we were expecting revenue to be achievable, but EPS forecasts would be a stretch. After all, in July last year, they issued a trading statement that said:

The improved operating margins seen in the first half of the year are expected to result in full year adjusted profit before tax in line with market expectations. This is notwithstanding revenues which are now expected to be broadly in line with the previous year, as customers unwind their stock positions and management continues to focus on higher quality revenue.

This caused the share price to fall from around £1.60 share to bottom around 95p. So it is very pleasing to see this week’s trading statement say:

The Group continues to make good strategic progress and the Board is pleased to announce that it expects to report full year adjusted profit before tax comfortably ahead of market expectations.

Brokers had maintained their forecasts for this period before upgrading in response to this trading update:

2024 numbers are upgraded, too, and the company trades on a P/E of around 9. That alone would make it look like good value, but on top of that, we have around a quarter of the market cap in cash:

Net cash at 31 December 2023 increased substantially to $27.9m from $18.5m at 30 June 2023

The increase is partly due to retained profits but also due to a favourable working capital position:

…increased profitability enhanced by improved cash from operations and positive working capital movements as the Group reduced overall stock levels.

Broker Cavendish doesn’t see this as anomalous, though, as they forecast net cash will be $35m at the end of 2024 after paying $2.8m out in dividends.

By way of comparison, Concurrent Technologies, who issued a trading update on the same day indicating that they were trading slightly ahead of their expectations, are on a forward EV/EBIT of 13.3 vs just 4.3 for Nexteq. In general, we consider Nexteq management better and more trustworthy than Concurrent Technologies, so this valuation looks anomalous on many levels.

Portmeirion (PMP.L) - FY23 Trading Update

We are pleased to report a good Christmas trading period with robust demand across our portfolio of consumer goods brands. As a result, FY23 sales are now expected to be at least £102 million, marginally ahead of consensus market expectations. This is 10% above pre-Covid 2019 levels but lower than FY22's record results as anticipated. We expect FY23 profit before taxation to be in line with underlying consensus market expectations.

Sales ahead and profits in line, so why did the share price take a bath? Well, we knew 2023 was a write-off, so it’s got to be the outlook:

Following a positive Christmas performance, we expect sales to return to growth in 2024 YOY alongside a healthy operating margin improvement compared to 2023. However, we expect 2024 to be a challenging year due to ongoing macro uncertainty with customers remaining cautious in relation to H1 order flow, in particular in the US and Korean markets. In addition, we expect to continue to incur higher interest costs during the year given current rates.

So not great, but we don’t think you’d guess from this that Shore has taken a whopping 36%/28% out of FY24/25 EPS. On this basis, the drop seems light. This is another one where the Santa rally has hit economic reality.

If they do hit broker forecasts, then this looks cheap again, but only because they use heavily adjusted figures. Investors need to do their own work to add back in exceptional restructuring costs that are anything but exceptional and the pension recovery and admin costs. The impact is around 8p per share on EPS. So the “real” adjusted adjusted FY 2024 EPS is now around 17p. And if they do 33p in 2025, which was previously broker forecast for FY 2024, that gives 25p adj EPS, discount back 20% and apply a PE of 10, and fair value is around 200p.

The Works (WRKS.L) - Interim Results & Christmas Trading

The results are loss-making, but they always are in H1:

There’s a big gap between statutory and adjusted loss, but this is entirely due to non-cash write-downs. It looks like they are setting us up for a sales miss for H2, though:

Overall, LFL sales declined by 4.9% in the 11 weeks ended Sunday, 14 January 2024. This was lower than anticipated and was primarily a result of the challenging consumer environment and subdued demand over the festive period.

They say they will be debt-free at year-end but this excludes lease liabilities, many of which are onerous, with lease liabilities exceeding lease assets by over £30m, and they obviously pick a good point for working capital as their year-end:

We entered the new calendar year with stock levels in line with our original plans, having taken action to reduce planned intake and with seasonal stock selling through as expected. Our cash position improved following Christmas, with £18.4m of cash as of 14 January 2024 and we expect to end the financial year debt-free.

They have been making cost savings and claim that the last few weeks have been on a more positive sales trajectory, leading to:

Given the more positive sales trajectory in recent weeks, coupled with expected benefits from cost action and new ranges, the Board's expectation for FY24 pre IFRS 16 Adjusted EBITDA of approximately £6.0m currently remains unchanged.

But with a current ratio of 0.8, low even for a retailer, why take the risk that they manage to pull a rabbit out of the hat?

Watches of Switzerland (WOSG.L) - Trading Update

Many companies this week have been missing on revenue but beating on PBT, as they have mostly been slashing costs. Not so for Watches of Switzerland, who have managed to warn on revenue, margin, interest, cash conversion and tax in the same update:

It is unsurprising, then, that the shares dropped 37% on the day. The blame was put on weakness in the UK. Mere mortals don’t have access to brokers' notes, so we are flying a bit blind here. A rough estimate suggests that EPS should now be between 30-35p versus a previous consensus that appears to be around 51p. Historically, they have had a decent ROCE and have grown the top line, and investors have been willing to pay up for that. They are still investing capex in new stores, such as the new Rolex megastore on Bond Street. But the ROCE isn’t going to look that great going forward, which makes paying 12x earnings or so not necessarily good value. And while luxury watch prices were rising, then it made sense for buyers to treat them like an asset, take 0% finance and get their names on waiting lists. With higher interest rates and prices perhaps beginning to fall, it is hard to know if this is a blip or the start of a longer-term reversion to the mean. Overall, this appears to be in the too-hard category for us.

Zotefoams (ZTF.L) - Trading Update

A mixed bag here. Revenue in line and profits ahead:

Consistent with the Group's update of 7 November 2023, the Group expects to report full year revenue in line with current market expectations and similar to the previous year at £127.0m (2022: £127.4m).

Adjusted profit before tax for the year is expected to be £13.1m (2022: £12.5m), which is a Group record and approximately 5% ahead of current market expectations

Driven by higher margin HPP sales being a greater part of the product mix:

· 7% growth in High Performance Product (HPP) sales to £58.2m (2022: £54.5m)

· 4% decline in AZOTE® polyolefin sales to £67.5m (2022: £70.1m)

· 57% decline in MEL sales to £1.2m (2022: £2.8m), with most of the business unit resources focusing on the development of ReZorce mono-material packaging.

So, the overall picture is encouraging, but the decline in MuCell sales is particularly worrying. This is meant to be their next big product, but it has been permanently loss-making, increasingly so as their broker, Singer, says:

Ahead of commercial trials in 2024, further investment in ReZorce (fully recyclable & circular barrier packaging for beverage cartons) has led to a £4.1m loss which is consistent with our modelling.

This has always been a very capital-intensive business (we’ve commented before about how rarely it is that they can manage to generate a return on capital above their cost of capital, and hence, so far, have destroyed shareholder value as a listed business). It appears it remains capital-intensive going forward:

In response to increasing opportunities in the region, the Group has committed to further development of its USA foam manufacturing site in Kentucky, with investment in a second low-pressure autoclave and increased warehouse space. This reflects a significant capital investment of approximately £10m, will be funded from existing cash resources and is expected to be completed around mid-2025.

Debt forecasts have been increased by £7m to fund growth in production equipment and warehousing, with no extra revenue to show out until at least December 2025. Nor is this bringing forward planned investment since cash remains £7m lower than previously forecast in FY 2025. This simply appears to be an expenditure which was always required but not previously budgeted for, or communicated to brokers.

By paying 17x forward earnings for a capital-intensive business with significant debt, shareholders are betting heavily on the unproven ReZorce product becoming a commercial success very soon. We are less sure.

That’s it for this week. Have a great weekend!